Red Clover Supplement Market Size

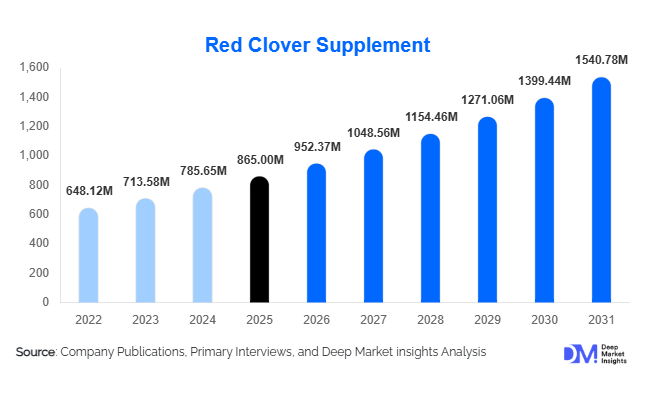

According to Deep Market Insights,the global red clover supplement market size was valued at USD 865 million in 2025 and is projected to grow from USD 952.37 million in 2026 to reach USD 1,540.78 million by 2031, expanding at a CAGR of 10.1% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer preference for plant-based hormonal health solutions, rising awareness of menopause symptom management, and expanding adoption of botanical nutraceuticals within preventive healthcare regimes worldwide.

Key Market Insights

- Plant-based hormone support solutions are gaining rapid acceptance as consumers increasingly seek alternatives to synthetic hormone replacement therapies.

- Standardized isoflavone extracts are becoming the industry benchmark, improving product credibility and clinical positioning.

- North America dominates global demand due to mature supplement consumption habits and strong practitioner recommendations.

- Asia-Pacific is the fastest-growing regional market, supported by rising preventive healthcare awareness and expanding middle-class populations.

- E-commerce channels are reshaping distribution, enabling direct-to-consumer supplement brands to scale globally.

- Product innovation combining red clover with probiotics, collagen, and adaptogens is expanding applications beyond menopause management.

What are the latest trends in the red clover supplement market?

Shift Toward Clinically Standardized Botanical Supplements

The market is witnessing a strong transition toward standardized botanical formulations with defined isoflavone concentrations. Consumers increasingly demand measurable efficacy, pushing manufacturers to invest in validated extraction processes and quality certifications. Clinical positioning has strengthened physician confidence, enabling red clover supplements to move beyond traditional herbal remedies into evidence-supported nutraceutical categories. Brands are highlighting standardized potency, traceability, and third-party testing as key differentiators, contributing to premium pricing strategies and improved consumer trust.

Digital Health and Personalized Nutrition Integration

Technology adoption is reshaping supplement consumption patterns. Personalized nutrition platforms now integrate hormonal health assessments, allowing red clover supplements to be recommended within customized wellness programs. Subscription-based supplement models are improving repeat purchases and consumer retention. AI-driven wellness applications, digital menopause communities, and telehealth consultations are also increasing product awareness among women seeking natural health solutions, especially in developed markets.

What are the key drivers in the red clover supplement market?

Growing Demand for Natural Menopause Management

Rising global female aging demographics are significantly increasing demand for non-pharmaceutical menopause solutions. Red clover supplements, rich in phytoestrogens, are widely perceived as safer alternatives to synthetic hormone therapies. Healthcare practitioners increasingly recommend botanical interventions for mild-to-moderate menopausal symptoms, accelerating adoption across North America and Europe. Growing consumer education campaigns and women’s health awareness initiatives further reinforce this trend.

Expansion of Plant-Based Preventive Healthcare

The broader shift toward plant-based lifestyles has positively influenced nutraceutical consumption patterns. Consumers increasingly prioritize vegan, clean-label, and sustainably sourced supplements. Red clover aligns strongly with these preferences, benefiting from botanical origin positioning and compatibility with holistic wellness routines. Preventive healthcare adoption among younger consumers is expanding usage beyond menopause applications into cardiovascular and bone health categories.

What are the restraints for the global market?

Regulatory Variability Across Markets

Regulatory frameworks governing herbal supplements vary significantly across countries, particularly regarding health claims and ingredient standardization. Compliance requirements increase product development timelines and operational costs for manufacturers seeking global expansion. Smaller brands often face barriers when navigating diverse approval pathways.

Raw Material Quality and Supply Variability

Red clover cultivation is sensitive to climate conditions, which can influence isoflavone concentration levels in raw materials. Variability in botanical quality creates challenges in maintaining consistent product potency. Manufacturers must invest heavily in testing, sourcing controls, and standardized extraction technologies to ensure uniform efficacy, increasing production costs.

What are the key opportunities in the red clover supplement industry?

