Soft Fruit Market Size

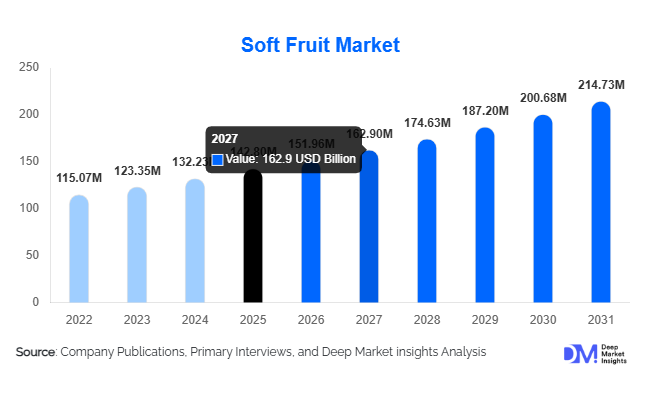

According to Deep Market Insights, the global soft fruit market size was valued at USD 142.8 billion in 2025 and is projected to grow from USD 151.96 billion in 2026 to reach USD 214.73 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). Market expansion is primarily driven by rising consumer preference for nutrient-dense fresh foods, increasing adoption of plant-forward diets, and strong demand from food processing and beverage industries. Soft fruits such as strawberries, blueberries, raspberries, and blackberries are increasingly positioned as premium health foods due to their antioxidant properties, natural sweetness, and versatility across fresh consumption and processed applications.

Key Market Insights

- Health-conscious consumption patterns are significantly increasing demand for antioxidant-rich berries across developed and emerging markets.

- Frozen and processed soft fruit segments are expanding rapidly due to year-round availability requirements from foodservice and beverage manufacturers.

- Asia-Pacific is emerging as the fastest-growing consumption hub, supported by rising disposable income and dietary westernization.

- Controlled-environment agriculture and greenhouse cultivation are improving yields and stabilizing supply chains globally.

- E-commerce grocery platforms are accelerating direct-to-consumer fresh fruit distribution models.

- Export-oriented production clusters in Latin America and Europe continue to dominate global trade flows.

What are the latest trends in the soft fruit market?

Premiumization and Functional Nutrition Positioning

Soft fruits are increasingly marketed as functional foods due to high vitamin content, fiber, and antioxidant compounds. Consumers are willing to pay premium prices for organic-certified berries, sustainably grown produce, and traceable supply chains. Retailers are introducing branded berry programs emphasizing freshness, origin transparency, and nutritional labeling. Premium berry packaging formats, including ready-to-eat snack packs and portion-controlled containers, are gaining traction among urban consumers seeking convenience and healthy snacking alternatives.

Expansion of Frozen and Value-Added Processing

The frozen soft fruit segment is witnessing rapid adoption across smoothies, bakery fillings, dairy products, and plant-based beverages. Processing technologies such as IQF (Individually Quick Frozen) preserve flavor and nutrient integrity, enabling year-round availability independent of harvest cycles. Food manufacturers increasingly rely on frozen berries to maintain supply stability and manage price volatility. This trend is strengthening vertical integration between growers and processors while expanding export potential from producing regions.

What are the key drivers in the soft fruit market?

Rising Demand for Healthy and Natural Foods

Consumers worldwide are shifting toward fresh, minimally processed foods as awareness of lifestyle-related diseases increases. Soft fruits benefit from strong scientific associations with heart health, immunity support, and weight management. Retail expansion of fresh produce sections and increasing penetration of organized supermarkets are reinforcing consumption frequency. The rise of plant-based diets further amplifies demand, as berries are widely incorporated into vegan desserts, smoothies, cereals, and functional beverages.

Advancements in Cultivation Technologies

Technological innovation in protected agriculture, hydroponics, and precision irrigation is improving productivity and extending growing seasons. Greenhouse-grown strawberries and blueberries are enabling consistent supply even in non-traditional climates. Automation technologies, including robotic harvesting and AI-based crop monitoring, are reducing labor dependency and improving yield predictability. These advancements are lowering production risks while improving profitability for commercial growers.

