Sleep Drink Market Size

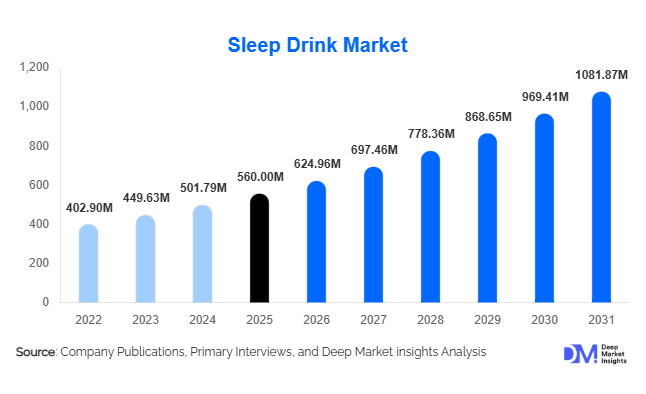

According to Deep Market Insights, the global sleep drink market size was valued at USD 560 million in 2025 and is projected to grow from USD 624.96 million in 2026 to reach USD 1,081.87 million by 2031, expanding at a CAGR of 11.6% during the forecast period (2026–2031). The sleep drink market growth is primarily driven by rising awareness around sleep health, increasing prevalence of insomnia and stress-related disorders, and growing consumer preference for natural, non-pharmaceutical sleep aids. The market is also benefiting from innovation in functional beverages, including plant-based formulations and clean-label products that align with evolving wellness trends.

Key Market Insights

- Sleep drinks are gaining traction as a natural alternative to pharmaceutical sleep aids, particularly among urban consumers seeking convenient wellness solutions.

- Ready-to-drink (RTD) formats dominate the market, driven by convenience, portability, and increasing on-the-go consumption patterns.

- North America leads the global market, supported by high awareness of sleep disorders and strong distribution networks.

- Asia-Pacific is the fastest-growing region, fueled by rising stress levels, urbanization, and increasing adoption of functional beverages.

- Plant-based and clean-label sleep drinks are expanding rapidly, as consumers shift toward organic and herbal formulations.

- Online retail channels are transforming distribution, enabling direct-to-consumer models and subscription-based wellness solutions.

What are the latest trends in the sleep drink market?

Rise of Clean-Label and Plant-Based Formulations

Consumers are increasingly demanding transparency in ingredients, driving the adoption of clean-label sleep drinks formulated with natural botanicals such as chamomile, ashwagandha, and valerian root. Plant-based formulations using almond, oat, and soy milk are gaining popularity, particularly among vegan and health-conscious consumers. Manufacturers are reducing sugar content, eliminating artificial additives, and focusing on functional blends that combine sleep support with additional benefits such as immunity and stress relief. This trend is encouraging premium product positioning and expanding the consumer base beyond traditional users of sleep aids.

Integration with Digital Health and Personalization

The growing adoption of wearable devices and sleep tracking applications is enabling the development of personalized sleep solutions. Companies are exploring subscription-based models that tailor sleep drink formulations based on individual sleep patterns and lifestyle data. Integration with mobile apps allows consumers to track sleep quality and optimize consumption timing, enhancing product effectiveness. This convergence of nutrition and digital health is expected to redefine consumer engagement and create new revenue streams within the sleep drink market.

What are the key drivers in the sleep drink market?

Increasing Prevalence of Sleep Disorders

The rising incidence of insomnia, anxiety, and lifestyle-related sleep disruptions is a major driver of market growth. Factors such as increased screen time, irregular work schedules, and high stress levels are contributing to poor sleep quality globally. Sleep drinks provide a convenient and accessible solution, particularly for individuals seeking immediate relief without medical intervention.

Shift Toward Preventive Healthcare and Wellness

Consumers are increasingly prioritizing preventive health measures, driving demand for functional beverages that support overall well-being. Sleep drinks are positioned as part of a broader wellness routine, appealing to individuals focused on mental health, stress management, and recovery. This shift is particularly prominent among millennials and working professionals.

What are the restraints for the global market?

Regulatory Challenges Across Regions

Variations in regulations governing ingredients such as melatonin create challenges for global market expansion. Inconsistent labeling requirements and restrictions on dosage levels limit product standardization and increase compliance costs for manufacturers.

Consumer Skepticism Regarding Efficacy

Despite growing awareness, some consumers remain skeptical about the effectiveness of sleep drinks compared to pharmaceutical solutions. Limited clinical evidence for certain formulations and varying individual responses can hinder widespread adoption.

What are the key opportunities in the sleep drink industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific and Latin America present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of sleep health. Localized formulations incorporating traditional herbal ingredients can enhance market penetration and consumer acceptance.

