Soil Remediation Market Size

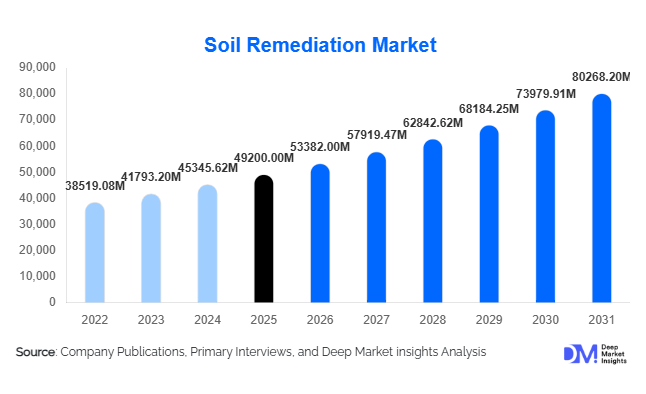

According to Deep Market Insights, the global soil remediation market size was valued at USD 49,200 million in 2025 and is projected to grow from USD 53,382 million in 2026 to reach USD 80,268.20 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The soil remediation market growth is primarily driven by stringent environmental regulations, rising industrial contamination, and increasing demand for sustainable land use and redevelopment. Governments and private stakeholders are actively investing in restoring contaminated land to enable safe agricultural use, infrastructure development, and environmental conservation.

Key Market Insights

- Biological remediation technologies are gaining strong traction, driven by their eco-friendly and cost-effective characteristics compared to traditional methods.

- In-situ remediation dominates the market, as it minimizes soil disturbance and reduces overall project costs.

- North America leads the global market, supported by stringent environmental regulations and large-scale brownfield redevelopment projects.

- Asia-Pacific is the fastest-growing region, driven by rapid industrialization and increasing government initiatives for pollution control.

- Oil & gas and mining industries remain key demand drivers, contributing significantly to soil contamination and remediation needs.

- Technological advancements, including AI-based monitoring and IoT-enabled soil assessment, are improving remediation efficiency and scalability.

What are the latest trends in the soil remediation market?

Shift Toward Sustainable and Bio-Based Remediation

The soil remediation market is witnessing a strong shift toward sustainable solutions such as bioremediation and phytoremediation. These methods leverage natural biological processes to degrade contaminants, offering environmentally friendly alternatives to chemical and physical remediation techniques. Increasing regulatory support for green technologies and growing awareness about ecological conservation are accelerating adoption. Companies are investing in research to enhance microbial efficiency and plant-based remediation capabilities, enabling faster and more effective soil restoration. This trend is particularly prominent in Europe and North America, where sustainability mandates are stringent.

Integration of Digital Technologies in Soil Monitoring

Advanced technologies such as IoT sensors, AI-driven analytics, and remote monitoring systems are transforming soil remediation processes. Real-time data collection enables precise assessment of contamination levels and remediation progress, reducing operational inefficiencies. Predictive analytics is also being used to design optimized remediation strategies, minimizing time and cost. These innovations are especially beneficial for large-scale industrial and mining sites, where continuous monitoring is critical. Digital transformation is expected to become a key differentiator among market players in the coming years.

What are the key drivers in the soil remediation market?

Stringent Environmental Regulations

Governments across the globe are enforcing strict soil quality standards to mitigate environmental and health risks associated with contaminated land. Regulatory frameworks mandate cleanup of industrial sites before redevelopment, significantly driving demand for remediation services. Compliance requirements are particularly stringent in developed regions, compelling industries to adopt advanced remediation technologies.

Expansion of Industrial and Mining Activities

Rapid industrialization and increased mining operations, especially in emerging economies, are contributing to soil contamination. Activities such as oil extraction, chemical manufacturing, and metal processing release hazardous substances into the soil, necessitating remediation. As industries expand, the need for effective soil cleanup solutions continues to grow, supporting market expansion.

Rising Demand for Urban Redevelopment

The growing need to convert contaminated land into usable real estate is a major driver of the soil remediation market. Urbanization and population growth are increasing demand for land, encouraging governments and developers to invest in brownfield redevelopment projects. Soil remediation plays a critical role in enabling safe construction and infrastructure development.

What are the restraints for the global market?

High Cost of Remediation Technologies

Advanced soil remediation methods, particularly in-situ and chemical treatments, involve significant costs related to equipment, expertise, and operational complexity. This can limit adoption, especially in developing regions where budget constraints are prevalent.

