Soy Isoflavones Supplements Market Size

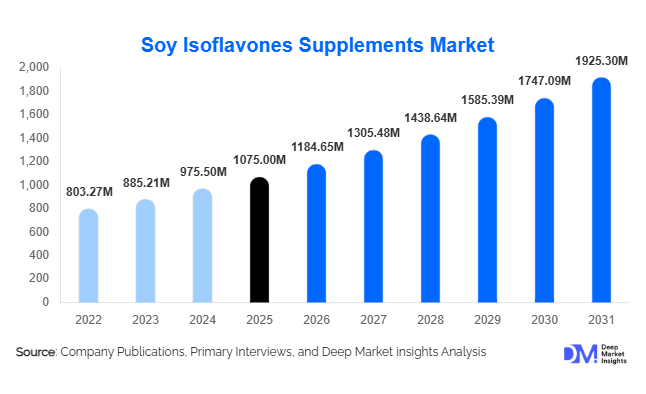

According to Deep Market Insights,the global soy isoflavones supplements market size was valued at USD 1,075 million in 2025 and is projected to grow from USD 1,184.65 million in 2026 to reach USD 1,925.30 million by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). Market growth is primarily driven by increasing adoption of plant-based nutraceuticals, rising awareness regarding menopause and hormonal health management, and growing consumer preference for natural alternatives to hormone replacement therapies. Expanding preventive healthcare spending, coupled with rapid growth in online supplement retail channels, is further accelerating global demand for soy isoflavones supplements.

Key Market Insights

- Plant-based hormone support supplements are gaining widespread adoption as consumers increasingly prefer natural phytoestrogen solutions over synthetic therapies.

- Women aged 40–60 years represent the largest consumer demographic, driven by menopause management and bone health applications.

- North America dominates global consumption due to strong nutraceutical penetration and high preventive healthcare expenditure.

- Asia-Pacific is the fastest-growing region, supported by traditional soy consumption and expanding middle-class health awareness.

- Online retail and direct-to-consumer channels are transforming supplement distribution through subscription-based wellness models.

- Technological advancements in extraction and bioavailability enhancement are enabling premium, high-potency formulations.

What are the latest trends in the soy isoflavones supplements market?

Shift Toward Clean-Label and Non-GMO Supplements

Consumers are increasingly prioritizing transparency, sustainability, and ingredient traceability when purchasing dietary supplements. Non-GMO and organic-certified soy isoflavones are gaining strong traction, particularly in North America and Europe. Manufacturers are investing in identity-preserved soybean sourcing and clean-label certifications to differentiate products in a competitive nutraceutical landscape. This trend is also supported by regulatory emphasis on labeling clarity and growing consumer scrutiny regarding genetically modified ingredients. Premium positioning of certified formulations allows brands to command higher pricing while improving consumer trust and long-term brand loyalty.

Integration of Personalized Nutrition Platforms

Digital health ecosystems are reshaping supplement consumption through personalized nutrition solutions. Companies are integrating soy isoflavones into customized supplement packs tailored to hormonal stage, age, and metabolic needs. AI-driven wellness platforms and subscription-based delivery models are increasing consumer retention while enabling precise dosing recommendations. Personalized supplement strategies are particularly appealing to younger consumers adopting preventive healthcare practices earlier in life. This evolution is transforming soy isoflavones from a niche menopause supplement into a broader lifestyle wellness ingredient.

What are the key drivers in the soy isoflavones supplements market?

Growing Global Menopause Population

The rising population of women entering menopause is a primary driver of market expansion. Increasing awareness regarding symptoms such as hot flashes, hormonal imbalance, and bone density loss is encouraging adoption of phytoestrogen-based supplements. Soy isoflavones provide a plant-derived alternative that supports long-term use, making them increasingly recommended within preventive healthcare programs. Healthcare practitioners are also incorporating nutraceutical solutions into holistic treatment strategies, further strengthening demand.

Expansion of Preventive Healthcare and Nutraceutical Consumption

Consumers globally are shifting from reactive treatment toward preventive wellness approaches. Nutraceutical supplements addressing cardiovascular health, hormonal balance, and aging-related concerns are experiencing strong adoption. Soy isoflavones align with this trend by offering antioxidant and metabolic benefits beyond menopause support. Rising disposable incomes and increasing health awareness in emerging economies are accelerating supplement penetration across new consumer groups.

What are the restraints for the global market?