Growth of Global Food Processing Industry

Soft fruits are essential ingredients in yogurt, bakery products, beverages, confectionery, and frozen desserts. Rapid expansion of processed food industries across Asia-Pacific and Latin America is increasing industrial demand volumes. Beverage manufacturers increasingly incorporate berries into functional drinks, kombucha, and nutraceutical formulations, supporting sustained market growth.

What are the restraints for the global market?

High Supply Chain Sensitivity and Perishability

Soft fruits are highly perishable and require temperature-controlled logistics, increasing operational costs. Post-harvest losses remain significant in developing markets due to limited cold chain infrastructure. Transportation delays and improper storage conditions directly impact product quality and profitability, posing a major challenge for exporters.

Labor Intensity and Production Costs

Berry cultivation remains labor-intensive, particularly during harvesting seasons. Rising agricultural labor costs in North America and Europe are pressuring margins. Climate variability and unpredictable weather events further increase production risk, affecting yield stability and pricing consistency.

What are the key opportunities in the soft fruit industry?

Expansion into Emerging Asian Markets

Rapid urbanization and rising middle-class populations across India, China, and Southeast Asia are creating significant consumption opportunities. Increasing supermarket penetration and online grocery adoption enable broader availability of imported berries. Governments promoting healthy diets and agricultural modernization further support market expansion.

Investment in Controlled Environment Agriculture

Greenhouse and vertical farming systems allow year-round production with optimized resource usage. Investors are funding high-tech farms that reduce climate dependence and enhance yield efficiency. These systems also enable local production closer to urban consumption centers, reducing logistics costs and spoilage.

Functional Food and Nutraceutical Applications

The integration of berry extracts into supplements, functional beverages, and wellness foods represents a high-margin opportunity. Demand for natural antioxidants in pharmaceutical and nutraceutical sectors is expanding rapidly, opening new revenue streams beyond fresh consumption markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 142.8 Million |

| Market Size in 2026 | USD 151.96 Million |

| Market Size in 2031 | USD 214.73 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global soft fruit market is strongly shaped by product diversification, cultivation scalability, and evolving consumer dietary preferences, with strawberries maintaining a dominant leadership position across both developed and emerging economies. Strawberries accounted for approximately 34% of total global market share in 2025, supported by their broad adaptability across climatic zones, relatively shorter cultivation cycles, and high consumer familiarity. Their balanced flavor profile, affordability compared to other berries, and compatibility with multiple consumption formats — including fresh consumption, dairy integration, desserts, beverages, and processed foods — continue to strengthen demand stability. Large-scale commercial farming practices, greenhouse cultivation expansion, and improved post-harvest technologies have enabled consistent year-round supply, further reinforcing strawberries as the leading revenue-generating product segment globally.Raspberries continue to hold strong demand within bakery, confectionery, and gourmet dessert industries due to their distinctive flavor intensity and visual appeal. Premium patisserie segments across Europe and North America rely heavily on raspberries for high-value applications, supporting stable institutional demand. Meanwhile, blackberries and currants serve niche but expanding markets, particularly within specialty jams, artisanal beverages, and nutraceutical applications. These fruits benefit from rising consumer interest in unique flavors and heritage food products, contributing to gradual premium market expansion. Collectively, product diversification supports market resilience while strawberries remain the primary growth anchor due to scalability, cost efficiency, and widespread consumption patterns.

