Soft Drinks Market Size

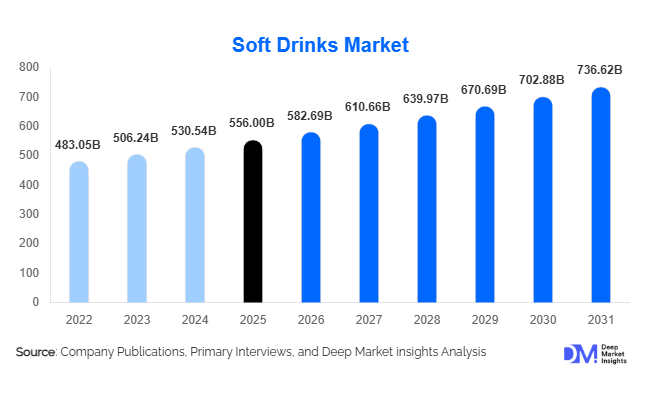

According to Deep Market Insights, the global soft drinks market size was valued at USD 556 billion in 2025 and is projected to grow from USD 582.69 billion in 2026 to reach USD 736.62 billion by 2031, expanding at a CAGR of 4.8% during the forecast period (2026–2031). The soft drinks market growth is primarily driven by rising consumer demand for convenient ready-to-drink beverages, increasing health-consciousness leading to functional drink adoption, and expansion of modern retail and e-commerce channels across emerging economies.

Key Market Insights

- Carbonated beverages continue to dominate the market, accounting for approximately 45% of total consumption in 2024, supported by strong brand loyalty and widespread availability in both mature and emerging markets.

- Non-carbonated and functional beverages are growing rapidly, reflecting increasing consumer preference for low-sugar, vitamin-fortified, and health-oriented drinks.

- Asia-Pacific is the fastest-growing region, led by China, India, and Japan, driven by urbanization, rising disposable income, and younger population demographics.

- North America and Europe remain major markets, with high consumption of premium and functional soft drinks, especially in the U.S., Germany, and the U.K.

- Online retail and e-commerce adoption is accelerating, providing manufacturers with direct-to-consumer opportunities and personalized marketing platforms.

- Technological innovations, including automated bottling, functional ingredient integration, and AI-enabled consumer insights, are reshaping product development and distribution strategies.

What are the latest trends in the soft drinks market?

Rise of Health-Focused and Functional Beverages

Health-conscious consumers are increasingly seeking beverages that go beyond hydration, favoring products with added vitamins, minerals, probiotics, and natural ingredients. This trend has led to a surge in demand for low-calorie carbonates, fortified juices, energy drinks, and herbal-infused beverages. Companies are responding with reformulated products that reduce sugar content and enhance functional benefits, such as immunity-boosting ingredients and antioxidants. This shift is particularly evident in North America, Europe, and the Asia-Pacific region, where consumers actively seek transparent labeling and natural ingredients, positioning functional beverages as a premium growth segment within the soft drinks market.

Packaging and Sustainability Innovations

Modern consumers prioritize convenience, portability, and eco-conscious packaging. PET bottles remain the most widely used format due to affordability and ease of distribution, accounting for 55% of the market in 2024, followed by cans and Tetra Pak cartons. Simultaneously, recyclable, biodegradable, and reusable packaging solutions are gaining traction as brands address environmental concerns and regulatory pressures. Companies are integrating sustainable initiatives, such as carbon footprint reduction in production and packaging optimization, which are increasingly influencing purchasing decisions among younger demographics and environmentally conscious consumers.

What are the key drivers in the soft drinks market?

Convenience and Ready-to-Drink Consumption

The urban lifestyle and fast-paced schedules have increased the demand for convenient beverage options, including single-serve and ready-to-drink formats. Bottled soft drinks and RTD teas and coffees cater to this need, enhancing on-the-go consumption. Supermarkets, convenience stores, and online platforms are key distribution channels supporting growth, particularly in emerging markets such as India, China, and Brazil, where modern retail penetration is expanding rapidly.

Innovation in Functional Ingredients

The incorporation of functional ingredients, such as vitamins, minerals, plant extracts, and probiotics, is a significant growth driver. Functional beverages cater to consumers seeking immunity support, weight management, or digestive benefits. Brands investing in R&D for healthier formulations are capturing premium segments, particularly in North America and Europe, where consumers are willing to pay a higher price for health-oriented products.

Expansion of Modern Retail and E-Commerce Channels

Supermarkets, hypermarkets, and online retail platforms are increasing accessibility and visibility for soft drink products. E-commerce allows direct-to-consumer engagement, subscription models, and personalized promotions, enabling brands to capture young, tech-savvy consumers. This trend is accelerating in APAC and LATAM, where smartphone penetration and digital payment adoption are rising.

What are the restraints for the global market?

Health Concerns over Sugar and Artificial Ingredients

Rising awareness of obesity, diabetes, and other lifestyle diseases has created pressure on traditional sugary carbonated beverages. Consumers increasingly prefer low-calorie, sugar-free, or naturally sweetened options. This trend is constraining growth in mature markets, such as North America and Europe, and forcing companies to innovate with reduced-sugar alternatives.

Volatility in Raw Material Prices

Fluctuating costs of sugar, fruit concentrates, aluminum, and packaging materials impact production expenses. Price volatility can reduce profit margins, limit competitive pricing flexibility, and challenge smaller manufacturers in emerging markets. Efficient supply chain management and long-term procurement strategies are essential to mitigate these risks.

