Shelf Stable Food Market Size

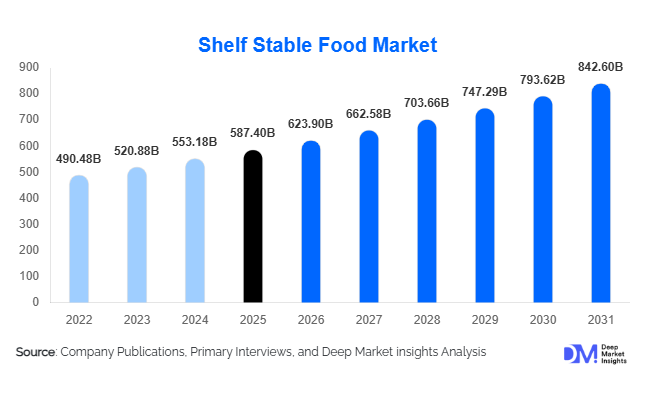

According to Deep Market Insights, the global shelf stable food market size was valued at USD 587.4 billion in 2025 and is projected to grow from USD 623.9 billion in 2026 to reach USD 842.6 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The shelf stable food market growth is driven by rising demand for long-life packaged foods, increasing urbanization, expansion of modern retail infrastructure, and evolving consumer preferences toward convenience-oriented consumption. Shelf stable foods — including canned products, dried foods, ready-to-eat meals, sauces, grains, and packaged snacks — have become essential components of global food security systems and modern supply chains.

Key Market Insights

- Convenience-driven consumption patterns are accelerating adoption of ready-to-eat and easy-to-store food products globally.

- E-commerce grocery expansion is boosting demand for durable food categories with longer shelf life and lower logistics risk.

- Asia-Pacific dominates global consumption due to population scale, urban migration, and rising middle-class purchasing power.

- Private label expansion by retailers is reshaping pricing structures and intensifying competition.

- Food security policies and emergency stockpiling are supporting institutional demand for shelf stable food products.

- Packaging innovation, including retort pouches and aseptic processing, is extending shelf life while improving nutritional retention.

What are the latest trends in the shelf stable food market?

Premiumization and Health-Focused Shelf Stable Foods

Consumers are increasingly shifting toward healthier shelf stable alternatives such as organic canned vegetables, plant-based ready meals, high-protein snacks, and preservative-free packaged foods. Manufacturers are reformulating products with clean-label ingredients, reduced sodium levels, and fortified nutrition profiles. Functional shelf stable foods enriched with vitamins, probiotics, and protein are gaining traction, particularly among urban consumers seeking convenience without compromising health. Premium shelf stable categories now command higher margins, especially in developed markets where nutritional transparency influences purchasing decisions.

Technology-Driven Packaging Innovation

Advancements in aseptic processing, vacuum sealing, modified atmosphere packaging, and retort pouch technologies are transforming the shelf stable food landscape. These technologies extend product longevity while maintaining flavor and texture quality. Lightweight flexible packaging is reducing transportation costs and improving sustainability metrics. Smart packaging solutions incorporating freshness indicators and traceability QR codes are increasingly adopted by global manufacturers to enhance consumer confidence and regulatory compliance.

What are the key drivers in the shelf stable food market?

Urbanization and Changing Lifestyles

Rapid urbanization and dual-income households are increasing reliance on convenient meal solutions. Consumers increasingly prefer foods requiring minimal preparation, driving demand for packaged soups, instant meals, canned proteins, and ready sauces. Time-constrained lifestyles across Asia-Pacific and North America continue to accelerate consumption frequency of shelf stable products.

Expansion of Modern Retail and E-Commerce

Supermarkets, hypermarkets, and online grocery platforms have significantly expanded shelf stable food accessibility. These products are ideal for omnichannel distribution due to reduced spoilage risks and longer inventory cycles. Online grocery retailers prioritize shelf stable foods because they simplify warehousing and last-mile delivery logistics.

Food Security and Emergency Preparedness

Governments and institutions increasingly maintain strategic food reserves, boosting bulk demand for shelf stable staples such as grains, canned goods, and powdered foods. Climate disruptions and geopolitical uncertainties have strengthened national food storage initiatives, supporting consistent long-term demand.

What are the restraints for the global market?

Perception of Reduced Freshness

Despite technological advancements, some consumers perceive shelf stable foods as less nutritious compared to fresh alternatives. This perception slows adoption in premium health-conscious segments, particularly in Western Europe.

Raw Material Price Volatility

Fluctuations in agricultural commodity prices, packaging materials, and energy costs impact manufacturer margins. Price instability in grains, edible oils, and metals used in cans creates cost pressures across supply chains.

