Rice and Broken Rice Market Size

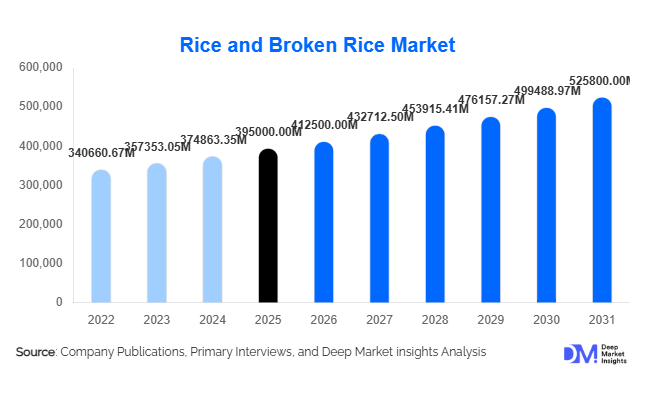

According to Deep Market Insights, the global rice and broken rice market size was valued at USD 395,000 million in 2025 and is projected to grow from USD 412,500 million in 2026 to reach USD 525,800 million by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). Market growth is primarily supported by rising global population levels, expanding food security programs, increasing export trade flows, and growing industrial utilization of broken rice across feed, brewing, and processed food industries. Rice continues to serve as the staple food for more than half of the global population, ensuring consistent baseline demand even during economic volatility. Meanwhile, broken rice is increasingly transitioning from a milling by-product into a value-generating commodity due to its affordability and versatility in industrial processing applications.

Key Market Insights

- Asia-Pacific dominates global consumption and production, accounting for the majority of rice output and exports worldwide.

- Broken rice demand is rising rapidly due to increasing adoption in animal feed, ethanol production, and brewing industries.

- Government food security and fortified rice programs are creating long-term procurement stability across developing economies.

- Africa represents the fastest-growing import market, driven by population expansion and limited domestic cultivation capacity.

- Premium aromatic rice varieties such as basmati and jasmine are witnessing strong export-led growth.

- Technological advancements in milling and grading are improving yield efficiency and export competitiveness.

What are the latest trends in the rice and broken rice market?

Fortified Rice Adoption Expanding Globally

Governments across Asia and Africa are increasingly integrating fortified rice into public food distribution systems to address micronutrient deficiencies. National nutrition initiatives are mandating iron, zinc, and vitamin-enriched rice supplies, creating large institutional procurement volumes. This trend is encouraging millers to invest in blending and coating technologies while improving value realization compared to conventional rice trading. International organizations are also supporting fortification programs through funding and policy frameworks, accelerating adoption across emerging markets.

Industrialization of Broken Rice Applications

Broken rice is evolving into a strategic industrial raw material. Food processors utilize it for rice flour and snack manufacturing, while feed producers leverage it as a digestible carbohydrate alternative to maize. Brewing and ethanol industries increasingly favor broken rice due to cost efficiency and fermentation advantages. This diversification is stabilizing price realizations for millers and reducing dependence on traditional household consumption demand. The trend is particularly visible in Southeast Asia and South America, where biofuel policies are supporting grain-based ethanol expansion.

What are the key drivers in the rice and broken rice market?

Population Growth and Staple Food Dependence

Rice remains the primary calorie source across Asia and large parts of Africa. Rapid population growth and urbanization are sustaining baseline consumption demand. Government procurement systems, buffer stock policies, and food subsidy schemes ensure consistent purchasing volumes, protecting the market from cyclical economic downturns.

Expansion of Processed Food Manufacturing

The growth of packaged foods, ready meals, gluten-free products, and rice-based snacks is significantly increasing industrial rice utilization. Urban lifestyles and convenience-oriented consumption patterns are encouraging food manufacturers to incorporate rice derivatives into multiple product categories, strengthening long-term demand stability.

What are the restraints for the global market?

Climate Sensitivity and Yield Volatility

Rice cultivation depends heavily on water availability and climatic stability. Floods, droughts, and temperature variations can significantly impact yields, leading to supply fluctuations and price volatility. Climate-related uncertainties remain a major operational risk for producers and exporters.

Trade Restrictions and Export Policy Risks

Export bans and tariff adjustments implemented during inflationary periods disrupt global trade flows. Import-dependent countries face supply uncertainty, while exporters encounter unpredictable policy environments that complicate long-term contracts and pricing stability.

What are the key opportunities in the rice and broken rice industry?

Expansion into Emerging African Markets

Sub-Saharan Africa represents one of the largest untapped growth opportunities due to strong population growth and limited domestic production capacity. Exporters investing in logistics infrastructure and bilateral trade partnerships can secure long-term supply agreements with importing governments.

