RUTF & RUSF Market Size

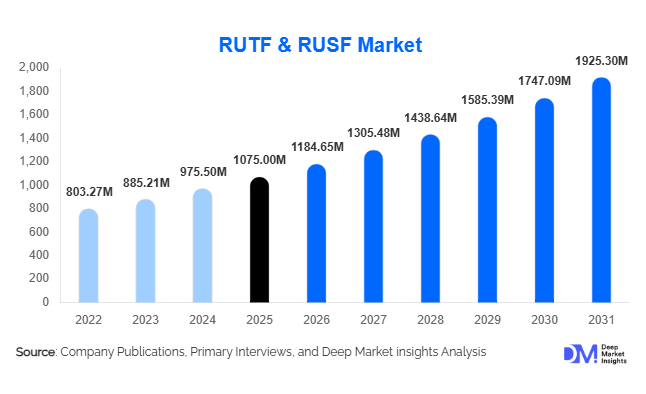

According to Deep Market Insights, the global Ready-to-Use Therapeutic Food (RUTF) and Ready-to-Use Supplementary Food (RUSF) market size was valued at USD 1,075 million in 2025 and is projected to grow from USD 1,184.65 million in 2026 to reach USD 1,925.30 million by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). Market growth is primarily driven by rising global malnutrition prevalence, expansion of government-led nutrition programs, increasing humanitarian aid funding, and the integration of therapeutic nutrition into national healthcare systems. RUTF and RUSF products have become essential interventions for treating and preventing acute malnutrition due to their long shelf life, high nutrient density, and suitability for low-resource environments without refrigeration or medical supervision.

Key Market Insights

- Institutional procurement dominates global demand, with UN agencies and humanitarian organizations accounting for a large share of purchases worldwide.

- Middle East & Africa leads consumption, supported by high malnutrition prevalence and sustained international nutrition programs.

- Preventive nutrition programs are expanding rapidly, shifting demand from emergency response toward long-term healthcare integration.

- Localized manufacturing initiatives are reducing import dependency and improving supply chain resilience across developing economies.

- Peanut-based paste formulations remain the industry standard, though plant-based and allergen-free alternatives are gaining momentum.

- Digital monitoring and supply chain technologies are improving treatment tracking, procurement efficiency, and program accountability.

What are the latest trends in the RUTF & RUSF market?

Shift Toward Preventive Nutrition Programs

The RUTF and RUSF industry is transitioning from emergency-driven deployment toward preventive healthcare nutrition models. Governments are increasingly incorporating supplementary feeding programs into maternal and child healthcare frameworks to prevent moderate acute malnutrition before escalation into severe conditions. This shift is stabilizing procurement cycles and creating recurring demand patterns rather than episodic emergency purchasing. Preventive programs targeting pregnant women and young children are expanding across South Asia and Sub-Saharan Africa, positioning RUSF products as essential public health tools rather than temporary humanitarian supplies.

Localization of Manufacturing and Supply Chains

Local production is emerging as a defining trend within the market. Governments and international organizations are encouraging regional manufacturing facilities to reduce logistics costs, improve response times, and support local economies. Domestic ingredient sourcing is increasing, enabling culturally acceptable formulations while minimizing foreign exchange exposure. Localization also strengthens supply resilience during global disruptions and aligns with procurement policies prioritizing locally produced nutrition products.

What are the key drivers in the RUTF & RUSF market?

Rising Global Burden of Acute Malnutrition

Growing food insecurity driven by climate change, conflicts, and economic instability has significantly increased the number of children suffering from severe and moderate acute malnutrition. International health organizations continue expanding treatment coverage, directly boosting demand for therapeutic and supplementary nutrition products. Population growth in vulnerable regions further amplifies long-term demand.

Expansion of Institutional Nutrition Funding

Global development organizations and philanthropic institutions have increased funding allocations toward nutrition security programs. Long-term financing commitments enable predictable procurement contracts, encouraging manufacturers to expand production capacity and invest in improved formulations. Nutrition is increasingly recognized as a foundational component of economic development and healthcare outcomes, reinforcing sustained investment.

What are the restraints for the global market?

Dependence on Donor Funding Cycles

A significant portion of RUTF and RUSF demand relies on international aid budgets. Variations in donor priorities or economic conditions can influence procurement volumes, creating periodic demand uncertainty for manufacturers. Companies must diversify geographic exposure and strengthen partnerships with national governments to mitigate funding volatility.

Raw Material Price Volatility

Key ingredients such as peanuts, milk powder, and vegetable oils experience price fluctuations influenced by agricultural output and global commodity markets. Since institutional buyers maintain strict pricing benchmarks, manufacturers face margin pressures when raw material costs increase. Ingredient diversification and localized sourcing strategies are increasingly used to manage these risks.

What are the key opportunities in the RUTF & RUSF industry?

