Salt Curing Meat Market Size

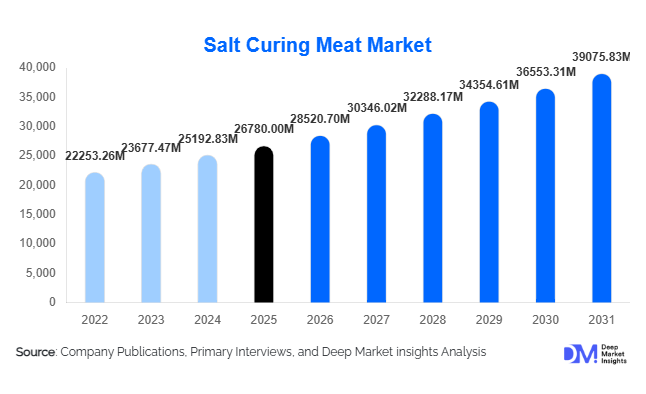

According to Deep Market Insights,the global salt curing meat market size was valued at USD 26,780 million in 2025 and is projected to grow from USD 28,520.70 million in 2026 to reach USD 39,075.83 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The market growth is primarily driven by rising global protein consumption, expanding foodservice demand, premiumization of traditional cured meats, and increasing retail penetration across emerging economies. Growing consumer preference for ready-to-eat and shelf-stable meat products, along with technological advancements in curing and packaging processes, continues to strengthen global demand.

Key Market Insights

- Pork-based cured meat dominates the global market, accounting for over 60% of total revenue due to widespread consumption of bacon, ham, and prosciutto.

- Europe remains the largest regional market, supported by strong demand for traditional and GI-certified cured meat products.

- Asia-Pacific is the fastest-growing region, driven by rising disposable income and expanding organized retail infrastructure.

- Supermarkets and hypermarkets account for the largest distribution share, benefiting from improved cold-chain logistics.

- Clean-label and reduced-sodium innovations are accelerating, responding to regulatory pressure and evolving health preferences.

- The top five companies collectively hold around 42% market share, indicating moderate consolidation.

What are the latest trends in the salt curing meat market?

Premiumization and Geographic Indication (GI) Branding

Premium cured meats such as Prosciutto di Parma, Jamón Ibérico, and Bresaola are witnessing strong global demand. Consumers increasingly associate GI-certified products with authenticity, superior quality, and heritage production methods. These products command price premiums of 25–40% over mass-produced variants. Export growth to Asia-Pacific and the Middle East is expanding revenue streams for European producers. Retailers are dedicating shelf space to artisanal and specialty cured meats, while e-commerce platforms are facilitating cross-border gourmet sales.

Shift Toward Clean-Label and Reduced-Sodium Formulations

Growing health awareness regarding sodium intake and nitrite usage is encouraging manufacturers to innovate. Natural curing agents such as celery extracts and nitrate-free processing are gaining traction. Companies are investing in R&D to maintain flavor and shelf life while reducing additive levels. Regulatory compliance in Europe and North America is also influencing formulation strategies. Clean-label positioning is particularly appealing to urban millennials and premium buyers seeking transparency and traceability in processed meat products.

What are the key drivers in the salt curing meat market?

Rising Global Protein Consumption

Increasing per capita meat consumption, especially in developing economies, is a major driver. Salt-cured meats provide convenient, ready-to-eat protein solutions with extended shelf life, making them suitable for urban consumers and working professionals. Rapid urbanization in Asia-Pacific and Latin America is further stimulating retail and foodservice demand.

Expansion of Organized Retail and Cold-Chain Infrastructure

Supermarkets and hypermarkets account for approximately 45% of distribution share, supported by enhanced refrigeration and logistics networks. Growth in modern retail chains across India, China, and Southeast Asia has improved product accessibility and visibility, boosting overall market penetration.

Foodservice and QSR Growth

Quick service restaurants are a significant demand contributor, particularly for bacon, ham, and specialty cured slices used in sandwiches, pizzas, and breakfast menus. The global QSR segment is expanding steadily, creating consistent bulk procurement demand from meat processors.

What are the restraints for the global market?

