Specialty Food Ingredients Market Size

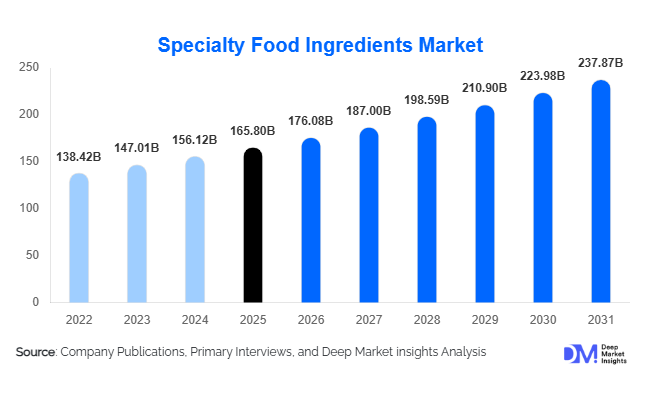

According to Deep Market Insights, the global specialty food ingredients market size was valued at USD 165.8 billion in 2025 and is projected to grow from USD 176.08 billion in 2026 to reach USD 237.87 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The specialty food ingredients market growth is primarily driven by rising demand for clean-label formulations, plant-based innovations, functional fortification, and advanced food processing technologies. Increasing consumer preference for health-oriented, minimally processed, and nutritionally enriched food products is accelerating ingredient innovation across bakery, beverages, dairy, processed foods, and nutraceuticals.

Key Market Insights

- Functional ingredients account for the largest revenue share, supported by rising demand for probiotics, plant proteins, and fortified food products.

- Plant-based ingredients dominate by source, contributing over 40% of total market revenue in 2025 due to vegan and flexitarian trends.

- Asia-Pacific holds the largest regional share, driven by rapid processed food consumption growth in China and India.

- Natural flavors and clean-label preservatives are replacing synthetic additives, reshaping formulation strategies across developed markets.

- Powdered ingredients remain the preferred form, accounting for nearly half of total demand due to ease of storage and transport.

- The top five global players collectively hold around 40% market share, indicating moderate consolidation with high innovation intensity.

What are the latest trends in the specialty food ingredients market?

Shift Toward Clean-Label and Natural Reformulations

Food manufacturers are actively replacing synthetic preservatives, artificial colors, and chemical flavor enhancers with plant-based extracts, fermentation-derived ingredients, and natural antioxidants. Regulatory scrutiny in North America and Europe is reinforcing this transition. Consumers increasingly scrutinize ingredient lists, favoring recognizable components and minimally processed additives. This trend has expanded demand for botanical extracts, natural emulsifiers, and enzyme-based processing aids. Manufacturers are investing in traceability systems and sustainable sourcing partnerships to maintain brand trust and justify premium pricing.

Precision Fermentation and Functional Fortification

Technological innovation is transforming ingredient production. Precision fermentation is enabling the development of bio-identical proteins, specialty enzymes, and high-purity nutritional compounds with improved yield and sustainability profiles. Encapsulation technologies are enhancing ingredient stability and bioavailability, particularly in beverages and nutraceuticals. Functional fortification, including immunity-boosting blends and digestive health solutions, is gaining prominence in mainstream food categories, blurring the line between conventional foods and supplements.

What are the key drivers in the specialty food ingredients market?

Growing Health and Wellness Awareness

Consumers worldwide are prioritizing preventive health, increasing demand for foods enriched with fibers, omega-3 fatty acids, vitamins, minerals, and plant proteins. The global nutraceutical industry, valued at over USD 430 billion, continues to integrate specialty ingredients into mainstream formulations, significantly driving revenue growth.

Expansion of the Processed and Convenience Food Industry

Urbanization and rising disposable incomes in emerging markets are fueling processed food demand. Bakery, dairy alternatives, ready-to-drink beverages, and frozen foods require stabilizers, emulsifiers, preservatives, and flavor systems, directly stimulating specialty ingredient consumption. Asia-Pacific markets are particularly influential in driving volume growth.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuating agricultural commodity prices, supply chain disruptions, and energy cost inflation impact production expenses for botanical extracts, protein isolates, and fermentation substrates. Margin pressure remains a concern for mid-sized manufacturers.

