Smart Pet Products Market Size

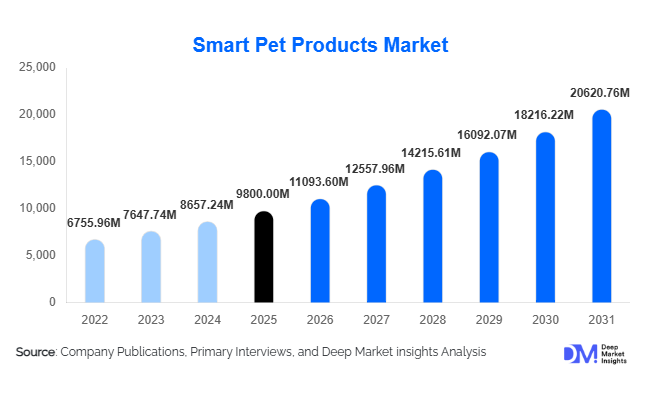

According to Deep Market Insights, the global smart pet products market size was valued at USD 9,800 million in 2025 and is projected to grow from USD 11,093.60 million in 2026 to reach USD 20,620.76 million by 2031, expanding at a CAGR of 13.2% during the forecast period (2026–2031). The market growth is primarily driven by the increasing humanization of pets, rising adoption of IoT-enabled devices, and growing demand for automated and AI-integrated pet care solutions that enhance pet health, safety, and owner convenience.

Key Market Insights

- Smart pet products are increasingly evolving into multifunctional, AI-enabled devices, providing health monitoring, feeding automation, and real-time tracking to enhance pet well-being.

- North America dominates the market, supported by high pet ownership rates, disposable income, and early adoption of smart home technologies.

- Asia-Pacific is the fastest-growing region, with countries like China and India driving demand through rising urbanization and expanding middle-class populations.

- Online retail is the primary distribution channel, providing consumers with access to a wide range of smart pet products, comparison tools, and convenient purchasing options.

- Integration with smart home ecosystems and IoT platforms is reshaping consumer engagement, enabling remote pet monitoring, automated feeding, and voice-assisted controls.

- Subscription-based services and consumables, such as refill packs for smart feeders or health monitoring analytics, are emerging as new revenue models for manufacturers.

What are the latest trends in the smart pet products market?

AI-Enabled Health Monitoring and Preventive Care

Smart pet products are increasingly integrating AI to provide predictive health insights. Wearables and monitoring devices now track activity, sleep patterns, and vital signs to detect early signs of illness or behavioral issues. This trend enables preventive care, reduces vet visits, and increases the overall lifespan and well-being of pets. Manufacturers are collaborating with veterinary service providers and insurance companies to develop data-driven solutions, offering personalized recommendations and creating new avenues for revenue through subscription analytics.

Smart Home Integration and IoT Connectivity

Products like automated feeders, GPS trackers, and interactive toys are increasingly integrated with home IoT systems. Wi-Fi and Bluetooth-enabled devices allow owners to manage multiple aspects of pet care remotely via mobile apps. Smart voice assistants are also being leveraged to issue feeding commands or check real-time pet activity. The rise of hybrid connectivity devices ensures seamless functionality even in regions with variable network coverage. Consumers are favoring products that combine safety, entertainment, and health monitoring within a single connected ecosystem.

What are the key drivers in the smart pet products market?

Rising Pet Humanization

Globally, pets are increasingly treated as family members, driving higher spending on premium products. Owners are seeking devices that enhance pet safety, comfort, and health. High-value segments such as smart collars, interactive toys, and health-monitoring wearables are benefiting from this emotional attachment, encouraging innovation and adoption across pet types and regions.

Technological Advancements in IoT and AI

Advances in IoT, cloud computing, and AI are enabling smarter and more connected devices. Real-time monitoring, predictive analytics, and automated interventions allow owners to manage pet care efficiently. The integration of AI into wearable devices helps in early detection of health anomalies and improves behavioral training, further expanding market adoption.

Urbanization and Busy Lifestyles

With increasing urban living and longer working hours, pet owners seek automation and remote monitoring solutions. Smart feeders, pet cameras, and GPS trackers allow owners to maintain pet routines and safety remotely. Urban populations are also more tech-savvy, preferring devices that offer convenience, reliability, and integration with existing smart home ecosystems.

What are the restraints for the global market?