Complexity and Time-Intensive Processes

Soil remediation projects are often complex due to variations in contamination types, soil composition, and environmental conditions. Customized solutions are required for each site, leading to longer project timelines and increased costs. This complexity can act as a barrier to rapid market growth.

What are the key opportunities in the soil remediation industry?

Brownfield Redevelopment Initiatives

Governments are increasingly promoting the redevelopment of contaminated industrial sites into residential and commercial spaces. Incentives and funding programs are encouraging cleanup activities, creating significant opportunities for remediation service providers. Urban areas with limited land availability are particularly driving demand for such projects.

Adoption of Smart and Automated Technologies

The integration of AI, IoT, and automation in soil remediation offers substantial growth opportunities. These technologies enable efficient monitoring, data-driven decision-making, and optimized remediation processes. Companies adopting digital solutions can enhance operational efficiency and gain a competitive advantage.

Growing Demand from Emerging Economies

Rapid industrial growth in regions such as Asia-Pacific and Latin America is leading to increased soil contamination. Governments in these regions are implementing environmental regulations and cleanup initiatives, creating new market opportunities for both local and international players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49200.00 Million |

| Market Size in 2026 | USD 53382 Million |

| Market Size in 2031 | USD 80268.20 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

The soil remediation market is characterized by a diverse range of technologies, with biological remediation emerging as the leading segment, accounting for approximately 34% of the total market share. This dominance is largely attributed to its cost-effectiveness, sustainability, and minimal environmental disruption compared to conventional methods. Biological remediation leverages naturally occurring microorganisms to degrade hazardous contaminants into less toxic substances, making it particularly suitable for long-term environmental restoration projects. Increasing regulatory pressure to adopt eco-friendly remediation techniques and growing public awareness regarding environmental sustainability are key drivers reinforcing the adoption of biological methods across both developed and emerging economies.Electrokinetic remediation is gaining traction as an emerging niche technology, particularly for fine-grained soils such as clays and silts where conventional methods may be less effective. This technique uses electric currents to mobilize contaminants, enabling targeted remediation in complex geological settings. Its growing adoption is driven by increasing demand for innovative solutions capable of addressing difficult contamination scenarios, including heavy metals and mixed pollutants. As research and development efforts continue, electrokinetic methods are expected to play a more prominent role in specialized applications, contributing to the overall technological evolution of the soil remediation market.

Contaminant Type Insights

Based on contaminant type, petroleum hydrocarbons represent the leading segment, accounting for approximately 30% of the total market share. This dominance is primarily driven by extensive contamination resulting from upstream and downstream activities in the oil and gas industry, including drilling, transportation, refining, and accidental spills. The widespread presence of hydrocarbon pollutants across industrial and urban landscapes necessitates large-scale remediation efforts, thereby sustaining strong demand for effective treatment solutions. Increasing global energy consumption and ongoing exploration activities further contribute to the prevalence of hydrocarbon contamination, reinforcing this segment’s leading position.Emerging contaminants, particularly per- and polyfluoroalkyl substances (PFAS), are gaining considerable attention in recent years. These persistent chemicals, commonly used in industrial and consumer applications, are resistant to degradation and pose long-term environmental and health risks. The rising awareness of PFAS contamination, coupled with evolving regulatory frameworks and guidelines, is creating new opportunities for advanced remediation technologies. As governments and environmental agencies intensify efforts to monitor and control emerging pollutants, this segment is expected to witness significant growth, driving innovation and investment in next-generation remediation solutions.

Service Type Insights

In terms of service type, remediation services dominate the market, accounting for approximately 55% of the overall share. This segment encompasses the core activities involved in soil cleanup, including excavation, treatment, disposal, and site restoration. The leading position of remediation services is driven by the increasing number of contaminated sites globally and the growing need for comprehensive solutions to address complex environmental challenges. Stringent environmental regulations and liability concerns are compelling industries and property owners to invest in professional remediation services, ensuring compliance and minimizing legal risks.The growth of this segment is further supported by advancements in project management and integrated service offerings, enabling service providers to deliver end-to-end solutions tailored to specific site conditions. The increasing involvement of private sector companies and public-private partnerships in large-scale remediation projects also contributes to the expansion of this segment.Site assessment and monitoring services play a critical role in supporting remediation activities, providing essential data for decision-making and ensuring the effectiveness of treatment processes. These services include soil sampling, contamination analysis, risk assessment, and post-remediation monitoring, all of which are vital for achieving regulatory compliance and long-term environmental sustainability. The rising adoption of digital technologies, such as remote sensing and data analytics, is enhancing the accuracy and efficiency of site assessment processes, further driving demand for these services.

