Seitan Market Size

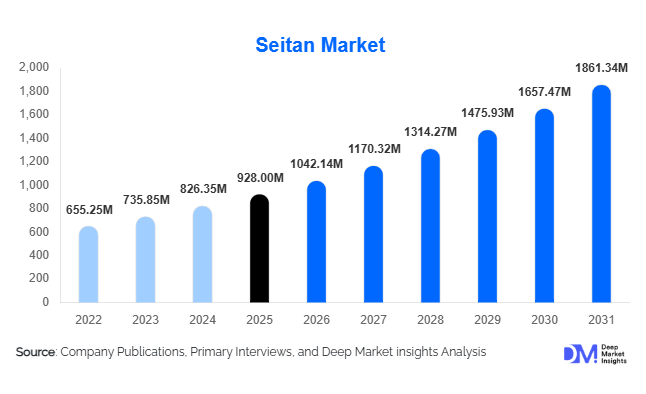

According to Deep Market Insights,the global seitan market size was valued at USD 928 million in 2025 and is projected to grow from USD 1,042.14 million in 2026 to reach USD 1,861.34 million by 2031, expanding at a CAGR of 12.3% during the forecast period (2026–2031). The seitan market growth is primarily driven by increasing consumer adoption of plant-based diets, rising demand for high-protein meat alternatives, and expanding product innovation across retail and foodservice sectors. Growing environmental awareness and the need for sustainable protein sources are accelerating global demand, while advancements in food processing technologies are enabling improved texture, taste, and nutritional performance of seitan-based products.

Key Market Insights

- Seitan is emerging as a cost-efficient plant protein, benefiting from stable wheat supply chains compared with volatile legume protein markets.

- Foodservice adoption is accelerating globally, with restaurants and quick-service chains integrating seitan into plant-based menu offerings.

- North America dominates the global market, supported by mature vegan ecosystems and strong retail penetration.

- Asia-Pacific is the fastest-growing region, driven by urban dietary transitions and familiarity with wheat-based meat analogs.

- Private-label expansion by supermarkets is improving accessibility and reducing price barriers for consumers.

- Technological advancements in extrusion processing are enhancing meat-like texture and supporting premium product positioning.

What are the latest trends in the seitan market?

Clean-Label and Minimally Processed Protein Products

Consumers increasingly prefer plant-based foods with recognizable ingredients and minimal processing. Seitan benefits from a relatively simple ingredient profile compared with highly processed protein isolates, positioning it as a clean-label alternative. Manufacturers are reducing additives, sodium levels, and artificial flavor enhancers while promoting transparency in ingredient sourcing. Organic-certified and non-GMO seitan products are gaining traction, particularly in Europe and North America, where health-conscious consumers prioritize natural formulations. Retailers are expanding shelf space dedicated to minimally processed plant proteins, further reinforcing this trend.

Expansion of Ready-to-Eat and Convenience Formats

The growth of convenience foods has significantly influenced seitan product innovation. Ready-to-cook marinated seitan, frozen meals, and prepared plant-based dishes are increasingly available across supermarkets and online platforms. Busy urban lifestyles and rising demand for quick meal solutions are encouraging manufacturers to develop pre-seasoned and ready-to-eat formats that reduce preparation time. Meal kit providers and plant-based subscription services are also incorporating seitan as a core protein ingredient, broadening consumer exposure and supporting recurring demand.

What are the key drivers in the seitan market?

Rising Flexitarian Consumer Base

The global shift toward flexitarian diets—where consumers reduce meat intake without fully eliminating animal products—is a major growth driver. Seitan’s meat-like texture and high protein content make it a suitable substitute for traditional meat dishes, enabling easy dietary transition. Retailers and restaurants increasingly target flexitarian consumers with familiar meal formats such as burgers, stir-fries, and wraps, driving volume growth.

Sustainability and Environmental Awareness

Growing concern about climate change and resource-intensive livestock production is accelerating adoption of plant-based proteins. Seitan production requires significantly lower water and land resources compared with animal protein, making it attractive for environmentally conscious consumers and institutional buyers. Food companies are integrating seitan products into sustainability strategies to meet carbon reduction goals and ESG commitments.

What are the restraints for the global market?

Gluten Sensitivity and Dietary Restrictions

Seitan is derived from wheat gluten, limiting adoption among consumers with gluten intolerance or celiac disease. This restricts total addressable demand compared with gluten-free plant proteins such as pea or soy alternatives. Manufacturers must diversify portfolios or develop blended formulations to mitigate this limitation.

