Staple Pins Market Size

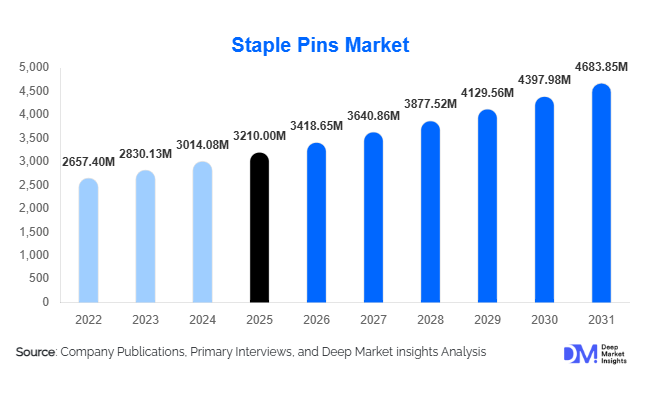

According to Deep Market Insights, the global staple pins market size was valued at USD 3,210 million in 2025 and is projected to grow from USD 3,418.65 million in 2026 to reach USD 4,683.85 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). Market growth is primarily driven by stable institutional demand from offices and educational institutions, rising global packaging activities, and expanding industrial applications such as furniture manufacturing and light construction fastening solutions. Despite gradual digitization trends reducing paper usage in developed economies, staple pins remain an essential consumable due to compliance-driven documentation, logistics paperwork, and cost-effective fastening requirements across industries.

Key Market Insights

- Packaging and logistics expansion is emerging as a major growth catalyst, increasing demand for heavy-duty and industrial staple pins globally.

- Asia-Pacific dominates global consumption, supported by strong manufacturing ecosystems and growing institutional infrastructure.

- Institutional procurement continues to stabilize demand, particularly across education, government, and healthcare sectors.

- Galvanized and corrosion-resistant staples are gaining popularity due to durability and long-term storage requirements.

- E-commerce growth is reshaping bulk purchasing patterns, driving higher demand through B2B and wholesale distribution channels.

- Automation-compatible stapling systems are encouraging technological upgrades in staple manufacturing and product design.

What are the latest trends in the staple pins market?

Shift Toward Industrial and Packaging Applications

The staple pins market is gradually transitioning beyond traditional office usage toward industrial fastening and packaging applications. Growth in global e-commerce and logistics infrastructure has significantly increased the consumption of heavy-duty staples used in corrugated packaging, labeling, and warehouse documentation processes. Manufacturers are developing stronger, precision-engineered staples compatible with pneumatic and electric staplers to cater to automated environments. Industrial diversification is improving profitability margins as industrial staples command higher pricing compared to standard office variants.

Sustainable Material Adoption and Product Innovation

Environmental considerations are influencing procurement decisions across corporate and public institutions. Manufacturers are increasingly introducing recyclable packaging, reduced-metal designs, and corrosion-resistant coatings to meet sustainability requirements. Governments and organizations are prioritizing environmentally responsible office supplies, encouraging producers to adopt recycled steel inputs and energy-efficient manufacturing processes. Eco-certified products are becoming a key differentiation factor, particularly in Europe and North America where sustainability regulations are stronger.

What are the key drivers in the staple pins market?

Expansion of Global Logistics and Packaging Industry

The rapid growth of global trade and e-commerce fulfillment networks has increased the need for reliable fastening solutions in warehouses and packaging facilities. Staple pins are widely used for bundling documentation, carton reinforcement, and labeling, making logistics expansion a major growth driver. Increasing cross-border shipments and warehouse automation investments are strengthening bulk procurement contracts with manufacturers.

Stable Institutional Consumption

Educational institutions, government agencies, and healthcare systems continue to generate recurring demand for staple pins. Regulatory compliance and physical recordkeeping requirements ensure continued usage even in digitally advanced economies. Rapid expansion of education infrastructure in developing countries further strengthens demand stability.

Growth in SMEs and Office Infrastructure

Rising entrepreneurship and small business formation globally are supporting steady consumption of office supplies. Co-working spaces, shared office environments, and administrative service providers rely heavily on affordable fastening solutions, sustaining consistent replacement-driven sales.

What are the restraints for the global market?

Increasing Digitalization of Documentation

The shift toward paperless workflows and cloud-based record management systems is gradually reducing document stapling requirements in developed markets. Corporate sustainability initiatives encouraging reduced paper consumption may moderate long-term growth rates.

Raw Material Price Volatility

Staple pins are primarily manufactured using steel wire, making production costs sensitive to fluctuations in metal prices. Since the market is highly price competitive, manufacturers often face margin pressure when raw material costs increase rapidly without proportional pricing adjustments.

What are the key opportunities in the staple pins industry?

E-commerce Infrastructure Expansion

The continued rise of online retail globally is creating sustained demand for packaging and warehouse documentation solutions. Staple manufacturers can capitalize on long-term supply agreements with logistics companies by offering specialized heavy-duty staples optimized for automated systems and high-volume usage environments.

Sustainable Product Development

Growing environmental governance policies are opening opportunities for eco-friendly staple products manufactured from recycled materials. Companies investing in green production technologies and biodegradable packaging formats are expected to gain competitive advantages in institutional tenders and corporate procurement programs.

