Snack Pellets Market Size

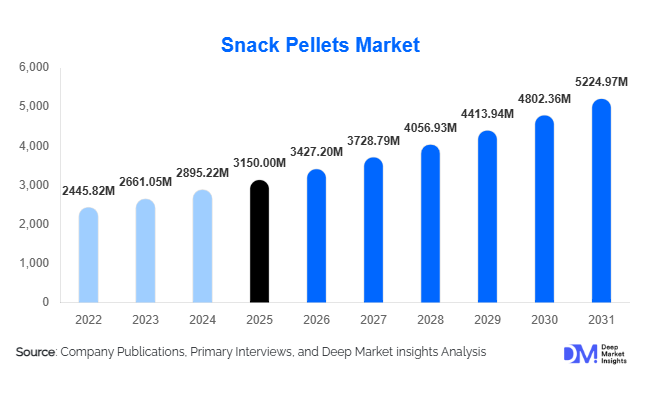

According to Deep Market Insights, the global snack pellets market size was valued at USD 3,150 million in 2025 and is projected to grow from USD 3,427.20 million in 2026 to reach USD 5,224.97 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The snack pellets market growth is primarily driven by rising global consumption of packaged savory snacks, increasing demand for semi-finished snack intermediates, and technological advancements in extrusion processing. Snack pellets enable manufacturers to optimize logistics, extend shelf stability, and customize expansion and seasoning closer to end markets, thereby improving cost efficiency and product flexibility.

Key Market Insights

- Dried snack pellets dominate the market, accounting for nearly 68% of global demand due to extended shelf life and ease of international trade.

- Potato-based pellets hold the largest product share, contributing approximately 34% of total revenue in 2025 owing to superior expansion properties and consumer familiarity.

- Asia-Pacific leads global production and consumption, representing around 38% of market share in 2025, driven by China and India.

- Twin-screw extrusion technology is gaining rapid adoption, accounting for nearly 41% of production due to superior flexibility and texture control.

- Packaged snack manufacturers remain the primary end users, representing over 70% of total demand globally.

- Multigrain and pulse-based pellets are the fastest-growing segment, supported by rising demand for healthier snack alternatives.

What are the latest trends in the snack pellets market?

Shift Toward Health-Focused and Functional Pellets

Manufacturers are increasingly incorporating multigrain, lentil, chickpea, and vegetable-based formulations to meet growing demand for healthier snack alternatives. Clean-label ingredients, gluten-free options, and high-protein snack pellets are becoming mainstream across North America and Europe. Food processors are reformulating pellet compositions to reduce oil absorption during frying and enhance fiber content, enabling snack brands to align with regulatory and consumer health expectations. This transition is expanding the market beyond traditional potato and corn bases into functional snack solutions.

Advanced Extrusion and Custom Texture Engineering

The adoption of twin-screw extrusion and co-extrusion technologies has enabled highly customized shapes, layered structures, and 3D pellet formats. Manufacturers are leveraging these technologies to create differentiated snack textures such as hollow cores, laminated layers, and tridimensional shapes. Automation, energy-efficient drying systems, and digital quality control integration are further enhancing production efficiency. As global snack brands seek differentiation through texture innovation, pellet suppliers are transitioning from commodity producers to strategic R&D partners.

What are the key drivers in the snack pellets market?

Rising Global Packaged Snack Consumption

Urbanization, dual-income households, and changing eating habits have significantly increased demand for convenient snack foods. The global packaged snack industry exceeds USD 600 billion and continues to expand steadily, directly stimulating demand for pellet intermediates used in extruded and expanded snack production. Emerging markets in Asia and Latin America are witnessing rapid growth in branded snack penetration, further accelerating pellet demand.

