Ready-to-Drink Cocktails Market Size

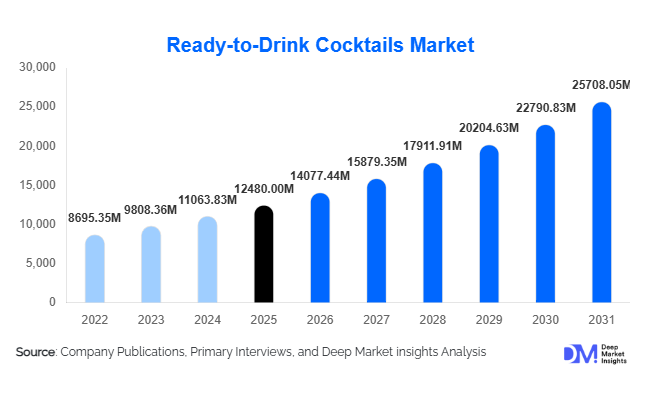

According to Deep Market Insights, the global ready-to-drink (RTD) cocktails market size was valued at USD 12,480 million in 2025 and is projected to grow from USD 14,077.44 million in 2026 to reach approximately USD 25,708.05 million by 2031, expanding at a CAGR of 12.8% during the forecast period (2026–2031). Market expansion is driven by changing consumer lifestyles, premiumization trends in alcoholic beverages, and increasing demand for convenient, bar-quality drinks that require minimal preparation. The category has transitioned from niche flavored alcoholic beverages to a mainstream premium segment supported by innovation in craft formulations, packaging formats, and flavor diversity.

Key Market Insights

- Convenience-led consumption patterns are accelerating adoption among urban consumers seeking portable and ready-made alcoholic beverages.

- Premium and craft RTD cocktails are reshaping the category, with higher alcohol quality, natural ingredients, and mixology-inspired flavors.

- North America dominates global demand, supported by strong retail distribution and brand innovation.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and westernized drinking culture.

- Low-alcohol and health-conscious formulations are gaining traction among younger consumers.

- E-commerce and direct-to-consumer alcohol sales are transforming distribution dynamics globally.

What are the latest trends in the ready-to-drink cocktails market?

Premiumization and Craft Mixology Expansion

The RTD cocktails industry is rapidly shifting toward premium offerings that replicate bar-quality experiences. Consumers increasingly prefer beverages made with real spirits, natural fruit extracts, and low artificial additives. Craft-inspired cocktails such as margaritas, mojitos, espresso martinis, and spritz variants are witnessing strong retail performance. Brands are emphasizing authenticity through small-batch production narratives and transparent ingredient sourcing. Premium price tiers are expanding faster than mass-market alternatives, reflecting consumer willingness to pay more for quality and sophistication.

Functional and Low-Alcohol Innovation

Health-conscious drinking behavior is influencing product development. Low-calorie, low-sugar, and sessionable alcohol variants are becoming mainstream across supermarkets and convenience stores. Some manufacturers are experimenting with botanical infusions, adaptogens, and natural flavor enhancements to appeal to wellness-oriented consumers. This shift aligns with moderation trends among Millennials and Gen Z consumers who seek balanced alcohol consumption without compromising taste or social experience.

What are the key drivers in the ready-to-drink cocktails market?

Convenience and On-the-Go Consumption

Urban lifestyles and evolving social occasions are major growth drivers. RTD cocktails eliminate preparation complexity while offering consistent taste profiles, making them ideal for outdoor gatherings, travel consumption, and home entertainment. Growth in single-person households and casual social drinking occasions further supports demand.

Expansion of Modern Retail and E-commerce Alcohol Sales

The expansion of organized retail channels and online alcohol delivery platforms has significantly improved product accessibility. Digital marketplaces allow brands to reach new demographics while enabling rapid product discovery through targeted marketing campaigns and subscription beverage models.

Flavor Innovation and Brand Collaborations

Continuous flavor experimentation and collaborations between spirits brands, celebrities, and beverage innovators are expanding consumer engagement. Seasonal releases and limited-edition flavors create excitement and increase repeat purchases, contributing to sustained category momentum.

What are the restraints for the global market?

