Specialty Carbohydrate Market Size

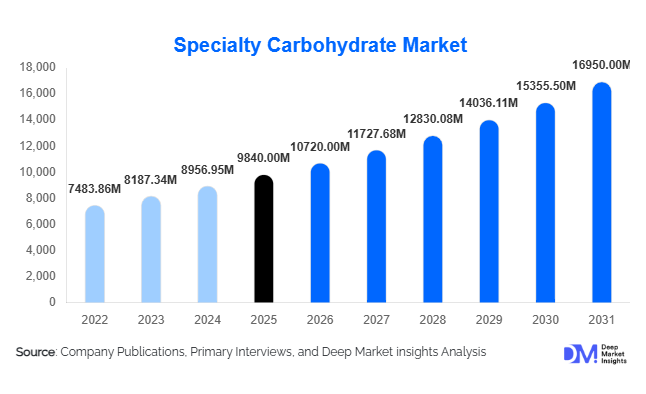

According to Deep Market Insights, the global specialty carbohydrate market size was valued at USD 9,840 million in 2025 and is projected to grow from USD 10,720 million in 2026 to reach approximately USD 16,950 million by 2031, expanding at a CAGR of 9.6% during the forecast period (2026–2031). Growth in the specialty carbohydrate market is primarily driven by increasing demand for functional food ingredients, expanding applications in pharmaceuticals and nutraceuticals, and rising consumer preference for low-glycemic and gut-health-supporting products.

Specialty carbohydrates, including oligosaccharides, sugar alcohols, resistant starches, and functional polysaccharides, are gaining widespread adoption across food & beverage, infant nutrition, clinical nutrition, and biotechnology industries. These ingredients provide functional benefits such as prebiotic activity, improved digestion, sugar reduction, and enhanced texture stabilization, making them essential components in modern food formulation. The global transition toward healthier diets, combined with regulatory support for sugar reduction and clean-label products, is accelerating innovation in carbohydrate engineering and fermentation technologies.

Food manufacturers are increasingly reformulating products to incorporate functional carbohydrates that deliver both nutritional and technological advantages. Meanwhile, pharmaceutical applications are expanding due to the role of specialty carbohydrates in drug delivery systems, vaccine stabilization, and microbiome-targeted therapies. Asia-Pacific and North America are emerging as innovation hubs due to strong investments in biotechnology infrastructure and dietary supplement markets. With growing awareness of metabolic health and microbiome science, specialty carbohydrates are evolving from commodity sweeteners into high-value functional ingredients, positioning the market for sustained long-term expansion.

Key Market Insights

- Prebiotic carbohydrates are witnessing rapid adoption due to rising awareness of gut microbiome health.

- Food and beverage reformulation initiatives focused on sugar reduction are accelerating demand globally.

- Asia-Pacific accounts for the fastest growth supported by expanding infant nutrition and functional food sectors.

- Pharmaceutical and clinical nutrition applications are emerging as high-margin segments.

- Biotechnology-driven production methods such as enzymatic synthesis and precision fermentation are improving scalability.

- Clean-label and plant-based product innovation continues to expand specialty carbohydrate usage.

What are the latest trends in the specialty carbohydrate market?

Microbiome-Focused Functional Nutrition

Scientific advances linking gut microbiota to immunity, metabolism, and mental health have significantly increased demand for prebiotic carbohydrates such as inulin, fructooligosaccharides (FOS), and galactooligosaccharides (GOS). Food and supplement brands increasingly market microbiome-supporting products, creating strong commercial opportunities for specialty carbohydrate producers. Clinical validation studies and regulatory approvals for digestive health claims are further supporting adoption across functional beverages, dairy alternatives, and nutritional supplements.

Precision Fermentation and Enzymatic Processing

Manufacturers are investing heavily in enzymatic conversion technologies and fermentation-based carbohydrate production. These technologies enable tailored molecular structures with targeted health benefits while improving yield efficiency and reducing environmental impact. Precision fermentation is also allowing the development of rare sugars and customized oligosaccharides previously difficult to scale commercially, opening new premium product categories.

What are the key drivers in the specialty carbohydrate market?

Rising Demand for Sugar Reduction Solutions

Global regulatory pressure to reduce sugar consumption has driven food companies to adopt specialty carbohydrates as sugar substitutes and functional bulking agents. Sugar alcohols and resistant starches enable calorie reduction while maintaining texture and taste, making them critical in bakery, confectionery, and beverage reformulations.