Operational Flexibility and Cost Efficiency

Snack pellets allow manufacturers to separate extrusion from final frying or baking stages, reducing transportation costs and minimizing product breakage. This flexibility supports export-oriented snack production models where pellets are shipped in bulk and expanded closer to retail markets. Cost optimization, inventory management efficiency, and reduced wastage are key drivers encouraging manufacturers to adopt pellet-based production systems.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in potato starch, corn derivatives, rice flour, and edible oil prices directly impact production costs. Climate variability, agricultural policies, and supply chain disruptions can compress margins, particularly for small and mid-sized manufacturers.

Health Regulations and Reformulation Pressures

Increasing scrutiny over ultra-processed foods, sodium levels, and fat content is pushing manufacturers to invest in R&D and reformulation. Compliance with food safety certifications such as BRCGS, HACCP, and ISO 22000 adds operational costs and complexity.

What are the key opportunities in the snack pellets industry?

Emerging Market Manufacturing Hubs

Countries such as India, Vietnam, Mexico, and Poland are emerging as export-oriented snack processing hubs. Government incentives supporting food processing infrastructure, including initiatives like “Make in India” and “Made in China 2025,” are encouraging pellet production expansion. Establishing regional extrusion facilities in these markets offers cost advantages and proximity to growing consumer bases.

Premium and Specialty Pellet Development

There is strong opportunity in specialty pellets designed for baked snacks, air-popped formats, and reduced-oil applications. Custom-designed 3D shapes and multigrain blends allow suppliers to command premium pricing while supporting brand differentiation in mature markets such as the U.S. and Western Europe.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3150 Million |

| Market Size in 2026 | USD 3427.20 Million |

| Market Size in 2031 | USD 5224.97 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global snack pellets market demonstrates strong product diversification driven by evolving consumer preferences, manufacturing flexibility, and innovation in extrusion technology. Potato-based snack pellets continue to dominate the global market, accounting for approximately 34% share in 2025. Their leadership position is primarily supported by superior expansion characteristics, uniform frying performance, and the ability to deliver consistent texture and mouthfeel across multiple snack formats. The high starch content in potatoes enables optimal puffing and structural integrity during processing, making them the preferred raw material for large-scale snack manufacturers seeking operational efficiency and standardized product quality. Additionally, potato-based pellets offer strong compatibility with flavor coatings and seasoning applications, further strengthening their adoption among branded snack producers.Corn-based pellets represent a significant secondary segment, particularly across North America and Latin America where corn remains a staple agricultural commodity and cost-effective input material. These pellets are widely utilized in traditional extruded snacks and shaped products due to their favorable expansion properties and relatively lower raw material volatility. Rice-based and tapioca-based pellets maintain strong demand in Asia-Pacific markets, where regional taste preferences favor lighter textures and gluten-free snack alternatives. Their neutral flavor profile enables customization for both savory and sweet applications, supporting rapid adoption among regional snack brands.Multigrain and pulse-based pellets are emerging as the fastest-growing product category, supported by rising consumer awareness regarding protein intake, digestive health, and clean-label ingredients. Manufacturers are increasingly incorporating lentils, chickpeas, quinoa, and other functional grains to position products within premium and better-for-you snack categories. Furthermore, tridimensional and laminated pellet formats are gaining traction in premium snack segments where texture differentiation, visual appeal, and innovative shapes enhance product positioning and shelf visibility. These advanced formats allow manufacturers to introduce value-added snacks that command higher margins and cater to evolving consumer expectations for experiential snacking.