What are the key opportunities in the shelf stable food industry?

Emerging Market Penetration

Rapid growth in Southeast Asia, Africa, and Latin America presents major opportunities for manufacturers. Rising disposable income and expanding retail penetration are increasing packaged food consumption. Localized product formulations tailored to regional tastes allow new entrants to capture underserved consumer segments.

Institutional and Government Procurement Programs

Public food distribution programs, disaster relief reserves, and military provisioning systems represent stable demand channels. Governments worldwide are increasing investments in food resilience strategies, creating long-term procurement opportunities for manufacturers specializing in shelf stable products.

Plant-Based and Sustainable Product Development

Plant-based shelf stable meals, legumes, and protein-rich snack categories are expanding rapidly. Sustainability-conscious consumers favor products with lower carbon footprints and recyclable packaging, encouraging innovation in eco-friendly processing and packaging solutions.

Product Type Insights

Canned food products continue to dominate the global shelf stable food market, accounting for approximately 24.8% of total market revenue in 2025. The leadership of canned foods is primarily attributed to their extended shelf life, strong food safety assurance, affordability, and universal consumer familiarity across both developed and emerging economies. Technological improvements in thermal processing, preservation techniques, and nutrient retention have enhanced product quality, enabling manufacturers to expand offerings beyond traditional vegetables and meats into premium soups, plant-based meals, and ready culinary solutions. The leading segment driver remains the growing consumer preference for long-lasting food products that support pantry stocking behavior, emergency preparedness, and reduced food waste. Increasing climate uncertainties and supply chain disruptions have further strengthened consumer reliance on canned food formats as reliable food reserves.Ready-to-eat meals represent one of the most dynamic product categories, supported by accelerating urbanization, dual-income households, and time-constrained lifestyles. Demand growth is particularly strong in major metropolitan regions across Asia-Pacific and North America, where convenience-oriented consumption patterns continue to reshape food purchasing decisions. Advances in retort packaging and flavor preservation technologies allow ready meals to deliver restaurant-quality experiences without refrigeration, expanding adoption among younger demographics and working professionals.Dry staples such as rice, pasta, lentils, and grains remain foundational consumption categories within the shelf stable ecosystem, supported by government food security initiatives and humanitarian supply programs. These products maintain consistent demand due to affordability, cultural dietary integration, and long storage capabilities. Population growth in developing regions and strategic national food reserve policies further reinforce stable long-term consumption trends.Meanwhile, shelf stable dairy alternatives and powdered beverages are gaining substantial traction as plant-based diets, lactose intolerance awareness, and functional nutrition trends expand globally. Manufacturers are investing in fortified formulations enriched with protein, vitamins, and probiotics, positioning these products at the intersection of convenience and health-focused consumption. The expansion of vegan and flexitarian lifestyles continues to drive innovation across this emerging segment.

Packaging Type Insights

Metal cans dominate packaging formats, capturing approximately 32.6% market share in 2025, supported by superior durability, airtight sealing capabilities, and long-term preservation efficiency. The leading segment driver for metal packaging is its ability to maintain food integrity without refrigeration while offering strong recyclability credentials aligned with global sustainability goals. Improvements in lightweight can manufacturing and BPA-free linings have strengthened consumer trust and regulatory compliance, ensuring continued adoption across multiple food categories.Flexible pouches represent the fastest-growing packaging format, benefiting from reduced material usage, lower transportation costs, and enhanced consumer convenience. Their lightweight structure improves supply chain efficiency and reduces carbon emissions during logistics operations. Additionally, resealable and microwave-compatible pouch innovations are expanding applicability across ready meals, sauces, and snack-based shelf stable foods, particularly among urban consumers seeking portability.Aseptic cartons are gaining momentum in premium product categories including soups, dairy alternatives, broths, and functional beverages. These cartons enable sterile packaging without preservatives, supporting clean-label positioning while extending shelf life. Increasing environmental awareness and brand differentiation strategies are encouraging manufacturers to adopt aseptic packaging as part of premiumization and sustainability initiatives.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, contributing nearly 41.3% of global sales in 2025. The leading driver for this segment is the ability of large-format retail stores to provide extensive product variety, bulk purchasing options, and strong private-label penetration. Established retail infrastructure in developed economies ensures consistent product availability, while emerging markets continue expanding organized retail networks, strengthening consumer accessibility to shelf stable food products.Online retail is the fastest-growing distribution channel, fueled by rapid digital adoption, improved last-mile logistics, and changing consumer shopping behaviors. E-commerce platforms enable price comparison, subscription-based purchasing, and automated replenishment models that align with routine pantry stocking habits. The growth of digital grocery ecosystems accelerated during pandemic-driven behavioral shifts and continues to expand through mobile commerce adoption and personalized marketing strategies.Direct-to-consumer subscription models are emerging as an innovative distribution pathway, particularly for meal kits and curated food bundles incorporating shelf stable components. These models allow brands to build recurring revenue streams while leveraging consumer data analytics to tailor offerings based on dietary preferences and consumption frequency.

