Soya Milk Market Size

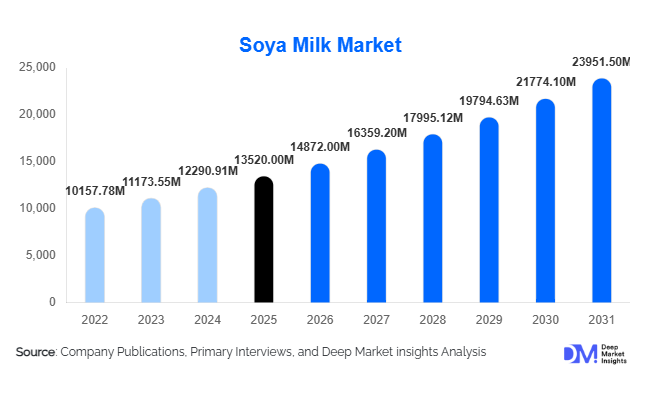

According to Deep Market Insights,the global soya milk market size was valued at USD 13,520 million in 2025 and is projected to grow from USD 14,872 million in 2026 to reach USD 23,951.50 million by 2031, expanding at a CAGR of 10.0% during the forecast period (2026–2031). The soya milk market growth is primarily driven by increasing adoption of plant-based diets, rising lactose intolerance awareness, growing demand for sustainable dairy alternatives, and expanding applications across foodservice and functional beverage industries. Continuous product innovation, including fortified and flavored formulations, along with expanding retail and e-commerce penetration, is transforming soya milk from a niche health product into a mainstream global beverage category.

Key Market Insights

- Plant-based nutrition trends are accelerating global demand, with soy milk remaining the most protein-rich and nutritionally comparable dairy alternative.

- Fortified and functional soy beverages are gaining traction, driven by demand for calcium, vitamin B12, and protein-enriched products.

- Asia-Pacific dominates global consumption due to long-standing soy consumption traditions and large population bases.

- Foodservice adoption is expanding rapidly, particularly among coffee chains using barista-grade soy milk.

- Online grocery platforms are emerging as the fastest-growing distribution channel, supporting premium product penetration.

- Sustainability concerns surrounding dairy production are encouraging consumers and retailers to shift toward plant-based beverages.

What are the latest trends in the soya milk market?

Functional and Fortified Plant-Based Beverages Rising

Soya milk manufacturers are increasingly developing functional formulations enriched with vitamins, minerals, probiotics, and added protein to address evolving consumer health priorities. Calcium- and vitamin-enriched soy milk products are particularly popular among vegan consumers and aging populations seeking bone health support. Clean-label positioning and reduced-sugar formulations are becoming essential competitive differentiators. Brands are also launching immunity-support and sports-nutrition variants, enabling premium pricing strategies while expanding consumer demographics beyond traditional dairy-alternative buyers.

Technology-Driven Flavor and Texture Improvements

Technological innovation is significantly improving soy milk taste and mouthfeel, historically considered barriers to adoption. Advanced enzyme processing and protein stabilization technologies are reducing the characteristic “beany” flavor while improving foamability for café applications. Ultra-high temperature processing and aseptic packaging innovations are extending shelf life and enabling global export expansion. Digital retail analytics and AI-driven demand forecasting are further helping manufacturers optimize production planning and personalize product offerings across regions.

What are the key drivers in the soya milk market?

Growing Adoption of Plant-Based Diets

The increasing global shift toward vegan, vegetarian, and flexitarian diets is a primary driver of soy milk demand. Consumers are reducing animal product consumption due to health, ethical, and environmental considerations. Soy milk benefits from strong consumer familiarity and nutritional advantages, particularly its complete amino acid profile comparable to dairy milk. Expanding plant-based product ecosystems across supermarkets and restaurants continue to normalize consumption.

Rising Lactose Intolerance Awareness

A significant portion of the global population experiences lactose intolerance, particularly in Asia-Pacific and parts of Africa and Latin America. Soy milk provides a lactose-free alternative suitable for daily consumption, driving widespread household adoption. Healthcare professionals increasingly recommend plant-based beverages for digestive health, reinforcing consumer confidence and long-term market growth.

What are the restraints for the global market?

Flavor Perception and Consumer Acceptance Challenges

Despite technological improvements, certain consumers still perceive soy milk as having a distinct aftertaste compared with dairy milk or newer plant alternatives like oat milk. Overcoming taste perception requires continuous R&D investment and flavor innovation, increasing production costs for manufacturers.