Application Insights

Packaged snack manufacturers remain the dominant application segment, accounting for nearly 71% of global snack pellet demand. The leading driver behind this segment’s dominance is the scalability and production efficiency that pellets offer compared to traditional direct extrusion snacks. Snack pellets enable manufacturers to decouple production and expansion processes, allowing centralized pellet manufacturing and decentralized frying or expansion closer to consumer markets. This flexibility significantly reduces logistics costs, enhances inventory management, and supports rapid product launches aligned with changing flavor trends.Quick Service Restaurants (QSRs) are increasingly incorporating ready-to-fry pellet-based snacks into menus as operators seek standardized, easy-to-prepare side dishes and appetizers that maintain consistency across outlets. Pellet-based snacks provide operational convenience, reduced preparation time, and extended shelf stability, making them particularly attractive for high-volume foodservice environments. Retail-ready frozen and semi-finished pellets are also gaining traction, especially in emerging economies where modern retail expansion and home consumption trends are accelerating demand for convenient snack preparation solutions.Export-oriented snack processing units form a critical application segment, particularly across Asia-Pacific and Eastern Europe. These facilities support global supply chains by producing standardized pellets that can be customized regionally through localized frying, seasoning, and packaging. The growing globalization of snack brands and contract manufacturing partnerships continues to strengthen pellet adoption across international processing networks.

Distribution Channel Insights

Direct B2B supply agreements dominate distribution channels, accounting for more than 62% of total market revenue. The primary growth driver for this segment is long-term procurement contracts between pellet manufacturers and large snack brands seeking stable raw material supply, price predictability, and quality assurance. These partnerships enable efficient production planning and support economies of scale across industrial snack manufacturing operations.Contract manufacturing supply chains are expanding rapidly as private-label snack brands gain momentum across global retail channels. Retailers increasingly rely on third-party manufacturers that utilize standardized pellet inputs to produce customized snack offerings under store brands. Foodservice ingredient distributors continue to play a vital role in regional markets by bridging supply gaps for smaller processors and independent foodservice operators.Private-label pellet supply is expanding notably across North America and Europe, supported by retailer investments in differentiated snack portfolios and competitive pricing strategies. Meanwhile, digital procurement platforms are gradually transforming industrial sourcing practices by improving price transparency, supplier comparison, and procurement efficiency. These platforms enable manufacturers to optimize sourcing decisions while strengthening supply chain resilience.

Technology Insights

Twin-screw extrusion technology leads global production with approximately 41% share of installed capacity, primarily driven by its superior process control, ingredient flexibility, and ability to produce complex shapes and textures. The leading growth driver for this segment is its capability to incorporate diverse raw materials such as multigrain blends, plant proteins, and functional ingredients while maintaining consistent product quality. Twin-screw systems also allow precise control over moisture content, density, and expansion behavior, enabling manufacturers to develop innovative premium snack formats.Single-screw extrusion technology remains widely used in cost-sensitive markets due to lower capital investment requirements and operational simplicity. This technology continues to serve high-volume production of conventional pellet formats where product complexity is limited but production efficiency remains critical. Co-extrusion technology is emerging as an important innovation area, allowing layered snack structures and filled pellet designs that enhance product differentiation.Hot air expansion processing is gaining adoption as manufacturers respond to increasing demand for low-oil and reduced-fat snack options. By minimizing frying requirements, this technology aligns with global health and wellness trends while enabling brands to position products within baked or air-expanded snack categories without compromising texture or crunch.

