Salmon Market Size

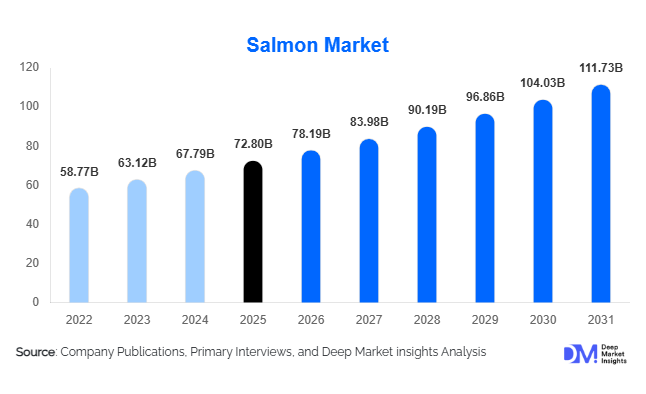

According to Deep Market Insights, the global salmon market size was valued at USD 72.8 billion in 2025 and is projected to grow from USD 78.19 billion in 2026 to reach approximately USD 111.73 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The salmon market growth is supported by rising global consumption of high-protein seafood, increasing health awareness associated with omega-3 fatty acids, and expanding aquaculture production technologies that enable consistent year-round supply. Salmon has transitioned from a premium seafood product into a mainstream protein source across developed and emerging economies due to improved cold-chain logistics, retail availability, and foodservice adoption.

Key Market Insights

- Farmed salmon dominates global supply, accounting for over 75% of total production due to scalability and stable pricing.

- Retail and supermarket channels drive consumption growth as ready-to-cook and processed salmon products gain popularity.

- Asia-Pacific is emerging as the fastest-growing consumption region, supported by rising middle-class income and westernized dietary habits.

- Value-added salmon products, including smoked, frozen, and marinated formats, are expanding profit margins for producers.

- Sustainability certifications and traceability technologies are influencing purchasing decisions globally.

- Aquaculture innovation, including offshore farming and land-based RAS systems, is reshaping supply dynamics.

What are the latest trends in the salmon market?

Shift Toward Value-Added and Convenience Products

Consumers increasingly prefer convenient seafood options that require minimal preparation. Ready-to-eat smoked salmon, portioned fillets, seasoned cuts, and frozen meal kits are gaining traction across supermarkets and online grocery platforms. Retailers are expanding private-label salmon offerings, improving affordability while maintaining quality standards. This transition toward processed and packaged formats enables producers to capture higher margins compared to raw whole fish sales. Demand for premium smoked salmon products in Europe and North America continues to rise, while frozen salmon formats are expanding rapidly in Asia-Pacific due to storage flexibility and growing e-commerce grocery adoption.

Sustainable Aquaculture and Traceability Adoption

Sustainability has become a defining factor in seafood purchasing decisions. Producers are investing heavily in environmentally responsible aquaculture practices such as low-impact feed, antibiotic reduction programs, and digital monitoring systems. Blockchain-enabled traceability solutions allow retailers and consumers to track salmon origin, farming conditions, and environmental certifications. Governments and retailers increasingly mandate eco-labeling standards, pushing producers toward certified operations. Land-based recirculating aquaculture systems (RAS) are gaining attention as they reduce disease risk, minimize environmental impact, and enable farming closer to consumption markets, thereby lowering logistics costs.

What are the key drivers in the salmon market?

Growing Demand for Healthy Protein Alternatives

Rising awareness of cardiovascular health and nutrition is a major driver of salmon consumption globally. Salmon’s high omega-3 fatty acid content positions it as a preferred alternative to red meat and processed proteins. Health-conscious consumers in North America, Europe, and increasingly Asia are incorporating seafood into weekly diets, supporting consistent demand growth. Government dietary guidelines promoting seafood consumption further strengthen this trend.