Regulatory Compliance Complexity

Different additive approval standards across regions increase certification costs and prolong commercialization timelines. Companies must comply with GRAS standards in the U.S., EFSA regulations in Europe, and country-specific food codes in Asia.

What are the key opportunities in the specialty food ingredients industry?

Plant-Based and Alternative Protein Expansion

Rising vegan and flexitarian diets create strong opportunities for plant protein isolates, hydrocolloids, and flavor-masking systems. Government-backed sustainability programs are encouraging domestic production of plant-derived ingredients, especially in India and China.

Emerging Market Urbanization

Rapid expansion of modern retail and food processing industries in Southeast Asia, Latin America, and Africa offers long-term growth prospects. Localized production facilities and partnerships can reduce import dependency and improve cost competitiveness.

Product Type Insights

Functional ingredients lead the market with approximately 32% share in 2025, driven by fortified food demand and probiotic integration in dairy and beverages. Sensory ingredients, including flavors and colors, represent a substantial share due to product differentiation needs. Texture and stability enhancers remain essential in processed foods, particularly in bakery and frozen applications. Nutritional fortification ingredients are witnessing accelerated uptake in developing economies targeting micronutrient deficiencies.

Source Insights

Plant-based ingredients account for nearly 41% of global revenue in 2025, making them the dominant source segment within the specialty food ingredients market. The leadership of plant-derived ingredients is primarily driven by accelerating vegan, vegetarian, and flexitarian dietary trends across North America and Europe, alongside rising lactose intolerance and allergen concerns globally. Food manufacturers are increasingly reformulating products using plant proteins (pea, soy, rice), botanical extracts, plant-based emulsifiers, and natural colorants to align with clean-label and sustainability positioning. In addition, lower carbon footprint perceptions and ESG commitments among multinational food brands are strengthening procurement preference toward plant-based inputs.

Microbial and fermentation-derived ingredients represent the fastest-growing source category, supported by advancements in biotechnology, enzyme engineering, and precision fermentation. These technologies enable scalable production of specialty enzymes, probiotics, organic acids, and bio-identical proteins with improved purity and yield consistency. The segment’s growth is also fueled by rising demand for gut-health solutions, dairy alternatives, and functional beverages. Compared to traditional agricultural sourcing, fermentation offers supply stability and lower dependency on climate-sensitive crops, making it increasingly attractive to global manufacturers.

Form Insights

Powdered ingredients dominate the market with approximately 46% share in 2025, primarily due to their extended shelf life, reduced transportation costs, ease of storage, and compatibility with automated large-scale food manufacturing systems. Powder formats are especially preferred in bakery, nutraceutical, dairy premixes, and dry beverage applications. The stability of powdered emulsifiers, proteins, stabilizers, and flavor systems allows manufacturers to maintain consistent batch quality, which is critical in high-volume food production environments.

Liquid forms maintain strong demand in beverage, dairy, and confectionery segments, where rapid solubility and uniform dispersion are essential. Meanwhile, encapsulated formats are gaining significant traction, particularly for high-value functional ingredients such as probiotics, omega-3 fatty acids, and vitamins. Encapsulation enhances bioavailability, masks undesirable flavors, and protects sensitive compounds from heat, oxygen, and moisture during processing. This format is increasingly used in fortified beverages and functional snack applications, contributing to its above-average growth rate compared to traditional liquid systems.

End-Use Industry Insights

The bakery & confectionery segment accounts for approximately 24% of total 2025 demand, maintaining its position as the largest end-use industry. Global packaged baked goods consumption exceeds USD 550 billion annually, driving sustained demand for emulsifiers, sweeteners, natural colors, preservatives, and texture-modifying hydrocolloids. The leading driver within this segment is reformulation toward reduced sugar, clean-label preservation, and gluten-free alternatives. Manufacturers are increasingly incorporating specialty fibers, enzyme blends, and plant-based stabilizers to improve texture and shelf stability while meeting evolving consumer preferences.

