Shipping and Logistics Market Size

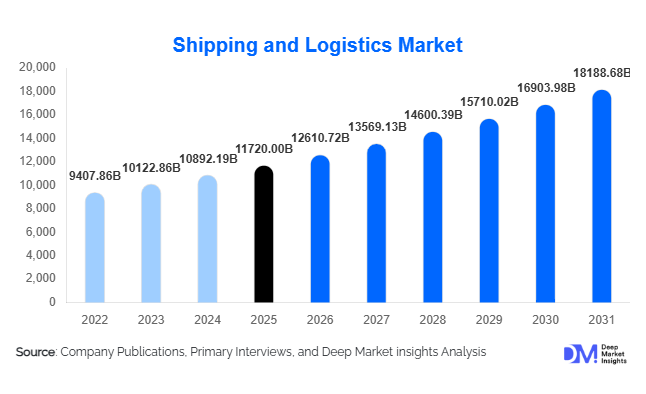

According to Deep Market Insights, the global shipping and logistics market size was valued at USD 11,720 billion in 2025 and is projected to grow from USD 12,610.72 billion in 2026 to reach USD 18,188.68 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The shipping and logistics market growth is primarily driven by rapid globalization of trade, expansion of e-commerce ecosystems, increasing cross-border industrial supply chains, and growing investments in digital freight infrastructure and smart warehousing technologies.

The market continues to evolve as global industries prioritize supply chain resilience, transportation efficiency, and real-time shipment visibility. Rising demand for fast delivery services, integrated multimodal transportation, and contract logistics solutions is significantly transforming the industry landscape. Logistics operators are increasingly investing in artificial intelligence, warehouse robotics, blockchain-enabled cargo tracking, and IoT-based fleet management systems to improve operational efficiency and customer satisfaction.Asia-Pacific remains the largest regional market due to its dominant manufacturing ecosystem, export-oriented economies, and large-scale infrastructure investments. Meanwhile, North America and Europe continue advancing smart logistics adoption and sustainable transportation initiatives. Growing demand for cold-chain logistics, pharmaceutical transportation, and e-commerce fulfillment services is further accelerating market expansion globally. Additionally, government infrastructure modernization programs, port expansion projects, and dedicated freight corridor developments across emerging economies are creating substantial long-term growth opportunities for logistics providers worldwide.

Key Market Insights

- E-commerce-driven logistics expansion is reshaping global supply chains, accelerating investments in last-mile delivery, urban fulfillment centers, and warehouse automation systems.

- Digitally enabled logistics platforms are gaining strong adoption globally, driven by AI-based route optimization, predictive analytics, and blockchain-enabled cargo visibility.

- Asia-Pacific dominates the global shipping and logistics market, led by China, India, Japan, and Southeast Asian manufacturing economies.

- India is emerging as one of the fastest-growing logistics markets globally, supported by infrastructure modernization, GST reforms, and rapid industrialization.

- Sustainable transportation solutions are becoming critical competitive differentiators, with companies investing heavily in electric fleets, LNG-powered vessels, and carbon-neutral logistics operations.

- Cold-chain logistics demand is rising significantly, supported by pharmaceutical exports, biologics transportation, and growing global food trade.

- Third-party logistics (3PL) services continue dominating outsourced supply chain management, as businesses increasingly focus on operational efficiency and cost optimization.

Shipping and Logistics Market Latest Trends

Rapid Digitalization of Global Logistics Networks

The global shipping and logistics industry is rapidly adopting advanced digital technologies to improve supply chain visibility, reduce operational costs, and enhance delivery efficiency. Artificial intelligence, blockchain platforms, cloud-based transportation management systems, and IoT-enabled cargo monitoring are increasingly becoming standard across modern logistics ecosystems. Companies are integrating predictive analytics to optimize routing, forecast freight demand, and minimize transportation delays. Warehouse automation technologies including robotics, autonomous forklifts, and automated sorting systems are improving inventory accuracy and operational throughput.

Digital freight marketplaces are also gaining traction by enabling real-time freight matching, dynamic pricing models, and improved fleet utilization. Logistics providers are increasingly offering customers end-to-end shipment visibility through mobile applications and cloud-based dashboards. This digital transformation trend is expected to remain one of the strongest long-term structural changes within the global shipping and logistics market.

Sustainable and Green Logistics Adoption

Sustainability initiatives are becoming central to logistics investment strategies globally. Governments and multinational corporations are implementing aggressive carbon-reduction goals, encouraging logistics providers to adopt low-emission transportation systems and environmentally sustainable supply chain operations. Shipping companies are increasingly investing in LNG-powered vessels, biofuel technologies, electric commercial vehicles, and hydrogen-based transportation solutions.

