Red Wine Market Size

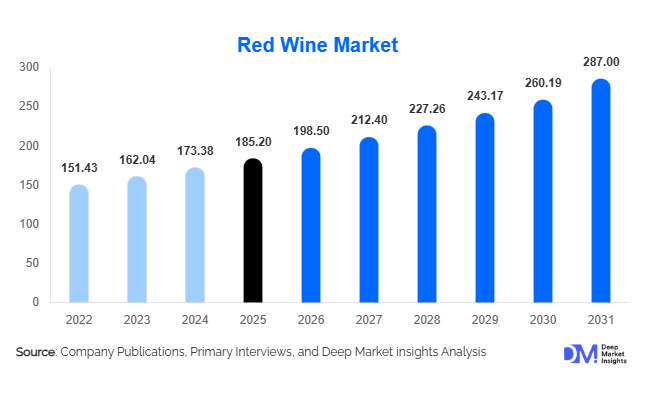

According to Deep Market Insights, the global red wine market size was valued at USD 185.2 billion in 2025 and is projected to grow from USD 198.5 billion in 2026 to reach USD 287 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The red wine market growth is primarily driven by increasing global wine consumption, rising premiumization trends, and growing demand for high-quality alcoholic beverages among middle- and high-income consumers.

Key Market Insights

- Premium and luxury red wines are witnessing strong demand, driven by consumers seeking quality, origin authenticity, and unique flavor profiles.

- Off-trade distribution channels dominate, supported by supermarkets and the rapid growth of online alcohol retail platforms.

- Europe leads the global market, benefiting from strong production capabilities and cultural wine consumption traditions.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and western lifestyle adoption.

- Glass bottle packaging continues to dominate, although canned and sustainable packaging formats are gaining traction.

- Sustainability and organic wine production are emerging as key differentiators influencing consumer purchasing decisions.

What are the latest trends in the red wine market?

Premiumization and Craft Wine Expansion

The global red wine market is increasingly shifting toward premium and craft wine offerings. Consumers are prioritizing quality over quantity, driving demand for boutique wineries, limited-edition vintages, and region-specific wines. This trend is particularly strong in developed markets such as North America and Europe, where consumers are willing to pay higher prices for superior taste and brand heritage. Producers are leveraging storytelling, vineyard origin transparency, and unique grape varietals to differentiate their offerings. The rise of micro-wineries and artisanal production techniques is also contributing to the diversification of premium wine portfolios globally.

Growth of Sustainable and Organic Wines

Sustainability has become a central theme in the red wine market, with consumers increasingly opting for organic, biodynamic, and natural wines. Producers are adopting eco-friendly viticulture practices, reducing chemical usage, and investing in recyclable packaging solutions. Certifications related to sustainability and organic farming are gaining importance, influencing consumer preferences and retail positioning. This trend is particularly prominent among younger consumers, who prioritize environmentally responsible products. Additionally, wineries are focusing on reducing carbon footprints through renewable energy adoption and sustainable water management practices.

What are the key drivers in the red wine market?

Rising Global Wine Consumption

The increasing acceptance of wine as a lifestyle beverage is a major driver of market growth. Urbanization, rising disposable incomes, and westernization of consumer habits have significantly boosted red wine consumption across emerging markets. Wine is increasingly being integrated into daily meals and social gatherings, expanding its consumer base beyond traditional markets.

Health Perception and Functional Benefits

Red wine is often associated with health benefits due to the presence of antioxidants such as resveratrol. Moderate consumption is perceived to support cardiovascular health, which has positively influenced demand among health-conscious consumers. This perception is particularly strong in developed markets, where wellness trends play a key role in purchasing decisions.

E-commerce and Digital Distribution Growth

The expansion of online retail channels has significantly improved accessibility to red wine products. E-commerce platforms offer a wide range of options, competitive pricing, and convenience, encouraging consumers to explore new brands and varieties. Subscription-based wine services and direct-to-consumer sales models are further driving market growth.

What are the restraints for the global market?

Stringent Regulations and High Taxation

The red wine market is subject to strict government regulations, including licensing requirements, advertising restrictions, and high taxation. These factors can limit market expansion, particularly in emerging economies where regulatory frameworks are more restrictive.

