Sports Nutrition Gummies Market Size

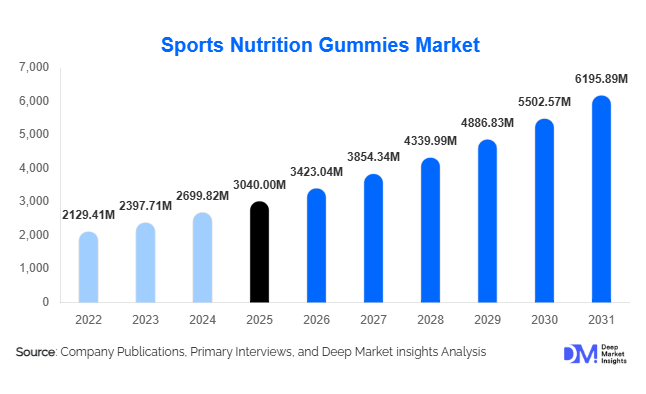

According to Deep Market Insights,the global sports nutrition gummies market size was valued at USD 3,040 million in 2025 and is projected to grow from USD 3,423.04 million in 2026 to reach USD 6,195.89 million by 2031, expanding at a CAGR of 12.6% during the forecast period (2026–2031). Market expansion is primarily driven by rising global fitness participation, growing consumer preference for convenient and chewable supplement formats, and increasing innovation in sugar-free and plant-based functional formulations. The transition from traditional powders and capsules to portable, flavored gummy formats is transforming sports supplementation into a mainstream lifestyle category, particularly among millennials, Gen Z consumers, and recreational fitness enthusiasts.

Key Market Insights

- Protein and performance-based gummies are gaining mainstream adoption, particularly among recreational fitness users seeking convenient muscle recovery solutions.

- Sugar-free formulations dominate product innovation, accounting for the largest share due to keto, low-carb, and metabolic health trends.

- North America leads global demand, supported by strong sports supplement penetration and D2C brand ecosystems.

- Asia-Pacific is the fastest-growing region, driven by expanding gym memberships and rising disposable incomes in China and India.

- Online retail channels account for the largest sales share, fueled by influencer marketing and subscription-based performance stacks.

- Technological advancements in micro-encapsulation and starchless molding are enabling higher bioavailability and improved ingredient stability.

What are the latest trends in the sports nutrition gummies market?

Sugar-Free and Clean-Label Innovation Accelerating

Manufacturers are increasingly reformulating products with stevia, monk fruit, and low-glycemic sweeteners to cater to consumers seeking sugar-free alternatives. Clean-label positioning, vegan certifications, and allergen-free claims are becoming competitive differentiators. Plant-based pectin is replacing traditional gelatin in many new launches, broadening the consumer base to include vegan athletes. Brands are also emphasizing clinically dosed actives such as creatine monohydrate, beta-alanine, and collagen peptides, strengthening the perception of gummies as serious performance supplements rather than confectionery-based wellness products.

Direct-to-Consumer and Personalization Models Expanding

The market is witnessing a strong shift toward digital-first distribution strategies. Subscription-based gummy packs tailored to workout intensity, gender, and fitness goals are gaining popularity. AI-driven nutrition platforms now integrate wearable fitness data to recommend personalized gummy stacks for pre-workout, intra-workout, and recovery phases. This personalization trend enhances customer retention and increases lifetime value. Influencer-led marketing campaigns across social platforms are further driving awareness and accelerating product trial among younger consumers.

What are the key drivers in the sports nutrition gummies market?

Rising Global Fitness Participation

Global gym memberships and organized sports participation have grown steadily over the past decade. Recreational fitness enthusiasts now represent the largest consumer group for sports supplements, accounting for approximately 34% of total market revenue. The democratization of fitness through boutique studios, home workouts, and endurance events has significantly expanded the addressable market for convenient supplement formats such as gummies.

Shift Toward Convenient Supplement Formats

Consumers increasingly prefer portable, easy-to-consume formats over powders that require mixing. Gummies offer taste, portion control, and ease of use, particularly appealing to busy urban populations. Higher compliance rates among women and younger athletes have further supported adoption.

What are the restraints for the global market?

Dosage Limitations Compared to Traditional Formats

Gummies face formulation constraints in delivering high protein or amino acid dosages compared to powders and ready-to-drink beverages. Athletes requiring 20–30 grams of protein per serving may still prefer traditional formats, limiting gummy penetration in elite bodybuilding segments.