What are the key opportunities in the soft drinks industry?

Health and Functional Beverage Expansion

Growing consumer demand for healthier options presents an opportunity for companies to innovate with functional beverages. Immunity-boosting drinks, plant-based soft drinks, and vitamin-fortified products are gaining traction globally. Manufacturers can leverage this trend to develop premium offerings with higher margins while catering to the health-conscious demographic. Collaborations with nutrition experts and endorsements from health authorities are expected to boost credibility and adoption.

Growth in Emerging Markets

Urbanization, rising disposable income, and expanding modern retail channels in countries such as India, China, Brazil, and Mexico present significant market opportunities. Early market entry strategies, local flavor adaptation, cost-effective packaging, and partnerships with regional distributors can accelerate penetration. E-commerce adoption and digital marketing campaigns targeting younger consumers further enhance market expansion potential.

Digital Transformation and E-Commerce Adoption

Online sales platforms and direct-to-consumer channels offer manufacturers an opportunity to enhance brand visibility, track consumer behavior, and develop personalized promotions. Subscription-based beverage services, AI-driven marketing, and loyalty programs are expected to drive incremental revenue growth. Digital transformation also enables manufacturers to collect real-time feedback and adapt product offerings, ensuring alignment with evolving consumer preferences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 556 Billion |

| Market Size in 2026 | USD 582.69 Billion |

| Market Size in 2031 | USD 736.62 Billion |

| CAGR | 4.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Carbonated soft drinks dominate the global market, accounting for 45% of the 2024 revenue, supported by brand loyalty and high consumption in North America, Europe, and APAC. Non-carbonated soft drinks, including juices, iced teas, and energy drinks, are rapidly growing, particularly in health-conscious markets. Functional beverages, fortified with vitamins, minerals, and plant extracts, represent a high-growth segment, targeting premium consumers seeking wellness-oriented options. Ready-to-drink teas and coffees are also expanding due to convenience and urban demand, particularly in the Asia-Pacific.

Application Insights

Household consumption remains the largest application, accounting for approximately 60% of demand. Foodservice, including restaurants, cafes, and fast-food outlets, is the fastest-growing segment, driven by on-premise consumption recovery post-pandemic. Export-driven demand is significant from North America to LATAM and Europe for premium and functional beverages. Emerging applications include fitness-focused energy drinks, RTD herbal teas, and functional beverages targeting younger demographics and wellness enthusiasts.

Distribution Channel Insights

Supermarkets and hypermarkets dominate, representing 48% of sales in 2024, offering product variety, promotions, and accessibility. Convenience stores cater to high-frequency purchases, while online retail is rapidly growing due to e-commerce adoption in APAC and LATAM. Foodservice channels support premium and functional drink consumption, with HoReCa demand driving product diversification. Direct-to-consumer sales and subscription models are increasingly being adopted to strengthen brand loyalty and consumer engagement.

Age Group Insights

Consumers aged 31–50 years account for the largest share of soft drink consumption, balancing disposable income with a preference for both carbonated and functional beverages. Younger consumers (18–30 years) drive demand for energy drinks, RTD teas and coffees, and low-sugar alternatives, leveraging digital channels. Older consumers (51–65 years) focus on functional beverages targeting wellness, while the above-65 segment, though smaller, contributes to premium product adoption due to health-related needs.

Explore more data points, trends and opportunities Download Free Sample Report

Soft Drinks Market Segmentations

By Product Type

- Carbonated Soft Drinks

- Non-Carbonated Soft Drinks

- Ready-to-Drink (RTD) Tea & Coffee

- Functional Beverages

By Packaging Type

- PET Bottles

- Glass Bottles

- Aluminum Cans

- Cartons & Tetra Packs

- Pouches & Sachets

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-Commerce

- Foodservice (HoReCa)

- Vending Machines & Institutional Sales

By Flavor Type

- Cola

- Citrus-Based

- Fruit-Based

- Herbal & Functional Flavors

Regional Insights

North America

North America accounts for 30% of the global market, led by the U.S. and Canada. Consumers increasingly demand low-calorie, functional, and premium beverages. High disposable income, urban lifestyles, and strong retail infrastructure drive steady growth. E-commerce penetration and health-focused innovations further support market expansion in this region.

Europe

Europe represents 25% of the global market, with Germany, the U.K., and France as leading countries. Consumer demand is shifting toward sugar-free, functional, and organic beverages. Mature markets prioritize product quality, sustainability, and regulatory compliance, with growth driven by functional drinks and premium offerings.

Asia-Pacific

Asia-Pacific is the fastest-growing region (CAGR 6.2%), led by China, India, and Japan. Urbanization, rising disposable income, and modern retail adoption drive market expansion. Consumers are adopting both traditional carbonated beverages and functional drinks, with e-commerce enabling wider distribution and personalized marketing.

Latin America

Brazil, Mexico, and Argentina are major contributors. Rising disposable income, urbanization, and retail modernization are fueling demand, particularly for carbonates and functional drinks. Outbound exports of premium soft drinks from North America are also contributing to regional growth.

Middle East & Africa

The Middle East, led by the UAE and Saudi Arabia, is experiencing growing demand for premium and functional beverages due to high-income populations. Africa, with countries like South Africa and Nigeria, is seeing steady urban consumption growth, supported by emerging retail infrastructure and functional beverage adoption.