Growth of Functional and Clinical Nutrition

Clinical nutrition products targeting digestive disorders, diabetes management, and elderly nutrition increasingly incorporate specialty carbohydrates. Hospitals and medical nutrition providers are adopting low-glycemic carbohydrates that improve nutrient absorption and metabolic outcomes, supporting consistent demand growth.

Expansion of Infant Nutrition Industry

Human milk oligosaccharides (HMOs) and related compounds are gaining adoption in infant formula formulations to replicate breast milk functionality. Rising birth rates in emerging economies and premiumization of infant nutrition products are strengthening long-term demand.

What are the restraints for the global market?

High Production Costs

Advanced carbohydrate synthesis processes require specialized enzymes, fermentation infrastructure, and purification technologies, leading to higher production costs compared to conventional sugars. Price sensitivity in developing markets limits adoption in mass-market food categories.

Regulatory Approval Complexities

Novel carbohydrate ingredients must undergo extensive safety assessments and regulatory approvals across regions, slowing commercialization timelines. Differences in labeling standards between the U.S., EU, and Asia create additional compliance challenges for manufacturers.

What are the key opportunities in the specialty carbohydrate industry?

Personalized Nutrition and Functional Supplements

The growing personalized nutrition market presents strong opportunities for specialty carbohydrates tailored to individual microbiome profiles. Companies developing customized prebiotic blends aligned with genetic and health data are expected to capture premium margins.

Emerging Market Food Fortification Programs

Governments across Asia, Africa, and Latin America are promoting nutritional fortification initiatives. Specialty carbohydrates that improve mineral absorption and digestive health are increasingly incorporated into fortified foods distributed through public health programs.

Biopharmaceutical Applications

Specialty carbohydrates are gaining importance in vaccine stabilization, drug encapsulation, and biologics manufacturing. Growth in biologics and mRNA therapeutics creates new high-value application areas beyond traditional food usage.

Product Type Insights

The global specialty carbohydrate market demonstrates a highly diversified product landscape characterized by functional versatility, technological innovation, and expanding health-oriented applications across industries. Among all product categories, prebiotic oligosaccharides continue to dominate the market, accounting for nearly 32% of the global market share in 2025. Their leadership position is primarily driven by increasing consumer awareness regarding digestive health, microbiome balance, and immune system support. Oligosaccharides such as fructooligosaccharides (FOS), galactooligosaccharides (GOS), and inulin-derived compounds have gained widespread acceptance in functional foods, dietary supplements, and infant nutrition products. The growing scientific validation of gut microbiota modulation has significantly strengthened demand, encouraging food manufacturers to integrate prebiotic ingredients into everyday products including dairy alternatives, beverages, snack bars, and fortified cereals.The leading segment growth is strongly supported by the rising global prevalence of digestive disorders, lifestyle-related health concerns, and preventive healthcare trends. Consumers increasingly seek ingredients that provide measurable health benefits beyond basic nutrition, positioning oligosaccharides as essential components in next-generation functional formulations. Regulatory approvals supporting health claims in multiple developed markets further accelerate adoption, while advancements in enzymatic production technologies have improved scalability and reduced manufacturing costs. Additionally, clean-label positioning and natural sourcing capabilities enhance market attractiveness, allowing manufacturers to align with transparency-driven purchasing behavior.Sugar alcohols hold approximately 24% market share, supported by their extensive application in sugar-free and reduced-calorie food formulations. Ingredients such as sorbitol, erythritol, and xylitol are widely used in confectionery, bakery products, chewing gums, and diabetic-friendly foods. Increasing global concerns surrounding obesity, diabetes, and excessive sugar consumption have accelerated reformulation initiatives among food manufacturers. Sugar alcohols provide sweetness with lower caloric contribution while maintaining desirable texture and mouthfeel, making them indispensable in modern food innovation. Growth in this segment is further strengthened by expanding regulatory pressure on sugar reduction across developed economies and rising consumer demand for low-glycemic index products.Resistant starch represents nearly 18% of the market, driven by its dual functionality as both a dietary fiber and a texture-enhancing ingredient. Resistant starch supports blood sugar management, improved satiety, and digestive health, aligning closely with metabolic wellness trends. The segment benefits from growing adoption in bakery reformulation, ready-to-eat meals, and plant-based food applications where texture stability and fiber enrichment are essential.