Expansion of Global Aquaculture Capacity

Advancements in aquaculture technologies have significantly improved production efficiency. Automated feeding systems, AI-based monitoring, and disease management innovations enable higher yield per farming cycle. Countries such as Norway and Chile continue expanding offshore farms, while new entrants invest in land-based aquaculture facilities closer to urban markets. These developments stabilize supply and reduce price volatility, supporting long-term market expansion.

Growth of Organized Retail and Foodservice Chains

The expansion of supermarkets, hypermarkets, and quick-service restaurant chains has increased salmon accessibility worldwide. Sushi chains, premium casual dining, and healthy meal concepts rely heavily on salmon due to consistent quality and versatility. Foodservice adoption is accelerating particularly in emerging markets, where salmon is becoming a staple ingredient in modern cuisine formats.

What are the restraints for the global market?

Environmental and Disease Risks in Aquaculture

Salmon farming faces challenges including sea lice infestations, water pollution concerns, and ecosystem impacts. Disease outbreaks can disrupt supply and increase operational costs. Regulatory scrutiny on farming practices is intensifying, requiring producers to invest heavily in compliance and sustainable operations.

Feed Cost Volatility and Supply Chain Risks

Fish feed prices, influenced by soybean meal, fishmeal, and marine ingredient availability, significantly affect production economics. Rising raw material costs and climate-driven supply disruptions can pressure profit margins and increase consumer prices, potentially slowing demand growth in price-sensitive markets.

What are the key opportunities in the salmon industry?

Land-Based Aquaculture Expansion

Investment in land-based recirculating aquaculture systems presents a major opportunity for industry participants. These facilities enable production near urban consumption centers, reducing transportation emissions and ensuring fresher supply. Governments in North America, Europe, and Asia are supporting such projects through sustainability incentives and infrastructure funding. New entrants can leverage this technology to bypass traditional coastal farming constraints.

Emerging Market Consumption Growth

Rapid urbanization and income growth in countries such as China, India, Vietnam, and Brazil are expanding seafood consumption patterns. Salmon is increasingly perceived as a premium yet aspirational protein. Retail chains and online grocery platforms are introducing smaller packaging formats to improve affordability, creating significant demand potential for exporters.

Product Innovation and Premium Branding

Premium organic salmon, antibiotic-free variants, and specialty cuts are gaining popularity among affluent consumers. Branding strategies emphasizing origin, sustainability certification, and nutritional benefits allow producers to command higher pricing. Value-added innovation including flavored smoked salmon and ready meals creates differentiation opportunities in competitive retail environments.

Product Type Insights

Atlantic salmon continues to dominate the global salmon market, accounting for nearly 64% of total market share in 2025. This leadership position is primarily supported by the species’ strong suitability for intensive aquaculture farming, high feed conversion efficiency, and predictable growth cycles that allow producers to maintain consistent year-round supply. Major producing nations such as Norway and Chile have developed highly optimized farming ecosystems, including advanced hatchery systems, disease management protocols, and automated feeding technologies that enhance productivity while maintaining quality standards. Atlantic salmon’s uniform size, mild flavor profile, and adaptable processing characteristics make it highly compatible with retail packaging, foodservice preparation, and value-added product formats. The species’ widespread global acceptance across cuisines—from Western grilled dishes to Asian sushi applications—further strengthens its commercial dominance. Additionally, growing investments in genetic improvement programs and offshore aquaculture are improving resilience and output stability, reinforcing Atlantic salmon’s long-term leadership within the product segment.

Form Insights

Fresh salmon leads the market with approximately 41% share of global consumption in 2025, reflecting strong consumer preference for minimally processed and nutritionally preserved seafood products. The expansion of refrigerated logistics infrastructure and rapid improvements in global cold-chain networks have significantly enhanced the ability to transport fresh salmon across long distances without compromising quality. Retailers increasingly prioritize fresh fillets due to their premium pricing potential and high consumer appeal linked to perceived freshness and health benefits. Culinary versatility also plays a major role, as fresh salmon can be prepared through multiple cooking methods including grilling, baking, steaming, and raw consumption in sushi and sashimi formats. Growth in urban lifestyles and premium grocery retail formats has strengthened demand for ready-to-cook fresh portions, while advancements in vacuum skin packaging and modified atmosphere packaging technologies extend shelf life and reduce waste. Rising consumer awareness regarding omega-3 fatty acids and clean-label protein sources continues to accelerate adoption of fresh salmon globally.

