Soy-Based Infant Formula Market Size

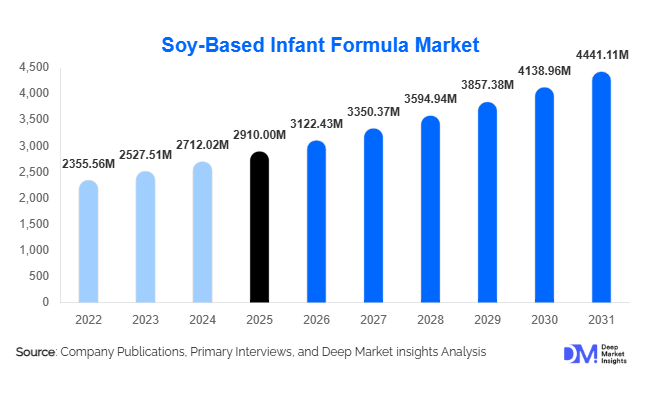

According to Deep Market Insights,the global soy-based infant formula market size was valued at USD 2,910 million in 2025 and is projected to grow from USD 3,122.43 million in 2026 to reach USD 4,441.11 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). Market growth is primarily driven by the rising prevalence of lactose intolerance and cow’s milk protein allergy among infants, increasing parental preference for plant-based nutrition, and expanding access to fortified, non-GMO, and organic soy formulations across developed and emerging economies.

Key Market Insights

- Powder-based soy infant formula dominates the market, accounting for nearly 74% of global revenue share in 2025 due to extended shelf life and cost efficiency.

- Stage 1 (0–6 months) formulations hold the largest demand share, representing approximately 46% of the total market in 2025.

- North America leads the global market, contributing around 32% of 2025 revenue, supported by established pediatric guidelines and high awareness levels.

- Asia-Pacific is the fastest-growing region, expanding at over 8% CAGR due to rising birth rates in select countries and urbanization trends.

- Mid-premium pricing tier captures the highest revenue share, balancing affordability with fortified nutritional claims.

- Institutional demand through hospitals and pediatric clinics is accelerating, supported by government-backed maternal nutrition programs.

What are the latest trends in the soy-based infant formula market?

Shift Toward Organic and Non-GMO Soy Formulations

Consumer demand for clean-label, organic, and non-genetically modified soy-based infant formulas is accelerating across North America and Europe. Parents increasingly scrutinize ingredient sourcing, protein extraction methods, and fortification quality. Manufacturers are responding by introducing certified organic soy isolates, removing artificial additives, and enhancing traceability across supply chains. Premium organic soy formula variants are growing at a CAGR above 9%, significantly outpacing conventional variants. Brands are also strengthening transparency through QR-enabled packaging that allows parents to trace raw material origins and quality testing certifications, reinforcing trust in infant nutrition products.

Advanced Nutritional Fortification and Functional Additives

Technological improvements in protein isolation and micronutrient fortification are reshaping product differentiation. Soy formulas are increasingly fortified with DHA, ARA, probiotics, prebiotics, nucleotides, and iron to closely mimic breast milk composition. These enhancements are improving pediatric acceptance and expanding soy formula beyond a niche lactose-intolerant segment into a broader preventive nutrition category. Innovation in enzymatic treatment processes is also improving digestibility and reducing phytoestrogen-related concerns, strengthening clinical confidence in soy-based products.

What are the key drivers in the soy-based infant formula market?

Rising Incidence of Lactose Intolerance and Milk Protein Allergy

The increasing diagnosis of lactose intolerance and cow’s milk protein allergy among infants is a core growth driver. Pediatricians frequently recommend soy-based formula as a primary alternative in cases of galactosemia or dairy sensitivity. Improved screening protocols and parental awareness are expanding the addressable patient base, particularly in North America, Europe, and parts of Asia.

Growing Adoption of Plant-Based Diets

Millennial and Gen Z parents are increasingly adopting plant-based lifestyles, influencing infant feeding choices. Vegan and vegetarian households are more inclined to select soy-based infant formula to align with ethical and environmental values. This demographic shift is particularly pronounced in urban centers across the United States, Germany, the United Kingdom, Australia, and Canada, contributing to steady demand growth.

What are the restraints for the global market?

Clinical Debate Around Phytoestrogen Exposure

Although soy-based infant formulas meet regulatory safety standards, ongoing discussions regarding phytoestrogen exposure create cautious adoption in certain markets. Consumer perception challenges may limit broader penetration in conservative healthcare systems.

