Salt Market Size

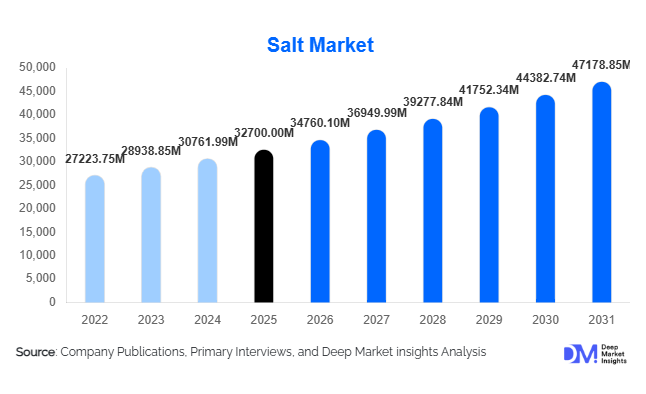

According to Deep Market Insights, the global salt market size was valued at USD 32,700 million in 2025 and is projected to grow from USD 34,760.10 million in 2026 to reach USD 47,178.85 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The salt market growth is primarily driven by increasing industrial demand from the chemical sector, rising consumption of processed foods, and expanding investments in water treatment and desalination infrastructure worldwide.

Key Market Insights

- Chemical processing dominates salt consumption globally, particularly in chlor-alkali production for chlorine and caustic soda.

- Asia-Pacific leads the global market, driven by large-scale industrialization in China and India.

- Water treatment and desalination demand is accelerating, especially in water-scarce regions.

- Industrial-grade salt accounts for the largest share, supported by bulk consumption in manufacturing industries.

- Specialty salts such as low-sodium and mineral-enriched variants are gaining popularity, especially in developed economies.

- Energy costs and logistics play a crucial role in determining pricing and profitability across regions.

What are the latest trends in the salt market?

Rising Demand for Specialty and Fortified Salts

Consumer preferences are shifting toward premium and health-oriented salt products, including low-sodium, iodized, and mineral-enriched variants. Growing awareness regarding lifestyle diseases such as hypertension has encouraged the adoption of healthier alternatives. Products such as sea salt and Himalayan pink salt are gaining traction in retail markets, offering higher margins for manufacturers. These specialty salts are increasingly marketed based on purity, trace mineral content, and origin, appealing to health-conscious and premium consumers.

Expansion of Sustainable Salt Production Technologies

Environmental concerns and regulatory pressures are pushing manufacturers to adopt sustainable extraction and production techniques. Solar evaporation methods and energy-efficient vacuum evaporation technologies are being increasingly utilized to reduce carbon footprint and operational costs. Automation and digital monitoring systems are improving yield efficiency and quality consistency, enabling companies to scale operations while maintaining sustainability standards.

What are the key drivers in the salt market?

Strong Growth in Chemical Industry Demand

The chemical industry remains the primary driver of the global salt market, accounting for over 40% of total consumption. Salt is a critical raw material in chlor-alkali production, which produces chlorine, caustic soda, and soda ash. These chemicals are essential in industries such as plastics, textiles, water treatment, and paper manufacturing. Rapid industrialization in emerging economies continues to fuel this demand.

Increasing Consumption of Processed Foods

Urbanization and changing lifestyles have led to a surge in demand for processed and convenience foods, significantly boosting food-grade salt consumption. Salt plays a vital role in preservation, flavor enhancement, and texture stabilization. Emerging markets are witnessing strong growth in packaged food consumption, supporting steady demand in this segment.

What are the restraints for the global market?

Volatility in Energy and Transportation Costs

Salt production, particularly vacuum evaporation, is energy-intensive. Fluctuating fuel prices and transportation costs directly impact production expenses and overall pricing. These cost pressures can affect profitability, especially for producers operating in energy-dependent regions.

Health Concerns Regarding Sodium Intake

Growing awareness of the health risks associated with excessive sodium consumption has led to regulatory interventions and reduced salt intake recommendations. This trend is particularly evident in developed markets, potentially limiting growth in the food-grade segment.

What are the key opportunities in the salt industry?

Expansion of Water Treatment and Desalination Projects

Rising global water scarcity has led to increased investments in desalination and water treatment infrastructure. Salt plays a crucial role in ion-exchange and water softening processes, making this a high-growth application area. Regions such as the Middle East, India, and Africa are actively investing in desalination facilities, creating sustained demand for high-purity salt.