Explore more data points, trends and opportunities Download Free Sample Report

Snack Pellets Market Segmentations

By Product Type

- Potato-Based Snack Pellets

- Corn-Based Snack Pellets

- Rice-Based Snack Pellets

- Tapioca-Based Snack Pellets

- Multigrain & Pulse-Based Snack Pellets

- Other Cereal & Specialty Pellets

By Form

- Dried Pellets

- Fresh/Un-dried Pellets

- Frozen Pellets

By Shape Type

- 2D Pellets

- 3D Pellets

- Laminated Pellets

- Die-Face Expanded Pellets

- Custom & Designer Shapes

By Processing Technology

- Single-Screw Extrusion

- Twin-Screw Extrusion

- Co-Extrusion Technology

- Hot Air Expansion Processing

By Distribution Channel

- Direct B2B Supply Contracts

- Food Ingredient Distributors

- Contract Manufacturing Supply

- Private Label Supply Chains

- Digital Procurement Platforms

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global snack pellets market, accounting for approximately 38% in 2025, supported by rapid urbanization, expanding middle-class populations, and increasing consumption of packaged convenience foods. China leads regional production due to the presence of large-scale extrusion facilities, strong domestic demand, and extensive export-oriented manufacturing capabilities. India represents the fastest-growing country in the region, expanding at over 11% CAGR, driven by rising investments in food processing infrastructure, rapid expansion of organized snack brands, and increasing penetration of modern retail and e-commerce channels. Additionally, favorable government initiatives supporting food manufacturing and agricultural processing are accelerating industry growth.Indonesia and Vietnam are emerging as secondary manufacturing hubs due to competitive labor costs, improving logistics networks, and rising foreign direct investment in snack production facilities. Regional growth is further supported by evolving consumer preferences toward affordable indulgence snacks, increasing adoption of western-style snack formats, and strong demand for localized flavors adapted to regional tastes.

Europe

Europe accounts for nearly 27% of the global market, led by Germany, Poland, Spain, and the Netherlands. Regional growth is primarily driven by the expansion of private-label snack brands and strong retailer influence across supermarket chains. Poland serves as a key export hub supplying pellet-based snack products across European Union markets due to its cost-efficient manufacturing base and strategic geographic location. Increasing consumer preference for baked, multigrain, and healthier snack alternatives is encouraging manufacturers to innovate with alternative raw materials and advanced pellet formats.Sustainability regulations and clean-label requirements across Europe are also accelerating adoption of plant-based and reduced-oil snack products, encouraging investment in advanced extrusion technologies. Additionally, high demand for premium snack experiences and gourmet textures continues to support growth in tridimensional and laminated pellet formats.

North America

North America represents approximately 21% of global demand, with the United States leading regional consumption due to strong innovation capabilities and a highly developed snack food industry. Regional growth is driven by rising demand for premium, functional, and better-for-you snack products, encouraging diversification of pellet formulations including protein-enriched and gluten-free variants. The presence of major snack brands and continuous product innovation cycles further support sustained pellet demand.Mexico plays a significant role as an export-oriented production hub, benefiting from integrated supply chains and trade agreements that facilitate cross-border snack manufacturing. Growth is also supported by increasing private-label penetration and expanding convenience store networks across the region.

Latin America

Latin America’s snack pellets market is led by Brazil and Mexico, where rising disposable incomes and expanding urban populations are driving packaged snack consumption. Regional growth is supported by improving food processing infrastructure, increasing investments in local extrusion facilities, and strong cultural acceptance of corn-based snack products. Manufacturers are increasingly adopting pellet technology to enhance production efficiency and introduce innovative snack shapes tailored to regional flavor preferences.The expansion of modern retail formats and growing demand for affordable snack options among younger consumers continue to strengthen market penetration across secondary economies within the region.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, led by key markets including the UAE, Saudi Arabia, and South Africa. Regional expansion is driven by rapid urbanization, a growing young population, and increasing penetration of international packaged snack brands. Rising investments in food manufacturing zones and import substitution strategies are encouraging local pellet production capabilities.Growth is further supported by expanding modern retail infrastructure, rising tourism-driven foodservice demand, and increasing consumer preference for convenient ready-to-fry snack products. As disposable incomes improve and western snacking habits become more prevalent, demand for diversified pellet formats is expected to accelerate across both Gulf Cooperation Council countries and emerging African economies.

Key Players in the Snack Pellets Market

- Limagrain Ingredients

- Liven S.A.

- J.R. Short Milling Company

- Mafin S.p.A.

- Noble Agro Food Products

- Leng-d'Or S.A.U.

- Pellsnack Products GmbH

- Pasta Foods Ltd.

- Intersnack Group

- Bach Snacks S.A.

- Chhajed Foods Pvt. Ltd.

- Quality Pellets A/S

- SanoRice Holding B.V.

- Snack Creations Ltd.

- Grupo Michel