High Product Costs

Advanced smart pet products often carry premium pricing due to technology integration, R&D, and brand positioning. High costs limit adoption in price-sensitive regions, particularly among first-time pet owners or emerging markets.

Data Privacy and Security Concerns

As connected devices collect and transmit sensitive data, including location and behavioral patterns, concerns about cybersecurity and privacy can hinder adoption. Compliance with data protection regulations is essential, but small manufacturers may struggle to implement robust security measures, impacting consumer confidence.

What are the key opportunities in the smart pet products industry?

Integration of Predictive Analytics and AI Health Monitoring

AI-driven health monitoring provides a significant growth opportunity. Devices capable of predictive diagnostics and early disease detection allow manufacturers to partner with veterinary services and pet insurance providers. Subscription-based analytics and personalized health recommendations create recurring revenue streams while offering differentiated products that improve pet wellness outcomes.

Expansion in Emerging Markets

Rapid urbanization, growing middle-class populations, and rising pet ownership in countries like China, India, and Brazil present untapped opportunities. Affordable smart devices tailored to regional preferences, multilingual app support, and localized customer service can help capture this expanding consumer base. Partnerships with regional e-commerce platforms can further enhance market penetration.

Subscription Models and Product Ecosystems

Moving beyond one-time product sales, manufacturers can develop ecosystem-based offerings and subscription services, including food refills, health analytics, and premium app features. Bundled solutions enhance customer retention, increase lifetime value, and provide a steady revenue stream, while fostering brand loyalty through integrated pet care solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9800 Million |

| Market Size in 2026 | USD 11093.60 Million |

| Market Size in 2031 | USD 20620.76 Million |

| CAGR | 13.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pet monitoring & tracking devices lead the smart pet products market with a 32% share in 2025, primarily driven by increasing concerns around pet safety, theft prevention, and real-time location tracking. The growing adoption of GPS-enabled collars and AI-powered health monitoring wearables reflects a broader shift toward preventive pet healthcare. Consumers are increasingly prioritizing devices that offer multi-functional capabilities such as activity tracking, sleep monitoring, and early disease detection, which strengthens the dominance of this segment. In terms of connectivity, Wi-Fi-enabled devices hold a leading 45% share, as they enable seamless integration with smart home ecosystems and provide real-time data access via mobile applications. This is particularly relevant in urban households where remote monitoring is essential.

By pet type, dogs represent the largest segment, accounting for 58% of total market demand, driven by higher ownership rates and greater spending on training, safety, and monitoring solutions compared to other pets. Distribution-wise, online retail channels dominate with a 52% share, supported by the rapid growth of e-commerce, wider product availability, and the ability to compare features and pricing easily. From a pricing perspective, mid-range products lead with a 47% market share, as they strike an optimal balance between affordability and advanced features, making them accessible to a broader consumer base. In terms of end users, residential pet owners account for over 70% of the market, driven by increasing pet humanization and the need for convenient, technology-driven pet care solutions in modern households.

Application Insights

The residential segment remains the primary application area for smart pet products, driven by increasing demand for convenience, automation, and enhanced pet well-being. Products such as smart feeders, interactive toys, and health monitoring devices are widely adopted by individual pet owners seeking to manage pet care remotely. The rising trend of single-person households and dual-income families has further accelerated the adoption of these solutions, as owners rely on automation to maintain consistent feeding and monitoring routines.

Commercial applications are emerging as a high-growth segment, expanding at an estimated 15% CAGR, particularly across veterinary clinics, pet boarding facilities, and training centers. These establishments are leveraging smart technologies to improve operational efficiency, monitor multiple animals simultaneously, and enhance service quality. Additionally, new applications are developing in areas such as telehealth and pet insurance integration, where connected devices provide real-time data for remote diagnostics, health assessments, and risk profiling. This evolution is transforming smart pet products from standalone devices into integral components of a broader digital pet care ecosystem.

Distribution Channel Insights

Online distribution channels dominate the smart pet products market, driven by the rapid expansion of e-commerce platforms and direct-to-consumer (D2C) brand strategies. Consumers increasingly prefer online platforms due to the convenience of home delivery, access to detailed product information, user reviews, and competitive pricing. The ability to compare multiple brands and features in real time has significantly enhanced online purchasing behavior, particularly among younger, tech-savvy consumers.

