Salad Dressing Market Size

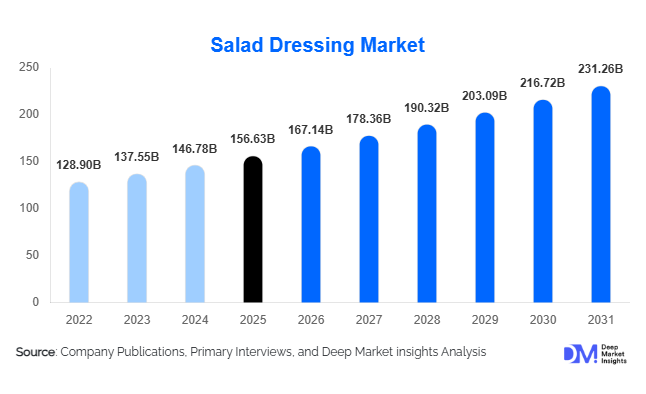

According to Deep Market Insights, the global salad dressing market size was valued at USD 156.63 billion in 2025 and is projected to grow from USD 167.14 billion in 2026 to reach USD 231.26 billion by 2031, expanding at a CAGR of 6.71% during the forecast period (2026–2031). The salad dressing market growth is primarily driven by rising health-conscious consumption, increasing adoption of ready-to-eat meals, and growing demand for flavor customization across household and foodservice applications. Expanding retail infrastructure, premium product innovation, and the shift toward clean-label and plant-based formulations are further strengthening long-term market expansion globally.

Key Market Insights

- Health-focused eating habits are accelerating global demand, with consumers increasingly incorporating salads and fresh meals into daily diets.

- Premium and gourmet dressings are gaining strong traction, supported by demand for organic, plant-based, and ethnic flavor profiles.

- North America dominates global consumption, driven by high packaged food penetration and strong retail distribution networks.

- Asia-Pacific is the fastest-growing regional market, fueled by urbanization, Western dietary adoption, and expanding middle-class populations.

- Foodservice and QSR expansion is significantly boosting bulk demand for mayonnaise and creamy dressings worldwide.

- Technological advancements in emulsification and packaging are improving shelf life, sustainability, and product quality.

What are the latest trends in the salad dressing market?

Clean-Label and Plant-Based Dressings Reshaping Product Innovation

Consumer preference is rapidly shifting toward natural, minimally processed foods, encouraging manufacturers to reformulate dressings using plant-based emulsifiers, cold-pressed oils, and natural preservatives. Vegan and allergen-free dressings are expanding shelf presence across supermarkets and online retail channels. Brands are emphasizing ingredient transparency and nutritional labeling, aligning with stricter food regulations and growing consumer awareness. Functional additions such as probiotics, protein enrichment, and reduced-sugar formulations are also emerging, positioning salad dressings as wellness-oriented food products rather than simple condiments.

Premiumization and Global Flavor Expansion

The globalization of cuisine and social media-driven food experimentation are accelerating demand for gourmet flavors. Mediterranean herbs, Asian sesame blends, spicy fusion dressings, and regional flavor innovations are becoming mainstream offerings. Premium SKUs command higher margins and attract younger consumers seeking restaurant-quality experiences at home. Limited-edition flavors and chef-inspired recipes are increasingly used by manufacturers to differentiate products and maintain consumer engagement, particularly in mature markets.

What are the key drivers in the salad dressing market?

Growth of Convenience and Ready-to-Eat Food Consumption

The expansion of ready meals, packaged salads, and meal kits is significantly increasing dressing consumption globally. Urban lifestyles and time-constrained consumers are driving demand for convenient flavor solutions integrated into prepared foods. Food manufacturers increasingly incorporate portion-controlled dressing packs into retail meal offerings, ensuring consistent demand from industrial buyers.

Rising Health Awareness and Dietary Shifts

Consumers are adopting balanced diets emphasizing vegetables and fresh ingredients, directly supporting dressing sales as essential meal complements. Low-fat, keto-friendly, and organic dressings are attracting health-conscious consumers while expanding the category beyond traditional users. Increasing gym culture and wellness trends further reinforce demand for lighter and functional dressing options.

What are the restraints for the global market?

Volatility in Raw Material Prices

Key ingredients such as vegetable oils, eggs, vinegar, and dairy products are subject to price fluctuations due to climate variability and global supply disruptions. These cost pressures directly impact manufacturer margins and pricing strategies, particularly within economy product tiers where price sensitivity is high.

