Pyrethrum Market Size

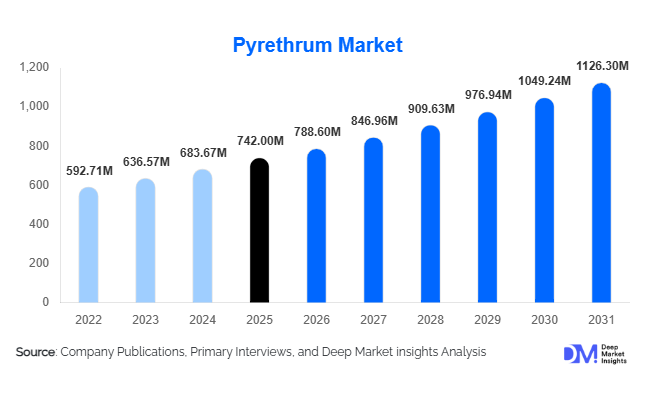

According to Deep Market Insights, the global pyrethrum market size was valued at USD 742 million in 2025 and is projected to grow from USD 788.6 million in 2026 to reach USD 1,126.30 million by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The pyrethrum market growth is primarily driven by increasing demand for bio-based insecticides, rising regulatory restrictions on synthetic pesticides, and expanding adoption of environmentally safe crop protection solutions across agriculture, public health, and household pest control applications.

Key Market Insights

- Bio-based crop protection demand is accelerating globally, positioning pyrethrum as a preferred natural insecticide alternative to synthetic chemicals.

- Agriculture remains the dominant application segment, supported by growth in organic farming and residue-free food production requirements.

- Asia-Pacific leads consumption growth, driven by expanding agricultural productivity initiatives and rising pest-control demand in India and China.

- Public health pest control programs are increasing adoption of pyrethrum-based formulations due to low toxicity to humans and rapid biodegradability.

- Supply concentration in East Africa, particularly Kenya and Tanzania, continues to influence global pricing and trade dynamics.

- Technological innovation in extraction and formulation is improving product stability, shelf life, and effectiveness across multiple end-use industries.

What are the latest trends in the pyrethrum market?

Shift Toward Natural and Residue-Free Crop Protection

The agricultural industry is witnessing a significant transition toward natural pesticides as food safety regulations tighten worldwide. Pyrethrum-derived insecticides are gaining traction due to their rapid knockdown effect on insects combined with minimal environmental persistence. Organic certification standards across Europe and North America increasingly favor plant-based solutions, encouraging farmers to replace synthetic chemical pesticides. Retailers and food exporters are also demanding low-residue crop inputs, further strengthening pyrethrum adoption across high-value horticulture and specialty crops.

Advancements in Botanical Extraction Technologies

Manufacturers are investing in advanced solvent extraction and purification technologies to enhance pyrethrin concentration and formulation consistency. Microencapsulation techniques are enabling controlled-release insecticides that improve field performance while reducing application frequency. These technological improvements are expanding pyrethrum use beyond traditional agriculture into urban pest control, veterinary care, and stored grain protection. Innovation is also helping stabilize supply chains by improving yield efficiency from cultivated chrysanthemum flowers.

What are the key drivers in the pyrethrum market?

Rising Organic Agriculture Adoption

The expansion of certified organic farmland globally is a major growth catalyst. Governments and consumers increasingly favor chemical-free farming practices, creating sustained demand for botanical pesticides. Pyrethrum’s natural origin and compliance with organic farming standards make it one of the most widely accepted insecticidal solutions in organic crop protection systems.

Stricter Regulations on Synthetic Pesticides

Regulatory bodies across Europe and North America are restricting or banning several synthetic pesticide classes due to environmental and health concerns. These regulatory shifts are pushing agrochemical companies and farmers toward safer alternatives. Pyrethrum benefits directly from this transition as it offers effective pest control with lower ecological impact.

Expansion of Public Health Vector Control Programs

Global mosquito and vector control initiatives aimed at reducing malaria, dengue, and other vector-borne diseases are increasing demand for fast-acting insecticides. Pyrethrum formulations are widely used in household sprays, aerosols, and community fumigation programs due to their rapid insect knockdown properties and relative safety for indoor applications.

