Shelf Life Testing Market Size

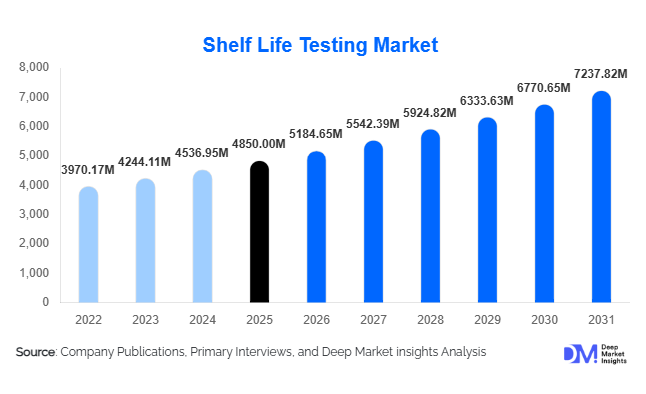

According to Deep Market Insights, the global shelf life testing market size was valued at USD 4,850 million in 2025 and is projected to grow from USD 5,184.65 million in 2026 to reach USD 7,237.82 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The shelf life testing market growth is primarily driven by stringent global food safety regulations, expanding pharmaceutical stability requirements, increasing processed food consumption, and rising export-oriented manufacturing across emerging economies.

Shelf life testing has become a critical compliance and quality assurance function across industries, including food & beverages, pharmaceuticals, cosmetics, nutraceuticals, and medical devices. With global supply chains lengthening and e-commerce penetration increasing, manufacturers require validated data on product stability, microbial safety, packaging interaction, and chemical degradation. Regulatory agencies across North America, Europe, and Asia-Pacific mandate detailed stability documentation, accelerating demand for both in-house and third-party testing laboratories. The growing adoption of accelerated shelf-life testing (ASLT), AI-based predictive modeling, and rapid microbial detection systems is further transforming operational efficiency and time-to-market strategies.

Key Market Insights

- Microbiological testing dominates the market, accounting for nearly 32% of global revenue in 2025 due to mandatory pathogen detection and contamination prevention standards.

- Third-party contract testing services lead the service model segment, contributing approximately 48% of total market demand as manufacturers increasingly outsource compliance testing.

- Food & beverage applications represent the largest end-use industry, with nearly 38% market share in 2025, driven by processed food growth and export regulations.

- North America holds the largest regional share, accounting for approximately 34% of the global market due to strong FDA compliance frameworks.

- Asia-Pacific is the fastest-growing region, expanding at over 8% CAGR, supported by export-driven pharmaceutical and food manufacturing.

- AI-enabled predictive stability modeling and rapid microbial detection technologies are emerging as competitive differentiators among testing providers.

What are the latest trends in the shelf life testing market?

Adoption of Accelerated and Predictive Shelf-Life Testing

Accelerated shelf-life testing (ASLT) is increasingly being adopted to shorten product development cycles. Manufacturers are using temperature and humidity simulation chambers combined with statistical modeling to predict long-term product stability within shorter timeframes. AI-driven predictive analytics platforms are enhancing degradation modeling accuracy for pharmaceuticals, plant-based foods, and preservative-free cosmetics. This trend is particularly valuable in high-innovation sectors where rapid product launches are critical. Predictive tools reduce time-to-market by 20–30%, enabling manufacturers to align with fast-moving consumer trends while maintaining compliance.

Rising Demand for Rapid Microbial Detection Systems

Traditional microbial testing methods requiring 3–7 days are increasingly being replaced by rapid detection systems that deliver results within hours. Advanced PCR-based diagnostics, ATP bioluminescence, and automated colony counters are gaining traction across food processing and pharmaceutical manufacturing facilities. These technologies improve operational efficiency, reduce product hold times, and minimize recall risks. As clean-label and preservative-free products gain popularity, microbial stability assurance has become a strategic priority, further accelerating the adoption of rapid detection platforms.

What are the key drivers in the shelf life testing market?

Stringent Regulatory Compliance Requirements

Regulatory agencies across the United States, the European Union, China, and India require validated shelf-life data before commercialization. Stability studies are mandatory under ICH guidelines for pharmaceuticals, while food safety regulations demand pathogen testing and expiry validation. Rising product recalls globally have intensified compliance scrutiny, compelling manufacturers to invest in comprehensive testing protocols. Increasing harmonization of international food safety standards is further strengthening demand for accredited testing laboratories.

