Rapid Food Safety Testing Market Size

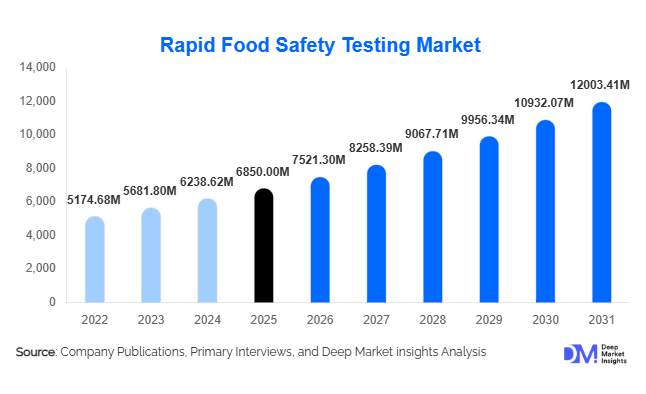

According to Deep Market Insights, the global rapid food safety testing market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,521.30 million in 2026 to reach USD 12,003.41 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). Market growth is primarily driven by stringent global food safety regulations, rising incidences of foodborne illnesses, and increasing demand for faster, high-throughput testing solutions across food manufacturing and export supply chains.

Key Market Insights

- PCR-based rapid testing technologies dominate the market, accounting for nearly 34% of total revenue in 2025 due to superior sensitivity and regulatory acceptance.

- Test kits and consumables represent the largest product segment, contributing approximately 42% of overall revenue, supported by recurring purchase cycles.

- North America leads the global market with around 32% share in 2025, driven by strict regulatory enforcement and advanced automation adoption.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR due to export-driven food manufacturing growth in China and India.

- Food manufacturers & processors account for nearly 46% of total demand, reflecting rising in-house quality control investments.

- Digital integration and AI-enabled data platforms are reshaping compliance management, enabling predictive risk monitoring and traceability.

What are the latest trends in the rapid food safety testing market?

Shift Toward Molecular and Multiplex Testing

Rapid food safety testing is increasingly transitioning from conventional culture-based methods to molecular diagnostics such as PCR and isothermal amplification technologies. Multiplex PCR platforms capable of detecting multiple pathogens simultaneously are gaining traction, particularly in meat and dairy processing facilities. These systems reduce turnaround time from days to hours, allowing faster product release and minimizing recall risks. Automation of sample preparation and integration with laboratory information management systems (LIMS) are further improving throughput and data accuracy, making molecular testing the gold standard across regulated markets.

Portable and On-Site Testing Solutions

The demand for portable biosensors and handheld testing devices is rising significantly. Food manufacturers are adopting on-site testing systems to decentralize laboratory operations and shorten decision cycles. Compact PCR units and lateral flow assays are being deployed at processing plants, warehouses, and ports of entry. This trend is particularly strong in export-driven regions where real-time compliance verification reduces shipment delays. Integration of cloud-based reporting tools is also enhancing supply chain transparency and traceability.

What are the key drivers in the rapid food safety testing market?

Stringent Regulatory Frameworks

Global food safety regulations, such as preventive control mandates and hazard analysis requirements, are compelling food producers to implement routine and batch-level testing. Export-oriented industries must comply with international standards, further increasing testing frequency. Government enforcement actions and heavy penalties for non-compliance are reinforcing investment in rapid testing technologies.

Rising Foodborne Illness Outbreaks

Increased reporting of contamination incidents has heightened consumer awareness and corporate accountability. High-profile recalls in meat, dairy, and processed food segments are driving proactive adoption of rapid pathogen detection technologies. Companies are prioritizing early detection to protect brand reputation and reduce financial losses associated with recalls.

What are the restraints for the global market?

High Capital Investment

Advanced PCR systems and automated analyzers require significant upfront investment, limiting adoption among small and mid-sized food processors, particularly in developing regions.