Nature Insights

Based on cultivation practices, conventional soft fruits accounted for nearly 78% of global market share in 2025, reflecting the dominance of large-scale agricultural production systems designed to ensure consistent output and competitive pricing. Conventional farming remains the backbone of global supply chains due to higher yields, established logistics infrastructure, and the ability to meet growing urban demand at accessible price points. Retailers and food processors continue to depend heavily on conventional fruit sourcing to maintain supply continuity and margin stability.The primary driver supporting the leadership of the conventional segment is production efficiency. Mechanized harvesting, optimized fertilizer application, and advanced irrigation technologies allow growers to achieve higher productivity per hectare, enabling large-volume distribution to supermarkets and industrial buyers. Developing regions particularly rely on conventional cultivation to satisfy rapidly growing population demand and export commitments.Government incentives supporting sustainable agriculture in Europe and North America, combined with improved organic farming techniques, are reducing yield gaps between conventional and organic production. Additionally, younger consumers demonstrate stronger willingness to pay for ethically sourced produce, reinforcing long-term growth prospects for organic berries. As sustainability becomes a core purchasing criterion, organic soft fruits are expected to capture an increasing share of premium retail shelves while complementing, rather than replacing, conventional production systems.

Form Insights

In terms of product form, fresh soft fruits dominated the global market with approximately 62% market share in 2025, largely driven by increasing consumer preference for natural, minimally processed foods and healthy snacking habits. Rising urbanization, growing disposable incomes, and heightened awareness of nutritional benefits have encouraged consumers to incorporate fresh berries into daily diets. Retail merchandising strategies emphasizing freshness, visual appeal, and convenience packaging further strengthen fresh segment performance.The leading driver behind the fresh segment is the global shift toward preventive healthcare and nutrient-dense diets. Soft fruits are widely perceived as low-calorie, vitamin-rich foods supporting immunity and digestive health, making them highly attractive to health-conscious consumers. Expansion of refrigerated logistics networks and controlled-atmosphere storage technologies has significantly reduced spoilage rates, enabling retailers to maintain product quality over longer distribution distances.Freeze-dried soft fruits are emerging as a premium innovation segment within functional snacks and sports nutrition categories. These products retain nutritional density while offering portability and long storage duration, making them popular among health-focused consumers and outdoor lifestyle segments. Although currently smaller in market share, freeze-dried berries demonstrate strong long-term growth potential driven by innovation in healthy snacking formats.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 46% of global soft fruit sales. Their leadership is supported by advanced cold-chain infrastructure, centralized procurement systems, and the ability to offer wide product assortments under controlled storage conditions. Consumers prefer these retail formats for reliability, product quality assurance, and competitive pricing enabled by bulk sourcing.A major driver sustaining supermarket dominance is investment in refrigeration technology and supply chain optimization, which ensures freshness while minimizing waste. Retail chains increasingly collaborate directly with growers through long-term sourcing agreements, improving traceability and ensuring stable supply volumes throughout the year.Specialty stores and local markets continue to play an important role in premium and organic fruit sales, particularly in Europe and Asia-Pacific, where consumers value freshness perception and locally sourced produce. The coexistence of traditional and digital retail channels is creating a multi-channel ecosystem that enhances overall market accessibility.

End-Use Insights

Household consumption represents the largest end-use segment globally, supported by growing awareness of balanced nutrition and increasing incorporation of berries into breakfast meals, snacks, and home-prepared desserts. Consumers increasingly view soft fruits as everyday health foods rather than occasional indulgences, driving consistent retail demand.The key driver behind household segment leadership is the expansion of health-oriented dietary patterns emphasizing natural antioxidants, fiber intake, and reduced processed sugar consumption. Social media influence and wellness trends have also contributed to increased berry usage in smoothies, oatmeal bowls, and functional home recipes.Emerging applications in plant-based dairy alternatives and functional beverages further broaden industrial demand. Berry extracts are increasingly incorporated into protein shakes, immunity drinks, and nutraceutical formulations, creating new revenue streams for growers and processors. Long-term supply contracts between agricultural producers and food manufacturers are strengthening supply chain stability while supporting investment in cultivation expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Soft Fruit Market Segmentations