Growth in Industrial Manufacturing in Emerging Economies

Government initiatives promoting industrial growth, such as domestic manufacturing programs, are creating opportunities for salt producers. Expanding chemical, textile, and construction industries are driving bulk consumption of industrial-grade salt. Emerging economies are also increasing exports, enhancing market potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 32700.00 Million |

| Market Size in 2026 | USD 34760.10 Million |

| Market Size in 2031 | USD 47178.85 Million |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global salt market continues to be structurally anchored by the dominance of solar salt, which accounts for approximately 45% of total market share in 2025. This leadership position is not incidental but rather the result of a strong combination of economic efficiency, scalability, and geographical advantage. Solar salt is produced through the natural evaporation of seawater or brine using sunlight and wind, making it significantly more cost-effective compared to other production methods. Regions with high solar intensity, low rainfall, and vast coastal areas are particularly conducive to large-scale solar salt production, allowing producers to maintain competitive pricing while ensuring consistent supply. This inherent cost advantage has made solar salt the preferred choice across multiple industrial applications, particularly in chemical manufacturing, where bulk volumes are required at relatively low costs.Vacuum evaporated salt, while holding a comparatively smaller share, occupies a critical niche in the market due to its superior purity and controlled production process. This type of salt is produced using advanced evaporation techniques that ensure consistent quality, making it indispensable in sectors such as food processing, pharmaceuticals, and specialty chemicals. The segment’s growth is primarily driven by increasing consumer demand for high-quality food-grade salt and stringent regulatory standards in pharmaceutical manufacturing. As health-conscious consumption patterns rise globally, refined salt products are gaining traction, further supporting the segment’s steady growth.Rock salt, another important segment, maintains its relevance due to its unique application profile. Extracted through mining, rock salt is widely used in de-icing, agriculture, and certain industrial processes. Its demand is highly seasonal in colder regions, particularly in North America and Europe, where winter conditions necessitate large-scale de-icing operations. The leading driver for this segment is the consistent need for road safety and infrastructure maintenance during harsh winters, ensuring a stable demand cycle despite its relatively lower share compared to solar salt.

Application Insights

Chemical processing remains the largest application segment in the global salt market, contributing approximately 40% of total demand. The dominance of this segment is fundamentally tied to the critical role of salt in the production of chlor-alkali chemicals, including chlorine, caustic soda, and soda ash. These chemicals serve as essential building blocks for a wide array of industries, including plastics, textiles, paper, detergents, and water treatment. The leading driver for this segment is the continuous expansion of downstream chemical industries, particularly in developing economies where industrialization is progressing rapidly. As manufacturing output increases, so does the demand for basic chemical inputs, thereby reinforcing the central role of salt in industrial value chains.Food processing represents another significant application area, characterized by stable and consistent demand. Salt is a fundamental ingredient in food preservation, flavor enhancement, and processing, making it indispensable across global food systems. The segment benefits from population growth, urbanization, and changing dietary habits, especially in emerging markets where processed and packaged food consumption is rising. Additionally, the increasing demand for specialty salts, such as low-sodium and fortified variants, is contributing to incremental growth within this segment.Water treatment is emerging as the fastest-growing application segment, driven by a combination of regulatory, environmental, and infrastructural factors. Governments across the globe are implementing stricter water quality standards, necessitating advanced treatment solutions that rely on salt-based processes such as ion exchange and desalination. The leading driver for this segment is the growing scarcity of clean water, particularly in urban and arid regions, which is accelerating investments in water treatment infrastructure. As municipalities and industries prioritize sustainable water management, the demand for salt in water treatment applications is expected to witness robust growth over the forecast period.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape of the global salt market, accounting for nearly 70% of total distribution. This dominance reflects the industrial nature of salt consumption, where large-scale buyers such as chemical manufacturers, water treatment facilities, and food processors rely on long-term supply agreements to ensure operational continuity. The leading driver for this segment is the need for reliable, high-volume supply chains that can support continuous industrial production. Direct contracts enable manufacturers to secure stable pricing, maintain quality consistency, and reduce logistical complexities, making this channel indispensable for bulk transactions.Retail distribution channels, although smaller in comparison, are experiencing steady growth, particularly in the specialty and consumer segments. Supermarkets, hypermarkets, and online platforms are increasingly becoming important channels for the sale of premium salts, including organic, Himalayan, and flavored variants. The expansion of e-commerce has further amplified this trend, allowing consumers to access a wider variety of products with greater convenience. The growth of this segment is primarily driven by changing consumer preferences, increased awareness of health and wellness, and the rising demand for differentiated food products. As branding and product innovation become more prominent, retail channels are expected to play a more significant role in the overall market.