Green warehousing initiatives involving solar-powered facilities, energy-efficient lighting systems, and carbon-neutral distribution centers are also expanding rapidly. Europe remains at the forefront of green logistics adoption due to strict environmental regulations, while North America and Asia-Pacific are witnessing accelerating investments in sustainable transportation infrastructure. Corporate ESG mandates are further encouraging logistics providers to strengthen sustainability reporting and carbon footprint optimization strategies.

Shipping and Logistics Market Drivers

Expansion of Global Trade and Manufacturing Activity

The continued growth of international trade and manufacturing output remains one of the primary drivers of the shipping and logistics market. Export-oriented manufacturing economies such as China, India, Vietnam, Germany, and Mexico continue increasing demand for multimodal transportation services, container shipping, freight forwarding, and contract logistics solutions. Rising industrial production across automotive, electronics, chemicals, and machinery sectors is further strengthening freight transportation requirements globally.

Large-scale infrastructure development initiatives, including dedicated freight corridors, smart ports, industrial clusters, and cross-border trade connectivity projects, are improving transportation efficiency and supporting long-term logistics market growth. Governments worldwide are increasingly prioritizing supply chain modernization to strengthen economic competitiveness and trade resilience.

Growth of E-Commerce and Last-Mile Delivery Services

The rapid expansion of e-commerce and direct-to-consumer retail models is significantly transforming logistics operations worldwide. Consumers increasingly expect faster deliveries, real-time shipment tracking, flexible return policies, and seamless order fulfillment services. This has accelerated investments in urban fulfillment centers, automated warehouses, same-day delivery networks, and last-mile transportation systems.

Major e-commerce companies are expanding logistics infrastructure aggressively to improve delivery speed and customer satisfaction. Cross-border online shopping is also increasing international parcel delivery volumes substantially. Emerging economies including India, Indonesia, Brazil, and Southeast Asian nations are witnessing particularly strong e-commerce logistics demand due to rising digital consumer adoption.

Global Market Restraints

Fuel Price Volatility and Freight Rate Fluctuations

The shipping and logistics industry remains highly vulnerable to fuel price volatility and fluctuating freight rates. Rising oil prices significantly increase transportation costs across road freight, air cargo, maritime shipping, and warehousing operations. Ocean freight markets are particularly susceptible to cyclical pricing instability caused by container shortages, geopolitical disruptions, and supply-demand imbalances in global shipping capacity.

Freight pricing unpredictability creates margin pressure for logistics providers and complicates long-term supply chain planning for businesses. Economic slowdowns and global trade uncertainties can also negatively impact freight demand and shipping profitability.

Infrastructure Bottlenecks and Labor Shortages

Infrastructure limitations and labor shortages continue creating operational challenges across the global shipping and logistics market. Port congestion, inadequate transportation networks, customs delays, and limited warehousing capacity in several developing economies negatively affect delivery efficiency and increase logistics costs.

The shortage of skilled truck drivers, warehouse operators, and logistics professionals is also becoming a major concern globally. Aging workforce demographics and rising labor costs are pressuring logistics companies to accelerate automation investments. However, infrastructure modernization often requires substantial capital expenditure and long implementation timelines, particularly in emerging markets.

Shipping and Logistics Industry Key Opportunities

Expansion of Cold-Chain and Pharmaceutical Logistics

The growing pharmaceutical, biologics, and food export industries are creating significant opportunities for temperature-controlled logistics providers. Increasing demand for vaccine distribution, specialty medicines, biologics transportation, and perishable food exports is driving investments in refrigerated transportation systems, cold-storage warehouses, and temperature-monitoring technologies.

Healthcare supply chains increasingly require precise temperature compliance and real-time monitoring capabilities, creating premium revenue opportunities for specialized logistics providers. Emerging markets are also rapidly investing in cold-chain infrastructure to reduce food wastage and support pharmaceutical manufacturing growth.

Nearshoring and Supply Chain Diversification

Global manufacturers are increasingly diversifying supply chains away from single-country sourcing models to improve resilience and reduce geopolitical risks. This trend is driving the development of new trade corridors, regional warehousing hubs, and integrated transportation networks across Southeast Asia, Mexico, Eastern Europe, and India.

Nearshoring strategies are particularly benefiting logistics operators capable of managing complex multimodal supply chains and cross-border transportation systems. Mexico is emerging as a major logistics hub for North American manufacturing supply chains, while India and Vietnam are strengthening their positions within global export ecosystems.