Industrial Application Diversification

Staple pins are increasingly used in upholstery, furniture manufacturing, insulation installation, and woodworking applications. Expansion of modular furniture exports and DIY construction activities worldwide presents opportunities for higher-margin industrial staple categories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3210 Million |

| Market Size in 2026 | USD 3418.65 Million |

| Market Size in 2031 | USD 4683.85 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global staple pins market demonstrates strong demand diversification across multiple product categories, with standard office staple pins continuing to dominate overall consumption patterns. In 2025, standard office staples accounted for nearly 41% of total market demand, primarily driven by their widespread usage across corporate offices, educational institutions, government departments, and administrative environments where daily documentation handling remains essential. The affordability, compatibility with conventional staplers, and consistent replacement cycles make standard staples a recurring procurement item for organizations worldwide. The leading position of this segment is supported by high-volume institutional purchasing and continuous administrative workflows that rely on physical documentation despite ongoing digital transformation initiatives.Heavy-duty and industrial staple pins are witnessing accelerated growth compared to traditional office staples, supported by expanding applications in packaging, corrugation, furniture manufacturing, and light industrial assembly. The rapid expansion of global e-commerce and export-oriented manufacturing has increased the need for durable fastening solutions capable of handling thicker materials and automated stapling systems. Manufacturers are increasingly developing high-tensile steel staples designed for industrial staplers, improving operational efficiency in logistics and production facilities.

Specialty staples, including rust-resistant, galvanized, stainless steel, and colored variants, are gaining increasing adoption in premium office environments, archival storage, and specialized documentation applications where durability and long-term preservation are critical. Organizations managing legal records, healthcare documentation, and archival materials are increasingly prioritizing corrosion-resistant solutions to prevent document degradation over extended periods. Meanwhile, colored staples are being adopted for workflow organization and document categorization in modern office environments.Mini staples continue to maintain stable niche demand, primarily supported by compact staplers used in personal workspaces, home offices, and portable stationery kits. The rise of hybrid working models and home-based administrative activities has contributed to sustained consumption within this smaller but consistent segment.

Application Insights

Paper fastening applications remain the largest application segment, representing approximately 46% of the global staple pins market. The dominance of this segment is primarily driven by ongoing administrative documentation requirements across corporate, educational, legal, and government institutions. Despite increasing digitalization, regulatory compliance, recordkeeping obligations, and physical document verification processes continue to sustain strong demand for reliable paper fastening solutions. The leading position of this segment is reinforced by recurring usage patterns and high replacement frequency across institutional environments.Packaging and corrugation applications represent the fastest-growing segment, supported by the rapid expansion of e-commerce logistics, warehousing operations, and cross-border trade activities. Staple pins are widely used for carton sealing, corrugated box assembly, and protective packaging processes, particularly in automated production lines. As global supply chains continue to scale, manufacturers and logistics providers are increasingly investing in high-speed stapling equipment, directly driving demand for industrial-grade staples.Upholstery and furniture assembly applications are also gaining notable momentum, especially in Asia-based manufacturing hubs where furniture exports are expanding rapidly. Automated fastening technologies used in sofa manufacturing, bedding production, and interior furnishings rely heavily on durable staple pins to ensure structural stability and manufacturing efficiency. The growth of residential construction and rising global furniture consumption further support demand in this application area.

Distribution Channel Insights

B2B wholesale and institutional procurement channels account for approximately 44% of global staple pin sales, reflecting the dominance of bulk purchasing by corporations, educational institutions, government agencies, and industrial buyers. Long-term supply contracts, predictable consumption cycles, and centralized procurement strategies enable organizations to procure staple pins in large volumes, ensuring cost efficiency and uninterrupted operational supply. The leadership of this segment is driven by recurring institutional demand and structured procurement frameworks.Office supply retail stores continue to play a critical role in serving small businesses, independent professionals, and household consumers. These retail channels provide accessibility to a wide range of staple types and brands, supporting steady replacement demand from decentralized buyers. Retailers are increasingly integrating private-label products and bundled stationery offerings to remain competitive in price-sensitive markets.

E-commerce platforms are emerging as one of the fastest-growing distribution channels, driven by convenience, competitive pricing structures, subscription-based office supply models, and improved last-mile delivery networks. Businesses are increasingly shifting toward automated replenishment systems through online platforms, enabling efficient inventory management and predictable supply cycles.Industrial suppliers are strengthening their market presence by offering bundled fastening solutions that combine staples with stapling machinery, maintenance services, and customized packaging solutions. This integrated approach enhances customer retention among manufacturing and logistics clients while supporting long-term supplier relationships.

End-Use Insights

Corporate offices represent the largest end-use segment, accounting for nearly 29% of total market demand. The leading position of this segment is supported by continuous administrative workflows, internal documentation handling, contract management, and operational recordkeeping requirements. Even with increasing digital adoption, hybrid documentation systems combining physical and electronic records continue to sustain staple pin consumption across enterprises.Educational institutions remain a major contributor to market demand due to expanding global student populations, increased academic documentation, examination processes, and administrative paperwork. Schools, colleges, and universities require staple pins for routine academic operations, ensuring consistent long-term consumption.