Regulatory and Labeling Complexities

Sports nutrition gummies are subject to dietary supplement and food safety regulations that vary across regions. Compliance with health claims, ingredient approvals, and labeling standards remains complex, particularly in Europe and Asia-Pacific markets. Non-compliance risks product recalls and reputational damage.

What are the key opportunities in the sports nutrition gummies industry?

Emerging Market Expansion

Asia-Pacific and Latin America present strong growth opportunities. Rising middle-class incomes in India, China, Brazil, and Indonesia are fueling gym enrollments and sports participation. Localized flavors, halal-certified products, and region-specific marketing strategies can significantly expand market penetration in these regions, which are projected to grow at double-digit rates.

Performance-Focused Clinical Formulations

There is growing demand for clinically validated gummy formulations containing creatine, BCAAs, electrolytes, and adaptogens. Companies investing in research-backed claims and bioavailability-enhancing technologies can capture premium pricing segments. Institutional sales to military and corporate wellness programs also represent untapped opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3040.00 Million |

| Market Size in 2026 | USD 3423.04 Million |

| Market Size in 2031 | USD 6195.89 Million |

| CAGR | 12.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product landscape of the global sports nutrition gummies market is characterized by diversified functional positioning, with protein gummies emerging as the leading product category. In 2025, protein gummies account for approximately 28% of total market share, primarily driven by increasing demand for convenient muscle recovery solutions among recreational fitness users and mainstream health-conscious consumers. The leading segment driver for protein gummies is the rising adoption of strength training and resistance-based workouts across both developed and emerging economies, combined with consumer preference for palatable, easy-to-consume alternatives to traditional protein powders and bars. The format’s portability, precise dosage, and improved taste profiles further enhance repeat consumption rates.Creatine gummies represent one of the fastest-growing sub-segments within the product portfolio. Growth in this category is supported by expanding scientific awareness around creatine’s role in enhancing muscular strength, performance output, and high-intensity exercise capacity. As clinical validation increases and social media fitness influencers promote creatine supplementation to broader audiences, demand continues to accelerate, particularly among younger gym-goers and performance-focused consumers seeking simplified supplementation formats.Electrolyte and hydration gummies are gaining substantial traction among endurance athletes and active lifestyle consumers. Their growth is driven by heightened awareness of hydration management, especially in regions with warm climates and expanding outdoor fitness participation. Additionally, pre-workout caffeine-based gummies account for a significant portion of product demand, supported by growing preference for rapid energy-boosting formulations without the need for mixing powders. The convenience factor, combined with demand for stimulant-based performance enhancement, continues to expand this segment’s addressable consumer base.

Application Insights

By application, pre-workout supplementation dominates the market, capturing nearly 31% share in 2025. The leading driver for this segment is the increasing demand for immediate energy enhancement, focus improvement, and performance optimization prior to workouts. Consumers increasingly seek fast-absorbing caffeine, beta-alanine, and nitric oxide–supporting formulations in convenient formats, which has positioned pre-workout gummies as a preferred alternative to traditional drinks and powders.

Post-workout recovery applications follow closely, supported by the growing integration of collagen, branched-chain amino acids (BCAAs), anti-inflammatory botanicals, and muscle repair nutrients into gummy formulations. The shift toward holistic recovery strategies, including joint health and inflammation management, has broadened the consumer base beyond competitive athletes to include aging fitness enthusiasts and recreational exercisers.Daily performance supplementation is expanding rapidly, driven by consumers who incorporate sports nutrition into routine wellness regimens rather than limiting usage to training sessions. This shift reflects the broader mainstreaming of sports nutrition, where products are increasingly positioned as lifestyle-enhancing functional foods rather than niche athletic supplements.

Distribution Channel Insights

Online retail channels represent the dominant distribution pathway, accounting for approximately 38% of global sales in 2025. The primary driver of this channel’s leadership is the rapid expansion of direct-to-consumer models and subscription-based purchasing patterns, which enhance brand loyalty and recurring revenue streams. Brand-owned websites enable personalized marketing strategies, product education, and influencer collaborations, while major e-commerce marketplaces provide global accessibility and price transparency.Specialty sports nutrition stores continue to maintain relevance, particularly for clinically positioned, premium, and performance-focused products where in-store consultation and product differentiation play a critical role in purchasing decisions. Meanwhile, supermarkets and pharmacies contribute significantly to mass-market penetration by improving product visibility and accessibility among general wellness consumers, further accelerating category mainstream adoption.