Service Type Insights

Freight transportation continues to dominate the global shipping and logistics market, accounting for nearly 39% of total market revenue in 2025. The leadership of this segment is primarily driven by the rapid expansion of international trade activities, rising industrial production, increasing cross-border commerce, and the growing need for efficient cargo movement across domestic and global supply chains. Road freight remains the leading mode for domestic transportation because of its operational flexibility, extensive road connectivity, and ability to support last-mile delivery requirements across urban, suburban, and rural regions. Increasing investments in highway infrastructure, fleet digitization, and fuel-efficient commercial vehicles are further strengthening road freight operations globally.Warehousing and distribution services are witnessing substantial expansion due to the rapid growth of e-commerce, omnichannel retailing, and increasing demand for inventory optimization across industries. Modern fulfillment centers equipped with robotics, automated guided vehicles, AI-driven inventory management systems, and smart sorting technologies are increasingly becoming central to supply chain operations. Companies are focusing heavily on warehouse automation to improve operational efficiency, reduce delivery timelines, and minimize labor dependency. In addition, courier, express, and parcel (CEP) services are recording strong growth globally due to rising online shopping penetration, increasing cross-border e-commerce transactions, and growing consumer preference for same-day and next-day deliveries.

Transportation Mode Insights

Maritime transportation accounted for approximately 32% of the global shipping and logistics market in 2025, making it the largest transportation mode segment globally. The segment’s dominance is primarily supported by the increasing volume of international trade, growing containerized cargo movement, and the cost advantages associated with large-scale marine transportation. Containerized shipping continues leading global trade logistics because of standardized cargo handling systems, improved operational efficiency, and lower transportation costs for bulk shipments. Governments and private operators worldwide are investing heavily in port modernization projects, deep-water terminals, smart port technologies, and mega-container fleets to improve cargo handling capacity and reduce trade bottlenecks.Rail freight transportation is steadily gaining market importance due to its cost advantages for bulk cargo movement and lower environmental impact compared to conventional road freight. Increasing investments in dedicated freight corridors, intermodal terminals, and transcontinental rail connectivity are supporting segment expansion across both developed and emerging economies. Multimodal transportation systems integrating rail, road, maritime, and air logistics are becoming increasingly popular as businesses seek improved supply chain efficiency, lower operational costs, and faster cargo transit times.

Operation Model Insights

Third-party logistics (3PL) services dominate the operational model landscape, accounting for nearly 46% of total market demand in 2025. The leading position of the segment is driven by the growing preference among businesses to outsource transportation management, warehousing, freight forwarding, inventory control, and order fulfillment activities to specialized logistics providers. Companies across manufacturing, retail, healthcare, and automotive sectors are increasingly relying on 3PL operators to reduce operational complexity, improve scalability, optimize transportation costs, and enhance overall supply chain efficiency.Fourth-party logistics (4PL) solutions are also gaining strong traction among multinational enterprises requiring integrated end-to-end supply chain management capabilities. Lead logistics providers offering centralized supply chain coordination, digital control tower services, real-time analytics, and multimodal transportation integration are increasingly becoming strategic partners for large global manufacturers and retailers. The growing complexity of global supply chains and rising emphasis on supply chain resilience are expected to accelerate adoption of 4PL solutions over the forecast period.

End-Use Industry Insights

Retail and e-commerce remain the largest end-use industries within the global shipping and logistics market, representing approximately 24% of total market demand in 2025. The dominance of the segment is primarily driven by rapid online shopping adoption, increasing smartphone penetration, expansion of omnichannel retail strategies, and rising consumer expectations for faster and more flexible delivery services. Global retailers and e-commerce companies are investing aggressively in fulfillment centers, warehouse automation technologies, urban distribution hubs, and advanced parcel delivery systems to strengthen order fulfillment capabilities and reduce delivery timelines.Healthcare and pharmaceutical logistics are emerging as some of the fastest-growing end-use segments due to increasing biologics transportation, vaccine distribution, medical device shipments, and cold-chain storage requirements. The growing prevalence of temperature-sensitive pharmaceutical products and rising global healthcare expenditure are accelerating investments in specialized cold-chain logistics infrastructure. Food and beverage logistics are also expanding steadily due to increasing international trade in processed foods, frozen products, agricultural commodities, and perishable goods requiring temperature-controlled transportation and storage systems.