Technical Skill Gaps

Operating molecular diagnostic platforms demands skilled personnel. Inadequate technical expertise in emerging economies can slow the deployment of advanced testing infrastructure.

What are the key opportunities in the rapid food safety testing industry?

Export-Driven Compliance Testing

Emerging economies in the Asia-Pacific and Latin America are strengthening food testing infrastructure to meet import requirements from North America and Europe. Investments in accredited laboratories and rapid testing kits present strong opportunities for global players to expand regional footprints.

Integration of AI and Data Analytics

The integration of AI-powered analytics platforms with rapid testing systems offers predictive contamination monitoring and automated compliance reporting. Cloud-based dashboards and blockchain-enabled traceability are expected to create recurring SaaS revenue streams and enhance customer retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7521.30 Million |

| Market Size in 2031 | USD 12003.41 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

PCR-based rapid testing leads the global rapid food safety testing market, accounting for approximately 34% of total revenue in 2025. Its dominance is primarily driven by superior sensitivity, high specificity, and strong validation under international regulatory frameworks for pathogen detection. Food manufacturers increasingly prefer PCR platforms because they significantly reduce detection time, from 48–72 hours in traditional culture methods to less than 8 hours, thereby accelerating product release cycles and minimizing recall risks. Moreover, multiplex PCR systems capable of detecting multiple pathogens in a single run are gaining strong adoption across meat, poultry, and dairy processing facilities. Automation compatibility and integration with laboratory information management systems (LIMS) further reinforce PCR’s leadership position.

Immunoassay-based methods remain widely adopted, particularly in small- and mid-scale processing facilities, due to their cost-effectiveness, operational simplicity, and minimal training requirements. Lateral flow assays and ELISA kits are extensively used for routine screening of allergens and pathogens. Meanwhile, biosensor-based detection systems are emerging as a high-growth segment, supported by demand for portable, real-time monitoring solutions in decentralized and on-site testing environments. Chromatography-based rapid systems, including HPLC and GC platforms with rapid detection modules, continue to dominate chemical contaminant analysis, particularly for pesticide residues, veterinary drugs, and mycotoxins in export-oriented agricultural commodities.

Product Type Insights

Test kits and consumables dominate the market, contributing nearly 42% of total revenue in 2025. The leading position of this segment is driven by its recurring demand model, as food manufacturers conduct routine batch-level and periodic compliance testing. The consumable-intensive nature of rapid diagnostics ensures stable and predictable revenue streams for manufacturers. Increasing regulatory mandates for frequent pathogen and allergen testing further strengthen the growth trajectory of this segment.

Instruments and analyzers represent a high-value segment characterized by strong profit margins, particularly automated PCR platforms and integrated detection systems. Food processors are investing in next-generation instruments to enhance throughput, reduce manual error, and improve traceability. Additionally, software and data management platforms are gaining traction as laboratories adopt digital compliance tools. Cloud-based reporting systems, blockchain-enabled traceability modules, and AI-driven analytics dashboards are becoming integral to modern food safety ecosystems, supporting predictive contamination monitoring and regulatory documentation.

Contaminant Type Insights

Pathogen testing accounts for approximately 38% of total market revenue in 2025, making it the largest contaminant segment. The leadership of pathogen testing is driven by mandatory regulatory requirements for detecting Salmonella, Listeria, and E. coli across meat, poultry, dairy, and ready-to-eat foods. Rising global awareness of foodborne illnesses and strict zero-tolerance policies for certain pathogens continue to fuel growth in this segment.

Allergen testing is expanding steadily due to stricter food labeling laws and heightened consumer awareness regarding allergenic ingredients. Mycotoxin and pesticide residue testing remain critical in cereals, grains, fruits, and vegetables, particularly for export markets where compliance with maximum residue limits (MRLs) is mandatory. Increasing global trade in agricultural commodities is expected to sustain strong demand for chemical contaminant testing technologies.