Expansion into Emerging Wellness Markets

Rapid healthcare awareness growth in Asia-Pacific and Latin America presents strong opportunities for market expansion. Countries such as China, India, Brazil, and Mexico are witnessing rising demand for herbal supplements influenced by traditional medicine practices. Localization strategies, affordable formulations, and online distribution partnerships are expected to unlock significant untapped consumer bases.

Personalized Women’s Health Platforms

The emergence of personalized nutrition and digital wellness ecosystems provides new revenue opportunities. Red clover supplements are increasingly incorporated into menopause management programs, hormone balance subscriptions, and aging-well solutions. Integration with telehealth services and digital diagnostics allows brands to position products as part of long-term wellness solutions rather than standalone supplements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 865 Million |

| Market Size in 2026 | USD 952.37 Million |

| Market Size in 2031 | USD 1540.78 Million |

| CAGR | 10.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Capsules dominate the red clover supplement market, accounting for nearly 34% of global revenue, primarily driven by their superior dosage precision, ease of consumption, longer shelf stability, and strong consumer familiarity within the dietary supplement category. The leading position of capsules is further supported by manufacturers’ ability to standardize isoflavone concentrations, which enhances clinical positioning and consumer trust, particularly among menopause-focused users seeking consistent therapeutic outcomes. Tablets and softgels follow closely, benefiting from cost efficiency and widespread availability across pharmacy retail and mass-market distribution channels. Softgels, in particular, appeal to consumers seeking improved bioavailability and easier swallowing experiences. Liquid extracts and tinctures are gaining momentum among herbal medicine practitioners and natural health consumers due to faster absorption characteristics and flexible dosing formats. Powdered formulations are expanding steadily as functional beverage manufacturers integrate botanical ingredients into wellness drink mixes and personalized nutrition systems. Ongoing innovation in delivery technologies, including vegan capsules, clean-label excipients, and sustained-release formulations, continues to strengthen premium product differentiation while supporting long-term category expansion.

Application Insights

Menopause symptom management represents the largest application segment, contributing approximately 41% of total market demand, primarily driven by increasing global awareness of natural alternatives to hormone replacement therapy and growing preference for plant-based phytoestrogens. Clinical research highlighting the effectiveness of red clover isoflavones in reducing hot flashes, hormonal imbalance symptoms, and sleep disturbances reinforces this segment’s leadership. Cardiovascular health and bone support applications are expanding steadily as scientific evidence links isoflavones with cholesterol regulation and bone density maintenance, encouraging broader adoption among aging populations focused on preventive healthcare. Skin health and anti-aging applications are emerging rapidly within the beauty-from-within movement, particularly across Europe and Asia, where consumers increasingly associate internal supplementation with long-term dermatological benefits. Preventive wellness adoption among younger demographics is also rising, with consumers aged 25–40 incorporating botanical supplements into daily health routines, thereby diversifying application areas beyond traditional hormonal health positioning and supporting sustained market expansion.

Distribution Channel Insights

Online retail and e-commerce channels lead distribution, accounting for roughly 37% of global sales, driven by digital health awareness, subscription-based purchasing models, personalized supplement recommendations, and cross-border accessibility. The convenience of online platforms allows consumers to access product education, clinical information, and peer reviews, significantly influencing purchasing decisions. Pharmacies and drug stores remain essential channels, particularly among older consumers who prioritize professional guidance and product credibility when purchasing hormonal health supplements. Health and nutrition specialty stores continue to attract premium consumers seeking curated wellness solutions and practitioner-recommended products. Meanwhile, direct-to-consumer brands are expanding rapidly through influencer marketing, telehealth integrations, and digital wellness communities, enabling brands to build stronger customer relationships while improving margins and brand loyalty.

Consumer Demographic Insights

Women aged 40 years and above represent the largest consumer demographic, accounting for approximately 52% of global consumption, primarily driven by the direct relevance of red clover supplements to menopause symptom management and hormonal balance support. This segment demonstrates high repeat purchase behavior due to long-term supplementation needs and growing awareness of natural therapeutic alternatives. Adult women aged 25–40 are increasingly adopting red clover supplements for preventive hormonal wellness, skin health benefits, and lifestyle-driven self-care practices, reflecting a shift toward proactive health management. Consumers aged above 60 also contribute significantly to sustained demand as aging populations seek cardiovascular, bone, and overall wellness support through plant-based solutions. Although still a niche category, emerging interest in men’s hormonal balance and healthy aging supplements is gradually expanding the consumer base, creating opportunities for product diversification and targeted marketing strategies.