Application Insights

Applications of specialty carbohydrates span multiple industries, reflecting their adaptability and functional value across nutritional, pharmaceutical, and industrial domains. The food & beverages segment remains the dominant application area, accounting for nearly 45% of total market share. The leadership of this segment is primarily driven by widespread reformulation initiatives aimed at reducing sugar content, enhancing fiber levels, and improving nutritional profiles without sacrificing sensory quality. Specialty carbohydrates enable manufacturers to achieve sweetness balance, improved texture, moisture retention, and shelf stability, making them essential in modern product innovation.The leading segment driver stems from the rapid expansion of functional foods and beverages, fueled by increasing consumer preference for products that support digestive health, energy management, and metabolic wellness. Beverage manufacturers increasingly incorporate prebiotic fibers into functional drinks, while bakery and snack producers rely on resistant starches and polysaccharides to enhance nutritional density. Rising demand for fortified and convenience foods among urban populations further strengthens adoption across developed and emerging markets.Dietary supplements account for approximately 20% of market share, supported by growing consumer emphasis on preventive healthcare and personalized nutrition. Specialty carbohydrates are widely used in capsules, powders, and functional blends targeting gut health, immunity, and sports performance. The expansion of e-commerce supplement distribution channels has significantly increased global accessibility, encouraging new product launches and brand diversification. Scientific research linking gut microbiota to overall health outcomes continues to reinforce demand within this application.The pharmaceutical sector contributes nearly 15% share, driven by increasing use of specialty carbohydrates as excipients, stabilizers, and drug delivery agents. As biologics and complex therapeutics gain prominence, pharmaceutical manufacturers increasingly require advanced formulation technologies to improve solubility and stability. Cyclodextrins and modified polysaccharides play a critical role in enabling these advancements, ensuring consistent demand growth aligned with global healthcare innovation.Infant nutrition represents around 12% of total applications, supported by rising demand for premium infant formulas designed to replicate the functional benefits of human milk.

Distribution Channel Insights

The specialty carbohydrate market operates through a predominantly business-to-business supply structure, reflecting the ingredient-centric nature of the industry. Direct B2B ingredient supply dominates distribution channels, accounting for more than 60% of total market share. Large food, pharmaceutical, and nutraceutical manufacturers typically establish long-term procurement partnerships with ingredient producers to ensure consistent quality, regulatory compliance, and supply chain stability. This channel benefits from customized formulations, technical collaboration, and large-volume purchasing agreements.The leading distribution driver lies in increasing formulation complexity, which requires close cooperation between ingredient suppliers and manufacturers during product development stages. Producers increasingly provide application-specific solutions, technical consulting, and co-innovation services, strengthening direct supply relationships and reducing reliance on intermediaries.Ingredient distributors account for approximately 25% share, playing a crucial role in regional market expansion and accessibility for small and mid-sized manufacturers. Distributors bridge logistical gaps by offering localized inventory management, regulatory guidance, and smaller order quantities. Their role is particularly important in emerging markets where direct supplier presence may be limited.Online specialty ingredient platforms and contract manufacturing supply chains collectively represent nearly 15% of distribution. Digital procurement platforms are gaining traction as manufacturers adopt data-driven sourcing strategies and streamlined purchasing processes. Increased transparency, price comparison capabilities, and faster procurement cycles are encouraging gradual migration toward digital sourcing ecosystems, especially among innovative startups and niche product developers.

End-Use Industry Insights

End-use industries for specialty carbohydrates continue to evolve alongside global nutrition trends, technological innovation, and consumer lifestyle changes. The functional food industry represents the fastest-growing end-use sector, expanding at approximately 10–11% CAGR. Rising awareness of preventive health, digestive wellness, and personalized nutrition has fundamentally reshaped food consumption patterns. Consumers increasingly prioritize products offering functional benefits such as improved gut health, sustained energy release, and metabolic balance, driving widespread adoption of specialty carbohydrates across product categories.The leading growth driver for this segment is the convergence of nutrition science and food technology. Manufacturers are developing multifunctional products that combine taste, convenience, and health benefits, supported by specialty carbohydrate ingredients that enhance both functionality and sensory performance. Growth in plant-based diets, clean-label formulations, and fortified foods further accelerates demand.The global dietary supplements industry, valued above USD 190 billion, remains a major demand contributor as consumers shift toward proactive health management. Specialty carbohydrates serve as carriers, stabilizers, and active functional ingredients in supplement formulations. Meanwhile, pharmaceutical demand continues expanding alongside biologics manufacturing and advanced therapeutic development, ensuring steady long-term consumption across healthcare applications.Export-driven demand remains particularly strong in Europe and North America, where manufacturers produce high-value functional foods and nutraceutical products for global distribution. Emerging applications are also gaining traction, including plant-based meat analogues requiring texture-enhancing carbohydrates and sports nutrition formulations designed to optimize energy delivery and recovery performance. These emerging uses highlight the expanding role of specialty carbohydrates beyond traditional food applications into performance nutrition and alternative protein innovation.

