Skimmed Milk Powder Market Size

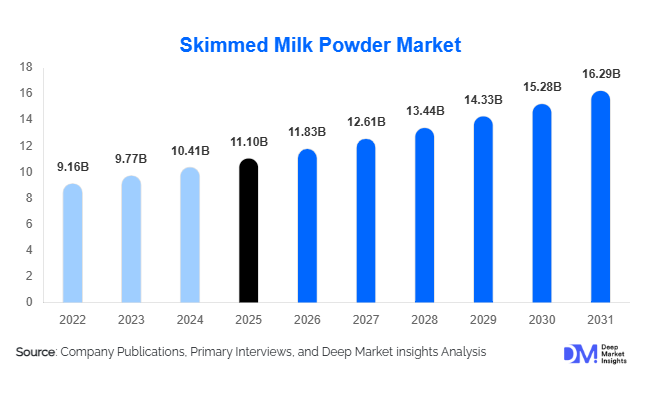

According to Deep Market Insights, the global skimmed milk powder (SMP) market size was valued at USD 11.1 billion in 2026 and is projected to grow from USD 11.83 billion in 2026 to reach USD 16.29 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The SMP market growth is primarily driven by rising demand for low-fat and high-protein dairy ingredients, expanding processed food and infant nutrition industries, and increasing adoption of fortified and instant SMP variants globally.

Key Market Insights

- Health-conscious consumers are driving SMP demand, favoring low-fat, high-protein dairy alternatives for bakery, beverages, and functional foods.

- Instant and fortified SMP products are gaining traction, due to ease of use, improved solubility, and enhanced nutritional benefits, making them preferred by food manufacturers and infant formula producers.

- Asia-Pacific leads in growth, driven by rising urban populations, increasing disposable incomes, and expanding food processing industries in India, China, and Southeast Asia.

- Europe remains a significant mature market, with Germany, France, and the U.K. showing stable demand for high-quality SMP and fortified variants.

- North America continues to account for a major share, led by U.S. and Canada’s established processed food and nutritional product industries.

- Technological advancements in processing and digital distribution, such as spray drying, instantization, and e-commerce, are enhancing product availability, shelf life, and consumer reach.

What are the latest trends in the skimmed milk powder market?

Fortified and Functional SMP Gaining Popularity

Manufacturers are increasingly offering SMP variants enriched with vitamins, minerals, and protein. These fortified powders cater to infant nutrition, sports supplements, and functional food applications. Enhanced formulations meet consumer demands for health, immunity, and wellness, while commanding premium pricing. The trend is particularly prominent in developed markets and urban areas of emerging economies.

Technological Integration in Processing and Distribution

Advanced spray drying, instantization, and digital traceability are transforming SMP production. Innovations improve solubility, shelf life, and product consistency. E-commerce platforms enable direct-to-consumer sales and supply to niche markets, reducing reliance on traditional retail. Traceability and sustainability certifications further strengthen consumer trust, particularly in quality-sensitive regions.

What are the key drivers in the skimmed milk powder market?

Rising Health-Conscious Consumer Base

Growing awareness about low-fat, high-protein diets drives SMP adoption in beverages, bakery, and nutritional products. Consumers increasingly prefer skimmed milk alternatives over full-fat variants for weight management and wellness, boosting demand globally.

Expansion of Processed Food and Infant Nutrition Industries

The growing bakery, confectionery, dairy beverage, and infant formula sectors are key contributors to SMP demand. Processed food manufacturers use SMP for texture enhancement, protein enrichment, and shelf stability, while infant formula producers rely on SMP as a primary ingredient for protein and micronutrient content.

Innovation and Functional Applications

Technological advancements, such as fortified, organic, and instant SMP, expand product applications and reach. These innovations allow manufacturers to enter premium segments and cater to health-focused consumer preferences.

What are the restraints for the global market?

Volatility in Raw Milk Prices

Fluctuations in raw milk supply and cost can directly impact SMP production margins. Seasonal changes, feed costs, and climate variations create production challenges, affecting pricing and market stability.

Trade Barriers and Regulatory Compliance

Strict quality regulations in regions like Europe and North America increase compliance costs for producers. Import tariffs and protectionist policies can hinder SMP trade, limiting market access for smaller or new entrants.

What are the key opportunities in the skimmed milk powder industry?

Expansion in Emerging Economies

Urbanization, rising disposable incomes, and expanding processed food sectors in Asia-Pacific, Africa, and Latin America present major growth opportunities. Governments supporting dairy infrastructure and supply chain development further enhance market potential.

