Ready-To-Eat Meal Delivery Service Market Size

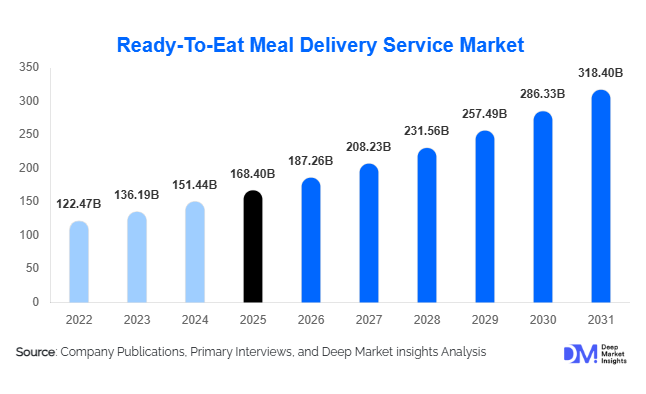

According to Deep Market Insights, the global ready-to-eat (RTE) meal delivery service market size was valued at USD 168.4 billion in 2025 and is projected to grow from USD 187.26 billion in 2026 to reach USD 318.40 billion by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). Market expansion is primarily driven by rising urbanization, increasing dual-income households, rapid digital food ordering adoption, and growing consumer preference for convenience-oriented nutrition solutions. The proliferation of cloud kitchens, subscription-based meal plans, and AI-enabled logistics optimization is further transforming the competitive landscape.

Key Market Insights

- Convenience-led consumption patterns are reshaping global foodservice demand, with ready-to-eat meals becoming a routine replacement for home cooking in urban markets.

- Subscription-based meal delivery models are expanding rapidly due to predictable revenue streams and personalized nutrition offerings.

- North America dominates market revenue owing to mature digital ordering ecosystems and high consumer spending on prepared meals.

- Asia-Pacific is the fastest-growing region, driven by rapid urban population growth and strong adoption of mobile food delivery platforms.

- Health-focused and diet-specific meals such as keto, vegan, and high-protein options are gaining significant traction globally.

- Automation and AI logistics optimization are improving delivery efficiency, reducing operational costs, and enhancing customer retention.

What are the latest trends in the ready-to-eat meal delivery service market?

Personalized Nutrition and Subscription Models

Consumers increasingly prefer customized meal solutions aligned with dietary goals, health conditions, and lifestyle preferences. Companies are leveraging AI-driven recommendation engines and nutritional analytics to curate personalized weekly meal plans. Subscription services offering calorie-counted meals, fitness-oriented diets, and medical nutrition programs are expanding across North America, Europe, and Asia-Pacific. This trend improves customer loyalty while enabling companies to optimize procurement and production planning through predictable demand cycles.

Expansion of Cloud Kitchens and Hyperlocal Fulfillment

The rapid growth of cloud kitchens is redefining food delivery economics. Operators are eliminating dine-in infrastructure and focusing entirely on delivery-centric production hubs. Hyperlocal fulfillment centers reduce delivery time and logistics costs while enabling menu localization based on regional preferences. Shared kitchen infrastructure is also lowering entry barriers for new brands, accelerating innovation and menu diversification within the ready-to-eat meal delivery ecosystem.

What are the key drivers in the ready-to-eat meal delivery service market?

Urban Lifestyle Transformation

Rapid urbanization and increasing working populations have significantly reduced time available for meal preparation. Busy schedules, long commuting hours, and growing single-person households are pushing consumers toward convenient food solutions. Urban consumers increasingly view ready-to-eat meals as a daily necessity rather than an occasional indulgence, driving consistent order frequency.

Digital Platform Penetration and Mobile Commerce Growth

The widespread adoption of smartphones and digital payment infrastructure has enabled seamless ordering experiences. Integrated apps offering real-time tracking, digital wallets, subscription discounts, and loyalty programs have increased consumer engagement. Data analytics allows providers to forecast demand patterns and optimize delivery routes, improving profitability and service reliability.

Health-Conscious Consumption Patterns

Consumers are shifting away from traditional fast food toward balanced ready meals emphasizing nutrition transparency. Demand for organic, plant-based, and portion-controlled meals is rising rapidly. Meal delivery companies are partnering with nutritionists and fitness platforms to capture health-focused demographics.

Market Restraints

Despite strong growth, high logistics and last-mile delivery costs remain a major challenge, particularly in low-density regions. Additionally, food quality consistency and packaging sustainability concerns continue to pose operational and reputational risks. Companies must invest heavily in cold-chain logistics and eco-friendly packaging innovations to sustain long-term growth.

What are the key opportunities in the ready-to-eat meal delivery service industry?