Climate Change Impact on Grape Production

Climate variability, including extreme weather conditions and changing rainfall patterns, is affecting vineyard productivity and grape quality. This has led to increased production costs and supply chain uncertainties, posing challenges for wine producers globally.

What are the key opportunities in the red wine industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Southeast Asian countries present significant growth opportunities for red wine producers. Rising disposable incomes, urbanization, and changing consumer preferences are driving demand in these regions. Market participants can leverage localized marketing strategies and distribution partnerships to capture this untapped potential.

Innovation in Packaging and Product Formats

The introduction of alternative packaging formats such as canned wine and bag-in-box solutions is attracting younger consumers and enhancing product convenience. These innovations also support sustainability initiatives by reducing packaging waste and transportation costs. Companies investing in innovative packaging solutions can expand their consumer base and improve brand visibility.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 185.2 Billion |

| Market Size in 2026 | USD 198.5 Billion |

| Market Size in 2031 | USD 287 Billion |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global red wine market continues to be overwhelmingly dominated by still red wine, which accounts for approximately 72% of the total market share in 2025. This dominance is primarily driven by its widespread acceptance across diverse consumer demographics, its versatility in pairing with a broad range of cuisines, and its availability across multiple price tiers, from economy to ultra-premium offerings. Still red wine benefits from deeply rooted consumption traditions, particularly in mature markets such as Europe, where it is considered an integral part of daily meals and social gatherings. Additionally, the relatively stable production processes and global familiarity with classic still wine styles further strengthen its leading position.Meanwhile, sparkling and fortified red wines occupy smaller but increasingly dynamic niches within the market. These categories are witnessing rising demand, particularly in premium and celebratory consumption segments, where consumers seek differentiated experiences. Sparkling red wines are gaining popularity among younger consumers and in emerging markets due to their approachable taste profiles and festive appeal. Fortified wines, on the other hand, continue to attract a niche but loyal consumer base, especially in regions with established consumption traditions.The growing inclination toward experiential consumption is further boosting demand for specialty red wines, including those produced from unique terroirs or employing unconventional winemaking techniques. Limited-edition releases, single-vineyard offerings, and wines with distinctive flavor profiles are increasingly appealing to enthusiasts and collectors, thereby expanding the overall scope of the product type segment.

Grape Variety Insights

Cabernet Sauvignon maintains its position as the leading grape variety in the global red wine market, holding an estimated 24% share in 2025. Its dominance can be attributed to its strong global recognition, consistent quality, and ability to thrive in a wide range of climatic conditions. This versatility allows producers across different regions to cultivate Cabernet Sauvignon, ensuring steady supply and reinforcing its presence in both premium and mid-range segments. Its bold flavor profile and aging potential further enhance its appeal among both casual consumers and connoisseurs.Blended wines are gaining considerable traction as producers increasingly experiment with combining different grape varieties to create unique flavor profiles. This trend aligns with the growing consumer interest in personalized and novel wine experiences. Blends allow winemakers to enhance consistency, balance, and complexity, while also providing flexibility in production. As a result, blended wines are emerging as a key growth area within the grape variety segment, particularly in markets where consumers are open to exploration and experimentation.

Price Segment Insights

The mid-range segment dominates the global red wine market, accounting for approximately 38% of the total share in 2025. This segment strikes a balance between affordability and perceived quality, making it highly attractive to a broad consumer base. Mid-range wines are widely available through both on-trade and off-trade channels, further supporting their strong market penetration. They are particularly popular among urban consumers who seek quality products without incurring the higher costs associated with premium offerings.Premium and luxury segments, although smaller in terms of overall share, are experiencing faster growth rates. This growth is fueled by increasing disposable incomes, evolving consumer preferences toward high-quality products, and the growing culture of wine appreciation. Premium wines are often associated with superior craftsmanship, unique terroirs, and limited production, which enhances their exclusivity and desirability. The rise of wine tourism and experiential consumption further contributes to the expansion of these segments.Economy wines continue to hold relevance, particularly in price-sensitive markets and among entry-level consumers. These wines serve as an important gateway for new consumers entering the category. In emerging economies, where affordability remains a key consideration, the economy segment plays a crucial role in driving volume sales and expanding the overall consumer base.