Packaging and logistics companies are the fastest-growing end-use segment, expanding at above-average growth rates as global shipping volumes rise alongside e-commerce penetration. Warehousing expansion, fulfillment centers, and export packaging operations increasingly rely on durable fastening solutions to maintain packaging integrity during transportation.Healthcare institutions maintain steady demand driven by documentation compliance requirements, patient record management, and regulatory filing processes. Although healthcare digitization is progressing, physical documentation continues to play a critical operational role in many regions.Furniture manufacturing is emerging as a high-growth industrial end-use segment, supported by expanding residential construction, global furniture trade, and automation adoption within production facilities requiring consistent fastening solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Staple Pins Market Segmentations

By Product Type

- Standard Office Staple Pins

- Heavy-Duty Staple Pins

- Industrial Staple Pins

- Mini Staple Pins

- Specialty Staple Pins

By Application

- Paper Fastening

- Packaging & Corrugation

- Upholstery & Furniture Assembly

- Construction & Woodworking

- Healthcare Documentation

By Distribution Channel

- Office Supply Retail Stores

- Online/E-commerce Platforms

- Wholesale & B2B Distribution

- Industrial Supply Vendors

- Institutional Procurement Contracts

By End Use

- Corporate Offices

- Educational Institutions

- Packaging & Logistics Companies

- Manufacturing & Furniture Industry

- Government Organizations

- Healthcare Institutions

Regional Insights

Asia-Pacific

Asia-Pacific leads the global staple pins market with approximately 42% market share in 2025, supported by strong manufacturing capacity, expanding institutional infrastructure, and rising packaging demand. China dominates both production and consumption due to its extensive manufacturing ecosystem, large-scale export operations, and integrated supply chains that require high-volume fastening solutions.India represents the fastest-growing market within the region, driven by expanding education infrastructure, rapid growth of small and medium-sized enterprises, increasing office formalization, and government administrative modernization initiatives that continue to rely on hybrid physical documentation systems. Rising e-commerce penetration and logistics expansion further strengthen industrial staple demand. Southeast Asian countries, including Vietnam, Indonesia, and Thailand, are witnessing increasing consumption supported by furniture exports, electronics manufacturing growth, and regional supply chain diversification.Key regional growth drivers include expanding manufacturing output, increasing institutional enrollment, growth in export-oriented packaging industries, cost-efficient production capabilities, and rising adoption of automated stapling technologies across industrial sectors.

North America

North America accounts for nearly 22% of global demand, led primarily by the United States. Market growth is supported by stable institutional procurement cycles, strong corporate office presence, and consistent demand from educational and healthcare systems. Organizations in the region increasingly prefer premium-quality and corrosion-resistant staple pins that ensure durability and long-term document preservation.The region is also witnessing growing adoption of automation-compatible stapling systems within logistics centers and warehouse environments, driven by advanced supply chain infrastructure and high e-commerce fulfillment volumes. Additional growth drivers include product innovation, replacement demand from established office infrastructure, and increasing preference for environmentally compliant fastening products.

Europe

Europe holds around 20% market share, with Germany, the United Kingdom, and France leading regional consumption. The market benefits from strong institutional frameworks, mature corporate environments, and steady educational demand. Sustainability regulations across the European Union are encouraging manufacturers to adopt recyclable materials, reduced metal usage, and environmentally compliant production processes.Regional growth is further supported by increasing demand for premium and specialty staples designed for archival documentation, legal recordkeeping, and professional office environments. Automation within packaging and furniture manufacturing sectors also contributes to industrial staple consumption across Central and Eastern Europe.

Latin America

Latin America represents roughly 9% of global demand, driven primarily by Brazil and Mexico. Market expansion is supported by improving retail distribution networks, growth in small business establishments, and increasing investments in packaging and food processing industries. Expanding urbanization and educational enrollment are contributing to rising office and institutional stationery consumption.Regional growth drivers include the expansion of organized retail channels, increasing cross-border trade activities, growing logistics infrastructure, and gradual modernization of administrative systems across both public and private sectors.

Middle East & Africa

The Middle East and Africa region represents an emerging growth market supported by ongoing education investments, administrative expansion, and infrastructure development initiatives. Countries such as the UAE and South Africa are witnessing increasing demand from institutional procurement programs and large-scale construction and commercial development projects.Government diversification strategies, rising business formation, and expanding logistics hubs are strengthening regional consumption of staple pins. Additionally, improvements in office infrastructure, growing private education sectors, and increasing import distribution networks are expected to support sustained long-term market growth across the region.

Key Players in the Staple Pins Market

- ACCO Brands Corporation

- Stanley Black & Decker, Inc.

- MAX Co., Ltd.

- Rapid Group AB

- Kokuyo Co., Ltd.

- Novus Dahle GmbH

- Maped Group

- PLUS Corporation

- Kangaro Industries Ltd.

- Pilot Corporation

- DELI Group Co., Ltd.

- Foska International

- Guangbo Group

- 3M Company

- Leitz (Esselte Group)