Technology Integration Insights

Digitally enabled logistics is emerging as one of the fastest-growing segments within the global shipping and logistics market and is projected to expand at a CAGR of more than 10% during the forecast period. The growth of this segment is being driven by rising demand for real-time shipment visibility, increasing supply chain complexity, and the growing need for operational efficiency and predictive decision-making across logistics networks.Cloud-based transportation management systems are enabling real-time coordination across highly complex global supply chains while improving transparency in shipment monitoring and freight management. Digital freight platforms are helping businesses improve capacity utilization, simplify freight procurement, and optimize carrier selection processes. Automation-driven logistics operations supported by advanced analytics, machine learning, and smart warehousing technologies are expected to become major competitive differentiators across the global logistics industry over the next decade.

| By Service Type | By Transportation Mode | By Operation Model | By Cargo Type | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global shipping and logistics market with approximately 39% market share in 2025. The region’s leadership is primarily driven by strong manufacturing activity, rapid industrialization, growing international trade volumes, and large-scale infrastructure development projects across emerging economies. China remains the largest contributor due to its export-oriented manufacturing ecosystem, advanced port infrastructure, extensive rail and highway connectivity, and dominant role in global trade flows. Continuous investments in smart ports, automated warehouses, and multimodal transportation systems are further strengthening China’s logistics capabilities.Japan and South Korea continue contributing significantly through advanced logistics technologies, strong automotive exports, sophisticated warehousing systems, and highly efficient transportation networks. Southeast Asian economies including Vietnam, Indonesia, and Thailand are witnessing rising logistics investments due to increasing manufacturing diversification, foreign direct investment inflows, expanding export activities, and the relocation of global supply chains into the region.

North America

North America accounted for nearly 26% of global market revenue in 2025, led primarily by the United States. The region benefits from highly developed transportation infrastructure, extensive warehousing capacity, strong consumer spending, and rapid adoption of advanced logistics technologies. The continued growth of e-commerce and omnichannel retailing is driving major investments in fulfillment centers, automated warehouses, autonomous delivery technologies, and last-mile transportation networks.Canada is strengthening logistics infrastructure through rail modernization programs, port expansion projects, and improved cross-border trade connectivity with the United States. Mexico is emerging as a major logistics hub due to nearshoring trends, expanding manufacturing exports, lower production costs, and increasing trade integration across North America. The relocation of supply chains closer to the U.S. market is significantly boosting transportation and warehousing demand throughout the region.

Europe

Europe remains one of the world’s most advanced logistics markets, led by Germany, the United Kingdom, France, and the Netherlands. The region benefits from highly integrated transportation networks, strong industrial output, sophisticated warehousing systems, and extensive international trade connectivity. Germany continues dominating regional logistics demand due to its strong automotive, machinery, and industrial manufacturing sectors, which require highly efficient freight transportation and supply chain coordination.Sustainability regulations are significantly influencing logistics investments across Europe, accelerating the adoption of electric commercial fleets, green warehousing technologies, carbon-neutral transportation systems, and environmentally sustainable supply chain practices. Increasing regulatory pressure to reduce carbon emissions is expected to drive further innovation in green logistics technologies throughout the region.

Latin America

Latin America is witnessing gradual but steady expansion within the shipping and logistics market, led primarily by Brazil and Mexico. Regional growth is being supported by improving transportation infrastructure, expanding industrial activity, rising international trade, and increasing penetration of e-commerce platforms. Brazil continues strengthening agricultural export logistics infrastructure, port operations, and industrial transportation networks to support growing exports of commodities, food products, and manufactured goods.The rapid growth of online retail activity across Latin America is also accelerating investments in urban fulfillment centers, parcel delivery systems, warehouse automation, and last-mile logistics infrastructure. Governments across the region are increasingly focusing on transportation modernization initiatives to improve regional trade efficiency and logistics competitiveness.

Middle East & Africa

The Middle East & Africa region is experiencing accelerated logistics infrastructure development led by the UAE and Saudi Arabia. The region’s growth is being driven by increasing trade diversification efforts, major investments in transportation infrastructure, expanding industrial activities, and rising focus on developing global logistics hubs. The UAE continues strengthening its position as a leading global maritime and re-export hub through large-scale port modernization projects, free trade zone expansion, and advanced multimodal transportation infrastructure.Africa is witnessing growing demand for transportation infrastructure modernization, particularly across mining, agriculture, manufacturing, and industrial supply chains. Increasing urbanization, rising regional trade integration initiatives, and growing investments in port and rail infrastructure are expected to create long-term opportunities for logistics providers across the continent. The continued expansion of cross-border trade corridors and industrial development programs is expected to further strengthen logistics market growth throughout the Middle East and Africa region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Shipping and Logistics Market

- DHL Group

- Kuehne+Nagel

- DSV A/S

- Maersk

- United Parcel Service (UPS)

- DB Schenker

- FedEx Corporation

- Nippon Express Holdings

- C.H. Robinson

- Sinotrans

- XPO Logistics

- Expeditors International

- CMA CGM

- CEVA Logistics

- Yusen Logistics