Application Insights

By application, industrial land remediation emerges as the leading segment, accounting for nearly 28% of the market share. This dominance is primarily driven by the high levels of contamination associated with industrial activities, including manufacturing, chemical processing, and waste disposal. Stringent environmental regulations and the need to mitigate environmental liabilities are compelling industries to invest in remediation solutions, thereby driving market growth. The increasing focus on sustainable industrial practices and corporate environmental responsibility further supports the expansion of this segment.Urban redevelopment is another key application area witnessing significant growth, fueled by the increasing demand for land in densely populated regions. As cities continue to expand, the redevelopment of contaminated brownfield sites into residential, commercial, and recreational spaces has become a priority for governments and developers. Soil remediation plays a crucial role in enabling such transformations, ensuring that previously unusable land can be safely repurposed. Rising investments in infrastructure development and smart city initiatives are further accelerating demand in this segment.Agricultural land remediation is also gaining importance, driven by the need to address soil contamination caused by excessive use of pesticides, fertilizers, and industrial runoff. Ensuring soil health and productivity is critical for food security, prompting increased adoption of remediation techniques in the agricultural sector. This trend is particularly prominent in regions with intensive farming practices, where soil degradation poses a significant challenge to sustainable agriculture.

Deployment Insights

In terms of deployment, in-situ remediation dominates the market, accounting for approximately 60% of the total share. The leading position of this segment is driven by its ability to treat contaminated soil directly at the site without the need for excavation, thereby reducing operational costs and minimizing environmental disruption. In-situ techniques, such as bioremediation, soil vapor extraction, and chemical injection, are increasingly preferred due to their efficiency and suitability for a wide range of contaminants and site conditions.The growing emphasis on sustainable and minimally invasive remediation solutions is a key driver for the adoption of in-situ methods. These techniques not only reduce the carbon footprint associated with transportation and disposal but also enable continuous treatment over extended periods, ensuring thorough remediation. Additionally, advancements in monitoring technologies and real-time data analysis are enhancing the effectiveness and reliability of in-situ approaches.Ex-situ remediation methods, while less dominant, remain essential for certain applications requiring intensive treatment. These methods involve the excavation and removal of contaminated soil for treatment at designated facilities, making them suitable for highly contaminated sites or projects with strict cleanup requirements. Despite their higher cost and logistical complexity, ex-situ techniques offer greater control over treatment conditions and can achieve faster results in specific scenarios. As a result, they continue to play a complementary role in the overall soil remediation market.

End-Use Industry Insights

The oil and gas sector represents the leading end-use industry, accounting for approximately 25% of the market share. This dominance is driven by the significant environmental impact of exploration, production, and refining activities, which often result in soil contamination from hydrocarbons and other hazardous substances. The increasing focus on environmental compliance and risk management within the industry is driving demand for effective remediation solutions, ensuring safe and sustainable operations.Mining is another major contributor to the soil remediation market, as extraction activities generate substantial quantities of waste and pollutants, including heavy metals and acidic compounds. The need to rehabilitate mining sites and mitigate environmental damage is a key driver for remediation efforts in this sector. Governments and regulatory bodies are increasingly enforcing stringent guidelines for mine closure and land restoration, further boosting demand.The agriculture and construction industries also play a significant role in driving market growth. In agriculture, soil remediation is essential for maintaining soil fertility and ensuring safe food production, particularly in regions affected by contamination from agrochemicals. In construction, remediation is often required to prepare contaminated land for development, enabling safe and sustainable urban expansion. The broad applicability of soil remediation solutions across multiple industries underscores the market’s growth potential and resilience.

