Residual Spraying Insecticides Market Size

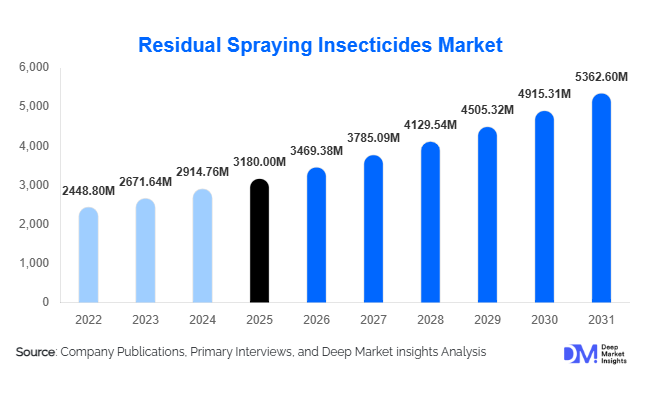

According to Deep Market Insights, the global residual spraying insecticides market size was valued at USD 3,180 million in 2025 and is projected to grow from USD 3,469.38 million in 2026 to reach USD 5,262.60 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The residual spraying insecticides market growth is primarily driven by increasing global vector-borne disease prevention programs, rising urban pest infestations, and expanding adoption of long-lasting insecticide formulations across public health and commercial pest management sectors. Governments and institutional buyers are increasingly prioritizing indoor residual spraying (IRS) as a cost-effective and scalable pest control solution, while technological improvements in microencapsulation and safer chemical formulations are improving product efficiency and regulatory acceptance worldwide.

Key Market Insights

- Public health vector control programs remain the largest demand driver, supported by malaria and dengue prevention initiatives across Asia and Africa.

- Microencapsulated and capsule suspension formulations are rapidly gaining adoption due to extended residual activity and reduced application frequency.

- Asia-Pacific dominates global consumption, led by India, China, and Southeast Asia’s expanding pest control programs.

- Africa represents a major institutional procurement hub, driven by international disease control funding and government spraying campaigns.

- Commercial pest control services are the fastest-growing end-use segment, supported by stricter hygiene compliance standards.

- Technological advancements in formulation chemistry are improving safety profiles, resistance management, and environmental compatibility.

What are the latest trends in the residual spraying insecticides market?

Shift Toward Long-Lasting Formulations

The industry is witnessing strong adoption of long-lasting insecticide formulations designed to provide extended protection on treated surfaces. Capsule suspension and microencapsulation technologies allow controlled release of active ingredients, improving residual effectiveness for several months compared to conventional sprays. Public health authorities increasingly favor these products because they reduce operational costs associated with frequent reapplication. Pest control operators are also transitioning toward formulations that minimize odor, staining, and human exposure risks, making them suitable for residential and hospitality environments.

Integration of Resistance Management Strategies

Growing insecticide resistance among mosquito and urban pest populations is driving innovation in chemical rotation strategies and multi-active formulations. Manufacturers are developing products combining different modes of action to sustain long-term effectiveness. Regulatory bodies and health organizations are encouraging integrated vector management approaches, combining residual spraying with monitoring systems and environmental control practices. Digital monitoring tools and data-driven pest surveillance programs are increasingly supporting targeted spraying interventions, improving efficiency while reducing excessive chemical use.

What are the key drivers in the residual spraying insecticides market?

Rising Incidence of Vector-Borne Diseases

Increasing outbreaks of malaria, dengue, chikungunya, and Zika virus infections are significantly driving global adoption of residual spraying solutions. Governments rely on indoor residual spraying programs to reduce disease transmission risk, particularly in tropical and subtropical regions. Climate change and expanding mosquito habitats have intensified prevention efforts, creating sustained long-term demand for residual insecticides.

Expansion of Professional Pest Control Services

The global pest control services industry is expanding rapidly as urban populations demand preventive pest management rather than reactive treatments. Commercial establishments such as food processing units, hospitals, hotels, and warehouses increasingly adopt scheduled residual spraying programs to comply with sanitation standards. Professional pest control operators benefit from recurring service contracts, strengthening consumption stability for residual insecticide products.

What are the restraints for the global market?

Development of Insecticide Resistance

Continuous exposure of pests to similar chemical classes, particularly pyrethroids, has resulted in resistance development in several regions. Reduced effectiveness requires chemical rotation and new formulation development, increasing research and operational costs for manufacturers and public health programs.

Stringent Environmental and Regulatory Policies

Regulatory restrictions on pesticide usage, especially in Europe and North America, limit the approval of certain active ingredients. Lengthy product registration procedures and environmental safety requirements increase compliance costs and delay product commercialization, posing challenges for smaller industry participants.

