Sodium Tripolyphosphate (STPP) Market Size

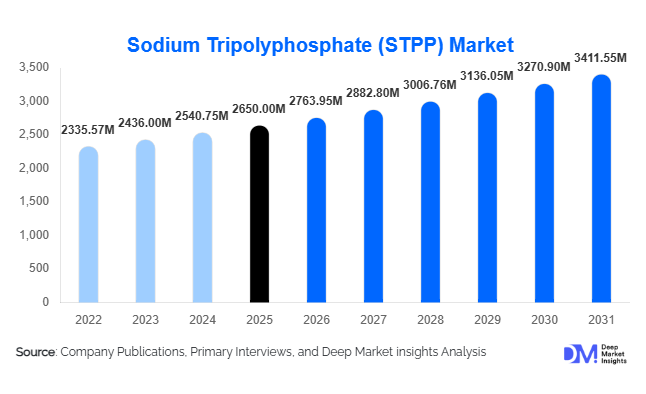

According to Deep Market Insights, the global sodium tripolyphosphate (STPP) market size was valued at USD 2,650 million in 2025 and is projected to grow from USD 2,763.95 million in 2026 to reach USD 3,411.55 million by 2031, expanding at a CAGR of 4.3% during the forecast period (2026–2031). The sodium tripolyphosphate market growth is primarily driven by sustained demand from detergent manufacturing, expanding processed food consumption, and increasing investments in industrial and municipal water treatment infrastructure.

STPP remains a critical phosphate compound used as a builder in detergents, a preservative and moisture-retention agent in food processing, and a scale inhibitor in water treatment. Asia-Pacific dominates both production and consumption due to large-scale phosphate processing capacity and strong export orientation. Meanwhile, regulatory controls on phosphate discharge in North America and Europe are reshaping product formulations and encouraging technological innovation. Despite environmental scrutiny, STPP continues to maintain a stable demand owing to its cost-effectiveness, chemical efficiency, and multifunctional performance across industries.

Key Market Insights

- Detergents & cleaning agents account for over 55% of global STPP consumption, maintaining dominance due to their superior water-softening and soil-dispersing properties.

- Industrial-grade STPP holds approximately 62% market share, driven by bulk procurement from FMCG and cleaning product manufacturers.

- Asia-Pacific dominates with nearly 48% market share in 2025, led by China and India as key production and export hubs.

- Food-grade STPP is the fastest-growing segment, expanding at over 5.5% CAGR due to rising processed meat and seafood exports.

- Powder form accounts for around 70% of global demand, favored for blending efficiency and cost-effective transport.

- The top five companies control nearly 42% of the global market, reflecting moderate consolidation with strong Chinese participation.

What are the latest trends in the sodium tripolyphosphate market?

Shift Toward High-Purity and Food-Grade STPP

With global processed meat and seafood exports exceeding USD 250 billion annually, food manufacturers increasingly prefer high-purity, regulatory-compliant STPP grades. Countries such as China, Vietnam, Brazil, and India are expanding protein processing capacity, fueling demand for food-grade phosphates that improve yield and moisture retention. Producers are investing in advanced purification and quality control systems to comply with FDA, EFSA, and international safety standards. This trend is elevating margins in specialty segments compared to traditional industrial-grade volumes.

Regional Diversification of Production Capacity

While China remains the dominant exporter, new investments in India, the Middle East, and parts of Southeast Asia are diversifying global supply chains. Governments promoting domestic chemical manufacturing under initiatives such as industrial modernization and local value addition are encouraging phosphate processing investments. This reduces reliance on single-country exports and strengthens supply security amid trade policy shifts.

What are the key drivers in the sodium tripolyphosphate market?

Growing Detergent Consumption in Emerging Economies

Rapid urbanization, rising disposable incomes, and expanding penetration of automatic washing machines in India, Indonesia, Nigeria, and Brazil are supporting detergent demand. STPP enhances cleaning performance by softening water and preventing redeposition of dirt, making it a cost-efficient builder agent. Household and institutional cleaning demand continues to sustain volume growth globally.

