Robusta Coffee Beans Market Size

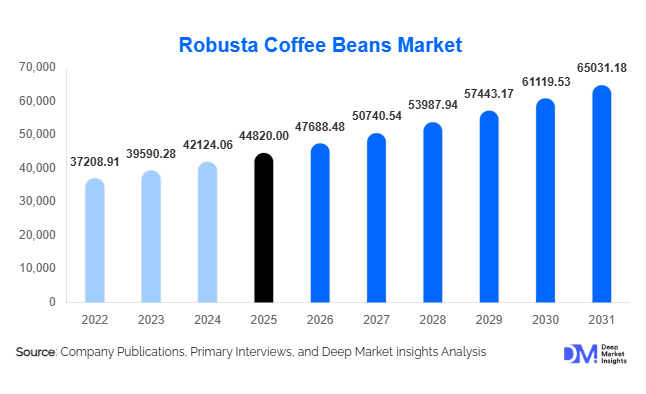

According to Deep Market Insights, the global robusta coffee beans market size was valued at USD 44,820 million in 2025 and is projected to grow from USD 47,688.48 million in 2026 to reach USD 65,031.18 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). Market expansion is supported by rising global coffee consumption, increasing demand for cost-efficient coffee blends, and rapid growth of instant coffee and ready-to-drink beverages across emerging economies. Robusta coffee beans, known for their higher caffeine content, disease resistance, and stable yields compared to arabica varieties, are increasingly preferred by manufacturers seeking price stability and consistent flavor profiles for mass-market products.

Key Market Insights

- Instant coffee and soluble coffee production remains the largest demand driver, accounting for a significant share of global robusta bean utilization.

- Asia-Pacific dominates global production and consumption, led by Vietnam, Indonesia, and India due to favorable agro-climatic conditions and export competitiveness.

- Private-label and value coffee brands are expanding globally, increasing dependence on robusta blends to maintain affordability.

- Out-of-home coffee consumption recovery across emerging markets is accelerating bulk procurement by foodservice chains.

- Sustainable sourcing certifications such as Rainforest Alliance and Fairtrade are influencing procurement strategies among multinational roasters.

- Technological improvements in post-harvest processing are improving robusta flavor quality, narrowing perception gaps with arabica beans.

What are the latest trends in the robusta coffee beans market?

Premiumization of Robusta Coffee

Historically positioned as a lower-cost alternative to arabica, robusta coffee is undergoing premium repositioning through improved cultivation practices and advanced processing techniques. Specialty-grade robusta, particularly fine robusta varieties from Vietnam and India, is gaining acceptance among specialty roasters and espresso-focused brands. Controlled fermentation, selective harvesting, and better drying infrastructure are improving cup profiles, enabling robusta beans to enter higher-margin market segments. This transition is allowing producers to command improved pricing while reducing dependence on commodity-grade exports.

Growth of Ready-to-Drink and Instant Coffee Segments

The rapid expansion of ready-to-drink coffee, canned coffee beverages, and single-serve instant products is reshaping demand dynamics. Robusta beans are widely used due to their stronger flavor, higher caffeine levels, and cost efficiency. Urbanization in Asia, Africa, and Latin America has accelerated demand for convenient coffee formats, driving large-scale procurement contracts by beverage manufacturers. Digital retail expansion and subscription-based coffee consumption models are also strengthening demand consistency across markets.

What are the key drivers in the robusta coffee beans market?

Rising Global Coffee Consumption

Global coffee consumption continues to expand steadily, particularly in emerging economies where coffee is transitioning from an occasional beverage to a daily consumption habit. Urban lifestyles, younger demographics, and café culture expansion are boosting overall demand volumes. Robusta beans benefit significantly due to their affordability and suitability for mass production, allowing manufacturers to scale supply efficiently while maintaining price competitiveness.