Perception of High Fat and Sodium Content

Despite innovation, some consumers continue to associate dressings with high calorie and sodium levels. Regulatory scrutiny and nutrition labeling requirements are encouraging reformulation efforts, increasing R&D costs for manufacturers while posing challenges in maintaining taste consistency.

What are the key opportunities in the salad dressing industry?

Expansion of Plant-Based and Functional Nutrition Products

Plant-based diets are creating substantial opportunities for egg-free and dairy-free dressing innovations. Functional products enriched with probiotics, proteins, and micronutrients are emerging as premium offerings capable of commanding higher price points. Companies investing in clean-label innovation and sustainable sourcing are likely to gain competitive advantages as consumer expectations evolve.

Localization Strategies in Emerging Markets

Asia-Pacific, Latin America, and the Middle East present strong growth opportunities through localized flavor development. Sesame, yogurt-based, and spice-forward dressings tailored to regional cuisines allow brands to penetrate new markets efficiently. Retail modernization and cold-chain expansion further support distribution growth across developing economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 156.63 Billion |

| Market Size in 2026 | USD 167.14 Billion |

| Market Size in 2031 | USD 231.26 Billion |

| CAGR | 6.71% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global dressings market demonstrates strong product diversification, with mayonnaise-based dressings continuing to dominate overall consumption patterns. These products account for nearly 34% of total market share in 2025, primarily supported by their versatility across both household and commercial food applications. The widespread integration of mayonnaise-based dressings into sandwiches, burgers, wraps, and ready-to-eat meals has strengthened their position as a staple condiment within quick-service restaurants and casual dining establishments worldwide. The leading segment growth is driven by increasing demand for convenience foods, expansion of global fast-food chains, and the ability of mayonnaise formulations to serve as a base for flavored and customized sauces, enabling continuous product innovation by manufacturers.Vinaigrette dressings are experiencing accelerating adoption as consumers increasingly prioritize healthier dietary choices and lighter meal options. Rising awareness of calorie intake, preference for oil-and-vinegar blends, and alignment with plant-forward diets are encouraging demand across developed and emerging markets. Creamy dressings such as ranch and Caesar continue to maintain strong consumption levels, particularly in North America and Europe, where they are deeply embedded in culinary habits and foodservice menus. Meanwhile, specialty and gourmet dressings represent the fastest-growing category, benefiting from premiumization trends, growing exposure to international cuisines, and consumer willingness to experiment with ethnic flavors, organic ingredients, and artisanal formulations. Manufacturers are increasingly introducing clean-label, preservative-free, and functional ingredient variants to capture evolving consumer expectations.

Application Insights

Household consumption remains the dominant application segment, contributing approximately 57% of total demand, supported by structural shifts in consumer eating behavior toward home-prepared meals and healthier lifestyle choices. The leading segment driver is the sustained rise in home cooking, accelerated by digital recipe culture, social media food trends, and growing consumer interest in meal customization. Dressings are increasingly used not only for salads but also as marinades, dips, and cooking ingredients, expanding frequency of usage within domestic kitchens.Foodservice applications are expanding rapidly as global quick-service restaurant chains and casual dining formats integrate dressings into core menu offerings to enhance flavor differentiation and menu innovation. Industrial applications are also gaining momentum, particularly within ready meals, sandwiches, packaged salads, and prepared snack categories, creating stable recurring demand from large-scale food processors. The emergence of meal kits, protein bowls, plant-based prepared foods, and convenience-focused packaged meals is further broadening application scope, positioning dressings as essential flavor components within modern convenience food ecosystems.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution channels, accounting for nearly 45% market share, driven by extensive product assortments, strong brand visibility, and consumer preference for one-stop grocery shopping experiences. The leading channel driver is high consumer trust in organized retail combined with effective in-store merchandising strategies that encourage impulse purchases and brand switching. Promotional pricing, private-label expansion, and premium shelf positioning further reinforce sales performance within this channel.Online retail represents the fastest-growing distribution channel as e-commerce adoption accelerates globally. Direct-to-consumer strategies, subscription grocery models, and digital marketing campaigns are enabling both multinational brands and emerging niche players to expand market reach. Convenience stores continue to generate steady revenue through single-serve and on-the-go packaging formats aligned with urban lifestyles. Foodservice distribution channels remain critical for bulk product supply, ensuring consistent procurement by restaurants, catering operators, and institutional buyers, thereby stabilizing overall market demand.

