Semi-Precious Jewelry Market Size

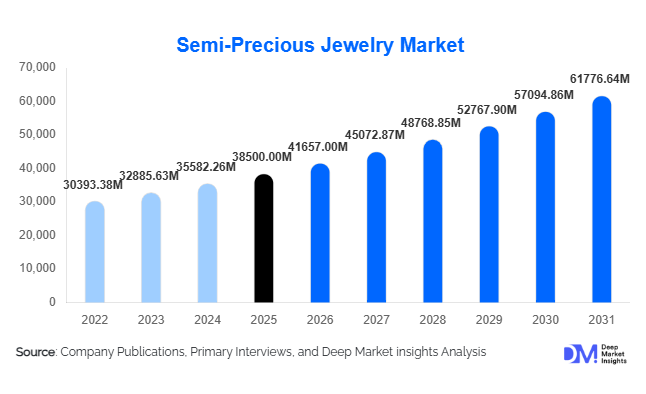

According to Deep Market Insights, the global semi-precious jewelry market size was valued at USD 38,500 million in 2025 and is projected to grow from USD 41,657.00 million in 2026 to reach USD 61,776.64 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The semi-precious jewelry market growth is primarily driven by rising demand for affordable luxury, increasing fashion consciousness among younger consumers, and the rapid expansion of digital retail platforms enabling global accessibility.

Key Market Insights

- Affordable luxury positioning is driving mass adoption, as consumers seek stylish yet cost-effective alternatives to precious gemstone jewelry.

- Online retail channels are rapidly expanding, contributing nearly 38% of total sales through D2C platforms and e-commerce marketplaces.

- North America dominates the global market, supported by strong consumer spending and trend-driven jewelry demand.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable income and cultural affinity toward gemstone jewelry.

- Personalization and customization trends are accelerating, with consumers favoring unique, handcrafted, and symbolic designs.

- Sustainability and ethical sourcing are becoming key purchasing factors, especially in developed markets.

What are the latest trends in the semi-precious jewelry market?

Rise of Personalized and Symbolic Jewelry

Customization is emerging as a dominant trend in the semi-precious jewelry market, with consumers increasingly opting for personalized designs such as birthstone jewelry, engraved pendants, and symbolic gemstone combinations. This trend is particularly strong among millennials and Gen Z consumers who prioritize individuality and emotional connection in their purchases. Jewelry brands are leveraging digital design tools and AI-driven customization platforms to offer tailored products at scale. Additionally, symbolic meanings associated with gemstones, such as healing properties and spiritual significance, are enhancing consumer engagement and driving repeat purchases.

Expansion of Digital-First and Direct-to-Consumer Models

The rapid growth of e-commerce and direct-to-consumer (DTC) channels is reshaping the competitive landscape. Online platforms enable brands to reach global audiences, reduce distribution costs, and improve margins. Technologies such as augmented reality (AR) for virtual try-ons and AI-powered recommendation engines are enhancing the online shopping experience. Social media platforms are playing a critical role in product discovery, with influencer marketing significantly impacting consumer preferences. This digital shift is enabling smaller and artisanal brands to compete effectively with established players.

What are the key drivers in the semi-precious jewelry market?

Growing Demand for Affordable Luxury

The increasing preference for affordable luxury is a major driver of market growth. Semi-precious jewelry offers an attractive balance between price and aesthetics, making it accessible to a broader consumer base. This trend is particularly evident in emerging markets where rising middle-class populations are seeking entry-level luxury products. The ability to frequently update collections at lower costs also supports higher purchase frequency among consumers.

Influence of Fashion Trends and Social Media

Fashion trends and social media platforms are significantly influencing consumer behavior. Influencers and celebrities are promoting semi-precious jewelry as a key fashion accessory, driving demand for statement pieces and trend-driven designs. The fast-paced nature of fashion cycles favors semi-precious jewelry due to its lower production costs and design flexibility. Brands are increasingly collaborating with influencers to launch limited-edition collections, further boosting market visibility.

What are the restraints for the global market?

Volatility in Raw Material Supply

The semi-precious jewelry market faces challenges related to the availability and pricing of raw materials. Gemstones are often sourced from specific regions, making supply chains vulnerable to geopolitical issues, mining regulations, and logistical disruptions. Price fluctuations can impact production costs and profit margins, particularly for small and medium-sized manufacturers.