End-Use Insights

Household consumption dominates market demand, accounting for approximately 68% market share in 2025. The primary driver behind this leadership is the integration of shelf stable foods into daily meal preparation and long-term pantry management practices. Rising food price volatility has encouraged consumers to purchase products with longer storage life, minimizing spoilage and improving household budget efficiency. Increased awareness of emergency preparedness and disaster resilience also contributes to sustained household stocking patterns across both developed and emerging markets.Foodservice and institutional buyers, including airlines, military organizations, hospitals, and educational institutions, are experiencing accelerated adoption of shelf stable foods due to operational efficiency advantages. These products reduce refrigeration dependency, simplify inventory management, and minimize food waste, making them ideal for large-scale catering and remote operations. Growth in global travel, healthcare infrastructure expansion, and defense logistics modernization continues to support institutional demand growth.

| By Product Type | By Packaging Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 24.5% of the global market share in 2025, led primarily by the United States, where convenience-driven consumption patterns strongly influence purchasing behavior. Regional growth is supported by high penetration of organized retail chains, advanced cold-chain alternatives through shelf stable innovation, and a deeply rooted culture of emergency food preparedness. Increasing consumer demand for premium, organic, and clean-label shelf stable foods is encouraging manufacturers to expand healthier product portfolios. Canada is witnessing growing adoption of organic and sustainably packaged shelf stable products, supported by environmentally conscious consumers and regulatory emphasis on recyclable materials. Continued innovation in ready meals and functional packaged foods remains a key regional growth driver.

Europe

Europe represents approximately 21.8% of global market share, with Germany, the United Kingdom, France, and Italy serving as major consumption hubs. Regional growth is driven by strong private-label expansion, sustainability-focused packaging innovation, and regulatory initiatives promoting food waste reduction. European consumers increasingly favor responsibly sourced and environmentally friendly shelf stable products, encouraging brands to adopt recyclable materials and carbon-reduction strategies. Eastern Europe is emerging as a high-growth area due to rising disposable incomes, modernization of retail infrastructure, and increasing exposure to Western consumption patterns, which collectively accelerate packaged food adoption.

Asia-Pacific

Asia-Pacific dominates the global market with nearly 34.7% market share in 2025, supported by large population bases, rapid urbanization, and evolving dietary habits. China and India drive large-scale consumption through expanding middle-class populations and growing demand for affordable, convenient food solutions. Urban migration and busy lifestyles are accelerating adoption of ready-to-eat and shelf stable meal formats. Japan and South Korea demonstrate strong demand for premium packaged soups, functional foods, and high-quality ready meals driven by aging populations and innovation-focused food industries. Southeast Asia represents the fastest-growing sub-region, supported by rising e-commerce penetration, improving retail infrastructure, and increasing participation of multinational food brands.

Middle East & Africa

The Middle East and Africa market is expanding steadily, supported by high food import dependence, government-led food security initiatives, and strategic national food reserve programs. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa are key demand centers due to rapid retail expansion, urban population growth, and tourism-driven foodservice demand. Harsh climatic conditions that limit local agricultural production further increase reliance on shelf stable foods, making long-life packaged products essential for regional supply stability. Investments in logistics infrastructure and modern retail formats continue to enhance product availability across urban and semi-urban markets.

Latin America

Latin America demonstrates consistent market expansion led by Brazil and Mexico, where improving economic conditions and expanding supermarket penetration are increasing packaged food consumption. Regional growth is supported by rising urbanization, changing dietary habits, and greater participation of multinational food manufacturers introducing affordable shelf stable options. Shelf stable staples remain essential household purchases due to price sensitivity and the need for long-lasting food products amid economic fluctuations. Government nutrition programs and retail modernization initiatives further contribute to steady demand growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Shelf Stable Food Market

- Nestlé S.A.

- The Kraft Heinz Company

- General Mills Inc.

- Conagra Brands Inc.

- Campbell Soup Company

- Unilever PLC

- Hormel Foods Corporation

- Tyson Foods Inc.

- Ajinomoto Co., Inc.

- Maruha Nichiro Corporation

- Del Monte Foods Inc.

- JBS S.A.

- Tingyi Holding Corp.

- Associated British Foods PLC

- Grupo Bimbo S.A.B. de C.V.