What are the key opportunities in the residual spraying insecticides industry?

Expansion of Government Vector Control Initiatives

Large-scale disease elimination programs across Africa and Asia provide long-term procurement opportunities for manufacturers. Multi-year government contracts ensure predictable revenue streams and encourage investment in WHO-recommended formulations. Countries expanding public health infrastructure are expected to significantly increase residual spraying coverage over the next decade.

Urbanization and Institutional Hygiene Compliance

Rapid urban growth is increasing pest pressure in residential complexes, transport infrastructure, and commercial facilities. Rising regulatory inspections in hospitality, healthcare, and food logistics sectors are accelerating adoption of preventive residual spraying solutions. Companies offering integrated pest management services combining monitoring, spraying, and compliance reporting are positioned to capture premium market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3180 Million |

| Market Size in 2026 | USD 3469.38 Million |

| Market Size in 2031 | USD 5362.60 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pyrethroid-based insecticides continue to dominate the global residual insecticides market, accounting for approximately 41% of total demand. The leadership of this segment is primarily driven by their high knockdown efficacy against a broad spectrum of vectors, cost-effectiveness for large-scale public health programs, extended residual action on treated surfaces, and relatively lower toxicity to humans and mammals compared to older chemistries. Their compatibility with indoor residual spraying programs and suitability across tropical and temperate climates further strengthen their market position. In addition, ongoing improvements in formulation technologies such as microencapsulation are enhancing residual performance and resistance management outcomes.Organophosphates and carbamates maintain stable demand, particularly in resistance-management strategies where rotation of active ingredients is required to combat vector resistance to pyrethroids. These chemistries are frequently deployed in areas with documented resistance patterns, ensuring continuity of vector control operations. Meanwhile, bio-based insecticides and insect growth regulators (IGRs) represent smaller but rapidly expanding segments, supported by tightening environmental regulations and growing public awareness regarding chemical exposure risks. Europe is at the forefront of adoption of sustainable formulations, while innovation in combination products and dual-mode-of-action formulations is improving performance across diverse pest species and climatic conditions.

Application Insights

Indoor residual spraying (IRS) represents the leading application segment, contributing nearly 46% of total global demand. The growth of this segment is primarily driven by large-scale malaria and vector-borne disease prevention programs funded by governments and international health organizations. IRS remains one of the most cost-effective interventions for reducing malaria transmission, particularly in endemic regions across Africa and parts of Asia. The long residual activity of modern insecticides enhances operational efficiency by reducing the frequency of reapplication, further strengthening this segment’s dominance.Outdoor barrier spraying is expanding steadily, particularly in urban and peri-urban environments where mosquito populations are increasing due to climate variability and water stagnation. Structural surface treatments in warehouses, food processing facilities, healthcare institutions, and logistics centers are gaining traction as hygiene compliance standards become stricter worldwide. Agricultural perimeter spraying and livestock facility treatments are emerging complementary applications, driven by the need to control disease-transmitting flies, ticks, and other vectors that affect animal health and productivity.

Distribution Channel Insights

Government procurement programs account for roughly 31% of global distribution, reflecting the institutional nature of vector control operations. The dominance of this channel is driven by centralized purchasing for national malaria control programs, public health campaigns, and emergency outbreak response initiatives. Bulk procurement agreements and long-term supply contracts ensure consistent demand volumes, particularly in developing economies.Professional pest control operators represent the fastest-growing distribution channel, supported by the expansion of recurring service models across residential, commercial, and industrial sectors. Urbanization, rising disposable incomes, and increased awareness of hygiene standards are accelerating demand for contract-based pest management services. Agricultural supply networks distribute residual insecticides for livestock and farm applications, while retail and DIY channels maintain moderate demand in developed markets where homeowners undertake preventive treatments. Institutional contracts with hospitality chains, healthcare facilities, and manufacturing plants are increasingly influencing purchasing decisions and product specifications.

End-Use Industry Insights

Public health agencies remain the largest end-use segment, contributing approximately 34% of global demand through organized vector control initiatives. The leadership of this segment is driven by sustained government investments in malaria eradication, dengue control, and other vector-borne disease management programs. International funding support and cross-border disease prevention collaborations further reinforce demand stability.Commercial pest control services are expanding at the fastest rate due to tightening hygiene regulations across hospitality, healthcare, food processing, and logistics industries. The agriculture and livestock sectors are emerging as important application areas as producers prioritize disease prevention, biosecurity compliance, and productivity improvement. Export-driven demand remains significant, particularly in African and Southeast Asian countries that import large volumes of residual insecticides for national indoor spraying programs and outbreak response measures.

