Soybean Food & Beverage Products Market Size

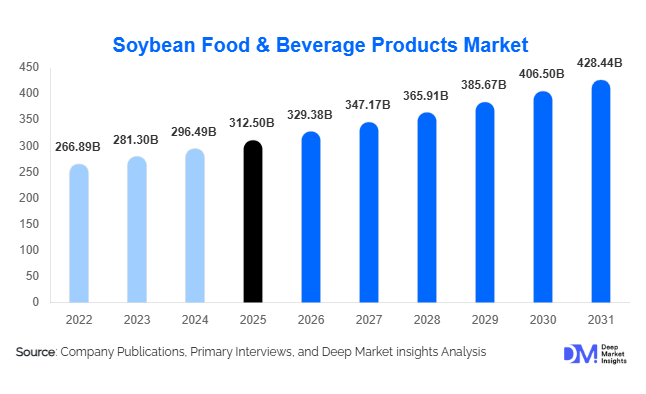

According to Deep Market Insights, the global soybean food & beverage products market size was valued at USD 312.5 billion in 2025 and is projected to grow from USD 329.38 billion in 2026 to reach USD 428.44 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). Market growth is primarily driven by rising global demand for plant-based protein, expanding lactose-intolerant and flexitarian populations, and increasing integration of soy ingredients across retail, foodservice, and clinical nutrition sectors.

Key Market Insights

- Asia-Pacific dominates global consumption, accounting for nearly 48% of total market revenue in 2025, supported by strong traditional soy food consumption in China and Japan.

- Soy-based beverages represent the largest product category, contributing approximately 26% of global market value due to widespread adoption of soy milk and RTD protein drinks.

- Retail consumer packaged foods account for nearly 46% of total demand, reflecting strong supermarket penetration and private-label expansion.

- Modern retail channels lead distribution, holding about 41% share due to organized retail expansion and e-commerce integration.

- Clinical and sports nutrition applications are the fastest-growing segments, supported by aging populations and preventive healthcare trends.

- Technological advancements in protein extraction and flavor neutralization are improving product quality and expanding applications in beverages and high-protein snacks.

What are the latest trends in the soybean food & beverage products market?

Premiumization of Plant-Based Protein Products

Manufacturers are increasingly moving beyond commodity soy products toward premium, value-added offerings such as fortified soy beverages, high-protein yogurts, and functional soy-based meal replacements. Advances in enzymatic processing and ultrafiltration technologies have significantly reduced off-flavors traditionally associated with soy protein, enabling manufacturers to position products within premium dairy-alternative and sports nutrition categories. Clean-label formulations, non-GMO certifications, and organic variants are gaining traction, particularly in North America and Europe. As a result, brands are achieving higher margins in specialized applications such as protein-fortified beverages and clinical nutrition products.

Expansion of Soy in Hybrid and Alternative Meat Applications

Soy continues to play a foundational role in plant-based meat formulations due to its complete amino acid profile and cost efficiency. High-moisture extrusion technology has enhanced texture replication, improving consumer acceptance of soy-based meat analogues. Foodservice chains and quick-service restaurants are incorporating soy-based patties, nuggets, and sausages into mainstream menus. Additionally, hybrid meat products, combining animal protein with soy protein, are emerging as a transitional solution for flexitarian consumers seeking reduced meat consumption without sacrificing taste or affordability.

What are the key drivers in the soybean food & beverage products market?

Rising Global Demand for Plant-Based Protein

Consumer preference is steadily shifting toward plant-based protein sources due to environmental concerns, health awareness, and dietary restrictions. Soy remains the most commercially scalable plant protein globally, offering a complete amino acid profile at competitive production costs. Increasing vegan and flexitarian populations in the U.S., Europe, and parts of Asia are fueling retail demand for soy beverages, tofu, and meat alternatives.

Cost Competitiveness Compared to Alternative Proteins

Compared to almond, oat, and pea protein, soy protein maintains a 20–30% cost advantage on a per-gram protein basis. This pricing stability makes soy particularly attractive in emerging markets and institutional procurement programs such as school feeding initiatives and hospital nutrition programs. Its well-established global supply chain further supports consistent availability.