Allergy Concerns and GMO Sensitivity

Soy allergies and consumer concerns regarding genetically modified crops pose challenges for market expansion. Manufacturers must invest in non-GMO sourcing certifications, transparent labeling, and supply chain traceability to maintain consumer trust, particularly in North America and Europe.

What are the key opportunities in the soya milk industry?

Expansion into Functional Nutrition and Clinical Applications

The growing functional beverage sector presents substantial opportunities for soy milk producers. Protein-rich formulations targeting elderly nutrition, sports recovery, and medical nutrition markets are gaining popularity. Hospitals, wellness centers, and nutrition programs increasingly adopt fortified plant-based beverages, enabling companies to diversify revenue streams beyond retail consumption.

Foodservice and Coffee Chain Partnerships

The rapid expansion of specialty coffee culture globally is creating sustained demand for soy milk as a dairy substitute. Barista-friendly formulations with improved frothing properties allow cafés and quick-service restaurants to standardize plant-based beverage offerings. Long-term supply contracts with foodservice operators provide stable volume growth and strengthen brand visibility among younger consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13520 Million |

| Market Size in 2026 | USD 14872 Million |

| Market Size in 2031 | USD 23951.50 Million |

| CAGR | 10% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global soy milk market is primarily led by plain or original soy milk, which accounts for nearly 38% of total demand due to its affordability, wide availability, and versatility across daily consumption occasions. Consumers increasingly incorporate plain soy milk into beverages, breakfast cereals, and home cooking, making it a staple dairy alternative in both developed and emerging markets. The dominance of this segment is driven by its neutral taste profile, competitive pricing compared to flavored or premium variants, and suitability for both direct consumption and food preparation applications. Flavored soy milk variants, including chocolate, vanilla, and fruit-infused options, are expanding steadily as younger consumers seek convenient, ready-to-drink plant-based beverages that combine nutrition with taste appeal. Meanwhile, fortified soy milk is emerging as the fastest-growing category, supported by rising awareness of micronutrient deficiencies and increasing demand for calcium-, vitamin D-, and protein-enriched plant-based beverages among vegan and lactose-intolerant populations. Organic soy milk continues to gain traction in developed economies where clean-label preferences, non-GMO sourcing, and sustainability considerations strongly influence purchasing decisions, further supported by premium retail positioning and transparent supply chains.

Application Insights

Household consumption remains the dominant application segment, representing approximately 58% of global demand as soy milk becomes increasingly embedded in everyday dietary routines. The leading driver for this segment is the growing consumer shift toward plant-based nutrition combined with the practicality of soy milk as a multifunctional ingredient used in beverages, cereals, baking, and cooking. Increasing lactose intolerance awareness and rising adoption of flexitarian diets continue reinforcing household penetration globally. Foodservice applications are witnessing rapid expansion as cafés, quick-service restaurants, and specialty beverage outlets incorporate plant-based milk options to cater to evolving consumer preferences. Barista-grade soy milk products designed for foam stability and taste consistency are accelerating adoption within coffee chains and independent cafés. Food and beverage manufacturers are also expanding soy milk utilization as a base ingredient for dairy-free yogurts, desserts, smoothies, and functional beverages, driven by innovation in plant-based product formulations. Clinical and nutritional applications are emerging as niche yet high-value segments, particularly in aging populations where soy milk’s protein content and cholesterol-free properties support dietary management and specialized nutrition programs.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global soy milk distribution, contributing nearly 46% of total revenue owing to strong shelf visibility, established consumer trust, and the ability to offer diverse product assortments across price tiers. The leading growth driver within this channel is large-scale retail expansion combined with private-label product penetration, which enhances affordability and accessibility for mass-market consumers. Online retail represents the fastest-growing distribution channel, fueled by the rapid adoption of digital grocery platforms, subscription-based purchasing models, and increasing consumer preference for convenience-driven shopping experiences. E-commerce also enables niche and premium brands to reach wider audiences without traditional retail constraints. Specialty health stores continue to play an important role in promoting organic, fortified, and functional soy milk variants, particularly among health-conscious consumers seeking curated wellness products. Foodservice distribution channels are expanding steadily through strategic partnerships between manufacturers and cafés, institutional buyers, and hospitality providers, strengthening bulk purchasing volumes and consistent supply demand.