Explore more data points, trends and opportunities Download Free Sample Report

Soil Remediation Market Segmentations

By Technology

- Physical Remediation

- Chemical Remediation

- Biological Remediation

- Electrokinetic Remediation

By Contaminant Type

- Heavy Metals

- Petroleum Hydrocarbons

- Pesticides & Agrochemicals

- Industrial Chemicals

- Emerging Contaminants

By Application

- Industrial Land

- Agricultural Land

- Urban Redevelopment Sites (Brownfields)

- Mining Sites

- Landfills & Waste Disposal Sites

By Deployment

- In-situ Remediation

- Ex-situ Remediation

By End-Use Industry

- Oil & Gas

- Mining & Metallurgy

- Agriculture

- Construction & Real Estate

- Chemical & Manufacturing

Regional Insights

North America

North America holds the largest share of approximately 35% of the global soil remediation market, with the United States leading regional demand. The region’s dominance is primarily driven by stringent environmental regulations enforced by agencies such as the Environmental Protection Agency (EPA), which mandate the cleanup of contaminated sites. The presence of a large number of brownfield sites and ongoing redevelopment initiatives further contribute to market growth. Additionally, strong government funding programs and incentives for environmental restoration are encouraging investment in remediation projects.Technological advancement is another key driver in North America, with widespread adoption of innovative remediation techniques and digital monitoring solutions. The region also benefits from a well-established infrastructure and the presence of leading market players, enabling efficient project execution. Increasing public awareness regarding environmental protection and sustainability further supports the demand for soil remediation solutions across residential, commercial, and industrial sectors.

Europe

Europe accounts for approximately 28% of the global market, with countries such as Germany, the United Kingdom, and France at the forefront of demand. The region’s growth is strongly influenced by its commitment to environmental sustainability and stringent regulatory frameworks governing soil and water quality. Policies under the European Union, including directives on waste management and environmental protection, are driving the adoption of advanced remediation technologies.Another significant driver in Europe is the increasing focus on circular economy principles and sustainable land use. Governments are actively promoting the redevelopment of contaminated sites to optimize land utilization and reduce environmental impact. Technological innovation, supported by research and development initiatives, is further enhancing the efficiency and effectiveness of remediation solutions. The growing emphasis on green technologies and renewable energy projects also contributes to the demand for soil remediation, particularly in the context of site preparation and environmental compliance.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the soil remediation market, with a CAGR exceeding 10%. Countries such as China and India are major contributors, driven by rapid industrialization, urbanization, and increasing environmental concerns. The expansion of manufacturing industries and infrastructure development has led to significant soil contamination, necessitating large-scale remediation efforts.Government initiatives and policy reforms aimed at pollution control and environmental protection are key drivers of market growth in the region. For instance, stricter regulations on industrial emissions and waste disposal are compelling industries to adopt remediation solutions. Rising public awareness regarding environmental health and sustainability is also contributing to increased demand. Furthermore, the growing adoption of advanced technologies and international collaboration in environmental projects are expected to accelerate market expansion in Asia-Pacific.

Latin America

Latin America is experiencing steady growth in the soil remediation market, with countries such as Brazil and Mexico leading regional demand. The region’s growth is primarily driven by extensive mining activities, which result in significant soil contamination from heavy metals and other pollutants. The need to rehabilitate mining sites and comply with environmental regulations is a key factor driving remediation efforts.Agricultural expansion is another important driver, as soil contamination from agrochemicals and industrial runoff poses challenges to sustainable farming practices. Governments in the region are increasingly implementing policies to promote environmental protection and sustainable land use, further supporting market growth. Additionally, foreign investment in infrastructure and industrial projects is contributing to the demand for soil remediation solutions.

Middle East & Africa

The Middle East & Africa region exhibits moderate growth, primarily driven by oil-producing countries such as Saudi Arabia and the United Arab Emirates. The region’s soil remediation market is closely linked to the oil and gas industry, where contamination from exploration, production, and transportation activities necessitates effective remediation solutions. Oil spill management and environmental restoration projects are key drivers of demand.In addition to the oil and gas sector, increasing industrialization and urban development are contributing to soil contamination, creating opportunities for remediation services. Governments are gradually strengthening environmental regulations and investing in sustainability initiatives, which are expected to support market growth over the forecast period. The adoption of advanced technologies and international expertise is also enhancing the region’s capability to address complex contamination challenges, further driving the expansion of the soil remediation market.

Key Players in the Soil Remediation Market

- Tetra Tech, Inc.

- AECOM

- Jacobs Solutions Inc.

- Veolia Environment S.A.

- Clean Harbors, Inc.

- WSP Global Inc.

- ERM Group

- SUEZ SA

- Stantec Inc.

- Arcadis NV

- SNC-Lavalin Group

- GeoGroup Inc.

- Regenesis Corporation

- Terra Systems Inc.

- Evonik Industries AG