Multi-Functional Beverage Innovation

There is strong potential for developing sleep drinks that offer additional benefits such as immunity support, digestive health, and stress reduction. These multi-functional beverages can expand consumption occasions and attract a broader audience beyond individuals with sleep disorders.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 560 Million |

| Market Size in 2026 | USD 624.96 Million |

| Market Size in 2031 | USD 1081.87 Million |

| CAGR | 11.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global sleep drink market is witnessing robust growth, driven by increasing awareness of sleep health, rising stress levels, and the growing adoption of functional beverages as part of daily wellness routines. Among product types, melatonin-based sleep drinks dominate the market, accounting for approximately 34% of the total market share in 2025. This leadership position is primarily attributed to the scientifically validated role of melatonin in regulating the body’s circadian rhythm and improving sleep onset latency. Consumers seeking fast-acting and clinically supported solutions often prefer melatonin-infused beverages, especially in developed markets where awareness of sleep disorders and supplement efficacy is high. The availability of these drinks in various flavors, formats, and dosages further enhances their appeal, enabling brands to cater to a wide demographic range.In addition to melatonin-based offerings, herbal sleep drinks are gaining substantial traction globally, particularly among consumers who prefer natural and plant-based alternatives. Ingredients such as chamomile, valerian root, ashwagandha, lavender, and passionflower are widely incorporated into these formulations, leveraging their traditional use in promoting relaxation and sleep. This segment is especially prominent in regions with strong cultural roots in herbal medicine, where consumers are more inclined to trust natural remedies over synthetic or hormone-based solutions. The clean-label movement and increasing demand for organic products are further accelerating the growth of herbal sleep beverages.Functional non-melatonin beverages are also emerging as a significant segment, catering to consumers who are cautious about hormone intake or seek gentler, non-habit-forming sleep aids. These drinks often include ingredients such as magnesium, L-theanine, GABA, and adaptogens that support relaxation and stress reduction without directly influencing hormonal pathways. The growing popularity of holistic wellness approaches and preventive healthcare is expected to drive continued innovation in this segment, making it a key area of focus for manufacturers aiming to diversify their product portfolios and address evolving consumer preferences.

Application Insights

From an application perspective, functional sleep beverages are primarily consumed by working professionals and individuals experiencing stress-related sleep disturbances, with this segment accounting for nearly 36% of overall demand. The dominance of this segment can be attributed to the increasing prevalence of high-pressure work environments, extended screen time, and irregular schedules, all of which contribute to sleep deprivation and insomnia. Sleep drinks offer a convenient and non-invasive solution for this demographic, enabling them to incorporate sleep support into their daily routines without the need for prescription medications.Another key application segment is athletes and fitness enthusiasts, who are increasingly recognizing the importance of sleep in recovery, muscle repair, and overall performance optimization. Sleep drinks formulated with recovery-enhancing ingredients are being integrated into post-workout routines, highlighting the intersection of sports nutrition and sleep health. This trend is particularly evident in developed markets, where consumers are more aware of the role of sleep in physical performance and longevity.The hospitality sector is also emerging as a niche yet promising application area, as hotels and wellness resorts seek to enhance guest experiences by offering sleep-enhancing products as part of premium wellness packages. Sleep drinks are being incorporated into in-room amenities, spa treatments, and bedtime rituals, reflecting a broader trend toward experiential wellness. This application segment is expected to grow steadily as the global travel and tourism industry increasingly emphasizes holistic well-being.

Distribution Channel Insights

In terms of distribution channels, online retail leads the market with approximately 31% share, driven by the rapid expansion of e-commerce platforms and the growing popularity of direct-to-consumer business models. The convenience of online shopping, coupled with access to a wide variety of products and detailed information, has made this channel particularly attractive for health-conscious consumers. Subscription-based models are also gaining traction within the online segment, enabling brands to build long-term customer relationships and ensure repeat purchases.Supermarkets and hypermarkets continue to play a crucial role in market growth by providing high product visibility and accessibility. These retail outlets allow consumers to physically examine products and make informed purchasing decisions, which is especially important for new or unfamiliar categories such as sleep drinks. The presence of dedicated health and wellness sections in modern retail stores further supports the growth of this channel.Pharmacies and specialty health stores cater to consumers seeking clinically positioned or medically endorsed sleep solutions. These channels are particularly important for melatonin-based and functional beverages that are perceived as closer to nutraceutical products. The credibility associated with pharmacy distribution enhances consumer trust and supports the adoption of sleep drinks among individuals with chronic sleep issues.

Consumer Type Insights

Working professionals dominate the consumer segment, accounting for around 36% of the market share, driven by high stress levels, demanding work schedules, and increasing exposure to digital devices. The need for effective yet convenient sleep solutions has made this group the primary target audience for sleep drink manufacturers. Products tailored to this segment often emphasize quick action, portability, and compatibility with busy lifestyles.The geriatric population represents another significant consumer segment, as aging is often associated with changes in sleep patterns and increased prevalence of insomnia. Sleep drinks offer a non-pharmaceutical alternative for older adults seeking to improve sleep quality without the side effects of traditional medications. This segment is expected to grow steadily in line with global demographic trends and the increasing aging population.Young adults are also emerging as a key consumer group, driven by rising awareness of preventive healthcare and wellness. This demographic is more likely to experiment with functional beverages and incorporate them into their daily routines as part of a broader focus on mental and physical well-being. Athletes, while representing a smaller share, are a rapidly growing segment, emphasizing the importance of sleep in achieving peak performance and recovery.