Competition from Hypoallergenic Dairy-Based Alternatives

Extensively hydrolyzed and amino acid-based dairy formulas compete directly with soy-based products in allergy management. Aggressive marketing and premium positioning of hypoallergenic dairy formulas may restrict soy formula’s share in severe allergy cases.

What are the key opportunities in the soy-based infant formula industry?

Expansion in Emerging Markets

Rapid urbanization, increasing female workforce participation, and improving healthcare infrastructure in countries such as China, India, Brazil, Indonesia, and Saudi Arabia present significant growth potential. Public maternal health initiatives and expanding retail networks are improving formula accessibility. Localization of manufacturing under national industrial initiatives is reducing import dependence and lowering price barriers.

Technological Upgradation and Premiumization

Investment in advanced spray-drying facilities, protein purification technologies, and automated packaging systems enables cost optimization and quality enhancement. Premium positioning through organic certification, allergen-free labeling, and fortified nutrient blends is improving profit margins, which currently range between 12% and 18% globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2910 Million |

| Market Size in 2026 | USD 3122.43 Million |

| Market Size in 2031 | USD 4441.11 Million |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Powder soy-based infant formula dominates the global market, contributing approximately 74% of total revenue in 2025. The leadership of the powdered segment is primarily driven by its extended shelf life, cost efficiency in storage and transportation, and suitability for bulk manufacturing and international trade. Powder formulations are less susceptible to spoilage, making them highly preferred in regions with complex distribution networks and varying climatic conditions. Additionally, powdered soy formula offers flexibility in packaging sizes and price positioning, enabling manufacturers to cater to both premium and mass-market consumers. The segment’s dominance is further supported by its compatibility with large-scale retail supply chains and government-supported nutrition programs.

Liquid soy formula, including ready-to-feed and concentrated variants, accounts for the remaining 26% of global revenue. Growth in this segment is largely concentrated in developed economies where convenience, time efficiency, and hygienic preparation are key purchase drivers. Working parents increasingly prefer ready-to-feed options due to ease of use and reduced preparation errors. Although liquid formats involve higher logistics costs and shorter shelf life, demand remains strong in urban markets with advanced cold chain infrastructure and higher disposable incomes.

Age Group Insights

Stage 1 (0–6 months) soy-based infant formula represents nearly 46% of global revenue share in 2025, making it the leading age segment. This dominance is primarily driven by higher feeding frequency during early infancy and increased medical recommendations for soy-based alternatives in cases of lactose intolerance, cow milk protein allergy, or specific dietary restrictions. Parents are particularly cautious during the first six months, resulting in higher expenditure on clinically validated and nutritionally balanced formulations.

Stage 2 (6–12 months) accounts for approximately 34% of total revenue, supported by continued nutritional supplementation as infants transition to semi-solid foods. Demand in this segment is driven by fortified formulations containing iron, DHA, ARA, and probiotics to support cognitive and immune development. Stage 3 (12–24 months) contributes around 20% of market share, benefiting from growing awareness of toddler nutrition, rising dual-income households, and increasing availability of premium fortified blends tailored to digestive health and immunity support.

Distribution Channel Insights

Supermarkets and hypermarkets hold approximately 38% of the 2025 revenue share, making them the leading distribution channel. Their dominance is driven by strong brand visibility, extensive shelf space, promotional pricing strategies, and consumer trust in organized retail. Large retail chains provide access to a broad portfolio of domestic and international brands, enabling parents to compare ingredients, pricing, and certifications in one location.

Pharmacies and drug stores account for around 27% of global revenue, supported by pediatric recommendations and consumer perception of higher product authenticity and safety. Parents often prefer purchasing infant nutrition products from pharmacies due to professional guidance and reassurance regarding regulatory compliance.

Online retail channels are expanding rapidly at a CAGR of over 9%, driven by subscription-based purchasing models, direct-to-consumer strategies, competitive pricing, and the convenience of home delivery. E-commerce platforms are particularly influential in urban areas and among digitally connected parents seeking product reviews, ingredient transparency, and doorstep replenishment services.

Price Tier Insights

The mid-premium segment leads the global soy-based infant formula market with nearly 44% market share in 2025. This segment’s leadership is driven by its balanced positioning between affordability and enhanced nutritional value. Mid-premium products typically offer added micronutrients, digestive support ingredients, and clinically backed formulations at accessible price points, appealing to a broad middle-income consumer base.