Integration into National Healthcare Systems

Embedding therapeutic and supplementary nutrition into routine healthcare delivery presents significant long-term opportunities. Governments implementing large-scale nutrition missions are transitioning from emergency response to structured treatment protocols, ensuring sustained procurement demand. Manufacturers capable of aligning with national healthcare policies are positioned for long-term contract stability.

Innovation in Alternative Formulations

Development of non-peanut and plant-based formulations is opening new growth avenues. These alternatives address allergy concerns, improve cultural acceptance, and reduce dependency on single commodity supply chains. Innovation in micronutrient stabilization and shelf-life enhancement is further expanding product usability across diverse climates and distribution conditions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1075 Million |

| Market Size in 2026 | USD 1184.65 Million |

| Market Size in 2031 | USD 1925.30 Million |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The Ready-to-Use Therapeutic Food (RUTF) segment dominates the global therapeutic and supplementary nutrition market, accounting for nearly 62% of total market share in 2025. The segment’s leadership is primarily driven by its clinical effectiveness in treating severe acute malnutrition (SAM), particularly among children under five years of age. RUTF products require no cooking or refrigeration and can be consumed directly from packaging, making them highly suitable for deployment in resource-limited and emergency environments. Increasing endorsement by global health authorities and standardized treatment protocols established by international humanitarian organizations continue to reinforce RUTF’s adoption as the frontline intervention for acute malnutrition management. Growing investments in community-based management of acute malnutrition (CMAM) programs further strengthen demand, as decentralized treatment models rely heavily on ready-to-consume therapeutic foods.Ready-to-Use Supplementary Food (RUSF) represents a rapidly expanding segment supported by the global shift from reactive treatment toward preventive nutrition strategies. The leading growth driver for this segment is the rising integration of preventive nutrition interventions into maternal health, early childhood development, and food security programs. Governments and development agencies increasingly recognize that addressing moderate acute malnutrition before progression to severe stages significantly reduces healthcare costs and mortality risks. Expansion of maternal supplementation initiatives, school feeding programs, and community health outreach campaigns is accelerating RUSF adoption. Over the forecast period, increased emphasis on early nutritional intervention and resilience-building within vulnerable populations is expected to narrow the gap between therapeutic and supplementary product categories.

Formulation Insights

Paste-based formulations lead the global market with approximately 71% share, driven primarily by their superior usability, long shelf life, and nutritional density. The leading driver behind paste dominance is operational efficiency in large-scale nutrition programs, where minimal preparation requirements enable rapid administration by caregivers and community health workers. Peanut-based lipid nutrient pastes, in particular, offer optimal energy concentration and stability under extreme climatic conditions, making them highly suitable for humanitarian deployment across tropical and arid regions. Their resistance to microbial contamination and ease of dosage control further enhance program scalability and treatment adherence.Bar and powdered formulations are gradually gaining traction as nutrition programs evolve toward preventive and long-term supplementation models. These formats enable improved portion control, simplified logistics, and reduced transportation costs, which are critical considerations for governments implementing nationwide nutrition initiatives. Powdered products also allow flexibility in dietary integration, enabling blending with locally available foods to improve cultural acceptance and consumption consistency. Meanwhile, liquid lipid emulsions remain a niche but strategically important category, primarily expanding within clinical and hospital-based nutrition settings where controlled dosing and specialized therapeutic administration are required. Growth in institutional healthcare nutrition programs is expected to gradually expand this segment’s role.

Distribution Channel Insights

UN procurement agencies represent the largest distribution channel, accounting for roughly 48% of global demand. The leading driver of this dominance is centralized procurement systems that ensure quality standardization, predictable large-volume purchasing, and efficient distribution across humanitarian operations. Organizations operating global nutrition programs rely on bulk sourcing agreements to maintain consistent supply chains during emergencies and long-term development initiatives. This centralized model also enables manufacturers to scale production efficiently while meeting strict international nutritional and safety guidelines.Government nutrition programs are emerging as the fastest-growing distribution channel as national administrations increasingly prioritize food security and child health outcomes within public policy frameworks. Expansion of publicly funded maternal and child welfare schemes, school nutrition initiatives, and integrated healthcare delivery systems is driving direct government procurement. NGO-led procurement continues to play a critical role during humanitarian crises, conflict displacement, and climate-related emergencies where rapid response mechanisms are required. At the same time, healthcare institutions are increasingly incorporating therapeutic foods into clinical treatment pathways, reflecting growing medical recognition of nutrition as a foundational component of disease management and recovery.