Cost Advantage and Supply Stability

Compared with arabica beans, robusta coffee offers higher yields, better resistance to pests, and adaptability to warmer climates. These advantages provide supply resilience amid climate volatility. Coffee brands increasingly incorporate higher robusta ratios in blends to manage price fluctuations and ensure consistent supply availability, particularly during arabica shortages.

Expansion of Instant Coffee Manufacturing

Instant coffee remains one of the fastest-growing categories globally, especially in Asia-Pacific and Eastern Europe. Robusta beans dominate this segment due to their strong flavor retention after processing. Multinational food companies are investing heavily in soluble coffee facilities, directly stimulating upstream demand for robusta production.

What are the restraints for the global market?

Price Volatility and Farmer Income Instability

Coffee prices remain sensitive to weather patterns, currency fluctuations, and global trade dynamics. Despite relatively stable yields, robusta farmers face margin pressures due to fluctuating export prices and rising input costs such as fertilizers and labor.

Perception Challenges Versus Arabica Coffee

Consumer perception continues to favor arabica as a premium product. Although quality improvements are narrowing the gap, branding challenges still limit adoption in specialty coffee segments, restricting value realization for producers.

What are the key opportunities in the robusta coffee beans industry?

Emerging Market Consumption Growth

Rapid income growth and urbanization across Southeast Asia, Africa, and South Asia present major opportunities for robusta coffee expansion. Countries such as India, Philippines, and Nigeria are witnessing rising domestic coffee consumption, supported by retail chain expansion and affordable beverage offerings. Local roasting capacity investments are enabling producing countries to capture more value domestically rather than exporting raw beans.

Climate-Resilient Coffee Cultivation

Climate change is shifting agricultural suitability away from arabica-growing regions, positioning robusta as a climate-resilient alternative. Governments and agricultural institutions are promoting robusta cultivation programs to secure long-term coffee supply. Investments in hybrid robusta varieties with improved flavor characteristics create opportunities for both producers and global buyers seeking sustainable sourcing.

Technology Integration in Supply Chains

Digital traceability platforms, blockchain-based sourcing verification, and AI-driven crop monitoring are improving transparency across coffee supply chains. These technologies enhance farmer productivity, reduce waste, and enable premium pricing through verified sustainability claims. Companies adopting traceable sourcing models are strengthening relationships with global retailers and specialty brands.

Product Type Insights

Conventional robusta coffee beans continue to dominate the global market landscape, accounting for nearly 72% of the total market share in 2025. This dominance is primarily attributed to their cost efficiency, high yield per hectare, and strong suitability for large-scale commercial applications, particularly within instant coffee manufacturing and blended roasted coffee formulations. Robusta beans contain higher caffeine levels and stronger flavor intensity compared to arabica, making them an essential component for mass-market coffee products where consistency, affordability, and supply stability remain critical purchasing factors. Large multinational roasting companies increasingly rely on conventional robusta sourcing to stabilize margins amid volatile arabica prices, reinforcing sustained demand growth for this segment.Organic robusta coffee is emerging as a high-growth segment as global consumers shift toward ethically sourced and environmentally sustainable products. Rising awareness regarding pesticide-free cultivation, biodiversity preservation, and traceability standards is encouraging retailers and specialty brands to expand organic offerings. Premium pricing opportunities and certification-driven exports are incentivizing producers in Asia and Africa to transition toward organic cultivation models. As sustainability commitments become central to corporate procurement strategies, organic robusta is expected to capture increasing attention from specialty roasters and premium instant coffee manufacturers.Washed robusta processing is gaining international traction as improvements in post-harvest processing technologies enhance flavor clarity, reduce bitterness, and allow robusta beans to penetrate higher-value espresso and specialty blends. Traditionally associated with lower-quality perception, robusta is undergoing repositioning as producers invest in advanced fermentation and washing techniques, enabling differentiation in global markets. This evolution is supporting diversification beyond commodity-grade usage and creating new revenue streams for producing countries.Green unroasted robusta beans remain the most widely traded product format globally, reflecting the strategic preference of international roasting companies to conduct centralized roasting operations. Centralized roasting enables better quality control, consistent flavor profiling, logistics optimization, and cost management across multiple regional markets. The dominance of green bean trade is further supported by global supply chain standardization and long-term procurement agreements between exporters and multinational coffee processors.