Source Insights

Farmed salmon represents nearly 76% of total global market share, highlighting the structural transformation of the salmon industry toward controlled aquaculture production. Farmed salmon provides predictable harvest volumes, standardized quality, and cost efficiency compared to wild catch, enabling stable supply chains that meet growing global demand. Technological innovation has played a critical role in this dominance, with advancements such as automated feeding systems, AI-driven biomass monitoring, disease detection technologies, and sustainable feed alternatives improving operational efficiency. Improved farming practices have narrowed the quality perception gap between farmed and wild salmon, while certification programs addressing environmental sustainability and traceability enhance consumer trust. Land-based recirculating aquaculture systems (RAS) are emerging as a complementary production model, particularly in North America and Asia, reducing transportation time and carbon footprint. These developments collectively position farmed salmon as the primary driver of industry scalability and long-term supply security.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 45% of global salmon sales, supported by the rapid expansion of organized retail and growing consumer reliance on modern grocery formats. Large retail chains benefit from integrated cold storage infrastructure, efficient procurement networks, and private-label seafood programs that offer competitive pricing while maintaining quality assurance. The shift from traditional fish markets toward structured retail environments is particularly evident in emerging economies, where urbanization and rising disposable income are reshaping purchasing habits. Supermarkets also enable product diversification through pre-portioned fillets, marinated variants, smoked products, and ready-to-cook meal solutions that enhance consumer convenience. Digital integration within retail, including omnichannel grocery platforms and online ordering systems, further strengthens distribution efficiency and accessibility. Retailers increasingly collaborate directly with aquaculture producers to ensure traceability and sustainability compliance, reinforcing consumer confidence and supporting channel expansion globally.

End-Use Insights

Foodservice applications hold nearly 52% of total market share, driven by expanding global dining-out culture and the growing incorporation of salmon into diverse culinary menus. Salmon’s versatility allows it to function as both a premium entrée and a healthy protein alternative, making it highly attractive for restaurants, hotels, and quick-service dining formats. The rapid proliferation of sushi restaurants and fast-casual dining concepts has significantly increased salmon consumption volumes, particularly in urban markets. Rising consumer preference for nutritious, high-protein meals further strengthens demand within institutional catering, airline food services, and corporate dining facilities. Foodservice operators value salmon for its consistent portioning, cooking adaptability, and ability to command premium menu pricing, reinforcing its dominance across professional culinary environments.

End-Use Analysis

The foodservice industry remains the largest global consumer of salmon, supported by sustained growth in international tourism, hospitality expansion, and evolving consumer dining preferences. The global restaurant industry surpassed USD 4 trillion in revenue in 2025, creating substantial demand for premium seafood ingredients. Sushi chains, premium casual restaurants, and health-focused dining establishments increasingly feature salmon as a core menu component due to its nutritional reputation and wide consumer acceptance. While foodservice dominates volume consumption, retail demand is expanding at a faster pace, driven by rising home cooking trends and increased availability of convenient seafood formats. Ready-to-cook packaged meals, meal kits, and subscription-based healthy diet programs are introducing salmon to new consumer segments. Institutional buyers such as schools, hospitals, and corporate cafeterias are gradually integrating salmon into protein diversification strategies. Strong export demand remains a defining industry characteristic, with Japan, the United States, China, and the European Union serving as major import destinations. Growth in airline catering and premium ready-meal solutions further broadens the application landscape, reinforcing diversified demand channels across global markets.