Regulatory Variability Across Regions

Differences in health claim approvals and phytoestrogen labeling regulations across countries create commercialization challenges for manufacturers. Companies must adapt marketing strategies and formulations to meet varying compliance requirements, increasing operational complexity and product launch timelines.

Raw Material Price Volatility

Soybean supply fluctuations influenced by climate conditions, agricultural yields, and global trade policies affect raw material pricing. Non-GMO and organic sourcing requirements further increase procurement costs, placing pressure on manufacturer margins and retail pricing structures.

What are the key opportunities in the soy isoflavones supplements industry?

Natural Alternatives to Hormone Replacement Therapy

Increasing consumer concern regarding synthetic hormone therapies creates significant opportunities for soy isoflavones supplements positioned as natural hormone-support solutions. Clinical validation and physician-backed formulations are expected to unlock premium healthcare segments and expand adoption across aging populations globally.

Emerging Market Expansion and Healthcare Awareness

Rapid growth in nutraceutical awareness across Asia, Latin America, and the Middle East presents strong opportunities for manufacturers. Rising middle-class populations and expanding pharmacy retail networks are improving supplement accessibility. Localized pricing strategies and educational campaigns are expected to accelerate adoption in developing economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1075 Million |

| Market Size in 2026 | USD 1184.65 Million |

| Market Size in 2031 | USD 1925.30 Million |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Capsules represent the leading product form in the soy isoflavones supplements market, accounting for nearly 38% of global demand. Their dominance is primarily driven by consumer preference for convenience, accurate dosage control, portability, and improved compliance compared to other supplement formats. Capsules also allow manufacturers to incorporate standardized soy isoflavone concentrations while minimizing taste and odor concerns, making them highly suitable for daily supplementation routines. Tablets continue to maintain a strong presence, particularly across pharmacy and drugstore distribution channels, supported by their cost efficiency, longer shelf life, and familiarity among older consumer groups who traditionally rely on conventional supplement formats. Powdered supplements are witnessing growing adoption as personalized nutrition gains momentum, enabling flexible dosing and seamless integration into functional beverages, smoothies, and wellness formulations. Meanwhile, softgels and liquid extracts are emerging as premium product formats designed to enhance bioavailability and absorption efficiency. These formats are increasingly favored by health-conscious consumers seeking faster physiological benefits, thereby supporting innovation and premiumization trends across the market.

Application Insights

Menopause management remains the dominant application segment, contributing approximately 41% of total market demand, primarily driven by strong clinical evidence supporting soy isoflavones in alleviating menopausal symptoms such as hot flashes, hormonal imbalance, and bone density decline. Rising awareness among women regarding natural alternatives to hormone replacement therapy continues to accelerate adoption within this segment. Bone health applications are expanding steadily as aging populations worldwide focus on preventive healthcare strategies aimed at reducing osteoporosis risk and maintaining long-term mobility. Cardiovascular wellness and hormonal balance applications are also gaining traction, supported by increasing research highlighting the role of phytoestrogens in supporting heart health and metabolic regulation. Additionally, skin health and anti-aging applications are emerging rapidly within the nutricosmetics sector, driven by growing consumer interest in beauty-from-within solutions that promote collagen support, skin elasticity, and healthy aging outcomes. The expansion of multifunctional supplements combining hormonal, cardiovascular, and cosmetic benefits further strengthens application diversification.

Distribution Channel Insights

Online retail platforms dominate the distribution landscape, accounting for roughly 32% of global sales, largely driven by increasing digital adoption, subscription-based supplement models, personalized product recommendations, and direct-to-consumer brand strategies. E-commerce channels enable broader product comparison, consumer education, and access to niche formulations, significantly enhancing market penetration. Pharmacies and drug stores continue to play a critical role due to strong consumer trust and healthcare professional recommendations, particularly for menopause-related and clinically positioned supplements. Health and nutrition specialty stores cater to informed consumers seeking premium and scientifically validated products, often supported by in-store expertise and personalized consultation. Supermarkets and hypermarkets contribute to mass-market accessibility by offering convenient purchasing options and expanding private-label supplement portfolios. Practitioner and clinical distribution channels are gradually expanding as integrative and functional medicine practices gain acceptance, encouraging physician-guided supplementation and evidence-based nutraceutical adoption.