Application Insights

Instant coffee production represents the leading application segment, contributing approximately 41% of total global demand in 2025. The segment’s leadership is primarily driven by affordability, convenience, and long shelf life, making instant coffee particularly popular across emerging economies in Asia-Pacific and Eastern Europe. Rapid urbanization, growing working populations, and rising demand for quick beverage solutions continue to reinforce consumption patterns favorable to robusta-based instant coffee products. Manufacturers prefer robusta beans for instant coffee due to their strong solubility characteristics and cost advantages, positioning the segment as the primary demand driver across global markets.Espresso blends are experiencing steady expansion as coffee culture evolves worldwide. Robusta plays a crucial functional role in espresso preparation by enhancing crema formation, body, and caffeine intensity, characteristics increasingly valued in both commercial cafés and home brewing environments. The expansion of specialty coffee chains and premium café formats across developing economies is encouraging roasters to incorporate higher-quality robusta into blends to balance flavor and price competitiveness.Ready-to-drink (RTD) coffee beverages represent the fastest-growing application category, supported by convenience-oriented lifestyles, increasing on-the-go consumption, and strong penetration among younger consumers. Beverage manufacturers are increasingly incorporating robusta extracts to deliver stronger flavor profiles and higher caffeine content while maintaining cost efficiency in large-scale production. Innovation in cold brew, canned coffee, and functional coffee beverages is further accelerating procurement demand from beverage companies.Industrial food applications are also expanding steadily, with robusta coffee increasingly used as a flavoring ingredient in confectionery products, bakery items, dairy beverages, desserts, and nutritional products. Food manufacturers are leveraging coffee flavor profiles to enhance product differentiation, particularly in premium packaged foods and indulgence-based categories, thereby broadening the application scope of robusta beans beyond traditional beverage consumption.

Distribution Channel Insights

Direct business-to-business (B2B) contracts between exporters and multinational roasting companies dominate global distribution channels, accounting for nearly 55% of worldwide trade volumes. Long-term procurement agreements ensure supply stability, consistent quality specifications, and predictable pricing structures, which are essential for large-scale roasting operations. These partnerships also facilitate investment in sustainable sourcing initiatives and traceability programs, strengthening long-term supplier relationships.Commodity exchanges and global trader networks remain fundamental to market functioning by enabling efficient price discovery and facilitating bulk transactions. Futures markets help manage price volatility risks associated with climate variability and fluctuating production outputs. International trading houses continue to play a crucial role in logistics coordination, financing, and inventory management across producing and consuming regions.Online specialty marketplaces are expanding rapidly as digital trade platforms reduce entry barriers for small and medium-sized producers. These platforms allow direct engagement with specialty roasters, improving price realization and enabling transparency in sourcing practices. The rise of digital procurement ecosystems is reshaping traditional trade structures by promoting shorter supply chains and improved producer visibility.Cooperative-led export models are gaining strength across producing nations, empowering farmers through collective bargaining, shared processing infrastructure, and improved access to international buyers. Cooperatives are increasingly adopting certification programs and quality improvement initiatives, enhancing export competitiveness while supporting rural income stability.

End-Use Industry Insights

Retail packaged coffee continues to dominate global consumption volumes, supported by extensive supermarket penetration, private-label brand expansion, and increasing household coffee consumption worldwide. Large retailers are prioritizing competitively priced blends incorporating robusta to meet demand from value-conscious consumers, reinforcing sustained procurement from producing countries.The foodservice industry represents the fastest-growing end-use segment, driven by rapid expansion of café chains, quick-service restaurants, and specialty coffee outlets across Asia and the Middle East. Urban lifestyle changes, rising disposable incomes, and growing social coffee consumption culture are significantly increasing out-of-home coffee demand, positioning foodservice expansion as a major growth catalyst for robusta consumption.Export-driven demand remains a critical pillar of market growth, with Europe and the United States functioning as major import hubs for roasting, blending, and re-export operations. Advanced roasting infrastructure and established distribution networks in these regions sustain consistent global trade flows.The ready-to-drink beverage industry is witnessing double-digit growth rates globally, encouraging beverage manufacturers to secure long-term robusta supply agreements. Increasing innovation in functional beverages, protein coffees, and energy-focused formulations is further strengthening robusta’s role as a key raw material across diversified beverage portfolios.