What are the restraints for the global market?

Supply Dependency on Limited Cultivation Regions

Pyrethrum production is geographically concentrated, primarily in East Africa. Climate variability, crop disease, and agricultural labor challenges can disrupt supply stability, leading to price volatility. This dependency increases risk exposure for downstream manufacturers.

Higher Cost Compared to Synthetic Alternatives

Natural extraction processes make pyrethrum-based products more expensive than synthetic pesticides. Price-sensitive farmers in developing economies may continue using conventional chemicals, limiting rapid adoption despite environmental advantages.

What are the key opportunities in the pyrethrum industry?

Expansion into Integrated Pest Management (IPM)

Integrated pest management strategies increasingly combine biological, cultural, and chemical controls. Pyrethrum fits well within IPM frameworks due to its biodegradability and compatibility with beneficial insects when properly applied. Agricultural advisory programs promoting IPM adoption are expected to create long-term demand opportunities.

Growth in Emerging Agricultural Economies

Countries across Southeast Asia, Latin America, and Africa are modernizing agricultural practices to boost productivity and export competitiveness. As these regions expand fruit, vegetable, and plantation crop production, demand for residue-safe pest control solutions is rising significantly. Pyrethrum producers can benefit by establishing localized formulation facilities and distribution networks.

Innovation in Household and Pet Care Products

Demand for plant-based pest control solutions in household insect sprays, pet shampoos, and livestock treatments is growing rapidly. Consumer preference for natural ingredients is encouraging FMCG and veterinary companies to incorporate pyrethrum-based formulations, creating diversification opportunities beyond agriculture.

Product Type Insights

Pyrethrin extract concentrates are the most significant segment in the global pyrethrum market, accounting for nearly 46% of the market share in 2025. These concentrates are highly valued for their effectiveness against a wide range of agricultural, household, and public health pests. Their ability to deliver rapid knockdown of insects while remaining environmentally friendly makes them the preferred choice for both commercial and small-scale applications. Standardized extracts allow for consistent active ingredient concentrations, which is critical for manufacturers producing aerosols, emulsifiable concentrates, and sprayable formulations. Technological advancements in extraction methods, including supercritical CO2 extraction, ultrafiltration, and microemulsion development, have improved yield, purity, and stability, enabling higher adoption in global markets. The segment’s leadership is reinforced by growing investments in industrial-scale processing facilities, mechanized harvesting, and quality control programs that ensure consistency and regulatory compliance. Sustainability trends, rising consumer awareness of chemical exposure, and the global shift toward botanical pesticides are also key factors that continue to support the dominance of pyrethrin extract concentrates over synthetic pyrethroids.In addition, product innovation is a major driver for this segment. Companies are focusing on developing concentrated formulations that allow for lower application rates without compromising efficacy. Research in enhancing residual activity and environmental stability is helping manufacturers expand applications in tropical and high-humidity regions, where product degradation can otherwise be rapid. The increasing convergence of agricultural and household insecticide markets also opens opportunities for multi-use concentrates that cater to both sectors, further consolidating the segment’s leading position.

Application Insights

Agricultural insecticides remain the leading application segment, accounting for nearly 52% of the global market in 2025. Market growth is driven by the increasing adoption of organic and sustainable farming practices, coupled with stricter pesticide residue regulations in export-oriented crops. Pyrethrin’s rapid degradation, low mammalian toxicity, and broad-spectrum efficacy make it ideal for high-value crops such as fruits, vegetables, and greenhouse produce. Farmers increasingly rely on pyrethrin to meet residue standards required by importing countries, particularly in Europe and North America. Moreover, integrated pest management (IPM) programs favor pyrethrin due to its selective activity, which preserves beneficial insects while targeting key pests.Beyond conventional crop protection, pyrethrin is being increasingly utilized in livestock management, post-harvest storage, and grain protection, where pest infestations can lead to significant economic losses. Expansion in high-value horticulture, vertical farming, and greenhouse cultivation has further amplified the demand for pyrethrin, as these systems require fast-acting, low-residue, and environmentally safe solutions. Research initiatives in nano-formulations and synergistic blends with other biopesticides are opening new avenues for application, allowing growers to achieve enhanced pest control while complying with evolving environmental regulations. The growing consumer preference for residue-free produce, combined with stringent government monitoring programs, continues to position agricultural insecticides as the primary growth engine for the pyrethrum market.