Consumer Type Insights

Recreational fitness enthusiasts account for approximately 34% of total market revenue, making them the largest consumer segment. The leading driver behind this segment’s dominance is the rapid expansion of gym memberships, home fitness adoption, and active lifestyle awareness across urban populations. As sports nutrition becomes less associated with professional bodybuilding and more aligned with everyday wellness goals, this demographic continues to expand.Professional athletes represent a comparatively smaller but high-value segment, characterized by higher spending per capita and preference for scientifically validated, performance-enhancing formulations. This group often prioritizes clinically tested ingredients, third-party certifications, and compliance with anti-doping regulations, sustaining demand for premium offerings.Youth sports participants are emerging as one of the fastest-growing consumer categories. Rising parental focus on athletic development, combined with the appeal of convenient and palatable gummy formats, supports increasing adoption among adolescent athletes engaged in organized sports programs.

Explore more data points, trends and opportunities Download Free Sample Report

Sports Nutrition Gummies Market Segmentations

By Product Type

- Protein Gummies

- Creatine Gummies

- BCAA Gummies

- Electrolyte & Hydration Gummies

- Pre-Workout Energy Gummies

- Post-Workout Recovery Gummies

- Vitamin & Mineral Performance Gummies

- Adaptogen & Endurance Gummies

By Consumer Type

- Professional Athletes

- Recreational Fitness Enthusiasts

- Bodybuilders & Strength Trainers

- Endurance Athletes

- Youth & Teen Sports Participants

- Active Lifestyle Consumers

By Distribution Channel

- Online Retail

- Specialty Sports Nutrition Stores

- Pharmacies & Drugstores

- Supermarkets & Hypermarkets

- Fitness Centers & Gyms

- Direct-to-Consumer Subscription Models

Regional Insights

North America

North America accounts for approximately 36% of global market share in 2025, with the United States alone contributing nearly 30% of total global revenue. Regional growth is primarily driven by high dietary supplement penetration, strong consumer awareness regarding performance nutrition, and advanced e-commerce infrastructure. The presence of established sports nutrition brands, widespread gym culture, and a mature influencer marketing ecosystem further amplify demand. In addition, increasing adoption of clean-label, sugar-free, and plant-based formulations supports sustained innovation. Canada contributes additional momentum through rising interest in vegan and natural ingredient positioning, reinforcing regional expansion.

Europe

Europe holds approximately 27% market share, led by Germany, the United Kingdom, and France. Regional growth is supported by a strong regulatory framework that enhances consumer trust in product quality and safety. Increasing demand for sugar-free, vegan, and non-GMO supplements aligns with broader European clean-label preferences. Additionally, the rising popularity of functional confectionery formats and expanding participation in recreational fitness activities drive market penetration. Growth is further supported by expanding cross-border e-commerce and private-label development across major retail chains.

Asia-Pacific

Asia-Pacific accounts for approximately 24% of global demand and represents the fastest-growing region, expanding at nearly 14% CAGR. Growth is driven by rising disposable incomes, rapid urbanization, and expanding gym membership bases in China and India. Increasing digital commerce penetration and social media fitness trends significantly influence purchasing behavior among younger consumers. Japan and Australia represent more mature sub-markets characterized by strong premium product uptake, innovation in functional ingredients, and high consumer awareness regarding performance nutrition. The region’s large youth population and growing sports participation further strengthen long-term growth potential.

Latin America

Latin America represents approximately 6% of global demand, with Brazil serving as the primary growth engine. Regional expansion is driven by a strong bodybuilding culture, increasing urban fitness participation, and expanding supplement retail networks. Growing middle-class income levels and rising awareness of sports nutrition benefits support gradual market formalization and product diversification across the region.

Middle East & Africa

The Middle East & Africa region contributes roughly 7% of global revenue. Growth is supported by increasing government investment in sports infrastructure, particularly in the United Arab Emirates and Saudi Arabia, alongside broader national wellness initiatives. Rising disposable incomes, expanding expatriate populations, and growing premium retail formats further stimulate demand. In addition, high climate temperatures enhance demand for hydration-focused formulations, indirectly supporting electrolyte gummy adoption across key markets.

Key Players in the Sports Nutrition Gummies Market

- Glanbia plc

- Herbalife Ltd.

- Nestlé Health Science

- GNC Holdings LLC

- Amway Corp.

- The Hut Group (Myprotein)

- Abbott Laboratories

- Bayer AG

- Otsuka Holdings Co., Ltd.

- Church & Dwight Co., Inc.

- Garden of Life LLC

- Nature’s Way Products LLC

- NOW Foods

- Iovate Health Sciences

- Olly Public Benefit Corporation