| By Product Type | By Application | By End Use | By Distribution Channel | By Processing Method |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 46% of the global robusta coffee market share in 2025, establishing itself as both the largest production and consumption hub globally. Vietnam leads global output due to highly mechanized farming practices, favorable climatic conditions, and strong government-backed agricultural modernization programs that enhance productivity and export competitiveness. Indonesia and India continue expanding production capacities while improving processing quality to access premium export markets. Regional growth is strongly driven by rising domestic consumption in China and India, fueled by urbanization, expanding middle-class populations, and rapid café chain proliferation. Increasing investments in processing infrastructure, supportive export policies, and growing adoption of sustainable farming practices further accelerate regional market expansion.

Europe

Europe represents nearly 24% of global demand, supported by its position as a major coffee importing, roasting, and re-exporting region. Countries such as Germany, Italy, and France maintain strong import volumes due to well-established roasting industries and deeply rooted espresso consumption culture. Growth in private-label coffee manufacturing and supermarket-driven retail expansion continues to sustain robusta demand. Additionally, rising instant coffee consumption across Eastern Europe, driven by affordability preferences and convenience-oriented lifestyles, is acting as a key regional growth driver. Sustainability regulations and traceability requirements are also encouraging sourcing diversification toward certified robusta origins.

North America

North America demonstrates stable but consistent market growth, led by the United States and Canada. Increasing popularity of ready-to-drink coffee beverages, cold brew innovations, and value-oriented coffee brands are driving higher robusta utilization among large commercial roasters. Periodic arabica supply constraints and price volatility are encouraging blending strategies that incorporate robusta to maintain affordability without compromising flavor consistency. Expansion of convenience retail channels and growing demand for high-caffeine beverages among younger demographics further support regional demand growth.

Latin America

Latin America is strengthening its role as an emerging robusta production region, with Brazil leading through its rapidly expanding Conilon coffee segment. Producers across Mexico and Colombia are gradually introducing robusta cultivation to diversify agricultural risk and improve climate resilience amid changing weather patterns affecting arabica yields. Regional consumption is also rising alongside urbanization and expanding café culture in metropolitan areas. Investments in agronomic research, irrigation systems, and yield optimization technologies are supporting long-term production growth and export potential.

Middle East & Africa

The Middle East & Africa region represents both a key production base and one of the fastest-growing consumption markets, expanding at nearly 7.8% CAGR through 2031. Uganda continues to dominate robusta exports due to favorable agro-climatic conditions and increasing government support for coffee sector development. Rising coffee consumption across the UAE and Saudi Arabia, driven by premium café expansion and evolving lifestyle preferences, is strengthening import demand. Investments in processing facilities, export infrastructure, and regional trade integration initiatives are improving market accessibility. Additionally, population growth, urban retail expansion, and increasing youth-driven coffee culture are collectively accelerating regional market momentum.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Robusta Coffee Beans Market

- Nestlé S.A.

- JDE Peet’s N.V.

- Olam Group Limited

- Louis Dreyfus Company

- ECOM Agroindustrial Corp.

- Volcafe Ltd.

- Neumann Kaffee Gruppe

- Tata Consumer Products Limited

- Starbucks Corporation

- Lavazza Group

- Illycaffè S.p.A.

- Trung Nguyen Coffee Corporation

- Simexco Daklak Ltd.

- Sucafina S.A.

- Export Trading Group