What are the restraints for the global market?

Competition from Emerging Plant Proteins

The rapid growth of oat, pea, and almond-based alternatives presents competitive pressure, particularly in Western dairy-alternative markets. Consumer perceptions around soy allergens and GMO concerns can influence purchasing behavior, requiring brands to invest heavily in labeling transparency and certification.

Raw Material Price Volatility

Global soybean production is concentrated in key exporting nations, making the industry vulnerable to climate disruptions and geopolitical trade fluctuations. Price volatility affects processing margins, particularly for manufacturers operating within commodity-driven ingredient segments.

What are the key opportunities in the soybean food & beverage industry?

Clinical and Infant Nutrition Expansion

Soy-based infant formulas and medical nutrition products represent high-margin opportunities. Rising lactose intolerance rates and dairy allergies are driving adoption. Aging populations in Japan and Europe are increasing demand for muscle-preserving soy protein supplements, positioning clinical nutrition as a high-growth application area.

Emerging Market Penetration and Government Support

Governments in India, China, and Brazil are encouraging domestic protein processing through industrial incentives and food security programs. Initiatives aligned with manufacturing expansion policies such as “Make in India” and “Made in China 2026” are accelerating plant-protein capacity investments, creating opportunities for both domestic producers and multinational investors.

Product Type Insights

Soy-based beverages remain the leading product segment, accounting for approximately 26% of global market value in 2025. Soy milk continues to dominate within this category due to its price competitiveness, nutritional completeness, and widespread availability across both developed and emerging markets. Rising lactose intolerance rates, dairy price volatility, and strong penetration in modern retail channels primarily drive the segment’s leadership. In Asia-Pacific, soy milk is a staple beverage, while in North America and Europe, it serves as a mainstream dairy alternative. Growth is further supported by product innovation in flavored, fortified, and high-protein RTD variants, which command premium pricing.

Soy-based protein foods, including tofu, tempeh, and textured soy protein (TSP), represent the second-largest category, supported by deep-rooted culinary integration in China and Southeast Asia and growing adoption in Western plant-based meat formulations. The segment benefits from the expansion of high-moisture extrusion technology, which improves meat analogue texture and scalability. Fermented soy foods such as miso and soy sauce maintain stable and culturally embedded demand in Japan and Korea, driven by daily dietary consumption patterns and export expansion. Food-grade soy ingredients, including soy protein isolate, concentrate, flour, lecithin, and fiber, play a critical role in B2B processed food manufacturing. Their demand is driven by protein fortification trends in bakery, confectionery, ready meals, and snack bars. Meanwhile, soy-based infant and clinical nutrition, though smaller in overall share, represents the fastest-growing segment due to increasing pediatric dairy allergies and rising geriatric protein supplementation needs, particularly in Japan, Germany, and the U.S.

Application Insights

Retail consumer packaged foods account for approximately 46% of total market demand in 2025, making it the leading application segment. Supermarket and hypermarket sales of soy beverages, tofu, and plant-based dairy alternatives drive this dominance. The segment’s growth is propelled by private-label expansion, increased shelf visibility, and competitive pricing strategies that position soy products as affordable protein sources.

Foodservice and quick-service restaurants are increasingly incorporating soy-based meat substitutes and hybrid protein formulations to address flexitarian demand and reduce ingredient costs. This is particularly visible in the U.S., the UK, and urban China. Functional and sports nutrition is expanding at nearly 7% CAGR, supported by global gym culture, preventive healthcare awareness, and rising consumption of protein powders and fortified beverages. Processed food manufacturers are also integrating soy isolates into bakery, confectionery, and ready-meal formulations to enhance protein content, improve emulsification, and stabilize textures, further reinforcing soy’s functional versatility across industrial applications.