End-Use Industry Insights

Product Type Insights

The global salt market continues to be structurally anchored by the dominance of solar salt, which accounts for approximately 45% of total market share in 2025. This leadership position is not incidental but rather the result of a strong combination of economic efficiency, scalability, and geographical advantage. Solar salt is produced through the natural evaporation of seawater or brine using sunlight and wind, making it significantly more cost-effective compared to other production methods. Regions with high solar intensity, low rainfall, and vast coastal areas are particularly conducive to large-scale solar salt production, allowing producers to maintain competitive pricing while ensuring consistent supply. This inherent cost advantage has made solar salt the preferred choice across multiple industrial applications, particularly in chemical manufacturing, where bulk volumes are required at relatively low costs.Vacuum evaporated salt, while holding a comparatively smaller share, occupies a critical niche in the market due to its superior purity and controlled production process. This type of salt is produced using advanced evaporation techniques that ensure consistent quality, making it indispensable in sectors such as food processing, pharmaceuticals, and specialty chemicals. The segment’s growth is primarily driven by increasing consumer demand for high-quality food-grade salt and stringent regulatory standards in pharmaceutical manufacturing. As health-conscious consumption patterns rise globally, refined salt products are gaining traction, further supporting the segment’s steady growth.Rock salt, another important segment, maintains its relevance due to its unique application profile. Extracted through mining, rock salt is widely used in de-icing, agriculture, and certain industrial processes. Its demand is highly seasonal in colder regions, particularly in North America and Europe, where winter conditions necessitate large-scale de-icing operations. The leading driver for this segment is the consistent need for road safety and infrastructure maintenance during harsh winters, ensuring a stable demand cycle despite its relatively lower share compared to solar salt.

Application Insights

Chemical processing remains the largest application segment in the global salt market, contributing approximately 40% of total demand. The dominance of this segment is fundamentally tied to the critical role of salt in the production of chlor-alkali chemicals, including chlorine, caustic soda, and soda ash. These chemicals serve as essential building blocks for a wide array of industries, including plastics, textiles, paper, detergents, and water treatment. The leading driver for this segment is the continuous expansion of downstream chemical industries, particularly in developing economies where industrialization is progressing rapidly. As manufacturing output increases, so does the demand for basic chemical inputs, thereby reinforcing the central role of salt in industrial value chains.Food processing represents another significant application area, characterized by stable and consistent demand. Salt is a fundamental ingredient in food preservation, flavor enhancement, and processing, making it indispensable across global food systems. The segment benefits from population growth, urbanization, and changing dietary habits, especially in emerging markets where processed and packaged food consumption is rising. Additionally, the increasing demand for specialty salts, such as low-sodium and fortified variants, is contributing to incremental growth within this segment.Water treatment is emerging as the fastest-growing application segment, driven by a combination of regulatory, environmental, and infrastructural factors. Governments across the globe are implementing stricter water quality standards, necessitating advanced treatment solutions that rely on salt-based processes such as ion exchange and desalination. The leading driver for this segment is the growing scarcity of clean water, particularly in urban and arid regions, which is accelerating investments in water treatment infrastructure. As municipalities and industries prioritize sustainable water management, the demand for salt in water treatment applications is expected to witness robust growth over the forecast period.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape of the global salt market, accounting for nearly 70% of total distribution. This dominance reflects the industrial nature of salt consumption, where large-scale buyers such as chemical manufacturers, water treatment facilities, and food processors rely on long-term supply agreements to ensure operational continuity. The leading driver for this segment is the need for reliable, high-volume supply chains that can support continuous industrial production. Direct contracts enable manufacturers to secure stable pricing, maintain quality consistency, and reduce logistical complexities, making this channel indispensable for bulk transactions.Retail distribution channels, although smaller in comparison, are experiencing steady growth, particularly in the specialty and consumer segments. Supermarkets, hypermarkets, and online platforms are increasingly becoming important channels for the sale of premium salts, including organic, Himalayan, and flavored variants. The expansion of e-commerce has further amplified this trend, allowing consumers to access a wider variety of products with greater convenience. The growth of this segment is primarily driven by changing consumer preferences, increased awareness of health and wellness, and the rising demand for differentiated food products. As branding and product innovation become more prominent, retail channels are expected to play a more significant role in the overall market.

End-Use Industry Insights

The chemical industry continues to lead the global salt market, accounting for over 42% of total consumption. This dominance is closely linked to the industry’s reliance on salt as a primary raw material in the production of essential chemicals. The leading driver for this segment is the sustained growth of chemical manufacturing across key regions, particularly in Asia-Pacific, where industrial expansion is occurring at an unprecedented pace. As industries such as plastics, construction, and automotive continue to grow, the demand for chemical intermediates-and consequently salt-remains strong.The water treatment industry is the fastest-growing end-use segment, reflecting the increasing global emphasis on environmental sustainability and resource management. Rising concerns over water scarcity, pollution, and public health are prompting governments and private entities to invest heavily in water treatment infrastructure. The leading driver here is the implementation of stringent environmental regulations, which mandate the treatment of wastewater and the provision of safe drinking water. As urban populations expand and industrial activities intensify, the importance of efficient water treatment systems-and the role of salt within them-continues to grow.The food and beverage industry remains a stable and essential contributor to the market. Salt’s role as a preservative and flavor enhancer ensures consistent demand across all regions. In developing economies, rising disposable incomes and changing consumption patterns are driving increased demand for processed foods, thereby supporting market growth. Additionally, the emergence of health-focused products and reformulated food items is creating new opportunities within this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Salt Market Segmentations