By Product Type

- Strawberries

- Blueberries

- Raspberries

- Blackberries

- Cranberries

- Gooseberries & Currants

- Other Soft Fruits

By Form

- Fresh Soft Fruits

- Frozen Soft Fruits

- Dried Soft Fruits

- Processed

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Wholesale & Export Markets

- Foodservice Distribution

By End Use

- Household Consumption

- Dairy & Frozen Dessert Industry

- Bakery & Confectionery

- Beverages & Smoothies

- Nutraceuticals & Functional Foods

- Food Processing Industry

Regional Insights

North America

North America accounted for approximately 28% of global soft fruit market share in 2025, led primarily by the United States, which demonstrates one of the highest per-capita berry consumption rates globally. Strong health awareness, widespread adoption of functional foods, and well-established retail infrastructure continue to drive regional demand growth. Blueberries and strawberries remain particularly popular due to their integration into breakfast foods, snacks, and ready-to-eat products.Regional growth is driven by advanced agricultural technology adoption, including precision farming, automated harvesting systems, and controlled-environment agriculture. Imports from Mexico complement domestic production, ensuring year-round availability and price stability. Canada contributes steady expansion through rising frozen berry consumption and increasing demand from processed food manufacturers. The rapid growth of plant-based food innovation and high consumer willingness to pay for organic produce further strengthens North America’s premium market positioning.

Europe

Europe held nearly 26% of global market share, supported by strong consumption culture, established berry farming traditions, and expanding organic agriculture policies. Germany, the United Kingdom, Spain, and Poland serve as major production and consumption centers. Spain and Poland function as key export hubs supplying fresh berries across European markets.Regional growth is driven by sustainability-focused consumer behavior and stringent food safety regulations encouraging high-quality production standards. Government support for organic farming and reduced pesticide usage has accelerated premium berry adoption. Increasing demand for locally sourced produce and seasonal food consumption patterns further strengthen domestic supply chains. Additionally, Europe’s robust bakery and confectionery industries continue to drive stable industrial demand for raspberries and specialty berries.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and growing adoption of Western dietary habits. China, Japan, South Korea, and India are emerging as major consumption markets, with regional demand projected to expand at over 9% CAGR. China is significantly expanding domestic berry cultivation through greenhouse investments and agricultural modernization initiatives.Regional growth drivers include rising disposable incomes, increasing health awareness, and expansion of modern retail formats. India is witnessing growing imports alongside investments in protected cultivation technologies aimed at improving yield consistency. E-commerce grocery platforms are accelerating berry accessibility in metropolitan areas, while café culture expansion increases demand for smoothies and dessert-based applications. The region’s large population base creates substantial long-term consumption potential.

Latin America

Latin America plays a strategically important role in the global soft fruit supply chain as a leading export-oriented production region. Countries such as Chile, Mexico, and Peru benefit from favorable climatic conditions enabling counter-seasonal production for Northern Hemisphere markets. Peru has emerged as one of the fastest-growing blueberry exporters globally due to strong agricultural investment and export-focused infrastructure development.Regional growth is driven by expanding international trade agreements, foreign investment in berry farming, and improvements in cold-chain logistics supporting long-distance exports. Government initiatives promoting high-value agricultural exports encourage farmers to shift toward berry cultivation due to higher profitability compared to traditional crops.

Middle East & Africa

The Middle East & Africa region is witnessing steady demand growth, particularly across the UAE, Saudi Arabia, and South Africa. Rising disposable incomes, expanding premium retail formats, and growing expatriate populations are increasing demand for imported fresh berries. The UAE functions as a regional re-export hub, facilitating distribution across Gulf Cooperation Council markets.Regional growth is supported by increasing investments in modern retail infrastructure, cold storage facilities, and food service expansion. Health-conscious consumer trends and the popularity of premium imported produce are strengthening berry consumption patterns. In Africa, South Africa leads regional production and export activity, benefiting from favorable agricultural conditions and expanding trade connectivity with European markets.

Key Players in the Soft Fruit Market

- Driscoll’s Inc.

- Dole Food Company

- BerryWorld Group

- Wish Farms

- Fresh Del Monte Produce Inc.

- NatureSweet Ltd.

- Camposol Holding PLC

- Hortifrut S.A.

- California Giant Berry Farms

- Angus Soft Fruits Ltd.

- Planasa Group

- Agrana Beteiligungs AG

- Greenyard NV

- S&A Produce (UK) Ltd.

- Total Produce Plc