End-Use Insights

Children under five suffering from severe acute malnutrition remain the largest end-use segment, representing approximately 55% of global consumption. The primary driver supporting this segment’s dominance is the high global burden of childhood malnutrition combined with strong international funding commitments focused on reducing child mortality rates. Therapeutic feeding protocols endorsed by global health organizations prioritize early intervention during childhood, ensuring sustained demand for specialized nutrition products across developing regions. Increasing expansion of community-based diagnosis and treatment programs further strengthens consistent product utilization.Maternal nutrition programs are witnessing rapid growth, supported by rising awareness of the intergenerational impact of prenatal nutrition on cognitive development, birth outcomes, and long-term population health. Governments and health agencies are increasingly integrating supplementary foods into antenatal and postnatal care frameworks, expanding the consumer base beyond pediatric applications. Emergency relief populations continue to represent a significant application area, particularly in regions affected by armed conflict, displacement, and climate shocks. Additionally, preventive community nutrition programs are emerging as a key growth engine, creating steady year-round demand rather than crisis-driven consumption cycles and contributing to improved supply chain stability for manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

RUTF & RUSF Market Segmentations

By Product Type

- Ready-to-Use Therapeutic Food

- Ready-to-Use Supplementary Food

- Lipid-Based Nutrient Supplements

- Preventive Supplementary Nutrition Products

By Formulation Type

- Paste-Based Formulations

- Powder-Based Formulations

- Bar-Based Formulations

- Lipid Emulsion & Liquid Formulations

By End User

- Children Under Five

- Children with Moderate Acute Malnutrition

- Pregnant & Lactating Women

- Emergency & Humanitarian Relief Populations

- Community Preventive Nutrition Programs

By Distribution Channel

- UN Agencies Procurement

- Government Nutrition Programs

- Non-Governmental Organizations

- Healthcare Institutions & Clinics

- Direct Institutional Contracts

Regional Insights

North America

North America accounts for around 12% of the global market, functioning primarily as a manufacturing, innovation, and funding hub rather than a major consumption center. The United States leads regional production capacity, supplying significant volumes to international humanitarian programs through established procurement partnerships. Regional growth is driven by strong research and development investments, advanced food processing technologies, and collaborations between private manufacturers and global aid organizations. Increasing innovation in formulation science, including allergen-reduced and plant-diversified therapeutic foods, further strengthens North America’s strategic role in shaping next-generation nutrition solutions. Additionally, sustained governmental and philanthropic funding commitments toward global food security initiatives continue to support export-oriented expansion.

Europe

Europe holds nearly 10% market share, supported by export-oriented manufacturing ecosystems and strong humanitarian financing structures. Countries such as France, the Netherlands, and the United Kingdom play central roles in procurement coordination and formulation innovation. Regional growth is primarily driven by development aid programs, policy leadership in global nutrition standards, and stringent regulatory frameworks that promote product quality and safety compliance. European institutions actively support innovation in sustainable ingredient sourcing and environmentally responsible packaging, aligning therapeutic nutrition production with broader sustainability goals. Continued collaboration between governments, NGOs, and multilateral agencies reinforces Europe’s influence as a regulatory and innovation leader within the global market.

Asia-Pacific

Asia-Pacific represents approximately 24% of global demand, led by India, Bangladesh, Pakistan, and Indonesia. Regional growth is driven by large population bases, persistent malnutrition challenges, and expanding government-led nutrition missions focused on maternal and child health. India is emerging as the fastest-growing country market due to increasing localization of production, public health investments, and integration of supplementary nutrition within national welfare programs. Rising awareness of early childhood nutrition, combined with improved healthcare access in rural areas, is accelerating adoption across South Asia. Additionally, regional manufacturing expansion aimed at reducing import dependency and improving cost efficiency is strengthening long-term market sustainability.

Latin America

Latin America accounts for nearly 8% of global market share, with Brazil, Haiti, and Guatemala leading adoption. Regional growth is supported by expanding preventive nutrition initiatives targeting vulnerable communities and improving child health indicators. Governments are increasingly collaborating with international organizations to strengthen nutrition infrastructure, enhance supply chain resilience, and expand community-based feeding programs. Urban poverty reduction initiatives and social protection schemes integrating nutritional supplementation are further contributing to gradual market expansion. Increased focus on localized production and culturally adapted formulations is expected to enhance program effectiveness and consumer acceptance across the region.

Middle East & Africa

The Middle East & Africa region dominates the global market with approximately 46% share in 2025, driven by high malnutrition prevalence and sustained humanitarian intervention programs. Countries such as Ethiopia, Nigeria, Kenya, and Sudan represent major demand centers due to food insecurity, climate vulnerability, and population displacement challenges. Regional growth is fueled by expanding community-based nutrition programs, international funding flows, and increasing localization of manufacturing capacity across Africa. Investments in regional production facilities are reducing logistical costs and improving supply responsiveness, transforming the region into both the largest consumer and fastest-growing production base globally. Rising collaboration between governments, NGOs, and private manufacturers is expected to accelerate market maturity while improving long-term nutrition outcomes.

Key Players in the RUTF & RUSF Market

- Nutriset

- Edesia Nutrition

- Valid Nutrition

- InnoFaso

- Mana Nutrition

- GC Rieber Compact

- Hilina Enriched Foods

- Insta Products EPZ

- Nutrivita Foods

- Compact AS

- Diva Nutritional Products

- Nutritional Foods International

- Power Foods Industries

- Amwili Foods

- Tabatchnick Nutrition Division