Regulatory Variability Across Countries

Alcohol regulations differ widely across markets, affecting distribution, advertising, and taxation policies. Complex licensing frameworks and restrictions on alcohol promotion slow expansion in emerging economies.

Price Sensitivity in Developing Markets

Premium RTD cocktails remain relatively expensive compared to traditional alcoholic beverages such as beer or local spirits. Price-conscious consumers in developing regions may limit adoption despite growing awareness.

What are the key opportunities in the ready-to-drink cocktails industry?

Emerging Market Urbanization

Rapid urban population growth across Asia-Pacific and Latin America is creating new demand pools. Young professionals with increasing disposable income are adopting western-style social drinking habits, presenting opportunities for localized flavor innovation and affordable premium positioning.

Technology Integration in Production and Packaging

Advanced canning technologies, sustainable packaging materials, and smart labeling solutions are improving shelf life and brand differentiation. Lightweight aluminum cans and recyclable packaging support sustainability goals while reducing logistics costs.

Expansion into Non-Traditional Consumption Occasions

RTD cocktails are expanding beyond nightlife into casual dining, home consumption, music festivals, and travel retail. Partnerships with hospitality and entertainment industries are creating new consumption occasions and increasing brand visibility.

Product Type Insights

The global ready-to-drink (RTD) cocktails market continues to experience structural transformation as evolving consumer lifestyles reshape alcohol consumption patterns worldwide. Among product types, spirit-based RTD cocktails dominate the industry landscape, accounting for approximately 58% of total market share in 2025. This leadership position is primarily attributed to consumer preference for authenticity, premiumization, and recognizable base spirits such as vodka, tequila, rum, and whiskey. Modern consumers increasingly associate spirit-based beverages with bar-quality experiences, which has encouraged manufacturers to replicate traditional cocktail recipes in convenient ready-to-consume formats. The expansion of craft spirits and mixology culture has further strengthened demand, as brands emphasize natural ingredients, real spirits, and sophisticated flavor layering to appeal to discerning consumers.The leading segment driver for spirit-based RTDs is the global shift toward premium alcoholic beverages combined with convenience-oriented consumption. Consumers, particularly millennials and Gen Z adults, seek high-quality beverages without the complexity of preparation. RTD cocktails address this demand by delivering consistency, portability, and controlled portion sizes. Additionally, the rapid growth of social gatherings at home and outdoor leisure activities has accelerated adoption, positioning spirit-based RTDs as substitutes for traditional cocktails prepared in bars. Innovation in tequila-based margaritas, vodka sodas, and whiskey highballs has broadened category appeal across demographic groups.Malt-based RTD beverages continue to maintain strong relevance in price-sensitive markets, particularly where taxation structures favor malt beverages over distilled spirits. These products appeal to consumers seeking affordable alternatives while maintaining flavor familiarity similar to cocktails. Manufacturers leverage flavor innovation and localized taste preferences to sustain demand, especially in emerging economies where affordability remains a key purchasing factor.Wine-based RTD cocktails are emerging as a rapidly expanding subsegment, particularly within premium spritz and low-alcohol categories. Growth is driven by lifestyle positioning aligned with wellness trends, outdoor dining culture, and daytime consumption occasions. Wine-based spritzers appeal strongly to consumers seeking lighter drinking experiences with lower alcohol intensity and refreshing flavor profiles. As social norms increasingly favor moderation, wine-based RTDs are gaining traction among health-conscious consumers and new entrants to alcoholic beverages.Overall, product diversification across spirit, malt, and wine bases reflects the industry’s strategy to capture multiple price tiers and consumption occasions. Continuous innovation in ingredient sourcing, clean labeling, and functional flavor additions is expected to further enhance product differentiation and sustain long-term category expansion.