Consumer Demographic Insights

Women aged 40–60 years constitute the largest consumer demographic, contributing nearly 48% of overall market demand, primarily due to menopause-related health concerns and increased awareness of hormone-supportive nutritional interventions. This demographic demonstrates high purchasing consistency, driving repeat consumption patterns and long-term supplement adherence. Younger female consumers below the age of 40 are increasingly incorporating soy isoflavones into preventive wellness routines, focusing on hormonal balance, reproductive health, and skin health benefits. The senior population aged above 60 represents a rapidly expanding segment as longevity trends encourage proactive management of cardiovascular health, bone strength, and metabolic wellness. Male consumers are emerging as a niche yet growing demographic, particularly for heart health, cholesterol management, and metabolic support applications, reflecting broader acceptance of plant-based functional ingredients across gender categories.

Explore more data points, trends and opportunities Download Free Sample Report

Soy Isoflavones Supplements Market Segmentations

By Product Form

- Capsules

- Tablets

- Powders

- Softgels

- Liquid Extracts

By Application

- Menopause Management

- Bone Health Support

- Cardiovascular Health

- Hormonal Balance & Wellness

- Skin & Anti-Aging (Nutricosmetics)

By Distribution Channel

- Online Retail & Direct-to-Consumer Platforms

- Pharmacies & Drug Stores

- Health & Nutrition Specialty Stores

- Supermarkets & Hypermarkets

- Practitioner & Clinical Channels

By Consumer Demographics

- Women Aged 40–60 Years

- Women Below 40 Years

- Seniors Above 60 Years

- Male Consumers

Regional Insights

North America

North America accounts for approximately 35% of global market share, supported by high dietary supplement penetration across the United States and Canada. Regional growth is driven by strong consumer awareness regarding menopause management, preventive healthcare adoption, and increasing preference for plant-based nutraceutical solutions. Advanced e-commerce infrastructure, widespread availability of clinically validated products, and growing demand for non-GMO and clean-label formulations contribute to premium product positioning. Additionally, rising healthcare costs are encouraging consumers to adopt preventive supplementation strategies, further strengthening long-term demand growth in the region.

Europe

Europe holds nearly 27% of the global market share, with Germany, France, Italy, and the United Kingdom representing key consumption hubs. Regional expansion is supported by stringent regulatory frameworks that promote standardized formulations, quality certifications, and consumer confidence in nutraceutical products. Increasing focus on women’s health initiatives, aging population dynamics, and strong acceptance of botanical supplements drive steady market growth. Furthermore, growing interest in sustainable and plant-derived ingredients aligns well with soy isoflavones positioning, reinforcing adoption across both preventive healthcare and wellness-oriented consumer segments.

Asia-Pacific

Asia-Pacific represents about 28% of the global market and remains the fastest-growing region, expanding at a CAGR above 11%. Growth is largely driven by cultural familiarity with soy-based foods and traditional dietary practices in countries such as China and Japan, where phytoestrogen consumption has long been integrated into daily nutrition. Rapid urbanization, expanding middle-class populations, and rising disposable incomes in India and Southeast Asia are accelerating nutraceutical adoption. Increasing preventive healthcare awareness, expanding online retail ecosystems, and government initiatives promoting healthy aging further support regional market expansion. Additionally, local manufacturing capabilities and abundant soy raw material availability enhance supply chain efficiency and cost competitiveness.

Latin America

Latin America contributes nearly 6% of global demand, led by Brazil and Mexico. Market growth is supported by expanding middle-class healthcare expenditure, improving awareness of natural and plant-based supplements, and the rapid expansion of organized pharmacy retail networks. Increasing consumer inclination toward preventive wellness and hormonal health solutions is strengthening adoption among female consumers. The growing influence of digital commerce and international supplement brands entering the region is also improving product accessibility and consumer education, supporting gradual market maturation.

Middle East & Africa

The Middle East & Africa region accounts for roughly 4% of the global market, with the UAE and Saudi Arabia emerging as key demand centers. Growth is driven by rising disposable incomes, expanding health-conscious populations, and increasing demand for premium imported nutraceutical products. Greater exposure to global wellness trends, combined with expanding modern retail infrastructure and private healthcare investments, is supporting steady adoption. Additionally, increasing awareness of preventive healthcare and women’s wellness solutions is expected to accelerate long-term market development across the region.

Key Players in the Soy Isoflavones Supplements Market

- Archer Daniels Midland Company

- Cargill Incorporated

- International Flavors & Fragrances Inc.

- DSM-Firmenich

- Kerry Group plc

- Fuji Oil Holdings Inc.

- Symrise AG

- Givaudan SA

- AIDP Inc.

- NOW Health Group Inc.

- Herbalife Ltd.

- Swanson Health Products

- NutraScience Labs

- Naturex (Givaudan)

- Frutarom Industries Ltd.