By Product Type

- Rock Salt

- Solar Salt

- Vacuum Evaporated Salt

By Grade

- Food Grade

- Industrial Grade

- Pharmaceutical Grade

- Water Treatment Grade

By Application

- Food Processing

- Chemical Processing

- De-icing

- Water Treatment

- Agriculture

- Pharmaceuticals

- Oil & Gas Drilling

By Distribution Channel

- Direct B2B Sales

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global salt market, accounting for approximately 45% of total market share in 2025. The region’s leadership is underpinned by a combination of large-scale production capabilities, strong industrial demand, and favorable climatic conditions for solar salt production. China stands as the largest consumer, contributing over 25% of global demand, driven by its expansive chemical manufacturing sector. India, on the other hand, plays a dual role as both a major producer and exporter, benefiting from abundant natural resources and cost-efficient production methods.The key drivers of regional growth include rapid industrialization, population expansion, and increasing investments in infrastructure. The rising demand for chemicals, coupled with the growth of water treatment facilities, is significantly boosting salt consumption. Additionally, government initiatives aimed at improving industrial output and ensuring water security are further supporting market expansion. The region’s ability to produce low-cost solar salt at scale provides a competitive advantage, making it a central hub for global supply.

North America

North America holds approximately 20% of the global salt market, with the United States being the primary contributor. The region’s demand profile is characterized by a strong combination of industrial usage and seasonal consumption patterns. Chemical manufacturing remains a key driver, supported by well-established industrial infrastructure and technological advancements.One of the most significant drivers of growth in North America is the consistent demand for de-icing salt during winter months. Harsh weather conditions necessitate large-scale use of rock salt for road safety and infrastructure maintenance. Additionally, ongoing investments in infrastructure repair and urban development are contributing to steady demand. The presence of advanced water treatment systems and regulatory frameworks also supports the use of salt in environmental applications, further strengthening the market.

Europe

Europe accounts for approximately 18% of the global salt market, with major contributions from countries such as Germany, France, and the United Kingdom. The region’s market is driven by a well-established industrial base, particularly in chemical manufacturing, as well as consistent demand for de-icing applications.Key growth drivers in Europe include stringent environmental regulations and a strong focus on sustainability. These factors are encouraging the adoption of advanced water treatment technologies, thereby increasing the demand for salt. Additionally, the region’s commitment to maintaining high standards in food safety and quality is supporting the use of refined salt in food processing. Seasonal weather patterns continue to play a crucial role, with winter conditions driving periodic spikes in demand for de-icing salt.

Middle East & Africa

The Middle East & Africa region is emerging as the fastest-growing market, with a CAGR exceeding 7%. This growth is largely driven by the increasing reliance on desalination and water treatment technologies, particularly in arid regions where freshwater resources are scarce. Countries such as Saudi Arabia and the United Arab Emirates are investing heavily in large-scale infrastructure projects, including desalination plants, which rely on salt-based processes.The primary drivers of regional growth include water scarcity, rapid urbanization, and government-led infrastructure development. As populations grow and industrial activities expand, the need for sustainable water solutions is becoming more critical. This has led to significant investments in advanced treatment systems, thereby boosting the demand for salt. Additionally, the region’s strategic focus on economic diversification is supporting industrial growth, further contributing to market expansion.

Latin America

Latin America holds around 7% of the global salt market, with Brazil and Mexico leading consumption. The region’s market is supported by a combination of industrial growth and expanding food processing sectors. As economies in the region continue to develop, the demand for basic industrial inputs, including salt, is steadily increasing.The key drivers of growth in Latin America include the expansion of the food and beverage industry, increasing urbanization, and rising consumer demand for processed foods. Additionally, industrial development in sectors such as chemicals and agriculture is contributing to higher salt consumption. Favorable climatic conditions in certain areas also support solar salt production, enabling cost-effective supply. As the region continues to industrialize and modernize its infrastructure, the salt market is expected to experience sustained growth.

Key Players in the Salt Market

- Cargill Incorporated

- Compass Minerals International Inc.

- K+S AG

- Tata Chemicals Ltd.

- China National Salt Industry Corporation

- Rio Tinto Group

- Mitsui & Co. Ltd.

- Dominion Salt Ltd.

- Salins Group

- Morton Salt Inc.

- INEOS Group

- Akzo Nobel N.V.

- Delmon Salt Factory

- Exportadora de Sal S.A.

- Zoutman NV