Packaging Insights

Packaging plays a critical role in influencing consumer purchasing decisions and brand perception within the sleep drink market. Bottles remain the leading packaging format, capturing approximately 45% of the market share, due to their convenience, durability, and strong branding potential. Bottled sleep drinks are often positioned as premium products, with visually appealing designs and informative labeling that highlight functional benefits and ingredient transparency.Cans are gaining popularity, particularly for single-serve consumption and on-the-go usage. Their lightweight nature and recyclability make them an attractive option for environmentally conscious consumers. Additionally, cans are well-suited for carbonated or lightly flavored sleep beverages, expanding the range of product offerings in the market.Sachets and powder formats are emerging as cost-effective and portable alternatives, especially in price-sensitive and emerging markets. These formats allow consumers to customize dosage and preparation, making them suitable for a wide range of use cases. The growing demand for convenience and affordability is expected to drive further innovation in packaging solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Sleep Drink Market Segmentations

By Product Type

- Herbal Sleep Drinks

- Melatonin-Based Sleep Drinks

- Functional Non-Melatonin Beverages

- Dairy-Based Sleep Drinks

- Plant-Based Sleep Drinks

By Formulation Type

- Ready-to-Drink (RTD)

- Powder Mix

- Liquid Shots & Concentrates

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Pharmacies & Health Stores

- Specialty Wellness Stores

Regional Insights

North America

North America holds the largest share of the global sleep drink market, accounting for approximately 38% in 2025. The United States leads regional demand, supported by a high prevalence of sleep disorders, advanced healthcare infrastructure, and strong consumer awareness regarding the importance of sleep health. The region’s well-established functional beverage industry and widespread availability of products across multiple distribution channels further contribute to market growth. Additionally, the increasing adoption of personalized nutrition and wellness solutions is encouraging innovation in sleep drink formulations. Canada is also experiencing steady growth, driven by rising consumer preference for natural and organic products, as well as supportive regulatory frameworks for nutraceuticals. The presence of key market players, high disposable incomes, and a strong culture of health and wellness collectively act as major drivers for regional expansion.

Europe

Europe represents around 27% of the global market, with significant contributions from countries such as Germany, the United Kingdom, and France. The region’s growth is driven by high levels of health consciousness, increasing awareness of sleep-related issues, and a strong preference for clean-label and organic products. European consumers tend to prioritize sustainability and transparency, leading to increased demand for natural and ethically sourced ingredients in sleep drinks. Regulatory support for functional foods and beverages, along with the expansion of premium retail channels, further enhances market penetration. Additionally, the growing trend of preventive healthcare and the integration of wellness into daily lifestyles are key factors driving demand across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the global sleep drink market, with a CAGR exceeding 13% during the forecast period. Rapid urbanization, increasing work-related stress, and rising disposable incomes are major factors contributing to market growth in countries such as China, India, and Japan. The region’s strong cultural affinity for herbal and traditional medicine plays a significant role in driving the adoption of sleep drinks, particularly those formulated with natural ingredients. In addition, the expanding middle-class population and growing awareness of health and wellness are fueling demand for functional beverages. The proliferation of e-commerce platforms and digital marketing strategies is also enhancing product accessibility and consumer engagement, making Asia-Pacific a key growth engine for the global market.

Latin America

Latin America accounts for approximately 8% of the global market, with Brazil and Mexico serving as the primary growth hubs. The region is witnessing increasing awareness of sleep health, driven by urbanization and changing lifestyles. The growing popularity of functional beverages, coupled with rising disposable incomes, is supporting market expansion. Additionally, the influence of global wellness trends and the introduction of innovative products by international and local players are contributing to increased consumer adoption. Improvements in retail infrastructure and the expansion of online distribution channels are further enhancing market accessibility across the region.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market for sleep drinks, particularly in countries such as the UAE and South Africa. Rising disposable incomes, rapid urbanization, and increasing exposure to global wellness trends are key factors driving demand. The region’s growing interest in premium and functional beverages is also contributing to market development. Additionally, the expansion of modern retail formats and e-commerce platforms is improving product availability and consumer reach. As awareness of sleep health continues to increase, supported by educational initiatives and marketing campaigns, the adoption of sleep drinks is expected to accelerate across the region.

Key Players in the Sleep Drink Market

- PepsiCo Inc.

- Coca-Cola Company

- Nestlé S.A.

- Unilever PLC

- Danone S.A.

- Suntory Holdings

- Kirin Holdings

- Otsuka Holdings

- Rebbl Inc.

- Som Sleep

- Dream Water

- Neuro Brands

- Vital Proteins

- Hain Celestial Group

- Califia Farms