Packaging Format Insights

Packaging innovation remains a critical competitive factor shaping purchasing behavior and supply chain efficiency within the global RTD cocktails market. Aluminum cans lead packaging adoption, accounting for nearly 67% share of the 2025 market. The dominance of cans is driven by a combination of portability, sustainability advantages, lightweight logistics, and superior product preservation. Aluminum packaging protects beverages from light and oxygen exposure, ensuring consistent taste quality while extending shelf life. These attributes align closely with consumer expectations for convenience and environmental responsibility.The leading segment driver for canned RTD cocktails is the convergence of sustainability initiatives and on-the-go consumption trends. Beverage companies increasingly prioritize recyclable materials to meet regulatory pressures and corporate environmental targets. Aluminum’s high recycling rate and reduced transportation emissions compared to glass packaging have made it the preferred format across both developed and emerging markets. Additionally, canned beverages are well suited for outdoor activities, music festivals, sporting events, and travel consumption, significantly expanding usage occasions.Bottled RTD cocktails continue to maintain a strong presence within premium retail channels, luxury hospitality environments, and gifting occasions. Glass packaging enhances perceived product value and supports premium branding strategies through aesthetic differentiation. High-end RTD offerings often utilize bottles to communicate craftsmanship and authenticity, appealing to consumers willing to pay higher prices for elevated drinking experiences.Emerging packaging formats such as multi-serve pouches, bag-in-box solutions, and draft-style kegs are gaining adoption within hospitality and event-driven environments. These formats allow bars and restaurants to reduce preparation time while maintaining consistent drink quality. Furthermore, large-format packaging improves operational efficiency by minimizing waste and simplifying inventory management.Advancements in smart labeling, resealable designs, and temperature-sensitive packaging technologies are expected to enhance consumer engagement while improving product usability. As sustainability regulations tighten globally, packaging innovation will remain central to brand differentiation and long-term market competitiveness.

Flavor Profile Insights

Flavor innovation plays a pivotal role in driving consumer engagement and repeat purchases within the RTD cocktails industry. Citrus-based cocktails represent the leading flavor category, capturing around 34% market share in 2025. The enduring popularity of citrus flavors stems from their universal appeal, refreshing taste characteristics, and strong association with classic cocktails such as margaritas, lemon spritzes, and citrus vodka sodas. These flavors provide a balanced sensory experience that appeals to both experienced drinkers and new consumers entering the alcoholic beverage category.The leading segment driver for citrus flavors is their versatility across cultures and consumption occasions. Citrus profiles complement various base spirits while delivering perceived freshness and lower sweetness intensity compared to dessert-style beverages. Additionally, citrus flavors align with wellness-oriented preferences, as consumers increasingly associate them with natural ingredients and lighter drinking experiences.Tropical flavors are witnessing rapid expansion, particularly among younger demographics seeking novel and experiential beverages. Mango, pineapple, passionfruit, and coconut variants reflect global culinary influences and vacation-inspired consumption trends. Beverage brands leverage tropical flavors to create emotional connections associated with leisure, travel, and social experiences. This trend is amplified by social media marketing, where visually appealing beverages contribute to brand discovery and consumer engagement.Herbal and botanical flavors are gaining traction within premium segments as consumers seek more sophisticated taste profiles. Ingredients such as rosemary, basil, elderflower, and lavender introduce complexity traditionally associated with craft cocktails. These flavors resonate with consumers interested in artisanal products and mixology-inspired beverages. Premium botanical RTDs also align with the broader premiumization trend shaping alcoholic beverage markets worldwide.Flavor innovation increasingly incorporates regional ingredients and seasonal limited editions, enabling brands to maintain consumer interest while responding to localized taste preferences. As experimentation becomes central to purchasing behavior, continuous flavor diversification will remain a major driver of category growth.

