Soft Drinks Sales Market Size

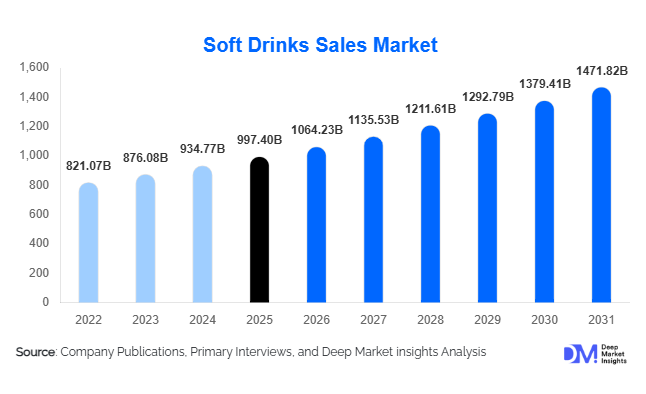

According to Deep Market Insights, the global soft drinks sales market size was valued at USD 997.4 billion in 2025 and is projected to grow from USD 1,064.23 billion in 2026 to reach USD 1,471.82 billion by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The soft drinks sales market growth is primarily driven by rising urbanization, increasing demand for functional and premium beverages, rapid expansion of organized retail channels, and shifting consumer preference toward convenience-oriented hydration products. Beverage manufacturers are increasingly investing in low-sugar formulations, plant-based beverages, premium bottled water, and energy drinks to align with evolving health-conscious consumption trends globally.

Key Market Insights

- Functional and wellness-oriented beverages are rapidly reshaping the soft drinks industry, with consumers increasingly demanding hydration drinks, electrolyte beverages, probiotics, and vitamin-enriched formulations.

- Asia-Pacific dominates the global soft drinks sales market, supported by rising middle-class populations, expanding retail infrastructure, and growing disposable incomes in China, India, Indonesia, and Southeast Asia.

- Premiumization trends are accelerating globally, particularly across North America and Europe, where consumers increasingly prefer clean-label, organic, and naturally sweetened beverages.

- Energy drinks and RTD beverages remain among the fastest-growing categories, fueled by urban lifestyles, fitness trends, and increasing demand for convenient on-the-go consumption.

- Sustainable packaging initiatives are becoming a major competitive differentiator, with beverage companies investing heavily in recyclable PET, aluminum cans, refillable systems, and lightweight packaging technologies.

- Digital retail and quick-commerce channels are transforming beverage distribution, enabling companies to strengthen direct-to-consumer engagement and improve premium product penetration.

soft drinks sales market latest trends

Rapid Growth of Functional and Health-Oriented Beverages

The global soft drinks sales market is witnessing a major transformation toward health-focused and functional beverages. Consumers are increasingly prioritizing products that offer hydration, immunity enhancement, digestive wellness, energy support, and mental focus benefits. This trend is driving significant growth in electrolyte beverages, vitamin-enhanced water, probiotic drinks, botanical beverages, kombucha, sports hydration products, and low-calorie functional drinks. Beverage companies are rapidly reformulating products with natural sweeteners such as stevia and monk fruit while reducing artificial additives and sugar content. Functional beverages targeting fitness enthusiasts, working professionals, and younger consumers are generating higher margins and premium positioning opportunities for manufacturers. Additionally, clean-label ingredients and plant-based beverage innovations are further strengthening the transition toward wellness-centric soft drink consumption patterns globally.

Sustainable Packaging and Circular Economy Adoption

Sustainability has become one of the most influential trends shaping the global soft drinks sales market. Governments and consumers are increasingly pressuring beverage manufacturers to reduce plastic waste, lower carbon emissions, and improve recycling rates. Major beverage companies are investing heavily in recyclable PET packaging, aluminum cans, biodegradable materials, refillable bottle systems, and lightweight packaging technologies. Water conservation systems, renewable energy integration, and sustainable sourcing initiatives are also gaining importance across production facilities worldwide. Consumers increasingly prefer environmentally responsible beverage brands, particularly in Europe and North America, where sustainability purchasing behavior is strongly influencing market competition. Companies implementing circular economy strategies and eco-friendly packaging innovations are expected to strengthen long-term brand positioning and gain regulatory advantages.

soft drinks sales market drivers

Growing Urbanization and Convenience Consumption

Rapid urbanization and changing consumer lifestyles are significantly driving the global soft drinks sales market. Increasing working populations, busy schedules, and rising demand for portable refreshment products are accelerating consumption of ready-to-drink beverages globally. Urban consumers increasingly prefer convenient hydration products that can be consumed during travel, work, sports, and leisure activities. This trend is strongly supporting growth in energy drinks, RTD coffee, RTD tea, bottled water, and functional beverages. Expansion of convenience retail chains, vending machine networks, and quick-commerce grocery delivery platforms is further strengthening product accessibility and driving higher beverage consumption volumes across both developed and emerging economies.