| By Product Type | By Source | By Application | By Functionality | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 34% of the global specialty carbohydrate market in 2025, maintaining its leadership position due to advanced food innovation ecosystems and strong consumer adoption of functional nutrition products. The United States represents the largest contributor, supported by a mature nutraceutical industry, high consumer awareness regarding gut health, and extensive investment in research and development. Food manufacturers actively reformulate products to meet clean-label and reduced-sugar requirements, accelerating adoption of specialty carbohydrate ingredients.Regional growth is driven by multiple structural factors, including rising healthcare costs encouraging preventive nutrition, widespread availability of dietary supplements, and strong collaboration between ingredient companies and academic research institutions. Expansion of personalized nutrition platforms and microbiome-based health solutions further increases demand for prebiotic ingredients. Canada contributes significantly through innovation in dairy alternatives, clinical nutrition products, and sustainable food technologies. The presence of major multinational food and pharmaceutical companies ensures continuous product innovation and commercialization across the region.

Europe

Europe holds nearly 27% of global market share, supported by stringent regulatory frameworks promoting sugar reduction and healthier food formulations. Countries such as Germany, France, and the Netherlands serve as major innovation hubs, combining strong food science expertise with advanced ingredient manufacturing capabilities. European consumers demonstrate high awareness of digestive health and sustainability, encouraging adoption of fiber-enriched and functional food products.Regional growth drivers include government-led nutrition policies targeting obesity reduction, widespread acceptance of plant-based diets, and strong demand for organic and clean-label ingredients. The European Food Safety Authority’s structured regulatory environment enhances consumer trust in functional claims, supporting long-term market stability. Additionally, robust export activity from European food manufacturers contributes to sustained ingredient demand, as functional products developed within the region reach global markets.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 11%. Rapid urbanization, rising disposable income, and evolving dietary patterns are transforming food consumption across the region. China dominates demand through large-scale infant nutrition manufacturing and expanding functional beverage production. Japan remains a global leader in functional carbohydrate innovation, supported by decades of research into prebiotics and digestive health ingredients.Regional growth is strongly driven by increasing middle-class populations seeking premium nutrition products, expanding dietary supplement markets, and modernization of food processing infrastructure. India is emerging as a high-growth market due to rapid expansion of dietary supplements, increasing health awareness among younger consumers, and growing investments in food processing and nutraceutical manufacturing. Government initiatives promoting food fortification and healthcare accessibility further support adoption. Southeast Asian markets also contribute through rising demand for fortified beverages and convenience foods aligned with urban lifestyles.

Middle East & Africa

The Middle East & Africa region accounts for roughly 6% of global market share, supported by improving healthcare infrastructure and increasing awareness of nutrition-related health outcomes. Countries such as the UAE and Saudi Arabia are investing heavily in healthcare modernization and food security initiatives, encouraging adoption of fortified and functional food products.Regional growth drivers include rising prevalence of lifestyle-related diseases, government-backed nutrition programs, and increasing imports of high-value functional food ingredients. Expansion of modern retail channels and growing consumer purchasing power are gradually improving market accessibility. Additionally, demand for specialized clinical nutrition products is increasing alongside healthcare sector expansion, supporting steady long-term growth prospects.

Latin America

Latin America represents approximately 6% of the global specialty carbohydrate market, led by Brazil and Mexico. The region is witnessing gradual transformation toward healthier food consumption patterns, particularly through rising demand for functional beverages and sugar-reduced products. Food manufacturers increasingly adopt specialty carbohydrates to comply with nutritional labeling regulations and evolving consumer expectations.Regional growth is driven by expanding urban populations, improving food processing capabilities, and increasing exports of processed food products to North America and Europe. Government initiatives promoting nutritional transparency and reduced sugar consumption further stimulate ingredient adoption. Additionally, growing sports nutrition and wellness trends among younger consumers are creating new opportunities for functional carbohydrate applications across beverage and supplement categories.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Specialty Carbohydrate Market

- Ingredion Incorporated

- DSM-Firmenich

- DuPont Nutrition & Biosciences

- Tate & Lyle PLC

- Roquette Frères

- Cargill Incorporated

- BENEO GmbH

- Glycosyn LLC

- Yakult Pharmaceutical Industry Co., Ltd.

- FrieslandCampina Ingredients

- Archer Daniels Midland Company

- Nissin Sugar Co., Ltd.

- Cosucra Groupe Warcoing

- Sudzucker AG

- Kerry Group plc