Alcohol Content Insights

Alcohol content segmentation reflects shifting global attitudes toward responsible drinking and lifestyle balance. Standard ABV products ranging between 5% and 8% dominate the market, accounting for approximately 49% share. These products offer an optimal balance between flavor intensity and sessionability, allowing consumers to enjoy multiple servings without excessive alcohol intake. Standard ABV beverages closely replicate traditional cocktail strength while maintaining accessibility for casual consumption occasions.The leading segment driver for standard ABV RTDs is the demand for social drinking experiences that prioritize moderation without sacrificing taste authenticity. Consumers increasingly seek beverages suitable for extended social gatherings, home entertainment, and daytime occasions. Standard ABV formulations provide familiarity while supporting responsible consumption patterns.Low-ABV offerings represent the fastest-growing category, fueled by global wellness movements and increased awareness surrounding alcohol intake. Younger consumers, in particular, are embracing mindful drinking habits, driving demand for lighter beverages that support healthier lifestyles. Manufacturers are investing heavily in flavor optimization technologies to ensure reduced alcohol content does not compromise taste quality.High-ABV RTDs remain relevant within niche segments targeting consumers seeking stronger cocktail experiences in convenient formats. However, growth within this category is comparatively moderate as regulatory scrutiny and health-conscious behaviors encourage moderation trends.The expansion of alcohol-content diversity demonstrates the industry’s adaptation to evolving consumer expectations. Flexible ABV ranges allow brands to capture multiple consumption occasions, from casual daytime refreshment to evening social gatherings, strengthening overall market resilience.

Distribution Channel Insights

Distribution channels significantly influence accessibility, brand visibility, and consumer purchasing behavior within the RTD cocktails market. Off-trade retail channels, including supermarkets, hypermarkets, liquor stores, and convenience outlets, account for nearly 72% of global sales. Retail dominance is supported by widespread availability, promotional pricing strategies, and growing consumer preference for at-home consumption.The leading segment driver for off-trade retail growth is the structural shift toward home-based socialization and entertainment. Consumers increasingly purchase RTD cocktails as convenient alternatives to bar visits, particularly during weekends, celebrations, and casual gatherings. Retailers benefit from impulse purchases driven by attractive packaging and seasonal promotions.Online alcohol retail represents the fastest-growing distribution segment, supported by digital transformation and e-commerce expansion. Consumers value the convenience of home delivery, expanded product selection, and access to premium or imported brands unavailable in local stores. Subscription models and personalized recommendations further enhance customer engagement, encouraging repeat purchases.On-trade channels, including bars, restaurants, and hotels, are experiencing renewed growth as hospitality sectors recover globally. Establishments increasingly adopt RTD cocktails to streamline operations, reduce labor costs, and maintain consistent drink quality during peak hours. RTDs also enable venues to expand cocktail menus without requiring specialized bartending expertise.Hybrid distribution strategies combining physical retail, online platforms, and hospitality partnerships are becoming essential for brand expansion. As digital commerce continues to evolve, omnichannel distribution will remain a cornerstone of market growth.

End-Use Analysis

End-use dynamics highlight how changing social behaviors are reshaping alcohol consumption worldwide. Household consumption represents the largest end-use segment, driven by rising interest in home entertainment and casual socialization. Consumers increasingly recreate bar-like experiences at home, supported by premium RTD offerings that eliminate preparation complexity. The affordability and convenience of ready-to-drink cocktails make them ideal for small gatherings, celebrations, and everyday leisure occasions.The leading segment driver for household consumption is the long-term behavioral shift toward personalized entertainment experiences. Streaming culture, home dining trends, and flexible work lifestyles have encouraged consumers to invest more in at-home leisure products, including premium beverages.Hospitality and foodservice sectors are recovering strongly, contributing significantly to incremental demand. Bars and restaurants utilize RTD cocktails to enhance operational efficiency while ensuring consistent taste delivery. These beverages reduce preparation time, minimize ingredient waste, and allow venues to maintain profitability despite labor shortages.Travel retail and event-based consumption are emerging as high-growth applications. Airports, music festivals, sporting events, and outdoor venues increasingly offer canned cocktails due to portability and regulatory convenience. These environments expose consumers to new brands, supporting category awareness and trial purchases.Export-driven demand is expanding as multinational beverage companies strengthen cross-border distribution networks. Premium imported RTD cocktails carry aspirational value in emerging markets, particularly across Asia-Pacific, where international brands symbolize lifestyle sophistication and global cultural influence.