Offline channels, including specialty pet stores, supermarkets, and veterinary clinics, continue to play a crucial role, especially for premium and high-involvement purchases where consumers seek hands-on demonstrations and expert advice. These channels are particularly relevant for first-time buyers who require guidance on product functionality and usage. Additionally, subscription-based and membership models are gaining traction, offering recurring delivery of consumables and access to premium digital services such as health analytics. Social media platforms and influencer marketing are also emerging as powerful distribution enablers, shaping consumer preferences and driving brand engagement across digital ecosystems.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Pet Products Market Segmentations

By Product Type

- Smart Feeding Devices

- Pet Monitoring & Tracking Devices

- Smart Pet Doors & Access Control

- Interactive Entertainment Devices

- Pet Safety & Training Devices

- Smart Hygiene Solutions

By Connectivity Technology

- Wi-Fi Enabled Devices

- Bluetooth Enabled Devices

- Cellular (SIM-Based) Devices

- Hybrid Connectivity Devices

By Pet Type

- Dogs

- Cats

- Small Animals

By Distribution Channel

- Online Retail

- Specialty Pet Stores

- Supermarkets/Hypermarkets

- Veterinary Clinics

By End User

- Residential Pet Owners

- Pet Boarding & Daycare Centers

- Veterinary Clinics

- Pet Training Facilities

Regional Insights

North America

North America remains the largest market, accounting for approximately 38% of global revenue in 2025, with the United States contributing the majority share. The region’s dominance is driven by high pet ownership rates, high disposable incomes, and early adoption of advanced technologies. Consumers in this region show a strong preference for premium, integrated smart pet solutions that combine feeding, monitoring, and health tracking within a single ecosystem. Additionally, the widespread penetration of smart home technologies and high awareness of pet wellness are key growth drivers. The presence of major market players and continuous product innovation further reinforces North America's leadership position.

Europe

Europe holds around 27% of the global market share, led by countries such as Germany, the United Kingdom, and France. Growth in this region is driven by increasing pet humanization, high purchasing power, and strong demand for sustainable and eco-friendly products. European consumers are particularly inclined toward multifunctional devices that align with environmental standards and ethical manufacturing practices. Regulatory frameworks supporting pet welfare and product safety also contribute to market expansion. Additionally, rising urbanization and the growing trend of companion animals among aging populations are further supporting demand for smart pet solutions.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 15%, and accounts for approximately 22% of the global market. Key countries such as China, India, Japan, and South Korea are driving growth through rapid urbanization, increasing disposable incomes, and expanding middle-class populations. The rising trend of pet ownership among younger demographics, coupled with strong adoption of digital technologies, is accelerating demand for smart pet products. Additionally, the presence of large-scale manufacturing hubs and cost-effective production capabilities in the region supports supply growth. Government initiatives promoting digital ecosystems and e-commerce expansion further facilitate market penetration.

Latin America

Latin America represents around 7% of the market, with Brazil and Mexico emerging as key contributors. Growth in this region is driven by increasing urbanization, rising awareness of pet health and wellness, and gradual improvement in disposable incomes. Consumers are increasingly adopting mid-range smart pet products, particularly automated feeders and tracking devices. The expansion of online retail platforms and improved logistics infrastructure are also supporting market accessibility. Additionally, the growing influence of social media and digital marketing is enhancing product awareness and adoption across urban populations.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of the global market, with countries such as the UAE, Saudi Arabia, and South Africa leading demand. Market growth is driven by rising disposable incomes, increasing adoption of premium pet care products, and a growing inclination toward luxury lifestyles. In the Middle East, high-income consumers are particularly drawn to advanced smart pet solutions that offer convenience and exclusivity. In Africa, urbanization and expanding middle-class populations are gradually increasing pet ownership and demand for basic smart pet products. Government support for digital transformation and improvements in retail infrastructure are further facilitating market growth, while increasing intra-regional trade is enhancing product availability.

Key Players in the Smart Pet Products Market

- Mars Incorporated

- Nestlé Purina PetCare

- Xiaomi Corporation

- Garmin Ltd.

- Tractive GmbH

- Whistle Labs Inc.

- PetSafe (Radio Systems Corporation)

- FitBark Inc.

- Dogness International Corporation

- Petcube Inc.

- Sure Petcare

- Invoxia

- Wagz Inc.

- Loc8tor Ltd.

- i4C Innovations