Development of Fortified and Functional SMP Products

Opportunities exist for producing value-added SMP with enhanced nutritional properties, including protein enrichment, vitamins, minerals, and probiotics. Such products meet rising health and wellness demands and appeal to premium consumers in developed and emerging markets.

Integration of Advanced Processing and Digital Sales Channels

Manufacturers can leverage technologies like spray drying, instantization, and traceability systems to improve quality and extend shelf life. Digital platforms enable direct distribution to niche consumers, expanding market penetration and brand visibility globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.10 Billion |

| Market Size in 2026 | USD 11.83 Billion |

| Market Size in 2031 | USD 16.29 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global skimmed milk powder (SMP) market demonstrates strong diversification across product types, reflecting evolving consumer preferences, technological advancements in dairy processing, and expanding industrial applications. Instant SMP continues to dominate the market, accounting for approximately 38% of total revenue share. Its leadership position is primarily attributed to superior solubility, rapid dispersion properties, and enhanced reconstitution performance, making it highly suitable for beverages, bakery formulations, dairy blends, and infant nutrition products. The growing demand for convenient and ready-to-mix nutritional solutions across both developed and emerging economies further strengthens adoption of instant SMP among manufacturers seeking efficiency and consistency in large-scale production processes.Conventional SMP maintains a substantial presence within industrial and food processing applications where cost efficiency and bulk usage remain critical. Food processors utilize conventional variants extensively in confectionery, sauces, dairy recombination, and bakery products due to their stable shelf life and functional protein characteristics. Meanwhile, organic SMP is witnessing accelerated growth as consumers increasingly prioritize clean-label, sustainably sourced, and chemical-free dairy ingredients. Rising awareness surrounding environmental sustainability and animal welfare practices is encouraging dairy producers to expand certified organic offerings, particularly in Europe and North America.Fortified SMP variants enriched with vitamins, minerals, and functional nutrients are gaining strong momentum within premium nutrition segments. Demand is especially pronounced in infant nutrition, medical nutrition, and functional food categories, where enhanced nutritional density is a key purchasing criterion. Manufacturers are increasingly investing in value-added formulations to differentiate products, improve margins, and address growing health-conscious consumer bases worldwide.

Application Insights

Infant nutrition and formula applications represent the leading segment, capturing nearly 29% of global market share. The segment’s dominance is driven by increasing global focus on early-life nutrition, rising birth rates in developing economies, and growing parental awareness regarding protein intake, immune development, and balanced micronutrient consumption. SMP serves as a critical ingredient in infant formula due to its standardized protein content, long shelf stability, and ability to support precise nutritional formulation. Expanding female workforce participation and urban lifestyles are also accelerating reliance on packaged infant nutrition products, further reinforcing demand.Beyond infant nutrition, bakery applications are experiencing steady expansion as manufacturers incorporate SMP to enhance texture, browning properties, moisture retention, and nutritional value in baked goods. The dairy beverages segment is also emerging as a key growth avenue, supported by rising consumption of ready-to-drink milk beverages, flavored milk, and protein-enriched drinks. Functional foods and nutritional supplements are increasingly utilizing SMP due to its high-quality protein profile, emulsification capability, and compatibility with fortified formulations. The convergence of convenience foods and health-oriented consumption patterns continues to broaden SMP’s application landscape globally.

End-Use Insights

Food and beverage manufacturers constitute the largest end-user segment, accounting for approximately 41% of overall market demand. The segment’s leadership is driven by the widespread integration of SMP into processed foods, bakery products, dairy recombination, confectionery, sauces, and beverage formulations. SMP’s extended shelf life, ease of transportation, and cost-effective storage compared to liquid milk make it an essential ingredient for large-scale food manufacturing operations. Growing demand for packaged and convenience foods across urban populations further strengthens utilization among industrial processors.Infant formula producers represent another rapidly expanding end-use category, supported by continuous innovation in pediatric nutrition and stricter quality standardization requirements. Sports nutrition and performance wellness companies are increasingly incorporating SMP into protein powders, recovery beverages, and nutritional blends due to its balanced amino acid composition and affordability compared to specialized protein isolates. Additionally, export-oriented dairy trade, particularly from Oceania, Europe, and North America to Asia-Pacific and Middle Eastern markets, significantly reinforces global SMP consumption patterns and stabilizes international supply chains.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels, collectively accounting for nearly 45% of market share. Their leadership stems from extensive product visibility, consumer trust, and strong cold-chain and logistics infrastructure that supports consistent availability of dairy products. Large retail chains enable manufacturers to reach broad consumer bases while facilitating brand comparison and promotional activities that drive purchasing decisions.However, distribution dynamics are evolving rapidly with the expansion of online retail and specialty stores. E-commerce platforms are gaining traction as consumers increasingly prefer convenient purchasing options, subscription-based grocery models, and direct-to-consumer delivery systems. Online channels are particularly effective for premium and niche categories such as organic, fortified, and instant SMP variants, allowing brands to target health-conscious and specialized consumer segments. Specialty nutrition stores and pharmacy-linked retail outlets are also emerging as important channels for fortified and infant nutrition products, reflecting growing demand for personalized nutrition solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Skimmed Milk Powder Market Segmentations