Value Addition Through Industrial Processing

Processing broken rice into starch, ethanol, flour, and feed ingredients allows producers to diversify revenue streams beyond commodity trading. Investments in downstream processing facilities are improving margins and reducing exposure to raw grain price fluctuations.

Product Type Insights

The global rice market is structurally anchored by the dominance of whole grain rice, which accounted for nearly 72% of global demand in 2025, reflecting its indispensable role as a primary calorie source across both developed and developing economies. Whole grain rice continues to maintain market leadership primarily due to its direct consumption patterns, nutritional perception, affordability, and widespread cultural integration into daily diets. In large consumption economies across Asia-Pacific, Africa, and parts of Latin America, rice functions not merely as a food commodity but as a dietary foundation, driving consistent baseline demand regardless of economic cycles. The leading segment driver for whole grain rice remains its universal dietary adoption combined with strong government procurement programs that prioritize staple food security. Public distribution systems in major producing countries ensure stable consumption volumes, further reinforcing this segment’s dominance.Long-grain rice varieties represent the most internationally traded category within the product landscape, supported by superior cooking characteristics such as grain separation, texture consistency, and adaptability across cuisines. Consumer preferences in regions including South Asia, the Middle East, and Sub-Saharan Africa strongly favor long-grain rice due to culinary traditions centered around biryani, pilaf, and steamed rice dishes. Export-oriented producers have increasingly specialized in long-grain varieties to meet global demand patterns, strengthening trade flows and enhancing supply chain efficiencies. The expansion of premium basmati and jasmine rice exports also reflects rising disposable incomes and consumer willingness to pay for aroma, quality, and origin certification.Broken rice, while historically considered a lower-value byproduct of milling operations, has emerged as the fastest-growing product category due to its expanding industrial applications. The leading growth driver for this segment lies in its cost efficiency and versatility across downstream industries. Food processors utilize broken rice extensively in rice flour production, breakfast cereals, extruded snacks, and gluten-free formulations, benefiting from its uniform starch profile and processing efficiency. Additionally, brewing and fermentation industries increasingly rely on broken rice as a carbohydrate source due to improved fermentation yields and lower raw material costs compared to alternative grains.Rising demand from animal feed manufacturers has further accelerated broken rice utilization, particularly in regions facing volatility in corn and wheat prices. Feed formulators are incorporating broken rice as a substitute ingredient, improving feed conversion ratios while managing production costs. This shift has significantly reduced wastage across rice milling operations, enabling processors to monetize previously undervalued output streams. Technological improvements in grading and sorting equipment have also enhanced quality consistency, supporting broader acceptance of broken rice across industrial applications.Overall, diversification within product types is transforming rice from a traditional staple commodity into a multi-functional agricultural input supporting food, feed, and industrial ecosystems. Increasing innovation in value-added rice derivatives, including fortified rice kernels and functional grain blends, is expected to further strengthen demand diversification over the forecast period.

Application Insights

Direct human consumption remains the dominant application segment, representing approximately 74% of total global demand, underscoring rice’s unmatched importance in global food security systems. The leading segment driver in this category is population-driven staple consumption combined with urban affordability advantages compared to alternative cereals. Rapid population growth in Asia and Africa continues to sustain large-scale household consumption, while government subsidy programs and food distribution initiatives stabilize demand during periods of economic uncertainty.Urbanization is reshaping consumption behavior within this segment, as consumers increasingly seek convenience without abandoning staple dietary preferences. Pre-cleaned, fortified, and quick-cooking rice products are gaining popularity among urban households with limited preparation time. Nutritional awareness initiatives promoting whole grains and fortified staples are further enhancing consumption volumes, particularly in emerging economies seeking to address micronutrient deficiencies through staple food enhancement.The food processing industry represents one of the most dynamic application areas, driven by the rapid expansion of packaged foods, ready-to-eat meals, and gluten-free product innovation. Rice flour serves as a critical ingredient in bakery substitutes, snack manufacturing, infant nutrition products, and instant meal formulations. The leading growth driver for food processing applications lies in the global shift toward allergen-free and plant-based food solutions, where rice-based ingredients offer neutral taste profiles and functional versatility.Brewing and distillation applications are emerging as high-growth segments, supported by rice’s fermentation efficiency and starch conversion advantages. Breweries increasingly incorporate rice adjuncts to enhance flavor consistency, reduce protein haze, and improve production scalability. Distillation industries in Asia and North America are also expanding rice-based spirits production, capitalizing on consumer interest in premium and craft beverages. Technological advancements in enzymatic processing have further improved yield efficiency, making rice a competitive fermentation substrate.Animal feed applications are gaining traction globally as agricultural producers seek cost-effective alternatives amid volatile grain markets. Broken rice inclusion in poultry, aquaculture, and livestock feed formulations provides digestible energy while reducing dependence on traditional feed grains. Rising protein consumption worldwide is indirectly supporting this segment by expanding livestock production systems, thereby increasing feed demand linked to rice byproducts.Collectively, application diversification is enhancing the resilience of the global rice market by reducing reliance on single-use consumption patterns and enabling value creation across multiple industrial sectors.