End-Use Insights

Household consumers represent the largest end-use segment globally, driven by the integration of soy milk into daily nutrition routines and the increasing perception of plant-based beverages as healthier long-term dietary choices. The leading driver for this segment is the growing replacement of traditional dairy products with plant-based alternatives among health-conscious and lactose-intolerant consumers. The foodservice sector is the fastest-growing end-use category, expanding at double-digit growth rates as cafés, restaurants, and beverage chains actively diversify menus with plant-based options to meet consumer expectations. Increased demand for specialty coffee beverages prepared with dairy alternatives continues accelerating adoption across urban markets. Industrial food processing applications are also expanding as manufacturers utilize soy milk in dairy-alternative product development, including frozen desserts, bakery formulations, and ready-to-drink nutritional beverages. Additionally, export-driven demand from Asia-Pacific producers supplying North American and European markets is strengthening global trade flows, enhancing production scale and encouraging international brand expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Soya Milk Market Segmentations

By Product Type

- Plain/Original Soya Milk

- Flavored Soya Milk (Chocolate, Vanilla, Fruit-Based)

- Fortified Soya Milk (Calcium, Vitamin, Protein-Enriched)

- Organic & Non-GMO Soya Milk

- Barista & Specialty Soya Milk

By Application

- Household Consumption

- Foodservice & Cafés

- Food & Beverage Processing

- Clinical & Nutritional Applications

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-commerce Platforms

- Specialty Health & Organic Stores

- Foodservice & Institutional Distribution

Regional Insights

North America

North America accounts for roughly 22% of the global soy milk market, led by strong consumption in the United States and Canada. Regional growth is driven by increasing vegan and flexitarian populations, heightened sustainability awareness, and widespread availability of plant-based products across modern retail networks. The expansion of fortified and organic soy milk variants reflects consumer demand for functional nutrition and clean-label products. Additionally, innovation by foodservice chains and specialty coffee retailers incorporating dairy alternatives into beverages continues stimulating demand growth. Rising health consciousness, growing lactose intolerance awareness, and strong marketing by plant-based brands further reinforce long-term market expansion across the region.

Europe

Europe represents approximately 18% of global demand, with Germany, the United Kingdom, France, and the Netherlands serving as key markets. Regional growth is supported by stringent environmental regulations encouraging reduced dairy consumption and increased adoption of sustainable food systems. Government-backed sustainability initiatives, expanding vegan product availability, and strong private-label penetration are improving affordability and accessibility. Consumers increasingly prioritize ethically sourced and non-GMO ingredients, driving demand for organic and fortified soy milk. In addition, rising innovation in plant-based product formulations and strong retail competition among supermarket chains continue accelerating market development across Western and Northern Europe.

Asia-Pacific

Asia-Pacific dominates the global soy milk market with nearly 46% market share, supported by deep-rooted cultural familiarity with soy-based beverages and large population bases. China remains the largest consumer due to longstanding dietary traditions and widespread domestic production capacity. Japan and South Korea demonstrate strong demand for premium and functional soy milk products emphasizing nutritional enrichment and convenience packaging. India is emerging as the fastest-growing market, driven by rapid urbanization, increasing lactose intolerance prevalence, rising disposable incomes, and expanding awareness of plant-based nutrition among younger consumers. Growth across Southeast Asia is further supported by expanding retail infrastructure, affordable pricing, and increasing investments by regional manufacturers.

Latin America

Latin America holds around 8% of the global market, led by Brazil and Mexico. Regional growth is primarily driven by expanding middle-class populations, increasing health awareness, and growing demand for affordable dairy alternatives. Improvements in retail distribution networks and local manufacturing investments are enhancing product availability and reducing price barriers. Rising interest in functional beverages and increasing adoption of plant-based diets among urban consumers are also contributing to steady market expansion. Additionally, regional brands are introducing localized flavors and cost-effective packaging formats to strengthen consumer acceptance.

Middle East & Africa

The Middle East and Africa account for nearly 6% of global demand but represent the fastest-growing regional market. Growth is supported by rising disposable incomes, expanding modern retail infrastructure, and increasing expatriate populations familiar with plant-based beverages. Urbanization and lifestyle changes are encouraging healthier dietary choices, while growing hospitality and café industries are expanding foodservice consumption of soy milk. Countries such as the UAE, Saudi Arabia, and South Africa are witnessing increased product availability through international brand entry and retail modernization, alongside rising awareness of lactose intolerance and nutritional diversification.

Key Players in the Soya Milk Market

- Danone S.A.

- Vitasoy International Holdings Ltd.

- Kikkoman Corporation

- Nestlé S.A.

- The Hain Celestial Group

- SunOpta Inc.

- Eden Foods Inc.

- Pacific Foods (Campbell Soup Company)

- Sanitarium Health Food Company

- Organic Valley

- Pureharvest

- American Soy Products Inc.

- Blue Diamond Growers

- Oatly Group AB

- Alpro (Danone brand)