Distribution Channel Insights

Modern retail channels lead distribution with approximately 41% of total global sales, driven by organized retail expansion in Asia-Pacific and strong supermarket penetration in North America and Europe. The growth of private-label soy beverages and dairy alternatives has strengthened retail bargaining power while maintaining affordability for consumers. E-commerce represents the fastest-growing channel, particularly for premium soy protein powders, clinical nutrition products, and fortified beverages. Online platforms enable subscription-based models and direct-to-consumer engagement, improving brand loyalty and margin realization. Specialty health and organic stores maintain strong traction in developed markets where consumers prioritize non-GMO and clean-label certifications. Institutional sales, covering hospitals, schools, and public nutrition programs, provide steady bulk demand, particularly in emerging economies where governments promote plant-based protein fortification in feeding programs.

End-Use Industry Insights

Retail packaged food remains the largest end-use segment, valued at over USD 140 billion in 2025 within the total market structure. Growth is supported by rising urbanization, increasing disposable incomes in Asia, and the expansion of cold-chain logistics that facilitate tofu and soy yogurt distribution. Functional and sports nutrition continues to outpace the broader market at nearly 7% CAGR, fueled by demand for muscle recovery and weight management solutions. Clinical nutrition demand is expanding steadily in Japan, Germany, and the United States, driven by aging populations and hospital procurement programs. Export-driven demand also remains significant, with the United States and Brazil supplying soy protein isolates and concentrates to Europe and Asia for processed food manufacturing. This B2B export ecosystem strengthens global supply integration and stabilizes ingredient demand.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global soybean food & beverage products market with approximately 48% share in 2025, supported by entrenched dietary reliance on soy-based foods. China alone accounts for nearly 22% of global demand, driven by high consumption of tofu, soy milk, and soy ingredients across urban and rural populations. Government food security initiatives and protein diversification policies further reinforce domestic processing capacity expansion. Japan maintains strong demand for fermented soy products, particularly through established manufacturers, supported by stable domestic consumption and exports. India is the fastest-growing country in the region, with an estimated CAGR above 7%, fueled by protein fortification programs, rising vegetarian demographics, and rapid organized retail expansion.

North America

North America accounts for approximately 24% of the global market share, led by the United States at nearly 20%. Regional growth is driven by rising adoption of plant-based dairy alternatives, innovation in soy-based meat substitutes, and strong sports nutrition consumption. Companies such as these have accelerated product development and consumer acceptance of soy-protein-based formulations. Growth is also supported by high disposable income, advanced retail infrastructure, and expanding e-commerce channels. Canada demonstrates steady growth driven by health-conscious consumers and strong regulatory clarity around plant-based labeling.

Europe

Europe represents roughly 17% of global demand, with Germany, the UK, and France leading plant-based adoption. Regional growth is strongly influenced by sustainability mandates, carbon-reduction targets, and high awareness of the environmental impacts of animal protein. EU policies encouraging alternative proteins and transparent labeling frameworks have enhanced consumer confidence. Expansion of private-label soy beverages and increased demand for organic and non-GMO certified products further drive market momentum.

Latin America

Latin America holds around 7% market share, led by Brazil and Argentina. While traditionally export-oriented soybean producers, these countries are witnessing growing domestic consumption of soy-based processed foods due to urbanization and middle-class income growth. Investment in domestic processing infrastructure is gradually shifting part of the value chain toward higher-margin food and beverage products rather than raw exports.

Middle East & Africa

This region accounts for approximately 4% of global demand, with growth primarily driven by dairy alternative imports and increasing urban health awareness. The UAE and South Africa represent key demand hubs due to higher per capita income and expanding modern retail networks. Rising lactose intolerance awareness and growing expatriate populations further contribute to soy beverage adoption. Gradual expansion of foodservice chains and supermarket infrastructure across Gulf Cooperation Council (GCC) countries supports continued growth in the medium term.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Soybean Food & Beverage Products Market

- Archer Daniels Midland Company

- Cargill Incorporated

- DuPont de Nemours Inc.

- Wilmar International Ltd

- Bunge Global SA

- Fuji Oil Holdings Inc.

- The Hain Celestial Group Inc.

- Danone SA

- Vitasoy International Holdings Ltd

- Kikkoman Corporation

- The Kellogg Company

- Impossible Foods Inc.

- Beyond Meat Inc.

- House Foods Group Inc.

- SunOpta Inc.