| By Product Type | By Packaging Format | By Distribution Channel | By Alcohol Content | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 38% of global market share in 2025, maintaining its position as the largest regional market for RTD cocktails. The United States represents the primary growth engine, contributing nearly 30% of global consumption. High disposable income levels, mature retail infrastructure, and strong consumer openness toward beverage innovation support sustained regional dominance.Regional growth is driven by several structural factors, including rapid premiumization of alcoholic beverages, expansion of craft distilleries, and widespread acceptance of canned cocktails across mainstream retail. Regulatory flexibility allowing spirit-based RTDs to enter broader distribution channels has significantly accelerated market penetration. Additionally, strong marketing investments and celebrity-backed beverage brands continue to stimulate consumer interest.The rise of health-conscious drinking habits has encouraged innovation in low-calorie and low-ABV formulations, aligning with wellness-oriented lifestyles prevalent across North America. Canada is witnessing steady growth driven by premium product adoption, evolving provincial alcohol policies, and increasing demand for convenient beverage formats suited to outdoor recreation and seasonal consumption.

Europe

Europe represents approximately 26% of global market share, supported by diverse drinking cultures and strong premium beverage traditions. Key markets include the United Kingdom, Germany, France, and Italy, where RTD cocktails increasingly complement established wine and beer consumption patterns.Regional growth drivers include the expansion of spritz culture, rising festival participation, and growing acceptance of canned beverages in social settings. Consumers across Europe increasingly value convenience without compromising quality, encouraging adoption of premium RTD offerings inspired by classic European aperitif traditions.The United Kingdom remains a leading innovation hub, characterized by rapid product launches and experimentation with botanical flavors and artisanal ingredients. Sustainability regulations across the European Union also encourage aluminum packaging adoption, reinforcing canned format growth. Additionally, tourism recovery and outdoor dining culture continue to stimulate seasonal demand for ready-to-consume cocktails.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 15% CAGR. The region’s growth trajectory is supported by rising urbanization, expanding middle-class populations, and increasing Western cultural influence on consumption habits. China, Japan, South Korea, Australia, and India represent key growth contributors.Japan’s long-established canned cocktail culture provides market maturity and technological leadership in flavor innovation and packaging efficiency. Meanwhile, emerging markets such as India and Southeast Asia demonstrate strong demand driven by young urban consumers seeking modern lifestyle beverages. Rapid expansion of organized retail and e-commerce platforms significantly improves product accessibility across metropolitan areas.Regional growth is further supported by rising disposable incomes, premium brand aspirations, and growing participation in nightlife and social entertainment activities. International beverage companies are actively investing in localized flavor development to cater to regional taste preferences, accelerating market penetration across diverse consumer segments.

Latin America

Latin America accounts for nearly 6% of global market share, led primarily by Brazil and Mexico. The region benefits from strong cocktail heritage and increasing modernization of retail infrastructure. RTD cocktails are gaining popularity among younger consumers seeking convenience and affordability.Regional growth drivers include innovation in tequila-based RTDs, expansion of modern supermarket chains, and rising urban populations. Social gatherings and outdoor celebrations remain integral to cultural lifestyles, creating favorable consumption environments for portable beverage formats. Economic recovery and growing tourism activity further support demand expansion.

Middle East & Africa

The Middle East & Africa region holds approximately 5% market share, with growth concentrated in South Africa and tourism-driven markets such as the United Arab Emirates. Despite regulatory limitations in certain countries, premium imports and hospitality sector expansion continue to drive consumption.Regional growth is supported by increasing international tourism, luxury hospitality investments, and expanding expatriate populations. Premium RTD cocktails appeal strongly to consumers seeking convenient yet sophisticated beverage options within licensed venues. South Africa’s established wine and spirits industry provides a foundation for local RTD production, while urbanization and modern retail development enhance accessibility.As tourism rebounds and entertainment infrastructure expands across key markets, RTD cocktails are expected to gain further visibility, supporting steady long-term regional growth despite regulatory complexities.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Ready-to-Drink Cocktails Market

- Diageo plc

- Pernod Ricard SA

- Bacardi Limited

- Brown-Forman Corporation

- Constellation Brands Inc.

- Anheuser-Busch InBev

- Molson Coors Beverage Company

- Beam Suntory Inc.

- Campari Group

- Asahi Group Holdings Ltd.

- Kirin Holdings Company

- Halewood Artisanal Spirits

- Manchester Drinks Company

- High Noon Spirits Company

- CUTWATER Spirits