Packaging Insights

Glass bottles remain the dominant packaging format in the global red wine market, accounting for over 85% of the total share. This dominance is largely due to the association of glass packaging with quality preservation, authenticity, and premium perception. Glass bottles are particularly preferred for wines that require aging, as they provide optimal conditions for maintaining flavor integrity over time. Additionally, traditional wine consumers often view glass bottles as an essential aspect of the overall wine experience.The leading segment driver for glass bottle packaging is its ability to preserve product quality while reinforcing brand value and consumer trust. Premium and luxury wines, in particular, rely heavily on glass packaging to convey sophistication and heritage, which are critical factors influencing purchasing decisions.Sustainability considerations are also playing a significant role in shaping packaging trends. As consumers become more environmentally conscious, there is growing demand for eco-friendly packaging solutions. This has prompted manufacturers to explore lightweight glass bottles, recyclable materials, and innovative packaging designs that reduce carbon footprints without compromising product quality.

Distribution Channel Insights

Off-trade channels dominate the distribution landscape, accounting for approximately 60% of the global red wine market share in 2025. Supermarkets, hypermarkets, specialty stores, and online retail platforms form the backbone of this segment. The convenience of purchasing wine alongside regular groceries, combined with competitive pricing and promotional offers, drives strong consumer preference for off-trade channels.The leading segment driver for off-trade distribution is the rapid expansion of e-commerce and organized retail infrastructure. Online platforms provide consumers with access to a wide variety of products, detailed information, and home delivery services, significantly enhancing the overall purchasing experience. This trend has been further accelerated by changing consumer behaviors and the increasing adoption of digital technologies.The interplay between on-trade and off-trade channels is evolving, with many brands adopting omnichannel strategies to maximize reach and engagement. This includes integrating online and offline experiences, offering click-and-collect services, and leveraging digital marketing to influence purchasing decisions across multiple touchpoints.

End-Use Insights

Social occasions and events represent the largest end-use segment in the global red wine market, accounting for around 35% of total consumption. Weddings, celebrations, corporate events, and festive gatherings drive significant demand for red wine, particularly in premium categories. The association of wine with sophistication and celebration enhances its appeal in these settings.Household consumption is another major contributor, driven by the rising trend of at-home dining and entertainment. The increasing popularity of home-cooked meals, coupled with the influence of digital content related to food and wine pairing, has encouraged consumers to incorporate wine into their daily routines. This trend was further accelerated by shifts in lifestyle patterns and continues to sustain demand in the post-pandemic era.The hospitality sector remains a key end-use segment, with strong demand from restaurants, hotels, and catering services. Premium wines are particularly востребованы in fine dining establishments, where they complement high-quality cuisine and enhance the overall guest experience. Emerging applications such as corporate gifting and wine tourism are also gaining traction, creating new avenues for market growth. Wine tourism, in particular, is fostering direct consumer engagement and boosting brand loyalty by offering immersive experiences at vineyards and wineries.

Explore more data points, trends and opportunities Download Free Sample Report

Red Wine Market Segmentations

By Product Type

- Still Red Wine

- Sparkling Red Wine

- Fortified Red Wine

By Grape Variety

- Cabernet Sauvignon

- Merlot

- Pinot Noir

- Syrah/Shiraz

- Zinfandel

- Malbec

- Blends

By Price Segment

- Economy

- Mid-Range

- Premium

- Luxury

By Packaging Type

- Glass Bottles

- Bag-in-Box

- Cans

- PET Bottles

By Distribution Channel

- On-Trade

- Off-Trade

Regional Insights

Europe

Europe continues to dominate the global red wine market, accounting for approximately 45% of the total share in 2025. Countries such as France, Italy, and Spain are at the forefront of both production and consumption, supported by centuries-old winemaking traditions and well-established industry infrastructure. France alone contributes nearly 15% of global demand, driven by its strong domestic consumption and robust export market for premium wines.The regional growth in Europe is primarily driven by the deep-rooted cultural integration of wine into daily life, which ensures consistent consumption across generations. Additionally, the region benefits from favorable climatic conditions, diverse terroirs, and strict quality regulations that enhance the global reputation of European wines. The strong presence of appellation systems and geographical indications further reinforces consumer trust and brand value.Another key driver is the thriving wine tourism industry, which attracts millions of visitors annually to renowned wine regions such as Bordeaux, Tuscany, and Rioja. This not only boosts direct sales but also enhances global brand visibility. Furthermore, the increasing demand for organic and sustainable wines is encouraging producers to adopt eco-friendly practices, aligning with evolving consumer preferences and supporting long-term market growth.