Nutritional Perception Challenges

Although high in protein, seitan lacks certain essential amino acids unless fortified. Consumer perception that legume-based proteins offer superior nutrition can slow adoption. Educational marketing and product fortification remain essential to overcome this restraint.

What are the key opportunities in the seitan industry?

Foodservice and Quick-Service Restaurant Expansion

Restaurants and quick-service chains are rapidly incorporating plant-based menu items to attract younger and environmentally conscious consumers. Seitan’s texture allows chefs to replicate grilled and roasted meat dishes effectively, making it ideal for foodservice adoption. Long-term supplier contracts with restaurant chains represent significant revenue opportunities for manufacturers.

Emerging Market Protein Demand

Developing economies facing protein supply challenges present strong growth opportunities. Seitan offers an affordable alternative protein that can be locally produced using wheat-based raw materials. Localization of flavors and partnerships with regional food producers can accelerate adoption across Asia, Latin America, and parts of Africa.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 928 Million |

| Market Size in 2026 | USD 1042.14 Million |

| Market Size in 2031 | USD 1861.34 Million |

| CAGR | 12.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The meat analog seitan products segment dominates the global market, accounting for the largest revenue share as consumers increasingly seek plant-based foods that closely replicate the taste, texture, and cooking performance of conventional meat. Rising flexitarian dietary patterns and growing environmental awareness have significantly accelerated demand for chicken-style, beef-style, and shredded meat alternatives made from seitan. The leading segment driver is the increasing consumer preference for high-protein, minimally processed meat substitutes that deliver authentic texture while maintaining clean-label positioning. Flavored and seasoned seitan variants are witnessing accelerated adoption as convenience-oriented consumers prioritize ready-to-cook and pre-marinated options that reduce meal preparation time. Additionally, organic and premium seitan products are gaining traction among health-conscious consumers who value non-GMO ingredients, sustainable sourcing, and certified production standards, particularly across developed economies. Meanwhile, traditional plain seitan continues to maintain consistent demand among home cooks, specialty food manufacturers, and foodservice operators who prefer customizable base ingredients for diverse culinary applications.

Application Insights

Household consumption represents the largest application segment, driven by the rapid increase in home-based plant-forward cooking and growing accessibility of meat alternatives through mainstream retail channels. The leading segment driver is the rising adoption of flexitarian diets, where consumers partially replace animal protein with plant-based alternatives for health, ethical, and environmental reasons. Consumers are increasingly experimenting with seitan in everyday meals due to its versatility, affordability, and high protein density. Foodservice applications are emerging as the fastest-growing category, supported by restaurant menu innovation, expansion of vegan and vegetarian offerings, and consumer demand for inclusive dining options. Quick-service restaurants and casual dining chains are incorporating seitan into sandwiches, wraps, and global cuisine formats to attract younger demographics. Ready-meal manufacturers are also integrating seitan into frozen and packaged meals to meet demand for convenient plant-based nutrition, while plant-based meat producers utilize seitan as a functional ingredient blended with pea, soy, or other proteins to enhance texture, improve mouthfeel, and optimize production costs.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global distribution channels, accounting for the largest market share due to strong shelf visibility, expanding private-label portfolios, and increasing allocation of retail space to plant-based food categories. The leading segment driver is the mainstream commercialization of plant-based diets, which has enabled mass retailers to introduce competitively priced seitan products accessible to a broad consumer base. Retail chains are actively promoting plant-based sections, enhancing product discoverability and encouraging trial purchases. Online retail channels are expanding rapidly as digital grocery adoption increases and direct-to-consumer brands leverage e-commerce platforms to reach niche consumer groups. Subscription meal kits and specialty vegan marketplaces further support online growth by offering curated plant-based selections. Specialty health food stores continue to play an important role in premium and organic product distribution, serving highly health-conscious consumers seeking certified and artisanal offerings. Additionally, foodservice distributors are gaining importance as restaurant demand increases, ensuring consistent supply chains for commercial kitchens and institutional buyers.

End-Use Insights

Household consumers represent the largest end-use segment, contributing approximately 36% of total market demand in 2025, supported by increasing consumer awareness of plant-based nutrition and rising interest in sustainable food consumption. The leading segment driver is the growing shift toward healthier lifestyles combined with rising concerns about animal welfare and carbon footprint reduction. Consumers are increasingly integrating seitan into weekly meal routines due to its affordability compared to many alternative proteins. Restaurants and foodservice operators represent the fastest-growing end-use category as plant-based menu expansion becomes a competitive differentiator across quick-service, fast-casual, and full-service dining formats. Institutional catering, including universities, hospitals, corporate cafeterias, and government facilities, is emerging as a significant demand channel driven by sustainability commitments, nutrition-focused procurement policies, and dietary diversification programs aimed at reducing reliance on animal-based proteins.