| By Product Type | By Form | By Source | By Distribution Channel | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 27% of the global salmon market in 2025, led by the United States as the world’s largest single-country importer. Regional growth is driven by rising consumer awareness of healthy protein consumption, strong penetration of organized retail, and increasing demand for convenient premium seafood products. Expansion of e-commerce grocery platforms and meal delivery services has improved accessibility to fresh and frozen salmon products across urban and suburban markets. Canada strengthens the region’s position through established Atlantic aquaculture operations and export-oriented production capabilities. Investments in land-based aquaculture facilities across the U.S. and Canada are reducing reliance on imports while enhancing supply resilience. Additionally, growing adoption of high-protein diets, wellness-focused consumption patterns, and restaurant innovation centered around seafood menus continue supporting long-term regional demand growth.

Europe

Europe holds the largest regional share, accounting for nearly 35% of global demand. The region’s dominance is supported by Norway’s position as the world’s leading exporter, alongside strong consumption markets in the U.K., France, Germany, Spain, and Italy. European consumers demonstrate high familiarity with salmon products, particularly smoked and fresh varieties, which are deeply integrated into daily dietary habits. Regional growth is strongly influenced by sustainability awareness, with certifications such as ASC and MSC playing a critical role in purchasing decisions. Advanced cold-chain infrastructure and mature retail networks enable efficient product distribution across borders. Government support for sustainable aquaculture innovation and offshore farming expansion further strengthens supply capabilities. Increasing demand for healthy convenience foods and premium ready meals continues to stimulate consumption across Western and Northern Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and evolving dietary preferences toward high-quality imported proteins. Japan remains a mature and stable market anchored by sushi consumption traditions, while China is emerging as a major growth engine due to expanding middle-class populations and significant investment in cold-chain logistics infrastructure. South Korea and Australia demonstrate strong demand for premium seafood products supported by modern retail penetration. Emerging markets such as India and Southeast Asia are witnessing increasing adoption of Western-style diets and health-conscious eating behaviors, creating new opportunities for salmon consumption. Growth of online grocery platforms and premium supermarket chains across major metropolitan areas further accelerates accessibility, positioning Asia-Pacific as a key future demand center.

Latin America

Latin America plays a dual strategic role as both a major production hub and an expanding consumption market. Chile stands among the world’s largest salmon exporters, benefiting from favorable coastal conditions, established aquaculture expertise, and strong trade relationships with North America and Asia. Regional growth is supported by increasing domestic seafood consumption, urban middle-class expansion, and improved retail infrastructure in countries such as Brazil and Mexico. Government initiatives aimed at strengthening aquaculture exports and improving processing capabilities continue attracting investment. Rising awareness of nutritional benefits and increasing availability of affordable salmon products are gradually stimulating local demand, complementing the region’s export-driven industry structure.

Middle East & Africa

The Middle East and Africa region is experiencing steady demand expansion, primarily driven by rising income levels, tourism growth, and rapid development of hospitality and luxury dining sectors. Countries such as the UAE and Saudi Arabia are witnessing increasing salmon imports as premium seafood consumption rises alongside international restaurant expansion. Modern retail development and growing expatriate populations contribute to higher adoption of imported seafood products. In Africa, although the market remains relatively small, long-term growth potential is supported by urbanization, improving cold-chain infrastructure, and modernization of retail channels. Government initiatives focused on food security and diversification of protein sources are expected to gradually stimulate salmon consumption across key urban centers over the coming decade.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Global Salmon Market

- Mowi ASA

- Cermaq Group AS

- Lerøy Seafood Group ASA

- SalMar ASA

- Grieg Seafood ASA

- Bakkafrost Group

- AquaChile

- Tassal Group Limited

- Cooke Aquaculture Inc.

- Norway Royal Salmon ASA

- Multi X S.A.

- Nordic Aqua Partners

- Scottish Sea Farms Ltd.

- Huon Aquaculture Group

- Atlantic Sapphire ASA