Growth of Processed Foods and Global Supply Chains

Urbanization and the expansion of organized retail have boosted demand for packaged and ready-to-eat foods. Longer distribution channels, cross-border trade, and e-commerce grocery sales require extended shelf-life validation to ensure product integrity throughout storage and transit. Export-driven food manufacturing hubs in Asia and Latin America are particularly fueling demand for third-party shelf life testing services aligned with importing country standards.

What are the restraints for the global market?

High Capital Investment and Operational Costs

Setting up accredited testing laboratories requires significant capital investment in chromatography systems, stability chambers, microbial labs, and skilled personnel. Compliance with ISO/IEC 17025 and GMP standards adds operational complexity. Smaller regional laboratories often face barriers in scaling due to these high infrastructure costs.

Pricing Pressure and Competitive Bidding

Large multinational food and pharmaceutical companies negotiate long-term contracts, leading to pricing pressure among third-party service providers. Competitive tendering and commoditization of basic microbial testing services can limit margin expansion, particularly in mature markets.

What are the key opportunities in the shelf life testing industry?

Export-Oriented Manufacturing Expansion

Emerging economies such as India, Vietnam, Brazil, and Mexico are expanding food and pharmaceutical exports. International buyers require validated shelf-life documentation compliant with importing country standards. Establishing accredited labs near export clusters offers recurring revenue opportunities for testing providers.

Biologics and Clean-Label Product Growth

The expansion of biologics, probiotics, plant-based foods, and preservative-free cosmetics is creating demand for advanced stability and microbial challenge testing. These products exhibit complex degradation profiles, requiring specialized analytical capabilities and environmental simulation chambers, offering high-value growth avenues for specialized laboratories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4850 Million |

| Market Size in 2026 | USD 5184.65 Million |

| Market Size in 2031 | USD 7237.82 Million |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Test Type Insights

Microbiological testing remains the leading test type, accounting for approximately 32% of the global shelf life testing market in 2025. The dominance of this segment is primarily driven by mandatory pathogen detection requirements in food processing and sterility validation in pharmaceutical manufacturing. Increasing global food recalls linked to contamination by Salmonella, Listeria, and E. coli have intensified regulatory scrutiny, making routine microbial stability testing non-negotiable for manufacturers. The shift toward clean-label and preservative-free formulations further strengthens demand, as reduced chemical preservatives increase susceptibility to microbial growth, necessitating more frequent and advanced testing protocols.

Chemical and nutritional stability testing holds a significant share, supported by oxidation studies, rancidity assessment in edible oils, preservative efficacy validation, and vitamin degradation analysis in fortified foods and nutraceuticals. Accelerated shelf-life testing (ASLT) is one of the fastest-growing sub-segments as manufacturers seek shorter product development cycles and faster commercialization timelines. Environmental simulation chambers combined with predictive modeling allow companies to estimate long-term stability in compressed timeframes. Meanwhile, physical and packaging integrity testing is gaining traction due to sustainability-driven material changes, including biodegradable and recyclable packaging, which require rigorous compatibility and moisture migration studies to maintain product stability.

Service Model Insights

Third-party contract testing services dominate the market, contributing nearly 48% of global revenue in 2025. The leading position of this segment is driven by manufacturers’ preference for asset-light operational models. Establishing accredited laboratories requires high capital expenditure in chromatography systems, stability chambers, microbial labs, and compliance infrastructure. Outsourcing enables food and pharmaceutical companies to reduce upfront investments while ensuring compliance with international standards such as ISO/IEC 17025 and GMP guidelines.

In-house laboratory testing remains prevalent among large multinational pharmaceutical and food corporations that require continuous batch validation and proprietary formulation testing. However, outsourcing is growing faster due to scalability advantages and access to advanced technologies. Rapid test kits and on-site solutions are expanding within mid-sized and regional processing facilities seeking operational efficiency and shorter product release cycles. The integration of digital data management platforms within third-party laboratories further enhances traceability and regulatory reporting, reinforcing the dominance of outsourced service models.

End-Use Industry Insights

The food & beverage industry leads the shelf life testing market with approximately 38% share in 2025, representing over USD 1,840 million in value. The segment’s leadership is driven by rising global consumption of processed and packaged foods, expansion of organized retail, and growing cross-border trade. Export-oriented manufacturers must comply with importing country regulations, necessitating validated microbial, chemical, and stability testing documentation.

The pharmaceutical and biologics segment is the fastest-growing end-use industry, expanding at over 7.5% CAGR. Increasing R&D spending, expansion of generic drug manufacturing in Asia, and stringent ICH stability guidelines are accelerating demand. Biologics and biosimilars, which are highly sensitive to temperature and environmental conditions, require extensive real-time and accelerated stability studies. Nutraceuticals, dietary supplements, and cosmetics are emerging as high-growth categories due to clean-label trends, functional health awareness, and global demand for natural formulations requiring validated shelf-life documentation.