Health and Regulatory Concerns

High sodium levels and links to cardiovascular risks have prompted stricter labeling regulations in several countries. Compliance costs and reformulation challenges may constrain smaller producers.

Volatility in Livestock Prices

Fluctuations in pork and beef prices due to feed costs, disease outbreaks, and supply chain disruptions impact production costs and profit margins. African Swine Fever outbreaks have particularly influenced pork supply in recent years.

What are the key opportunities in the salt curing meat industry?

Emerging Market Expansion

Asia-Pacific, particularly China and India, presents strong growth potential. Rising middle-class income and Western dietary influence are increasing demand for premium cured meats. Establishing localized processing facilities can reduce import dependency and logistics costs.

Artisanal and Specialty Product Innovation

Small-batch, region-specific products offer differentiation in competitive markets. Luxury hospitality sectors in the Middle East and Asia are creating new demand channels for high-margin artisanal cured meats.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26780 Million |

| Market Size in 2026 | USD 28520.70 Million |

| Market Size in 2031 | USD 39075.83 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Meat Type Insights

Pork continues to dominate the global cured meat market, accounting for approximately 62% of total market share in 2025. The segment’s leadership is primarily driven by the widespread global consumption of pork-based products such as bacon, ham, prosciutto, and salami. Pork offers favorable fat distribution, curing efficiency, and flavor retention, making it the preferred meat for traditional and industrial curing processes. Strong demand across Europe, North America, and parts of Asia-Pacific, combined with well-established pork processing infrastructure, reinforces the segment’s dominance. Additionally, cost-effectiveness compared to premium beef cuts supports its large-scale commercial adoption.

Beef holds nearly 21% market share, supported by strong consumption in Europe and North America. Products such as bresaola, corned beef, and pastrami are widely consumed in premium and delicatessen categories. The segment benefits from rising demand for high-protein diets and gourmet meat offerings. However, higher raw material costs and longer curing cycles limit broader penetration compared to pork.

Poultry-based cured meats are emerging as a fast-developing segment, driven by increasing health consciousness among consumers seeking leaner and lower-fat protein alternatives. Growing concerns over red meat consumption, along with religious and dietary restrictions in certain regions, are further expanding poultry-based innovation. Although currently smaller in share, this segment is expected to witness accelerated growth due to product diversification and clean-label positioning.

Product Type Insights

Whole cuts account for nearly 34% of total revenue, making them the leading product segment. This dominance is driven by strong consumer preference for premium cured hams and specialty whole-muscle products such as prosciutto and jamón. The segment benefits from premium pricing, geographical indication (GI) certifications, and artisanal branding, particularly in Europe. Rising global demand for authentic, heritage-based meat products continues to support whole-cut segment growth.

Sliced and pre-packaged cured meats are experiencing faster growth compared to whole cuts, primarily driven by convenience trends and ready-to-eat consumption patterns. Urbanization, increasing working populations, and demand for quick meal solutions have strengthened the segment’s penetration in supermarkets and online retail. Technological advancements in modified atmosphere packaging (MAP) are further enhancing shelf life and product safety.Dried and air-cured meats remain highly popular in Europe and are gaining traction in export markets due to premiumization trends and growing consumer interest in traditional European charcuterie. These products command higher margins and are increasingly marketed as gourmet or specialty items in emerging economies.

Distribution Channel Insights

Supermarkets and hypermarkets lead the distribution landscape with approximately 45% market share. Their dominance is supported by extensive product assortments, strong cold-chain infrastructure, and consumer preference for one-stop shopping experiences. Private label expansion and promotional pricing strategies further enhance volume sales through this channel.

Specialty gourmet stores maintain a significant presence, particularly for premium and imported cured meat products. These outlets benefit from knowledgeable staff, curated selections, and demand for artisanal offerings.Online retail is the fastest-growing distribution channel, driven by expanding e-commerce penetration, direct-to-consumer gourmet platforms, and cross-border specialty sales. Subscription-based meat delivery services and improved cold-chain logistics are further accelerating online adoption. Digital marketing and targeted premium product positioning are enhancing consumer reach globally.

End-Use Insights

Household consumption represents approximately 48% of total demand, valued at over USD 13 billion in 2026. The segment’s dominance is driven by widespread incorporation of cured meats into daily breakfast, sandwich, and snack consumption patterns. Growing at-home dining trends and retail product innovation continue to strengthen household demand.