Perception Gap Compared to Precious Jewelry

Despite growing popularity, semi-precious jewelry still faces a perception challenge, with some consumers associating it with lower value compared to precious gemstones. This perception can limit adoption in premium segments. Brands need to focus on quality assurance, branding, and storytelling to elevate the perceived value of semi-precious jewelry and overcome this barrier.

What are the key opportunities in the semi-precious jewelry industry?

Ethical Sourcing and Sustainability Initiatives

Increasing consumer awareness regarding environmental and social issues presents a significant opportunity for market players. Brands adopting ethical sourcing practices, fair-trade gemstones, and recycled materials can differentiate themselves in a competitive market. Transparency in supply chains and the use of blockchain for traceability are emerging as key strategies to build consumer trust and loyalty.

Expansion in Emerging Markets

Emerging economies, particularly in the Asia-Pacific and the Middle East, offer substantial growth opportunities. Rising disposable incomes, urbanization, and increasing fashion awareness are driving demand for semi-precious jewelry. Localized designs and culturally relevant marketing strategies can help companies effectively penetrate these markets. Countries such as India and China are expected to be major growth drivers due to their large consumer base and strong cultural affinity for gemstone jewelry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38500 Million |

| Market Size in 2026 | USD 41657.00 Million |

| Market Size in 2031 | USD 61776.64 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Necklaces and pendants dominate the semi-precious jewelry market, accounting for approximately 28% of the total market share in 2025. The leadership of this segment is primarily driven by its high versatility, strong gifting appeal, and compatibility with personalization trends. Consumers increasingly prefer pendants featuring birthstones, zodiac symbols, and healing crystals, making this category highly adaptable across both daily wear and occasion-based usage. In addition, necklaces offer higher perceived value compared to smaller accessories, supporting stronger price realization for brands. Rings and earrings collectively contribute a significant portion of demand, driven by their everyday usability and cultural importance in gifting and relationships. Meanwhile, bracelets and bangles are witnessing accelerated growth, particularly among Gen Z consumers, supported by the rising trend of stackable, mix-and-match, and customizable jewelry. This category benefits from fast fashion cycles, allowing brands to frequently introduce new designs at relatively low production costs.

Application Insights

Daily wear jewelry represents the largest application segment, contributing around 40% of total demand in 2025. The dominance of this segment is fueled by the increasing preference for lightweight, affordable, and versatile jewelry suitable for everyday use. Consumers are shifting away from heavy, occasion-specific jewelry toward minimalist designs that can be worn across multiple settings, including work and casual environments. Occasion and festive wear continue to hold a substantial share, particularly in culturally rich markets where jewelry plays an integral role in celebrations and ceremonies. Bridal jewelry remains a critical high-value segment, especially in regions such as India and the Middle East, where gemstone jewelry is deeply embedded in wedding traditions and contributes significantly to seasonal demand spikes. Additionally, fashion and statement jewelry are among the fastest-growing sub-segments, driven by social media influence, celebrity endorsements, and rapidly evolving fashion trends, encouraging repeat purchases and shorter product lifecycles.

Distribution Channel Insights

Online retail is the fastest-growing and increasingly dominant distribution channel, accounting for approximately 38% of the global market share in 2025. The growth of this segment is driven by increased smartphone penetration, digital payment adoption, and the rise of direct-to-consumer (DTC) business models. E-commerce platforms and brand-owned websites provide consumers with greater product variety, competitive pricing, and convenience, while also enabling brands to leverage data analytics for targeted marketing. Technologies such as augmented reality (AR)-based virtual try-ons and AI-driven recommendations are further enhancing online shopping experiences. Offline channels, including specialty jewelry stores, department stores, and independent boutiques, continue to play a vital role, particularly for premium purchases where tactile experience and product authenticity are important. The emergence of omnichannel strategies, integrating online discovery with offline experience, is becoming a key competitive differentiator in the market.