Distribution Channel Insights

Traditional wholesale trade continues to dominate global rice distribution, accounting for nearly 55% of market share, particularly across developing economies where bulk procurement and informal retail networks remain deeply embedded within food supply systems. The leading segment driver for wholesale dominance is the efficiency of large-volume transactions connecting farmers, millers, and regional distributors. Wholesale markets provide price flexibility, immediate liquidity, and extensive geographic reach, making them indispensable in countries with fragmented retail infrastructures.In many emerging markets, traditional distributors serve as critical intermediaries ensuring rice availability across rural and semi-urban populations. Established trader relationships, credit-based transactions, and localized logistics networks enable consistent product flow even in regions lacking advanced retail systems. Government procurement agencies frequently rely on wholesale channels for stock distribution, reinforcing their structural importance within national food security frameworks.Modern retail channels, including supermarkets and organized grocery chains, are expanding steadily due to rising consumer preference for branded and packaged rice products. Increasing awareness regarding food safety, traceability, and standardized quality grading is encouraging consumers to transition toward packaged offerings. Branding strategies emphasizing origin certification, organic cultivation, and premium grain varieties are strengthening margins within modern retail environments.E-commerce platforms are also beginning to influence distribution dynamics, particularly in urban centers where digital grocery adoption is accelerating. Online retail enables direct-to-consumer sales models, improving price transparency and expanding access to specialty rice varieties. Subscription-based grocery models and bulk online purchasing are expected to reshape purchasing behavior among younger consumers.Export trading houses remain a cornerstone of international rice commerce, facilitating large-scale shipments between surplus-producing nations and import-dependent markets. These entities manage logistics coordination, currency risk, quality inspection, and regulatory compliance, ensuring smooth cross-border transactions. The increasing complexity of global trade regulations and sustainability certifications is further elevating the strategic role of export intermediaries within the distribution ecosystem.

End-Use Industry Insights

Household consumption continues to account for approximately 63% of global demand, reflecting rice’s position as a daily dietary necessity rather than a discretionary food item. The leading segment driver is consistent population growth combined with affordability relative to alternative staple grains. Even during economic downturns, household demand remains resilient, highlighting rice’s defensive market characteristics.Changing lifestyles are gradually reshaping household purchasing patterns, with increased demand for premium, fortified, and easy-to-cook rice variants. Urban consumers are prioritizing convenience, hygiene, and nutritional value, encouraging producers to introduce vacuum-packed, parboiled, and enriched rice products. Health-conscious consumers are also gravitating toward brown and minimally processed rice varieties due to perceived wellness benefits.The food manufacturing sector represents the fastest-growing end-use industry, expanding at an estimated 6.5% CAGR. The primary growth driver is the surge in convenience food consumption driven by urbanization, dual-income households, and evolving dietary habits. Rice-based noodles, snacks, frozen meals, and ready-to-cook kits are gaining popularity globally, particularly in regions experiencing rapid retail modernization. Manufacturers benefit from rice’s gluten-free properties, long shelf life, and adaptability across cuisines, making it an attractive ingredient for product innovation.Animal nutrition is emerging as a complementary end-use segment supported by integrated agricultural systems that maximize resource efficiency. Rice byproducts such as bran and broken rice are increasingly incorporated into feed formulations, enhancing sustainability by reducing agricultural waste. Growth in aquaculture production across Asia and Latin America is particularly contributing to increased utilization of rice-derived feed inputs.The brewing and distillation industry is also evolving into a meaningful end-use category as beverage producers experiment with rice-based formulations to achieve distinct flavor profiles and cost advantages. Expansion of craft beverage markets and premium spirits segments is expected to sustain long-term demand growth within this industry.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global rice market, holding approximately 58% of total market share, supported by unmatched production capacity, population density, and cultural dependence on rice as a staple food. The primary regional growth driver is the combination of large-scale domestic consumption and strong export competitiveness. Countries such as India, China, Thailand, and Vietnam collectively shape global supply dynamics through extensive cultivation areas, favorable climatic conditions, and government-backed agricultural policies.India remains the world’s leading exporter due to competitive pricing, diversified rice varieties, and improvements in irrigation infrastructure and mechanized farming practices. Export incentives, expanding port logistics, and strong global demand for basmati and non-basmati varieties continue to enhance India’s trade position. China, meanwhile, represents the largest consumption market, supported by population scale and government stockpiling programs designed to ensure food security and price stability.Southeast Asian nations are strengthening their global competitiveness through modernization of milling facilities, adoption of high-yield seed varieties, and investments in post-harvest infrastructure. Technological adoption across precision farming, digital supply chain management, and climate-resilient crop development is improving productivity while mitigating environmental risks. Rising urban populations across the region are also increasing demand for packaged and premium rice products, contributing to value-added market expansion.Additionally, regional trade agreements and intra-Asian commerce are facilitating smoother cross-border grain flows, reinforcing Asia-Pacific’s leadership in both production and consumption throughout the forecast period.