Corporate and Institutional Meal Programs

Employers increasingly subsidize meal delivery subscriptions for hybrid and remote workers to improve productivity and employee well-being. Corporate partnerships offer stable bulk demand and recurring revenue streams. Educational institutions and healthcare facilities are also adopting centralized ready-meal delivery systems, creating large-scale B2B opportunities.

Emerging Market Expansion

Developing economies across Southeast Asia, Latin America, and the Middle East present strong untapped demand. Rising middle-class income and smartphone penetration enable rapid adoption of app-based meal delivery services. Localization strategies, affordable pricing tiers, and regional cuisine offerings allow companies to scale efficiently in these markets.

Automation and Smart Food Production

Robotic kitchens, automated portioning systems, and predictive inventory management are improving operational efficiency. Automation reduces labor dependency and enhances food consistency while enabling high-volume production scalability. Integration of IoT-enabled supply chains also reduces food waste and improves cost management.

Service Type Insights

The global meal delivery services market continues to evolve rapidly as consumer lifestyles increasingly prioritize convenience, personalization, and time efficiency. Among all service categories, subscription-based meal delivery services have emerged as the dominant segment, accounting for approximately 34% of global revenue in 2025. This leadership position is primarily driven by the growing preference for structured meal planning solutions that eliminate daily decision-making while supporting consistent dietary habits. Consumers are increasingly attracted to subscription models because they offer predictable pricing, curated menus, and personalized nutrition programs aligned with fitness, weight management, and wellness goals. The integration of artificial intelligence and data analytics into subscription platforms has enabled companies to tailor meal recommendations based on dietary preferences, allergies, calorie targets, and behavioral consumption patterns, significantly improving customer retention rates.The leading segment driver for subscription services lies in recurring consumer engagement supported by automated deliveries and loyalty ecosystems. As households seek to reduce grocery shopping frequency and food waste, subscription meal programs provide portion-controlled meals that simplify weekly planning. Furthermore, busy urban professionals and dual-income families increasingly value time-saving solutions that maintain nutritional quality without requiring cooking expertise. Subscription offerings also allow providers to forecast demand more accurately, optimize supply chains, and reduce operational inefficiencies, reinforcing profitability and long-term scalability.Additionally, evolving hybrid service models combining subscriptions with on-demand flexibility are reshaping competitive dynamics. Providers increasingly allow customers to pause subscriptions, customize weekly menus, or add instant orders, creating a seamless omnichannel consumption experience. As inflationary pressures influence food spending behavior globally, meal delivery companies are expanding tiered pricing strategies, including budget-friendly options alongside premium gourmet selections. This diversification ensures wider demographic penetration while maintaining consistent revenue streams.

Cuisine Type Insights

Cuisine preferences play a critical role in shaping consumer engagement within the meal delivery ecosystem. Local and regional cuisine dominates globally, capturing nearly 38% market share, reflecting consumers’ emotional connection to familiar flavors and cultural authenticity. The leading driver for this segment is the strong demand for comfort food that aligns with traditional dietary habits while offering modern convenience. Consumers often perceive locally inspired meals as fresher, healthier, and more trustworthy compared to unfamiliar alternatives, encouraging repeated purchases and long-term brand loyalty.The localization of menus enables providers to adapt quickly to regional taste profiles, seasonal ingredients, and cultural festivals, further strengthening adoption rates. In emerging economies, local cuisine-based meal delivery services benefit from strong acceptance among middle-income households transitioning toward digital food ordering while maintaining traditional eating patterns. Restaurants and cloud kitchens increasingly collaborate with regional chefs to preserve authenticity while achieving operational scalability.Healthy and diet-specific meals represent the fastest-growing cuisine category, driven by rising global awareness surrounding preventive healthcare, fitness culture, and nutritional transparency. Consumers are increasingly seeking meals aligned with specific dietary lifestyles such as high-protein diets, plant-based nutrition, ketogenic plans, and calorie-controlled programs. The expansion of wearable fitness technology and health tracking applications has amplified consumer focus on daily nutritional intake, encouraging adoption of structured meal solutions that simplify adherence to dietary goals.Overall, cuisine diversification enhances customer acquisition while increasing order frequency by preventing menu fatigue. Companies are increasingly investing in menu innovation teams and data-driven flavor analytics to predict emerging food trends and optimize menu rotations, ensuring sustained consumer engagement.