North America

North America holds approximately 25% of the global red wine market share, with the United States being the largest consumer in the region. The market is characterized by a strong preference for premium wines and a well-developed distribution network that ensures widespread availability. California serves as a major production hub, contributing significantly to domestic supply and exports.Regional growth is driven by rising consumer awareness and appreciation of wine, supported by educational initiatives, wine tastings, and media influence. The increasing popularity of wine culture among younger demographics is also contributing to market expansion. Additionally, the presence of a large number of wineries and innovative producers fosters product diversity and continuous innovation.The rapid growth of e-commerce and direct-to-consumer sales channels is another significant driver in North America. Consumers benefit from convenient access to a wide range of products, personalized recommendations, and subscription services. Furthermore, the trend toward premiumization, coupled with higher disposable incomes, continues to drive demand for high-quality and artisanal wines in the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the global red wine market, with a projected CAGR of over 9%. Key markets such as China, Japan, and India are driving demand, supported by increasing disposable incomes, rapid urbanization, and the adoption of Western lifestyles. China accounts for nearly 8% of global demand, while India is emerging as a high-growth market with significant untapped potential.The primary driver of regional growth is the expanding middle-class population, which is increasingly inclined toward premium and lifestyle-oriented products. Wine is often perceived as a symbol of sophistication and status, making it particularly appealing to urban consumers. Additionally, the growing influence of social media and digital platforms is enhancing awareness and encouraging experimentation with different wine varieties.Government initiatives to promote domestic wine production, particularly in countries like China and India, are also supporting market growth. Improvements in distribution infrastructure and the expansion of retail networks are making wine more accessible to a broader consumer base. Moreover, the rising popularity of wine in social and corporate settings is further boosting demand across the region.

Latin America

Latin America is an important region in the global red wine market, led by major producers such as Argentina and Chile. These countries benefit from favorable climatic conditions, abundant natural resources, and a strong focus on export-oriented production. The region is known for producing high-quality wines at competitive prices, making it an attractive source for international markets.Regional growth is driven by increasing investments in vineyard expansion, technological advancements in winemaking, and the strengthening of export capabilities. The depreciation of local currencies in some countries has also made exports more competitive, further boosting market growth. Additionally, the growing domestic consumption of wine, supported by rising incomes and changing lifestyles, is contributing to overall demand.The development of wine tourism in regions such as Mendoza and the Maipo Valley is another key growth driver. These destinations attract both domestic and international tourists, creating opportunities for direct sales and brand promotion. As awareness of Latin American wines continues to grow globally, the region is expected to strengthen its position in the market.

Middle East & Africa

The Middle East and Africa region exhibits moderate growth in the global red wine market, with South Africa serving as a key production hub. The region's growth dynamics are influenced by a combination of economic, cultural, and regulatory factors. While certain countries impose restrictions on alcohol consumption, others present significant growth opportunities driven by tourism and expatriate populations.Regional growth is primarily driven by the expanding hospitality and tourism sectors, particularly in countries with well-developed travel industries. Hotels, restaurants, and resorts play a crucial role in driving wine consumption, especially among international visitors. South Africa's strong export market and reputation for producing high-quality wines further support regional growth.Additionally, increasing urbanization and the gradual shift in consumer preferences toward premium and imported products are contributing to market expansion in select markets. Investments in marketing, distribution, and brand building are also helping to enhance the visibility and accessibility of red wine across the region, despite existing regulatory challenges.

Key Players in the Red Wine Market

- E. & J. Gallo Winery

- Constellation Brands

- Treasury Wine Estates

- Pernod Ricard

- Castel Group

- Accolade Wines

- The Wine Group

- Jackson Family Wines

- Concha y Toro

- Grupo Peñaflor

- Louis Jadot

- Antinori Group

- Beringer Vineyards

- Miguel Torres S.A.

- Viña Santa Rita