The beverages segment is among the fastest-growing end-use industries, expanding at over 7% CAGR, supported by rapid innovation in functional drinks, plant-based milks, energy beverages, and probiotic formulations. Demand for soluble fibers, botanical extracts, natural flavors, and fortification blends is accelerating, particularly in Asia-Pacific and North America. Functional hydration and immunity-focused beverages are major contributors to incremental specialty ingredient consumption. The nutraceuticals and dietary supplements segment represents a high-margin end-use category. With the global nutraceutical industry surpassing USD 430 billion, demand for specialty amino acids, encapsulated probiotics, plant bioactives, and micronutrient blends continues to rise. This segment benefits from preventive healthcare trends and personalized nutrition solutions, further strengthening specialty ingredient adoption.

| By Product Type | By Source | By Form | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 31% of the global market share in 2025, making it the largest regional market. China and India are the primary growth engines. In China, expanding domestic food processing capacity, strong government support for ingredient self-sufficiency, and rapid growth in plant-based beverages are driving demand. Rising disposable incomes and urbanization are accelerating packaged food and convenience product consumption. India’s growth is fueled by expanding dairy processing, increasing health awareness, and government initiatives supporting food manufacturing infrastructure. Southeast Asian countries such as Indonesia and Vietnam are also witnessing rising processed food imports and beverage innovation, further strengthening regional growth. Asia-Pacific remains the fastest-growing region, supported by population scale and expanding middle-class demand.

North America

North America accounts for nearly 29% of global revenue, with the United States contributing approximately 22% individually. Regional growth is driven by strong clean-label adoption, advanced food R&D infrastructure, and high penetration of plant-based and functional food products. Major food companies are aggressively reformulating portfolios to reduce artificial additives and enhance nutritional value. The U.S. leads in precision fermentation, alternative proteins, and specialty enzyme development, supported by significant venture capital and private equity investment. Canada contributes through strong demand for fortified bakery and dairy alternatives, while Mexico supports regional growth through expanding beverage manufacturing.

Europe

Europe represents around 26% of the global market share, led by Germany, France, and the United Kingdom. Strict regulatory frameworks promoting food safety, additive transparency, and sustainability act as strong growth catalysts. European consumers demonstrate a high willingness to pay premiums for organic, natural, and sustainably sourced ingredients. Additionally, plant-based innovation hubs across the Netherlands and Germany are accelerating ingredient R&D. The region’s strong bakery culture and expanding functional dairy alternatives segment further reinforce specialty ingredient consumption. Carbon reduction targets and circular economy initiatives are also influencing ingredient sourcing strategies.

Latin America

Latin America contributes approximately 8% of global demand, with Brazil and Mexico as leading markets. Regional growth is driven by expanding beverage manufacturing, rising processed snack consumption, and increasing export-oriented food production. Brazil’s strong agricultural base supports domestic specialty ingredient production, particularly in plant-derived extracts and sweeteners. Mexico’s proximity to North America enhances cross-border supply chains, supporting ingredient demand in bakery and beverage segments. Economic stabilization and retail modernization are expected to gradually expand specialty ingredient penetration across the region.

Middle East & Africa

The Middle East & Africa account for around 6% of the global market share. Growth is primarily supported by increasing food imports, urban population growth, and demand for fortified food products to address micronutrient deficiencies. The UAE and Saudi Arabia are leading markets due to strong processed food imports and premium retail expansion. South Africa drives demand through the domestic beverage and dairy processing industries. Additionally, government-backed food security initiatives in Gulf countries are encouraging local food manufacturing investments, indirectly stimulating specialty ingredient demand.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Specialty Food Ingredients Market

- Cargill Incorporated

- Archer Daniels Midland Company

- Kerry Group

- DSM-Firmenich

- Ingredion Incorporated

- Givaudan

- International Flavors & Fragrances (IFF)

- Tate & Lyle

- Symrise AG

- Chr. Hansen Holding

- Ajinomoto Co., Inc.

- Novozymes A/S

- Sensient Technologies

- Roquette Frères

- Corbion N.V.