Premiumization and Innovation in Beverage Formulations

The premiumization trend is becoming a major growth driver across the global soft drinks industry. Consumers are increasingly willing to pay higher prices for beverages offering natural ingredients, exotic flavors, organic certifications, and added wellness benefits. Premium bottled water, craft sodas, botanical beverages, functional hydration products, and energy drinks are witnessing particularly strong growth across North America, Europe, Japan, and urban Asia-Pacific markets. Beverage manufacturers are heavily investing in flavor innovation, personalized beverages, low-sugar alternatives, and clean-label formulations to capture higher-margin premium segments. This shift toward premium products is improving profitability and encouraging continuous product diversification within the market.

global market restraints

Rising Regulatory Pressure on Sugar and Packaging

Governments across multiple regions are implementing stricter regulations regarding sugar consumption, labeling requirements, and single-use plastic packaging. Sugar taxes introduced in several countries are increasing operational costs for beverage manufacturers while also impacting consumption of traditional high-sugar carbonated beverages. Environmental regulations targeting plastic waste management and recycling compliance are further increasing packaging costs across the industry. These regulatory challenges are forcing companies to invest heavily in product reformulation, sustainable packaging technologies, and compliance-related operational upgrades.

Volatility in Raw Material and Supply Chain Costs

The global soft drinks sales market remains highly exposed to fluctuations in raw material and logistics costs. Prices of sugar, PET resin, aluminum, fruit concentrates, coffee beans, transportation fuels, and packaging materials continue to experience volatility due to geopolitical tensions, climate disruptions, and supply chain bottlenecks. Rising input costs place substantial pressure on beverage manufacturers, especially within highly competitive mass-market categories where pricing flexibility is limited. Supply chain disruptions and global freight cost fluctuations also impact inventory management and production planning for multinational beverage companies.

soft drinks sales industry key opportunities

Expansion of Functional Hydration and Sports Beverages

The rapid expansion of the global fitness economy and rising health awareness are creating major opportunities within functional hydration and sports beverage categories. Consumers increasingly seek beverages that support energy recovery, endurance, hydration, and performance optimization. This is driving strong demand for electrolyte drinks, protein beverages, vitamin-enriched hydration products, and low-calorie sports beverages. Beverage companies investing in scientifically formulated functional drinks and wellness-focused product portfolios are expected to capture significant long-term growth opportunities. Emerging markets such as India, Southeast Asia, and the Middle East are also witnessing rising fitness participation rates, further expanding demand for performance-oriented beverages.

Emerging Market Expansion and Retail Penetration

Emerging economies across Asia-Pacific, Latin America, and Africa continue to provide substantial long-term growth opportunities for soft drink manufacturers. Rising disposable incomes, expanding urban populations, increasing refrigeration penetration, and modernization of retail infrastructure are accelerating beverage consumption across countries such as India, Indonesia, Vietnam, Nigeria, and Brazil. Beverage companies are increasingly establishing localized manufacturing facilities and strengthening regional distribution networks to improve accessibility and reduce operational costs. Rapid growth in digital grocery platforms and quick-commerce delivery systems in emerging markets is further enhancing premium beverage penetration and consumer reach.

Product Type Insights

Carbonated soft drinks continue to dominate the global soft drinks sales market, accounting for nearly 31% of total market revenue in 2025. Strong global brand recognition, aggressive marketing investments, and extensive retail penetration continue supporting category leadership despite rising health-conscious consumption trends. Non-carbonated beverages such as sports drinks, flavored water, RTD tea, and energy drinks are witnessing significantly faster growth due to increasing demand for healthier and functional alternatives. Juice-based beverages continue to maintain strong demand in emerging markets, while premium bottled water is expanding rapidly across urban populations seeking clean-label hydration products. Functional beverages enriched with vitamins, probiotics, adaptogens, and electrolytes are emerging as one of the most profitable segments globally, particularly among younger consumers and fitness-oriented demographics.

Sweetener Type Insights

Sugar-sweetened beverages remain the leading category globally, accounting for approximately 54% of total market value due to strong demand across developing economies where conventional formulations continue dominating consumption patterns. However, naturally sweetened beverages are witnessing significantly higher growth rates, particularly in North America and Europe, where consumers increasingly prefer low-calorie and sugar-free alternatives. Artificially sweetened beverages continue to maintain substantial market presence within diet soda and reduced-calorie product categories. Beverage manufacturers are rapidly reformulating portfolios using natural sweeteners such as stevia and monk fruit to address changing regulatory frameworks and shifting health-conscious purchasing behavior.