Platform Type Insights

Digital platforms form the technological backbone of the global meal delivery services market, with mobile application-based ordering leading the segment and accounting for approximately 62% of global transactions. The primary driver behind this dominance is the widespread adoption of smartphones combined with seamless user experiences that integrate browsing, ordering, payment, and tracking into a single interface. Mobile applications enable personalized notifications, loyalty rewards, subscription management, and AI-powered recommendations, significantly enhancing user engagement and repeat purchases.The leading segment driver for mobile platforms is convenience enhanced by ecosystem integration. Consumers increasingly rely on mobile apps not only for ordering meals but also for managing dietary plans, scheduling deliveries, and accessing exclusive discounts. Integration with digital wallets and contactless payment systems has further accelerated adoption, particularly among younger consumers comfortable with app-based transactions. Real-time order tracking and predictive delivery timelines improve transparency, strengthening consumer trust and satisfaction.Web-based platforms continue to maintain relevance, particularly for corporate clients and bulk ordering scenarios. Organizations often prefer desktop-based systems for managing employee meal programs, scheduling recurring deliveries, and coordinating large-scale catering requirements. Web platforms also provide enhanced administrative features such as invoicing, reporting, and account management tools that support enterprise-level adoption.Emerging smart-device integrations are beginning to reshape ordering behavior in developed markets. Voice assistants, connected home devices, and smart refrigerators increasingly enable automated meal reordering based on consumption patterns. These innovations represent the early stages of predictive commerce, where meal purchases occur with minimal manual input. As Internet of Things (IoT) adoption expands, platform ecosystems are expected to evolve toward fully integrated digital food management solutions.Additionally, platform providers are leveraging advanced analytics to understand consumer preferences, peak ordering times, and geographic demand clusters. These insights allow companies to optimize delivery routes, reduce operational costs, and enhance service efficiency, reinforcing the competitive advantage of technology-driven platforms.

End-User Insights

Individual consumers remain the primary demand drivers within the global meal delivery services market, contributing approximately 71% of total market revenue in 2025. The leading driver for this segment is lifestyle transformation characterized by longer working hours, urban commuting challenges, and reduced time available for meal preparation. Consumers increasingly prioritize convenience without compromising food quality, making delivered meals a routine component of daily life rather than an occasional indulgence.Young professionals, students, and single-person households represent key consumer groups fueling growth. The expansion of remote and hybrid work arrangements has also influenced consumption patterns, as individuals seek reliable meal solutions during home-based workdays. Personalized menus, flexible scheduling, and subscription discounts further enhance consumer retention.At the same time, corporate clients are emerging as the fastest-growing end-user segment as organizations integrate meal delivery services into employee welfare and productivity strategies. Companies increasingly provide subsidized meals or meal credits to improve employee satisfaction, support workplace wellness initiatives, and attract talent in competitive labor markets. Corporate meal programs also align with hybrid work models by enabling employees to receive meals at home or office locations.Educational institutions, healthcare facilities, and co-working spaces are also adopting structured meal partnerships to streamline food provisioning. This institutional demand introduces predictable high-volume orders, allowing service providers to stabilize revenue streams and optimize production planning.As workforce demographics evolve and employee expectations shift toward holistic benefits, corporate adoption is expected to accelerate further, contributing significantly to long-term market expansion.

Delivery Model Insights

Delivery infrastructure represents a critical determinant of operational efficiency and profitability within the meal delivery services market. Cloud kitchen-based delivery models hold nearly 44% market share, making them the leading delivery model globally. The primary driver behind this dominance is cost efficiency achieved through the elimination of traditional dine-in infrastructure. Cloud kitchens operate from centralized production facilities optimized exclusively for delivery, allowing companies to scale rapidly across multiple locations with reduced capital expenditure.The leading segment driver for cloud kitchens is operational scalability combined with data-driven location planning. Providers analyze demand density and consumer ordering patterns to establish strategically located kitchens that minimize delivery time while maximizing coverage areas. This approach enhances delivery efficiency and reduces logistics costs, enabling competitive pricing strategies.Cloud kitchens also allow brands to operate multiple virtual restaurant concepts from a single facility, expanding menu variety without significant additional investment. This flexibility enables rapid experimentation with new cuisines and seasonal offerings while minimizing financial risk. Furthermore, partnerships with third-party delivery platforms extend market reach and improve order volumes.Hybrid restaurant-delivery partnerships remain relevant, particularly in regions with well-established restaurant ecosystems. Traditional restaurants increasingly adopt delivery-focused operations alongside dine-in services to diversify revenue streams. These partnerships allow restaurants to leverage existing brand recognition while benefiting from digital distribution networks.Technological innovations such as route optimization algorithms, automated dispatch systems, and electric delivery fleets are further improving efficiency across delivery models. Sustainability considerations are also encouraging adoption of eco-friendly packaging and energy-efficient kitchen operations, aligning with evolving consumer expectations.

| By Service Type | By Cuisine Type | By Platform Type | By End User | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 34% of global market share in 2025, establishing itself as the most mature regional market for meal delivery services. The United States and Canada lead adoption due to high disposable incomes, advanced digital infrastructure, and well-developed logistics networks capable of supporting rapid delivery timelines. One of the primary regional growth drivers is the widespread acceptance of subscription-based meal programs among health-conscious consumers seeking structured dietary solutions. The region also benefits from a strong culture of convenience-oriented consumption, where consumers readily adopt technology-enabled services that reduce time spent on daily tasks.The expansion of premium ready meals and nutritionally optimized offerings further accelerates regional growth, particularly among urban professionals balancing demanding work schedules. Additionally, venture capital investment and innovation ecosystems continue to foster technological advancements, including AI-driven personalization and automated fulfillment systems. The presence of major delivery platforms and established cloud kitchen operators enhances competitive intensity while expanding consumer choice. Sustainability initiatives, including recyclable packaging and locally sourced ingredients, are increasingly influencing purchasing decisions across North American markets.