Premium and organic variants account for approximately 31% of total revenue, supported by increasing consumer preference for non-GMO ingredients, clean-label formulations, and organic certifications. Demand is particularly strong in developed markets where parents prioritize sustainability, plant-based nutrition, and traceable sourcing. Meanwhile, mass-market economy offerings represent nearly 25% of the market, primarily driven by price-sensitive consumers in emerging economies where affordability and basic nutritional adequacy remain key purchasing factors.

Explore more data points, trends and opportunities Download Free Sample Report

Soy-Based Infant Formula Market Segmentations

By Product Form

- Powder Soy-Based Infant Formula

- Ready-to-Feed Liquid Soy Formula

- Concentrated Liquid Soy Formula

By Infant Stage (Age Group)

- Stage 1 (0–6 Months)

- Stage 2 (6–12 Months)

- Stage 3 (12–24 Months / Toddler Formula)

By Certification & Labeling

- Conventional Soy Formula

- Organic Soy Formula

- Non-GMO Certified Soy Formula

- Allergen-Free / Medical-Grade Soy Formula

By Price Tier

- Mass-Market (Economy)

- Mid-Premium

- Premium / Organic

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Specialty Baby Stores

- Online Retail

- Institutional Sales

Regional Insights

North America

North America accounts for approximately 32% of the global soy-based infant formula market in 2025, with the United States contributing nearly 85% of regional demand. Regional growth is driven by high diagnosis rates of lactose intolerance and cow milk protein allergies, increasing adoption of plant-based nutrition, and strong pediatric endorsement of specialized formulas. The presence of established retail infrastructure, stringent regulatory standards, and high consumer awareness regarding infant health further supports steady demand. Additionally, innovation in fortified and organic soy formulations continues to strengthen product differentiation across the region.

Asia-Pacific

Asia-Pacific holds around 29% of global market share and represents the fastest-growing region, expanding at a CAGR of over 8.5%. Growth is primarily fueled by large infant populations in China and India, rising disposable incomes, expanding urbanization, and increasing maternal workforce participation. Growing awareness of infant nutrition and increasing acceptance of plant-based dietary alternatives are accelerating adoption rates. In mature markets such as Japan and Australia, demand is supported by premiumization trends, advanced healthcare systems, and preference for clinically tested fortified formulas. Expanding e-commerce penetration and cross-border trade further enhance regional growth prospects.

Europe

Europe captures approximately 23% of global revenue, with Germany, France, and the United Kingdom leading regional demand. Growth in Europe is strongly influenced by rising plant-based dietary adoption, stringent regulatory compliance standards, and heightened consumer focus on clean-label and non-GMO products. Increasing prevalence of dairy sensitivities and strong trust in certified infant nutrition brands further contribute to stable demand. The region also benefits from well-established pharmacy distribution networks and advanced healthcare advisory systems that encourage medically guided formula selection.

Latin America

Latin America contributes roughly 9% of global revenue, with Brazil and Mexico emerging as key growth markets. Regional expansion is driven by rapid urbanization, improving healthcare access, rising middle-class populations, and growing awareness of infant nutrition alternatives. Expanding modern retail chains and increased participation of international brands are enhancing product availability. Economic development and gradual improvement in purchasing power are further supporting demand for mid-premium and fortified soy-based formulas.

Middle East & Africa

The Middle East & Africa region accounts for nearly 7% of the global market. Saudi Arabia and South Africa lead regional demand, supported by high import dependency, expanding retail infrastructure, and growing awareness of specialized infant nutrition products. Rising birth rates in select African nations and increasing healthcare investments in Gulf countries are contributing to steady growth. The expansion of supermarket chains and online retail platforms, combined with improving cold chain logistics, is expected to further strengthen regional market penetration over the forecast period.

Key Players in the Soy-Based Infant Formula Market

- Abbott Laboratories

- Nestlé S.A.

- Danone S.A.

- Reckitt Benckiser Group plc

- Perrigo Company plc

- The Kraft Heinz Company

- Beingmate Baby & Child Food Co., Ltd.

- Feihe International

- HiPP GmbH & Co.

- Meiji Holdings Co., Ltd.

- Morinaga Milk Industry Co., Ltd.

- Bellamy’s Organic

- Synutra International

- Arla Foods amba

- Yili Group