North America

North America accounts for nearly 7% of global demand, with growth primarily driven by diversification of consumption patterns and expansion of processed food industries. The leading regional driver is increasing demand for specialty and value-added rice products supported by multicultural dietary trends and rising health awareness. The United States leads regional production, focusing on high-quality long-grain and specialty rice varieties tailored for both domestic consumption and export markets.The rapid expansion of gluten-free and plant-based food categories has strengthened rice utilization within food manufacturing applications. Rice flour, rice milk, and ready-to-eat meal products are gaining popularity among health-conscious consumers seeking allergen-friendly alternatives. Brewing industries also contribute significantly to demand through the use of rice adjuncts in large-scale beer production.Advanced agricultural technologies, including precision irrigation and yield optimization techniques, enable efficient production despite limited cultivation areas compared to Asia. Strong logistics infrastructure and export capabilities allow North American producers to maintain competitiveness in premium global markets.

Europe

Europe contributes approximately 8% of global market share, characterized by strong import dependency and high demand for premium aromatic rice varieties. The leading regional growth driver is changing consumer dietary preferences favoring international cuisines and specialty grains. Countries such as Italy, France, and the United Kingdom serve as major consumption hubs, supported by diversified culinary traditions and expanding ethnic food markets.European consumers increasingly prioritize sustainability, organic certification, and traceable supply chains, encouraging importers to source high-quality rice from certified producers. Demand for risotto rice varieties and specialty grains continues to grow alongside restaurant sector expansion and premium retail offerings.Policy support for sustainable agriculture and reduced pesticide usage is influencing regional production practices, particularly in Southern European rice-growing areas. Innovation in eco-friendly packaging and carbon-conscious supply chains is further shaping market development across the region.

Latin America

Latin America holds roughly 9% of global demand, with Brazil acting as both a major producer and consumer within the region. The primary growth driver is steady population expansion combined with government-led food security programs aimed at maintaining affordable staple supplies. Rice remains central to daily diets across many Latin American countries, ensuring stable baseline consumption.Regional agricultural modernization, including mechanization and improved seed technologies, is enhancing productivity levels and reducing production costs. Expansion of retail infrastructure and packaged food industries is also supporting higher demand for processed rice products. Trade integration within the region allows surplus production from key countries to supply neighboring markets efficiently, strengthening regional self-sufficiency.Economic recovery trends and urbanization are encouraging growth in convenience foods, indirectly boosting demand for rice-based ingredients used in ready-to-cook meals and snacks.

Middle East & Africa

The Middle East and Africa represent the fastest-growing regional market, expanding at nearly 6.8% CAGR, driven primarily by rising population levels, urbanization, and heavy reliance on imports due to limited domestic agricultural capacity. The leading regional growth driver is import dependency combined with strong staple consumption growth across rapidly expanding urban populations.Countries such as Nigeria, Saudi Arabia, and Senegal rely extensively on international trade to meet domestic demand, making the region highly sensitive to global supply dynamics and pricing trends. Government initiatives aimed at improving food security are increasing strategic grain reserves and encouraging diversification of import sources.Rapid urban expansion is accelerating demand for affordable, easy-to-cook staple foods, positioning rice as a preferred dietary option. Investments in port infrastructure, logistics networks, and distribution systems are improving supply chain efficiency and reducing import bottlenecks. Additionally, rising incomes in Gulf countries are driving demand for premium rice varieties, while African markets continue to expand volume consumption supported by demographic growth.Collectively, demographic expansion, trade dependency, and evolving consumption patterns position the Middle East and Africa as a critical demand center shaping future global rice trade flows and long-term market growth trajectories.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Rice and Broken Rice Market

- Olam Group

- LT Foods Ltd.

- KRBL Limited

- Wilmar International

- Charoen Pokphand Foods

- Riceland Foods Inc.

- Ebro Foods S.A.

- SunRice Group

- Tilda Ltd.

- Amira Nature Foods Ltd.

- Thai Hua Rubber & Rice Group

- Vinafood II

- Daawat Foods

- Kohinoor Foods Ltd.

- Asia Golden Rice Co. Ltd.