By Product Type

- Instant Skimmed Milk Powder

- Conventional Skimmed Milk Powder

- Organic Skimmed Milk Powder

- Fortified Skimmed Milk Powder

By Application

- Infant Nutrition & Formula

- Bakery & Confectionery

- Dairy Beverages

- Functional & Sports Nutrition

- Other Processed Foods

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / E-commerce

- Specialty Stores

- Direct Industrial Supply

Regional Insights

North America

North America accounts for approximately 28% of the global SMP market, supported by strong demand from the United States and Canada. Regional growth is driven by advanced dairy processing infrastructure, high consumption of processed and convenience foods, and widespread adoption of protein-enriched nutritional products. Increasing consumer preference for high-protein diets, functional beverages, and sports nutrition products continues to stimulate SMP utilization across multiple industries. Additionally, technological innovation in dairy processing, strong cold-chain logistics, and well-established export capabilities enable consistent product quality and stable market expansion. Growing demand for clean-label and fortified dairy ingredients further contributes to sustained regional growth.

Europe

Europe represents nearly 30% of global market share, with Germany, France, and the United Kingdom serving as major contributors. The region benefits from a mature dairy industry, strong regulatory frameworks ensuring product quality, and high consumer awareness regarding nutrition and sustainability. Growth is supported by increasing demand for fortified, organic, and functional dairy ingredients aligned with health-conscious consumption trends. European dairy exporters also play a significant role in supplying SMP to emerging markets, strengthening international trade flows. Government support for sustainable agriculture practices and technological modernization of dairy farms further enhances production efficiency and long-term market stability.

Asia-Pacific

Asia-Pacific, accounting for approximately 34% of the global market, is the fastest-growing region driven by rapid urbanization, population growth, and rising disposable incomes across countries such as China, India, and Southeast Asian nations. Expanding middle-class populations are increasing consumption of packaged foods, infant formula, and nutritional beverages, significantly boosting SMP demand. Limited domestic milk production capacity in several countries increases reliance on imported SMP, supporting global trade expansion. Furthermore, growing awareness of protein intake, expansion of modern retail infrastructure, and government initiatives promoting nutritional security are accelerating adoption across both consumer and industrial applications.

Latin America

Latin America holds approximately 6% of the global market, led by Brazil and Mexico. Regional growth is supported by increasing consumption of processed foods, bakery products, and dairy-based beverages as urban lifestyles expand. Improving retail penetration and rising middle-income populations are contributing to gradual increases in SMP utilization. Additionally, investments in food processing industries and expanding local dairy production capabilities are strengthening market development. Despite moderate penetration levels, growing demand for affordable nutritional ingredients presents significant long-term growth opportunities.

Middle East & Africa

The Middle East & Africa region accounts for around 2% of global market share but demonstrates strong future potential. Growth is largely driven by import-dependent dairy markets in countries such as the United Arab Emirates, Saudi Arabia, and South Africa, where climatic conditions limit large-scale milk production. Rapid urban population growth, increasing demand for shelf-stable dairy products, and expanding foodservice industries are key growth drivers. Government food security initiatives and strategic dairy import programs further support market expansion. Additionally, rising intra-African trade agreements and improvements in distribution infrastructure are expected to enhance accessibility and stimulate regional demand over the forecast period.

Key Players in the Skimmed Milk Powder Market

- Fonterra Co-operative Group Limited

- Nestlé S.A.

- Danone S.A.

- Arla Foods amba

- FrieslandCampina N.V.

- Lactalis Group

- Dairy Farmers of America Inc.

- Saputo Inc.

- Meiji Holdings Co., Ltd.

- Yili Group

- Mengniu Dairy Company

- Land O’Lakes, Inc.

- Glanbia plc

- Agropur Cooperative

- Synlait Milk Limited