Formulation Insights

Liquid formulations hold the largest share globally, with approximately 58% of the market in 2025. The ease of application, compatibility with modern spraying systems, and flexibility in dilution ratios make liquid pyrethrin formulations particularly attractive to large-scale growers. Advanced liquid formulations, including microemulsions and water-dispersible concentrates, offer improved stability, shelf life, and field performance, which facilitates adoption across diverse climatic conditions and crop types.Liquid concentrates also enable precise dosing, reducing overuse and minimizing environmental impact. They are readily integrated into automated spraying systems, drones, and other precision agriculture tools, which are increasingly being used in developed and emerging markets. The liquid formulation segment benefits from continuous innovation aimed at increasing residual activity, enhancing pest penetration, and improving ease of storage and transport. These advances have expanded the utility of pyrethrin in complex farming systems, greenhouse cultivation, and urban pest management, strengthening its position as the most widely used formulation type globally.

Source Insights

Natural pyrethrum derived from chrysanthemum flowers dominates supply, accounting for nearly 72% of market demand. The preference for naturally sourced pyrethrum is largely influenced by regulatory support for botanical insecticides, consumer demand for organic produce, and environmental sustainability considerations. Africa, particularly Kenya and Tanzania, remains the primary cultivation hub, producing high-quality pyrethrum flowers for global export. Mechanized harvesting, improved agronomic practices, and investment in post-harvest handling and storage have increased supply reliability, allowing manufacturers to maintain consistent extract quality year-round.Research in hybrid chrysanthemum varieties and controlled cultivation environments is further improving yields and active ingredient concentrations. Natural pyrethrum’s biodegradability and low environmental persistence are critical advantages in regions with strict environmental regulations. The strong regulatory preference for botanical insecticides and organic certification requirements in developed markets continue to reinforce demand for natural pyrethrum over synthetic alternatives. Additionally, the adoption of best practices in flower processing and extraction is enabling manufacturers to produce higher-grade pyrethrin concentrates, meeting the evolving standards of agrochemical and public health applications globally.

Distribution Channel Insights

Direct B2B sales to agrochemical manufacturers dominate distribution channels, capturing roughly 49% of global market share. Long-term contracts, bulk procurement agreements, and strategic alliances between extractors and formulation companies are driving this trend. Manufacturers prefer direct sourcing to ensure consistent quality, traceability, and regulatory compliance, particularly for export-oriented agriculture. The B2B channel also allows better supply chain management, reduces dependency on intermediaries, and ensures predictable raw material costs.While direct sales dominate, regional distributors and wholesalers are growing in importance, particularly in emerging markets with fragmented farming systems. E-commerce and digital marketplaces are slowly entering the pyrethrum trade ecosystem, enabling smaller producers to access global buyers. Investments in logistics, cold-chain storage, and packaging innovations are helping maintain product stability during transport, further enhancing the reliability of distribution channels. As regulatory standards tighten and traceability requirements increase, B2B procurement is expected to continue dominating the market while alternative channels gain incremental market share.

End-Use Analysis

Agriculture remains the largest end-use sector, fueled by steady expansion in organic, specialty crop, and greenhouse farming. The global organic farming sector continues growing at over 8% annually, providing a consistent demand base for pyrethrin. Public health applications are among the fastest-growing end-use segments, particularly in Asia and Africa, where mosquito-borne diseases necessitate effective vector-control programs. Urbanization, rising disposable incomes, and heightened consumer awareness of chemical exposure risks are driving household insecticide adoption. Export-driven horticulture further reinforces demand, as producers adopt residue-compliant botanical pesticides to meet stringent European and North American standards.Emerging applications in livestock protection, stored grain preservation, and indoor pest control diversify the market, providing additional revenue streams. Technological innovations such as drone-based pesticide delivery, precision spraying systems, and integrated pest monitoring tools enhance efficiency, reduce labor costs, and improve environmental compliance. The convergence of agricultural and household markets presents opportunities for multi-use pyrethrin formulations, further expanding the end-use landscape.