Europe

Europe represents nearly 26% of global market share, supported by strong adoption across the United Kingdom, Germany, France, and the Netherlands. Regional growth is primarily driven by sustainability regulations and environmentally conscious consumer behavior. European consumers demonstrate a strong preference for organic, locally sourced, and ethically produced meals, encouraging service providers to adopt transparent supply chains and eco-friendly packaging solutions.Government policies promoting reduced food waste and sustainable agriculture further contribute to market expansion. Subscription meal kits designed around seasonal ingredients resonate strongly with European households seeking both convenience and environmental responsibility. Urban density across major European cities supports efficient last-mile delivery operations, improving profitability for service providers.The increasing popularity of plant-based diets and flexitarian lifestyles also fuels demand for specialized meal offerings. Cultural diversity within Europe encourages menu innovation, allowing companies to offer regionally adapted cuisines while introducing international flavors. As digital payment adoption continues rising across the region, online ordering penetration is expected to grow steadily.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 13% during the forecast period. Rapid urbanization, expanding middle-class populations, and widespread smartphone adoption represent the primary growth drivers across countries such as China, India, Japan, and South Korea. The region’s strong digital ecosystem, supported by super-app platforms and integrated payment solutions, enables seamless meal ordering experiences.India demonstrates particularly rapid expansion driven by affordable subscription models, competitive pricing strategies, and the proliferation of cloud kitchen networks in metropolitan cities.The diversity of regional cuisines presents significant opportunities for localized menu development, enabling providers to cater to varied taste preferences across different markets. Additionally, increasing health awareness among younger consumers is driving demand for calorie-controlled and nutrition-focused meal plans. Investments in logistics infrastructure and digital payment systems further strengthen market accessibility across both developed and emerging economies within the region.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth, led primarily by the United Arab Emirates and Saudi Arabia. A major regional growth driver is the large expatriate population, which creates sustained demand for diverse international cuisines and convenient food solutions. High smartphone penetration and government-led smart-city initiatives are accelerating digital service adoption, enabling meal delivery platforms to expand rapidly.Premium meal delivery services are particularly popular in urban centers where consumers demonstrate strong purchasing power and preference for convenience-driven lifestyles. The expansion of modern retail infrastructure and digital payment adoption further supports market growth. In addition, rising tourism activity contributes to increased demand for high-quality prepared meals and subscription dining options.Across parts of Africa, improving internet connectivity and urbanization are gradually enabling the emergence of digital food delivery ecosystems. Local startups are introducing affordable meal bundles tailored to regional income levels, creating new growth opportunities while expanding food accessibility.

Latin America

Latin America continues to witness accelerating adoption of meal delivery services, with Brazil and Mexico dominating regional growth. Urbanization remains the primary growth driver, as densely populated cities create favorable conditions for efficient delivery logistics. Increasing reliance on mobile ordering platforms, supported by expanding fintech ecosystems, enables broader consumer participation in digital commerce.Economic sensitivity among consumers encourages strong demand for affordable meal bundles and value-oriented subscription plans. Providers increasingly localize menus to reflect regional culinary traditions while maintaining competitive pricing structures. Partnerships between delivery platforms and local restaurants are expanding service coverage and enhancing menu diversity.The region’s young demographic profile and growing familiarity with app-based services further support long-term growth potential. The ready-to-eat meal delivery service market is moderately fragmented, with the top five companies collectively accounting for approximately 29% of global market share. Competition centers around delivery speed, menu innovation, subscription pricing, and technology-driven customer engagement strategies. Over the past few years, companies have focused heavily on cloud kitchen expansion, AI logistics optimization, and partnerships with grocery and wellness platforms to diversify revenue streams.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Ready-To-Eat Meal Delivery Service Market

- HelloFresh SE

- DoorDash Inc.

- Uber Technologies Inc.

- Just Eat Takeaway.com N.V.

- Delivery Hero SE

- Blue Apron Holdings Inc.

- Freshly Inc.

- Sunbasket Inc.

- Gousto

- Home Chef (Kroger Co.)

- CookUnity

- Marley Spoon Group SE

- Zomato Ltd.

- Swiggy Pvt. Ltd.

- Factor75 LLC