End-Use Insights

Food manufacturers and processors represent the largest end-use segment, contributing nearly 46% of total demand in 2025. The segment’s dominance is driven by rising in-house laboratory investments aimed at improving quality assurance, reducing recall costs, and ensuring real-time compliance with domestic and international standards. Large-scale processors increasingly prefer integrated rapid testing systems to streamline production workflows and minimize operational downtime.

Contract testing laboratories are the fastest-growing segment, expanding at over 11% CAGR, supported by outsourcing trends among small and mid-sized producers that lack advanced in-house capabilities. Government and regulatory laboratories maintain consistent demand, particularly for import-export compliance, border inspections, and national surveillance programs. Retail chains and private-label brands are also strengthening internal quality testing protocols, further contributing to incremental market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Rapid Food Safety Testing Market Segmentations

By Technology

- PCR-Based Rapid Testing

- Immunoassay-Based Testing

- Chromatography-Based Rapid Systems

- Biosensor-Based Detection Systems

- Isothermal Nucleic Acid Amplification

- Spectroscopy-Based Rapid Methods

By Product Type

- Test Kits

- Reagents & Consumables

- Instruments & Analyzers

- Software & Data Management Platforms

By Contaminant Type

- Pathogens

- Allergens

- Mycotoxins

- Pesticide Residues

- Veterinary Drug Residues

- Genetically Modified Organisms (GMOs)

- Heavy Metals & Chemical Contaminants

By End-Use

- Food Manufacturers & Processors

- Contract Testing Laboratories

- Government & Regulatory Laboratories

- Retail & Food Service Chains

By Food Tested

- Meat, Poultry & Seafood

- Dairy Products

- Processed & Packaged Foods

- Fruits & Vegetables

- Cereals & Grains

- Beverages

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, with the United States accounting for nearly 26% of the total demand. Regional growth is driven by stringent enforcement of preventive food safety regulations, high consumer awareness, and advanced laboratory automation infrastructure. Strong presence of leading market players and early adoption of molecular diagnostic technologies further support market expansion. Canada also contributes significantly due to its robust meat export sector and harmonized food safety standards with the U.S.

Europe

Europe accounts for around 28% of global revenue, with Germany, France, the UK, Italy, and Spain serving as key contributors. Growth in this region is supported by harmonized European Union food safety regulations, mandatory traceability systems, and strict allergen labeling directives. High consumer preference for organic and clean-label products further increases testing frequency. Additionally, Europe’s strong export base for processed foods and agricultural commodities drives sustained demand for chemical residue and mycotoxin testing solutions.

Asia-Pacific

Asia-Pacific represents nearly 25% of the global market and is the fastest-growing region, expanding at over 11% CAGR. China contributes approximately 10% of global revenue, driven by export-oriented food manufacturing and government-led food safety modernization programs. India is emerging as the fastest-growing country with more than 12% CAGR, supported by expanding domestic food processing capacity, regulatory reforms, and public investment in laboratory infrastructure. Japan and Australia maintain stable demand due to high-quality standards and advanced testing capabilities.

Latin America

Latin America accounts for about 8% of global demand, led by Brazil and Mexico. Regional growth is primarily driven by strong meat and poultry exports to North America, Europe, and Asia. Increasing compliance requirements for international trade and the modernization of food safety laboratories are strengthening rapid testing adoption. Governments are also enhancing inspection systems to improve export competitiveness.

Middle East & Africa

The Middle East & Africa region contributes around 7% of global revenue. Growth is driven by increasing food import volumes in GCC countries, where strict border inspection and quality control protocols are being implemented. Investments in food security programs and laboratory infrastructure upgrades are supporting market expansion. South Africa serves as a regional hub due to its established food processing sector and export activities across the African continent.

Key Players in the Rapid Food Safety Testing Market

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- 3M

- Danaher Corporation

- Merck KGaA

- Neogen Corporation

- PerkinElmer

- Shimadzu Corporation

- Agilent Technologies

- QIAGEN

- bioMérieux

- Eurofins Scientific

- Romer Labs

- Idexx Laboratories

- Mérieux NutriSciences