Explore more data points, trends and opportunities Download Free Sample Report

Residual Spraying Insecticides Market Segmentations

By Active Ingredient Type

- Pyrethroids

- Organophosphates

- Carbamates

- Neonicotinoids

- Insect Growth Regulators

- Botanical & Bio-based Insecticides

By Formulation Type

- Wettable Powders

- Suspension Concentrates

- Emulsifiable Concentrates

- Capsule Suspension

- Water Dispersible Granules

- Ready-to-Use (RTU) Sprays

By Application Method

- Indoor Residual Spraying

- Outdoor Residual Barrier Spraying

- Structural Surface Treatment

- Agricultural Perimeter Spraying

By Target Pest

- Mosquitoes

- Cockroaches

- Bed Bugs

- Flies

- Termites

- Ticks & Fleas

- Stored-product Insects

By End-Use Sector

- Public Health Programs

- Residential Pest Control

- Commercial Facilities

- Agriculture & Livestock Premises

- Hospitality & Tourism Infrastructure

- Industrial & Warehousing Facilities

By Distribution Channel

- Government Procurement Programs

- Professional Pest Control Operators

- Agricultural Supply Networks

- Retail & DIY Channels

- Institutional Contracts

Regional Insights

North America

North America accounts for approximately 16% of the global residual insecticides market, led by the United States and supported by Canada. Regional growth is primarily driven by the strong presence of organized professional pest control companies, stringent food safety and workplace hygiene regulations, and rising consumer awareness regarding vector-borne diseases such as West Nile virus. Commercial real estate expansion, food processing infrastructure growth, and increasing demand for environmentally compliant formulations are further supporting market expansion. In Canada, regulatory alignment with sustainability standards is accelerating the shift toward lower-toxicity and bio-based products.

Europe

Europe holds nearly 14% of the global market share, with Germany, France, and the United Kingdom representing key demand centers. Regional growth is strongly influenced by strict regulatory frameworks governing pesticide usage, which are encouraging the adoption of low-toxicity, bio-based, and advanced residual formulations. Sustainability initiatives, integrated pest management (IPM) practices, and corporate environmental commitments are shaping procurement strategies across institutional and commercial sectors. Increasing urban density and cross-border trade activities also contribute to steady demand for structural pest control solutions.

Asia-Pacific

Asia-Pacific represents the largest regional market, accounting for approximately 34% of global demand in 2025, and is also the fastest-growing region. Growth is primarily driven by high population density, tropical climatic conditions conducive to mosquito breeding, rapid urbanization, and expanding public health investments. India plays a central role through large-scale government mosquito control and malaria prevention programs, while China’s expanding urban infrastructure and commercial real estate development support rising demand for professional pest control services. Southeast Asian countries such as Indonesia and Vietnam are witnessing increased adoption due to recurring dengue outbreaks. Infrastructure modernization, improving healthcare access, and greater awareness of vector control are expected to sustain long-term regional growth.

Latin America

Latin America accounts for nearly 9% of global demand, with Brazil and Mexico leading regional consumption. Market growth is primarily driven by recurrent dengue, Zika, and chikungunya outbreaks, prompting sustained municipal and national spraying programs. Favorable climatic conditions for mosquito proliferation, combined with expanding urban populations, continue to support demand. Increasing investments in public health infrastructure and cross-border disease surveillance initiatives are expected to further strengthen the regional market outlook.

Middle East & Africa

The Middle East & Africa region contributes approximately 27% of global demand, largely driven by malaria control programs across Sub-Saharan Africa. Countries such as Nigeria, Kenya, and Tanzania rely heavily on indoor residual spraying campaigns supported by international funding agencies and government-led initiatives. High malaria prevalence rates, warm climatic conditions, and limited access to preventive healthcare in certain areas sustain consistent procurement volumes. In the Gulf countries, rising hospitality sector expansion, urban development, and food safety compliance requirements are accelerating adoption of commercial pest control services, contributing to regional market diversification.

Key Players in the Residual Spraying Insecticides Market

- Bayer AG

- BASF SE

- Syngenta Group

- Sumitomo Chemical Co., Ltd.

- FMC Corporation

- Corteva Agriscience

- ADAMA Ltd.

- UPL Limited

- Rentokil Initial plc

- Rollins Inc.

- PelGar International

- Ensystex Inc.

- Neogen Corporation

- MGK (McLaughlin Gormley King Company)

- Central Garden & Pet Company