| By Product Type | By Application | By Source | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 34% of the global market in 2025, led by China, India, Japan, and Australia. India is rapidly adopting pyrethrin due to government-backed organic farming initiatives, sustainable agriculture policies, and increasing consumer demand for residue-free produce. Smallholder farmers are increasingly integrating pyrethrin into IPM strategies, supported by training and extension services. China’s demand is driven by intensive greenhouse cultivation and export-oriented vegetable production, where residue compliance is essential. Japan and Australia are investing in advanced extraction and formulation technologies to support domestic and export markets. The region benefits from a growing network of commercial greenhouses, vertical farms, and agro-industrial clusters. Asia-Pacific continues to be the fastest-growing market, with growth exceeding 8% annually, propelled by regulatory support, rising consumer awareness, and expansion of organic farming and public health initiatives.

North America

North America held nearly 24% of the market share in 2025, with the United States as the dominant consumer. Regional growth is driven by strong organic food demand, strict pesticide regulations, and widespread use of household insecticides. Canada is witnessing steady adoption in greenhouse agriculture and vector-control programs. Technological advancements in spraying equipment, liquid formulations, and precision agriculture enhance efficiency and reduce environmental impact. Strategic sourcing from African and Asian pyrethrum producers ensures supply consistency for large-scale manufacturing. Regulatory support, combined with consumer preference for safe and residue-free products, underpins long-term market expansion.

Europe

Europe demonstrates strong demand, especially in Germany, France, Italy, and Spain, supported by bans on certain synthetic pesticides and incentives for sustainable agriculture. Organic certification standards, environmental compliance requirements, and consumer awareness drive the adoption of botanical insecticides. Liquid formulations and standardized concentrates are preferred for their ease of application and reliability. European growers increasingly integrate pyrethrin into IPM and precision farming systems. Export-oriented horticulture and high-value crop production further reinforce regional growth. Government support for eco-friendly agriculture and residue-free produce contributes to the sustained demand for pyrethrin-based products across the region.

Middle East & Africa

Africa functions as both a key producer and emerging consumer. Kenya and Tanzania dominate global pyrethrum flower cultivation, supplying high-quality raw material to manufacturers worldwide. Urbanization and rising public health concerns in the Middle East are driving household insecticide demand. Regional governments are investing in processing infrastructure, agricultural value chains, and capacity-building programs to enhance local production efficiency. Public health campaigns targeting malaria, dengue, and other vector-borne diseases reinforce the demand base. Mechanized harvesting, improved farming practices, and access to modern agricultural inputs ensure higher yields and consistent supply. The Middle East benefits from urban population growth, increasing awareness of chemical safety, and expanding household pest control markets.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, is seeing rising adoption due to expanding fruit exports, greenhouse cultivation, and adoption of integrated pest management. Farmers are transitioning toward residue-compliant and environmentally friendly inputs to meet global trade standards. Investments in research, extension services, and supply chain improvements are facilitating broader access to pyrethrin products. Emerging applications in livestock protection, stored grain treatment, and household pest management diversify the market. Increased environmental sustainability awareness and regulatory alignment with export requirements support continued market growth, positioning Latin America as a resilient and high-potential region for pyrethrin-based insecticides.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Pyrethrum Market

- Botanical Resources Australia

- MGK (McLaughlin Gormley King Company)

- Sumitomo Chemical Co., Ltd.

- Kenyatta Pyrethrum Company

- AgroPy Ltd.

- Valent BioSciences LLC

- Pyrethrum Board of Kenya

- Tagros Chemicals India Ltd.

- Neudorff GmbH KG

- Santa Cruz Biotechnology

- Hunan Sunfull Bio-tech Co., Ltd.

- Herbalchem Industries

- BASF SE

- Bayer AG

- Syngenta Group