Expansion of Water Treatment Infrastructure

Governments across the Middle East, Asia, and Africa are investing heavily in desalination plants, municipal water systems, and industrial boiler treatment facilities. STPP’s sequestration properties make it an effective scale inhibitor, particularly in hard-water regions. Increasing industrialization further strengthens demand for chemical water treatment solutions.

What are the restraints for the global market?

Environmental Regulations on Phosphate Discharge

Phosphate runoff contributes to eutrophication in water bodies, prompting strict detergent phosphate regulations in Europe and parts of North America. Reformulation efforts and partial substitution with alternative builders may moderate growth in mature markets.

Raw Material and Energy Price Volatility

STPP production depends on phosphoric acid and soda ash, both sensitive to mining output and energy costs. Fluctuations in phosphate rock pricing and fuel expenses directly impact manufacturing margins, especially for mid-sized producers.

What are the key opportunities in the sodium tripolyphosphate industry?

Export-Oriented Processed Food Expansion

Growing global protein trade offers strong opportunities for food-grade STPP suppliers. Investments in cold chain logistics and export-focused seafood processing hubs in Southeast Asia and Latin America are increasing demand for moisture-retention additives.

Customized Industrial Blends for Water Treatment

Manufacturers can develop specialized phosphate blends integrated with automated dosing technologies for industrial customers. This allows premium pricing and long-term supply contracts, particularly in industrial boiler and cooling systems.

Grade Insights

Industrial-grade STPP dominates with approximately 62% share of the 2025 global market, primarily driven by its extensive use in large-scale detergent manufacturing and institutional cleaning formulations. The segment’s leadership is supported by the continued expansion of household laundry detergent production in Asia-Pacific, Latin America, and parts of Africa, where water hardness levels remain high and cost-effective builder systems are essential. Industrial-grade STPP offers strong chelation, water softening, and soil dispersion properties at competitive pricing, making it the preferred choice for high-volume FMCG manufacturers. In addition, industrial cleaning demand from hospitality, healthcare, and food processing facilities further strengthens this segment’s global dominance.

Food-grade STPP accounts for nearly 28% of the market and is the fastest-growing grade category, supported by rising global consumption of processed meat, poultry, and seafood products. Export-oriented protein processing hubs in China, Vietnam, India, Brazil, and Norway are driving steady demand for high-purity phosphates that improve moisture retention, texture, and yield. Strict food safety regulations in North America and Europe are encouraging investments in advanced purification technologies, enhancing margins within this segment. Specialty and technical grades contribute the remaining share, serving ceramics, oil & gas drilling fluids, textiles, and paper processing industries where functional performance and customized formulations are required.

Application Insights

Detergents & cleaning agents lead with about 55% of total global demand, maintaining clear dominance due to consistent household consumption patterns and expanding machine washing penetration across emerging markets. STPP acts as an effective builder, improving surfactant efficiency and preventing soil redeposition, particularly in hard-water regions such as India, the Middle East, and parts of Africa. Growth in institutional cleaning products post-pandemic, including hospital and hospitality sanitization chemicals, has further reinforced this segment’s volume stability.

Food processing accounts for roughly 20% of demand, supported by global protein trade and rising demand for convenience foods. Water treatment contributes approximately 12%, benefiting from investments in municipal water systems, desalination plants, and industrial boiler treatment. The remaining share is distributed across ceramics, construction materials, oil & gas, textiles, and paper industries. Growth in ceramic tile production in Asia and infrastructure expansion in developing economies provide incremental opportunities in these industrial applications.