End-Use Industry Insights

The nutraceutical and dietary supplements industry dominates end-use consumption, contributing nearly 63% of total demand, supported by established regulatory pathways, standardized formulations, and strong consumer trust in supplement-based health management. The leading position of this segment is driven by rising global preventive healthcare adoption and increasing reliance on natural botanical ingredients for long-term wellness support. Functional foods and beverages represent the fastest-growing end-use industry as manufacturers incorporate red clover extracts into fortified drinks, nutrition powders, and personalized wellness formulations aligned with clean-label trends. Cosmeceuticals are emerging as a promising application area, leveraging antioxidant and phytoestrogen properties to support skin elasticity, hydration, and anti-aging formulations within the ingestible beauty category. Additionally, export-oriented ingredient trade between Asia and developed markets in Europe and North America is strengthening global supply chains, improving raw material accessibility, and encouraging large-scale commercial expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Red Clover Supplement Market Segmentations

By Product Type

- Capsules

- Tablets

- Softgels

- Liquid Extracts & Tinctures

- Powdered Supplements

- Standardized Isoflavone Extract Formulations

By Application

- Menopause Symptom Management

- Hormonal Balance Support

- Cardiovascular Health

- Bone Health Support

- Skin Health & Anti-Aging

- General Preventive Wellness

By Distribution Channel

- Online Retail & E-commerce Platforms

- Pharmacies & Drug Stores

- Health & Nutrition Specialty Stores

- Supermarkets & Hypermarkets

- Direct-to-Consumer (Brand Websites & Subscription Models)

By End Use Industry

- Nutraceutical & Dietary Supplements

- Functional Food & Beverage Industry

- Cosmeceuticals & Beauty-from-Within Products

- Herbal Medicine & Traditional Wellness

By Consumer Demographics

- Women Aged 40+ (Menopause Segment)

- Adult Women (25–40 Preventive Health Users)

- Senior Consumers (60+ Wellness Support)

- Emerging Male Hormonal Health Users

Regional Insights

North America

North America accounted for approximately 36% of global market share in 2025, led by the United States and Canada. Regional growth is primarily driven by high dietary supplement penetration, strong consumer awareness regarding menopause health, and widespread acceptance of botanical alternatives to synthetic hormone therapies. Advanced e-commerce ecosystems, practitioner endorsements from naturopaths and integrative healthcare professionals, and increasing demand for clean-label and plant-based supplements continue to reinforce market leadership. Aging demographics and rising healthcare costs further encourage preventive supplementation, sustaining long-term demand growth across the region.

Europe

Europe held nearly 29% market share, with Germany, the United Kingdom, France, and Italy leading adoption. Growth across the region is supported by longstanding phytotherapy traditions, strong regulatory frameworks for herbal medicines, and high consumer confidence in scientifically validated botanical products. Germany remains a key contributor due to its mature botanical supplement industry and physician acceptance of herbal therapies. Increasing demand for natural women’s health solutions, expanding beauty-from-within trends, and growing organic product preferences are further strengthening regional market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 12% CAGR through 2031. Growth is driven by rising disposable incomes, rapid urbanization, and increasing awareness of preventive healthcare across China and India. Expanding middle-class populations are adopting dietary supplements as part of modern wellness lifestyles, while Japan and South Korea benefit from aging demographics and deeply established supplement consumption cultures. Additionally, strong manufacturing capabilities, expanding e-commerce penetration, and integration of traditional herbal medicine practices with modern nutraceutical innovation are accelerating regional adoption.

Latin America

Brazil and Mexico lead demand across Latin America, supported by improving healthcare awareness, expanding pharmacy retail networks, and growing accessibility of affordable herbal supplements. Consumers increasingly view botanical products as cost-effective preventive healthcare solutions amid rising medical expenses. Urbanization, increasing female workforce participation, and growing exposure to global wellness trends through digital platforms are further contributing to market expansion, creating favorable long-term growth opportunities across the region.

Middle East & Africa

The Middle East and Africa region is emerging steadily, led by the UAE and South Africa. Regional growth is driven by rising health consciousness, expanding premium supplement retail infrastructure, and increasing demand for imported nutraceutical products among urban populations. Wellness tourism initiatives, growing disposable incomes in Gulf countries, and expanding pharmacy chains are supporting product availability and consumer education. Additionally, gradual regulatory development and increasing awareness of preventive healthcare are expected to accelerate adoption across major metropolitan markets over the forecast period.

Key Players in the Red Clover Supplement Market

- Nature’s Way Products LLC

- NOW Foods

- Gaia Herbs

- Solgar Inc.

- Nature’s Bounty Co.

- Herbalife Ltd.

- Blackmores Limited

- Swanson Health Products

- Bio-Botanica Inc.

- Holland & Barrett International

- Solaray Inc.

- Integria Healthcare

- Arkopharma Laboratories

- Vitacost (Kroger Health Division)

- Thompson’s Herbal Supplements