Explore more data points, trends and opportunities Download Free Sample Report

Seitan Market Segmentations

By Product Type

- Plain/Traditional Seitan

- Flavored & Seasoned Seitan

- Ready-to-Cook Seitan Products

- Ready-to-Eat & Frozen Seitan Meals

- Organic & Clean-Label Seitan

By Application

- Meat Alternative Products

- Ready Meals & Processed Foods

- Foodservice & Restaurant Applications

- Ingredient Use in Plant-Based Formulations

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail & Direct-to-Consumer

- Specialty Health Food Stores

- Foodservice Distributors

- Convenience Stores

By End Use

- Household Consumption

- Restaurants & Quick-Service Chains

- Institutional Catering (Hospitals, Universities, Corporate Cafeterias)

- Food Manufacturing Industry

Regional Insights

North America

North America accounts for nearly 34% of the global seitan market share, led by the United States and Canada, where plant-based consumption trends are highly developed. Regional growth is driven by strong vegan and flexitarian consumer bases, advanced retail infrastructure, and widespread awareness of sustainable dietary practices. The expansion of private-label plant-based offerings by major supermarket chains has improved affordability and accessibility, encouraging mainstream adoption. Additionally, foodservice innovation, including plant-based menu launches by restaurant chains and growing investment in alternative protein startups, continues to strengthen regional market expansion. Increasing consumer focus on protein-rich, clean-label foods further supports long-term demand growth across the region.

Europe

Europe holds approximately 31% of global market share, with Germany, the United Kingdom, and the Netherlands serving as major consumption hubs supported by strong environmental policies and progressive food sustainability initiatives. Regional growth is driven by government-backed climate strategies encouraging reduced meat consumption, high consumer acceptance of vegetarian and vegan diets, and well-established organic food markets. The popularity of organic-certified and non-GMO seitan products is particularly strong, reflecting European consumer preference for transparent sourcing and ethical production standards. Additionally, innovation in plant-based culinary culture, expansion of vegan retail sections, and strong food labeling regulations continue to enhance consumer confidence and drive steady demand growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at an estimated CAGR above 15%, supported by both cultural familiarity and modern health trends. Regional growth is driven by longstanding culinary traditions involving wheat-based meat substitutes, particularly in China and Japan, which reduce adoption barriers compared to newer markets. Rapid urbanization, rising disposable incomes, and increasing awareness of lifestyle-related health concerns are encouraging consumers to explore plant-based protein options. Expanding modern retail infrastructure, growth of e-commerce grocery platforms, and increasing investment in plant-based innovation across South Korea and Australia further accelerate market penetration. The expanding middle-class population and demand for functional, protein-rich foods continue to position Asia-Pacific as a key future growth engine.

Latin America

Latin America is experiencing gradual market expansion, led by Brazil and Mexico, where rising plant-based awareness and improving retail availability are supporting adoption. Regional growth is driven by increasing health consciousness, urban dietary shifts, and growing exposure to global food trends through digital media and international restaurant chains. Local manufacturers are beginning to invest in cost-effective plant-based production to serve both domestic markets and export opportunities, particularly toward North America. Economic considerations also support seitan adoption as consumers seek affordable protein alternatives amid fluctuating meat prices.

Middle East & Africa

The Middle East and Africa region represents an emerging market for seitan products, with the United Arab Emirates and Israel acting as early adoption hubs due to strong food innovation ecosystems and reliance on imported food products. Regional growth is driven by increasing investment in food technology, rising expatriate populations familiar with plant-based diets, and expanding premium retail formats offering international vegan brands. Government-led food security initiatives encouraging diversified protein sources, combined with growing consumer interest in health and wellness, are gradually expanding demand. As plant-based awareness increases and distribution networks strengthen, the region is expected to witness steady long-term market development.

Key Players in the Seitan Market

- Upton’s Naturals

- The Tofurky Company

- Sweet Earth Foods

- Wheaty (Topas GmbH)

- Maya Foods

- VBites Foods Ltd

- Field Roast Grain Meat Co.

- Loma Linda Foods

- Veganz Group AG

- Greenforce Future Food AG

- Taifun-Tofu GmbH

- MorningStar Farms

- Plant Power Foods

- WestSoy

- Meatless Farm Co.