Material Insights

Sterling silver is the leading material segment, holding around 35% of the market share in 2025, primarily due to its optimal balance between affordability, durability, and aesthetic appeal. It serves as a preferred base material for a wide range of semi-precious stones, enabling manufacturers to produce high-quality jewelry at accessible price points. The segment’s growth is also supported by increasing consumer preference for hypoallergenic and sustainable materials. Gold-plated and gold-vermeil jewelry are gaining traction as premium alternatives, offering the appearance of fine jewelry at a fraction of the cost, thereby appealing to aspirational consumers. Brass and alloy-based jewelry cater to the economy segment, enabling mass-market penetration through low-cost offerings. Additionally, mixed-material jewelry incorporating elements such as resin, leather, and textiles is emerging as a niche but rapidly growing category, driven by experimental designs and fashion-forward consumer preferences.

Explore more data points, trends and opportunities Download Free Sample Report

Semi-Precious Jewelry Market Segmentations

By Product Type

- Necklaces & Pendants

- Rings

- Earrings

- Bracelets & Bangles

- Brooches & Pins

- Anklets & Toe Rings

By Application

- Daily Wear

- Occasion & Festive Wear

- Bridal Jewelry

- Fashion & Statement Jewelry

By Distribution Channel

- Online Retail

- Specialty Jewelry Stores

- Department Stores

- Independent Boutiques

- Pop-up & Artisan Markets

By Material Type

- Sterling Silver

- Gold-Plated / Gold-Vermeil

- Brass & Alloy-Based

- Platinum-Plated

- Mixed Materials

Regional Insights

North America

North America accounts for approximately 30% of the global market share in 2025, with the United States being the primary contributor. The region’s growth is driven by high disposable income levels, strong consumer inclination toward fashion accessories, and a mature e-commerce ecosystem. Additionally, the increasing demand for sustainable and ethically sourced jewelry is influencing purchasing decisions, prompting brands to adopt transparent sourcing practices. The presence of established global brands, coupled with aggressive digital marketing and influencer collaborations, further supports market expansion. Seasonal gifting occasions such as holidays and anniversaries also play a significant role in driving consistent demand.

Europe

Europe holds around 25% of the global market share, led by key markets including the UK, Germany, France, and Italy. The region’s growth is primarily fueled by strong design heritage, emphasis on craftsmanship, and increasing consumer awareness regarding sustainability. European consumers exhibit a preference for premium, artisanal, and ethically sourced jewelry, driving demand for high-quality semi-precious pieces. Regulatory frameworks promoting responsible sourcing and environmental compliance are also shaping market dynamics. Additionally, the region benefits from a well-established retail infrastructure and a growing trend of minimalist and contemporary jewelry designs.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 10% during the forecast period. China and India are the प्रमुख markets, collectively accounting for a significant share of global demand. Growth in this region is driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and strong cultural affinity toward gemstone jewelry. In India, semi-precious jewelry is widely used in both daily wear and traditional ceremonies, while in China, increasing fashion consciousness and digital retail penetration are key growth drivers. The expansion of online marketplaces and social commerce platforms is further accelerating adoption, particularly among younger consumers. Additionally, local manufacturing capabilities and export-oriented production hubs contribute to the region’s dominance in global supply.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico. The market is driven by rising middle-class incomes, increasing urbanization, and growing awareness of global fashion trends. Consumers in this region are increasingly adopting semi-precious jewelry as an affordable alternative to fine jewelry. The influence of Western fashion and the expansion of retail chains are further supporting market growth. Additionally, the region’s rich natural resources provide access to a variety of semi-precious stones, supporting local manufacturing and export potential.

Middle East & Africa

The Middle East and Africa region demonstrates strong growth potential, particularly in countries such as the UAE and Saudi Arabia. The market is driven by deep-rooted cultural preferences for jewelry, high per capita income in Gulf countries, and the expansion of luxury retail infrastructure. Jewelry plays a central role in social and cultural events, sustaining consistent demand. In Africa, the presence of abundant gemstone reserves positions the region as a key supplier in the global value chain. Increasing tourism and the growth of duty-free retail in the Middle East are further boosting sales. Additionally, government initiatives aimed at promoting local jewelry manufacturing and exports are expected to support long-term market growth.

Key Players in the Semi-Precious Jewelry Market

- Swarovski

- Pandora

- Tiffany & Co.

- Richemont Group

- Chow Tai Fook

- Signet Jewelers

- Malabar Gold & Diamonds

- Titan Company

- Blue Nile

- Mejuri

- David Yurman

- Kendra Scott

- Bulgari

- Cartier

- Harry Winston