Form Insights

Powder form holds nearly 70% market share, largely due to its compatibility with detergent manufacturing processes and ease of blending with surfactants and additives. Powdered STPP is cost-efficient in bulk transport and storage, making it ideal for high-volume FMCG production facilities. The dominance of powdered laundry detergents in emerging markets further strengthens this segment. Granular STPP represents the remaining share and is preferred in specialized industrial and water treatment applications where controlled dissolution, reduced dust formation, and improved handling safety are required. Growth in automated dosing systems within industrial water treatment plants is gradually supporting granular demand.

End-Use Industry Insights

The household & consumer goods sector accounts for approximately 52% of total demand, valued at over USD 1,350 million in 2025. The segment’s leadership is driven by steady consumption of laundry and dishwashing detergents, particularly in Asia-Pacific and Africa where urbanization and rising incomes continue to expand consumer product penetration. Multinational FMCG companies maintain long-term procurement contracts with phosphate suppliers, ensuring stable bulk demand.

The food & beverage industry is the fastest-growing end-use segment, expanding at over 5.5% CAGR. Increasing exports of processed poultry, seafood, and ready-to-eat meals are key drivers. Meanwhile, water utilities and municipal infrastructure projects in the Middle East and Africa are emerging as strong growth contributors, supported by public investments in desalination, wastewater treatment, and industrial water reuse. Oil & gas and ceramics industries provide cyclical but regionally significant demand.

| By Grade | By Application | By Form | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific commands approximately 48% of the 2025 global market, making it the largest and fastest-growing regional segment. China accounts for over 35% of global production capacity and remains the leading exporter, supported by integrated phosphate mining and processing infrastructure. India is witnessing rapid domestic demand growth due to expanding detergent manufacturing, government-backed chemical production initiatives, and increasing processed food consumption. Southeast Asian countries such as Vietnam and Indonesia benefit from export-oriented seafood industries, which drive food-grade STPP demand. Additionally, lower production costs, access to phosphate reserves, and strong regional trade networks continue to reinforce Asia-Pacific’s dominance.

North America

North America represents around 18% of the global market, led by the United States. Regional growth is driven by high consumption of processed and packaged foods, advanced water treatment infrastructure, and steady industrial cleaning demand. Although regulatory restrictions on phosphate use in household detergents moderate volume expansion, the region compensates through higher adoption of specialty and food-grade phosphates. Technological innovation, compliance with FDA standards, and strong industrial base stability contribute to sustained demand.

Europe

Europe accounts for approximately 16% share, with Germany, France, and Italy as key consumers. Strict environmental regulations limiting phosphate discharge have reduced detergent-related demand; however, growth persists in food-grade and technical applications. The region’s strong meat processing sector, particularly in Germany and Spain, supports stable consumption. Additionally, increasing investment in sustainable water management systems and industrial efficiency improvements maintains demand for specialty phosphate formulations.

Middle East & Africa

The Middle East & Africa region holds nearly 10% share of global demand. Growth is largely driven by desalination and industrial water treatment projects in Saudi Arabia and the UAE, where hard-water conditions require effective sequestration agents. Expanding urban populations across Nigeria, Kenya, and South Africa are increasing detergent imports, stimulating regional consumption. Government investments in infrastructure and water security initiatives are key long-term growth drivers in this region.

Latin America

Latin America contributes around 8% of global demand, with Brazil and Mexico leading regional consumption. Brazil is the fastest-growing country in the region at approximately 5.2% CAGR, supported by strong meat processing exports and expanding domestic detergent production. Mexico benefits from proximity to North American food processing supply chains and growing industrial cleaning demand. Urbanization, rising middle-class incomes, and expanding retail detergent penetration continue to drive steady market growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Sodium Tripolyphosphate Market

- ICL Group

- Innophos Holdings

- Prayon

- Yuntianhua Group

- Wengfu Group

- Guizhou Chanhen Chemical

- Sichuan Blue Sword Chemical

- Aditya Birla Chemicals

- Hubei Xingfa Chemicals

- Jordan Phosphate Mines Company

- Fosfa

- Haifa Group

- Chemische Fabrik Budenheim

- Tianjia Chem

- Mexichem Fluor