Technology Insights

Chromatography-based techniques, including HPLC and GC systems, account for nearly 29% of the total technology share, reflecting their critical role in chemical degradation analysis, preservative validation, and impurity profiling. These techniques are indispensable in pharmaceutical stability studies and high-value food applications such as fortified products and edible oils. Rapid microbial detection technologies are witnessing the highest growth rate, supported by automation, PCR-based diagnostics, ATP bioluminescence, and digital integration. These systems significantly reduce result turnaround time from days to hours, minimizing product hold times and recall risks. Stability chambers equipped with IoT-enabled environmental monitoring systems are also gaining traction, enabling real-time data capture and predictive analytics integration for improved efficiency.

Explore more data points, trends and opportunities Download Free Sample Report

Shelf Life Testing Market Segmentations

By Test Type

- Microbiological Testing

- Chemical & Nutritional Stability Testing

- Physical & Packaging Integrity Testing

- Accelerated Shelf-Life Testing (ASLT)

- Preservative Efficacy & Challenge Testing

By Service Model

- Third-Party Contract Testing Services

- In-House Laboratory Testing

- Rapid Test Kits & On-Site Testing Solutions

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Biologics

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Pet Food & Animal Nutrition

- Medical Devices

By Technology

- Chromatography (HPLC, GC)

- Spectroscopy & Molecular Diagnostics

- Environmental & Stability Chambers

- Rapid Microbial Detection Systems

- AI-Based Predictive Shelf-Life Modeling

Regional Insights

North America

North America holds approximately 34% of the global shelf life testing market in 2025, making it the largest regional contributor. The United States drives the majority of regional demand due to stringent regulatory oversight from federal food and pharmaceutical authorities, advanced pharmaceutical manufacturing capabilities, and a highly developed packaged food sector. The region’s strong culture of product liability management and recall prevention further accelerates testing volumes. Canada contributes steadily through processed food exports and increasing compliance enforcement. Growth in this region is supported by rising adoption of rapid microbial detection technologies and increased R&D spending in biologics.

Europe

Europe accounts for approximately 28% of global market share, led by Germany, France, the United Kingdom, and Italy. The region benefits from harmonized regulatory standards, strict food safety frameworks, and strong pharmaceutical production capabilities. Demand is driven by export-focused food manufacturers and the region’s growing nutraceutical and clean-label cosmetic sectors. Sustainability-driven packaging transitions across Europe are further increasing demand for packaging integrity and compatibility testing. Stable industrial infrastructure and advanced analytical capabilities sustain consistent regional growth.

Asia-Pacific

Asia-Pacific represents nearly 24% of global revenue and is the fastest-growing region, expanding at over 8% CAGR. China and India are primary growth engines due to export-oriented pharmaceutical production, generic drug manufacturing, and the rapid expansion of processed food industries. Increasing government initiatives to strengthen domestic manufacturing and improve food safety standards are accelerating laboratory investments. Japan and South Korea maintain high-quality standards and strong demand for technologically advanced stability testing solutions. Rising middle-class consumption, e-commerce grocery penetration, and cross-border exports are key drivers supporting regional expansion.

Latin America

Latin America accounts for approximately 8% of the global market share, led by Brazil and Mexico. The region’s growth is primarily driven by meat exports, processed food production, and increasing regulatory alignment with North American and European standards. Export validation requirements and rising foreign investments in food processing facilities are supporting demand for microbial and stability testing services. Improving food safety infrastructure across the region is expected to sustain moderate growth.

Middle East & Africa

The Middle East & Africa region contributes roughly 6% of global revenue. Growth in GCC countries is driven by stringent food import regulations, as a significant portion of packaged food is imported and requires validated shelf-life certification. In Africa, South Africa leads demand due to expanding pharmaceutical production and regional food processing activities. Government initiatives to strengthen food safety compliance frameworks and increase domestic pharmaceutical manufacturing are gradually boosting testing infrastructure investments across the region.

Key Players in the Shelf Life Testing Market

- Eurofins Scientific

- SGS SA

- Bureau Veritas

- Intertek Group plc

- ALS Limited

- Mérieux NutriSciences

- TÜV SÜD

- Thermo Fisher Scientific

- Agilent Technologies

- Charles River Laboratories

- WuXi AppTec

- NSF International

- Microbac Laboratories

- AsureQuality

- Campden BRI