End-Use Insights

Retail household consumption remains the primary end-use segment, reflecting the everyday integration of dressings into global dietary habits. Growth within this segment is supported by increasing experimentation with international cuisines, rising awareness of balanced nutrition, and demand for versatile flavor solutions that simplify meal preparation. Restaurants and quick-service chains represent the fastest-growing end-use category, driven by menu innovation, franchise expansion across emerging economies, and the growing importance of customizable meal options that rely heavily on sauces and dressings.Institutional catering services and food manufacturing industries are steadily increasing procurement volumes as production of ready-to-eat and ready-to-cook meals expands worldwide. Large-scale food processors rely on consistent dressing supply to maintain standardized flavor profiles across packaged products. Export-oriented demand is strengthening in food processing hubs such as the United States, Germany, China, and Thailand, where dressing manufacturing supports broader packaged food export ecosystems and international supply chain integration.

Explore more data points, trends and opportunities Download Free Sample Report

Salad Dressing Market Segmentations

By Type

- Ranch Dressing

- Caesar Dressing

- Italian Dressing

- Balsamic Vinaigrette

- Thousand Island Dressing

- Honey Mustard Dressing

- Blue Cheese Dressing

- French Dressing

- Greek Dressing

- Others

By Application

- Home Use

- Food Industry

- Catering

- Other

Regional Insights

North America

North America accounts for approximately 32% of the global market share, led by the United States, which contributes nearly 26% of global demand. Regional growth is supported by high per-capita salad consumption, strong penetration of organized retail, and widespread adoption of premium and flavored dressing varieties. The expansion of health-focused product lines, including organic, low-fat, and clean-label formulations, continues to reshape consumer purchasing behavior. Growth drivers also include strong quick-service restaurant density, continuous menu innovation, and rising demand for convenience foods aligned with busy lifestyles. Canada is witnessing increasing adoption of organic and natural dressings, supported by regulatory transparency and growing consumer preference for sustainably sourced ingredients.

Europe

Europe holds around 28% market share, with Germany, the United Kingdom, and France serving as major consumption centers. Regional growth is strongly influenced by stringent clean-label regulations and consumer preference for natural ingredients and minimally processed foods. The popularity of Mediterranean dietary patterns encourages demand for vinaigrettes and olive-oil-based dressings, supporting healthier product positioning. Expansion of private-label offerings by European retailers, rising vegan and plant-based food adoption, and increasing interest in locally sourced ingredients further contribute to market expansion. Innovation in gourmet and specialty dressings aligned with regional culinary traditions also strengthens premium segment growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at nearly 9% CAGR, driven by rapid urbanization, income growth, and westernization of dietary habits. China leads regional demand as Western-style fast food and packaged salad consumption expand across urban centers. India represents the fastest-growing country due to rising middle-class populations, expansion of modern retail chains, and increasing health awareness among younger consumers. Growth is further supported by rapid food delivery adoption and increasing exposure to global cuisines through digital platforms. Japan and South Korea maintain stable demand supported by premium product adoption, innovation in flavor fusion products, and strong convenience food consumption cultures.

Latin America

Latin America’s market growth is primarily driven by Brazil and Mexico, where expanding fast-food industries and improving retail infrastructure are increasing accessibility to packaged dressings. Rising disposable incomes and urban population growth are encouraging shifts from homemade condiments toward branded packaged products. Regional demand is also supported by increasing supermarket penetration, growth of modern grocery retail formats, and expanding youth demographics adopting Western-style eating habits. Local flavor adaptations and affordable product formats are enabling manufacturers to strengthen market penetration across price-sensitive consumer segments.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth supported by rising expatriate populations, tourism expansion, and increasing demand for international food products. Countries such as the UAE, Saudi Arabia, and South Africa are experiencing strong restaurant sector expansion, which is driving foodservice demand for dressings. Modern retail development, premium food imports, and growing consumer exposure to global cuisines are further accelerating adoption. Increasing urbanization, rising disposable incomes, and expansion of organized foodservice chains are expected to sustain long-term regional market growth, while halal-certified and premium-quality product offerings continue gaining importance among regional consumers.

Key Players in the Salad Dressing Market

- Unilever PLC

- The Kraft Heinz Company

- Nestlé S.A.

- Kewpie Corporation

- McCormick & Company Inc.

- Conagra Brands Inc.

- Hormel Foods Corporation

- Ken’s Foods Inc.

- Remia International

- Campbell Soup Company

- Litehouse Inc.

- Bolthouse Farms

- Mizkan Holdings Co., Ltd.

- Dr. Oetker Group

- Ajinomoto Co., Inc.