Quick Service Restaurants (QSRs) are expanding at a CAGR exceeding 7%, supported by rising global consumption of sandwiches, burgers, breakfast menus, and pizza toppings. Increasing franchise expansion in emerging markets and evolving fast-food culture significantly contribute to segment growth.Processed food manufacturers are increasingly incorporating cured meats into frozen meals, ready-to-cook kits, snack packs, and protein-rich convenience foods. Industrial demand is further supported by growing demand for high-protein packaged snacks and meal solutions targeted at urban consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Salt Curing Meat Market Segmentations

By Meat Type

- Pork

- Beef

- Poultry

- Lamb & Mutton

- Others (Game & Specialty Meats)

By Product Type

- Whole Cuts (Ham, Prosciutto, Bacon Slabs)

- Sliced & Pre-Packaged Cured Meat

- Dried & Air-Cured Meat

- Salt-Cured & Smoked Meat

- Traditional Regional Specialties

By Curing Method

- Dry Salt Curing

- Wet Brining

- Salt with Nitrite/Nitrate Curing

- Traditional Artisan Curing

- Industrial Controlled Curing

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Gourmet Stores

- Online Retail

- Foodservice Distributors

By End-Use

- Household Consumption

- Hotels & Restaurants

- Quick Service Restaurants (QSRs)

- Processed Food Manufacturers

- Institutional Catering

Regional Insights

Europe

Europe holds approximately 38% market share in 2025, maintaining its position as the largest regional market. Italy, Spain, Germany, and France are key contributors, with Italy and Spain alone accounting for nearly 18% of global revenue due to strong GI-certified exports such as Parma ham and Jamón Ibérico. The region’s leadership is supported by deep-rooted culinary heritage, strong export orientation, and premium product positioning.

Regional growth is driven by high per capita consumption, strong intra-European trade, expanding exports to Asia-Pacific and North America, and increasing global demand for authentic European charcuterie. Additionally, innovation in nitrate-free and organic cured meats aligns with evolving EU food safety regulations and consumer health preferences.

North America

North America accounts for nearly 29% of global demand, with the United States leading bacon and ham consumption. Industrial-scale curing operations, advanced meat processing technologies, and high QSR penetration contribute to stable market expansion.Growth drivers include rising demand for protein-rich diets, expansion of premium deli segments, strong retail infrastructure, and innovation in flavored and smoked cured meats. Increasing Hispanic population influence and cross-cultural culinary adoption further support diversified product demand.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a 7.8% CAGR. China, Japan, South Korea, and Australia are key growth markets. Rising disposable income, westernization of dietary habits, and expanding modern retail infrastructure are driving regional demand.Growth is further supported by increasing imports of European premium cured meats, rapid expansion of QSR chains, and growth in modern cold storage logistics. Urban middle-class consumers are increasingly adopting ready-to-eat and premium meat products, strengthening long-term regional prospects.

Latin America

Latin America represents approximately 9% of global market share, with Brazil and Mexico leading regional demand. The region benefits from strong domestic meat production capabilities and rising urbanization.Growth drivers include expanding QSR presence, increasing disposable income, modernization of retail channels, and growing consumption of processed and packaged food products. Regional export potential, particularly from Brazil, also supports industry expansion.

Middle East & Africa

The Middle East & Africa region holds approximately 6% market share. The UAE and Saudi Arabia are emerging as premium import markets, driven by expanding luxury hospitality sectors and rising expatriate populations.Regional growth is supported by increasing demand for premium imported European products, expansion of modern retail chains, rising tourism, and growing foodservice industries. Additionally, halal-certified cured meat product innovation is opening new avenues for market penetration within the region.

Key Players in the Salt Curing Meat Market

- WH Group Limited

- Hormel Foods Corporation

- JBS S.A.

- Tyson Foods, Inc.

- Danish Crown A/S

- Smithfield Foods

- Campofrío Food Group

- Vion Food Group

- Maple Leaf Foods

- Minerva Foods

- BRF S.A.

- OSI Group

- Seaboard Corporation

- Tönnies Group

- Fratelli Beretta