Packaging Type Insights

PET bottles dominate the global soft drinks sales market packaging landscape, representing nearly 46% of total packaging demand due to lightweight properties, transport convenience, durability, and cost efficiency. PET packaging remains highly preferred across bottled water, carbonated beverages, juices, and sports drinks. Aluminum cans are rapidly gaining market share due to strong recyclability advantages, premium brand positioning, and increasing sustainability adoption among beverage manufacturers. Glass bottles continue to retain importance within premium and specialty beverage categories, particularly in Europe and hospitality channels. Flexible pouches and carton packaging are also witnessing gradual adoption for children’s beverages and on-the-go hydration products.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels within the global soft drinks sales market, accounting for approximately 38% of global sales due to wide product availability, organized retail infrastructure, and strong promotional pricing strategies. Convenience stores continue representing a critical channel for impulse beverage purchases and urban consumption patterns. Online retail and quick-commerce platforms are emerging as the fastest-growing channels globally, driven by digital grocery adoption, mobile commerce penetration, and direct-to-consumer beverage subscriptions. Foodservice channels including restaurants, cafés, hotels, cinemas, and quick-service restaurants are also experiencing strong recovery-driven demand growth, particularly for premium and functional beverage categories.

Consumer Category Insights

Mass-market consumers continue to represent the largest share of the global soft drinks sales market, contributing nearly 62% of total beverage consumption volumes. Affordable carbonated beverages, juices, and bottled water products remain highly popular across emerging economies. Premium consumers are becoming increasingly important from a revenue perspective, driven by growing demand for organic beverages, functional drinks, premium hydration products, and clean-label formulations. Health-conscious consumers represent one of the fastest-growing demographics globally, accelerating growth in low-calorie beverages, sugar-free drinks, electrolyte hydration products, and plant-based functional beverages. Younger consumers continue driving experimentation with innovative flavors, energy drinks, and digital-first beverage brands.

End-Use Insights

Household consumption remains the leading end-use segment within the global soft drinks sales market, accounting for nearly 57% of total demand due to strong retail purchasing patterns and rising at-home beverage consumption. Foodservice and hospitality channels are among the fastest-growing segments globally, supported by tourism recovery, increasing restaurant visits, and expansion of quick-service restaurant chains. Sports and fitness consumption is also experiencing substantial growth due to increasing gym memberships, rising sports participation, and wellness-focused lifestyles. Corporate workplaces and institutional consumption are emerging as important demand segments due to vending machine deployment, employee wellness initiatives, and growing office beverage programs.

| By Product Type | By Sweetener Type | By Packaging Type | By Distribution Channel | By Consumer Category |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for nearly 24% of the global soft drinks sales market value, led primarily by the United States, which remains one of the world’s largest beverage consumption markets. Strong consumer preference for premium functional beverages, energy drinks, flavored water, and low-sugar formulations continues supporting regional market expansion. Canada is witnessing rising demand for clean-label beverages and sustainable packaging solutions. Mexico remains one of the highest per-capita consumers of carbonated beverages globally, sustaining strong regional demand. Beverage innovation, digital retail growth, and premiumization trends continue driving market transformation across North America.

Europe

Europe represents approximately 21% of the global soft drinks sales market, with Germany, the United Kingdom, France, Italy, and Spain serving as major demand centers. European consumers strongly prioritize sustainability, sugar reduction, and organic beverage consumption. Regulatory pressure regarding sugar taxation and packaging recycling is accelerating innovation across low-calorie beverages, sparkling water, and naturally sweetened product categories. Premium bottled water and functional hydration beverages continue witnessing strong demand growth across Western Europe. Eastern European countries are also experiencing rising beverage consumption due to improving disposable incomes and retail modernization.

Asia-Pacific

Asia-Pacific dominates the global soft drinks sales market with nearly 37% market share in 2025. China remains the largest country-level market due to its vast urban consumer base, expanding retail infrastructure, and increasing premium beverage consumption. India is among the fastest-growing countries globally, supported by rising disposable incomes, urbanization, and growing penetration of organized retail and foodservice channels. Japan and South Korea continue leading innovation in functional beverages, RTD coffee, and premium hydration products. Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are witnessing rapid beverage demand growth due to demographic expansion and rising middle-class populations.

Latin America

Latin America continues demonstrating strong beverage demand growth, particularly across Brazil, Mexico, Argentina, Chile, and Colombia. Carbonated soft drinks and juice beverages remain highly popular throughout the region due to strong consumer preference for flavored refreshment products. Brazil is also witnessing increasing demand for energy drinks, sports beverages, and premium bottled water categories. Rising retail modernization, urbanization, and expanding middle-income populations continue supporting long-term market growth across Latin America.

Middle East & Africa

The Middle East & Africa region is emerging as one of the fastest-growing soft drinks markets globally. Saudi Arabia and the UAE are witnessing strong growth in premium bottled water, functional hydration products, and energy drinks due to high temperatures, urban lifestyles, and increasing health awareness. South Africa remains one of the largest beverage markets in Africa, while Nigeria is experiencing substantial demand growth due to rapid population expansion and urbanization. Rising tourism activity, infrastructure development, and expanding foodservice industries continue contributing to long-term regional beverage demand growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Soft Drinks Sales Market

- The Coca-Cola Company

- PepsiCo

- Nestlé

- Red Bull

- Keurig Dr Pepper

- Monster Beverage Corporation

- Danone

- Suntory Holdings

- Asahi Group Holdings

- Unilever

- National Beverage Corp.

- Britvic

- Tingyi Holding Corp.

- Bisleri International

- Nongfu Spring