Puffed Wheat and Puffed Rice in Retail Market Size

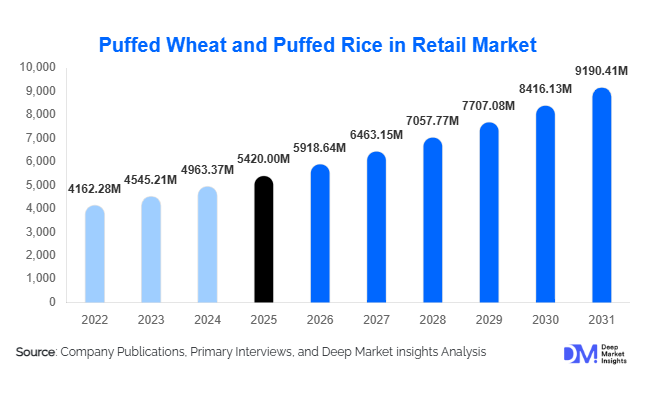

According to Deep Market Insights, the global puffed wheat and puffed rice in retail market size was valued at USD 5,420 million in 2025 and is projected to grow from USD 5,918.64 million in 2026 to reach USD 9,190.41 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). Market expansion is supported by rising consumer demand for affordable ready-to-eat cereals and traditional grain-based snacks, increasing urbanization across emerging economies, and growing adoption of healthier low-fat snack alternatives. Retail distribution modernization, private-label expansion, and innovation in flavored and fortified puffed grains are further strengthening global consumption trends.

Key Market Insights

- Health-conscious snacking trends are driving demand for low-calorie and gluten-light puffed grain products globally.

- Asia-Pacific dominates consumption due to cultural familiarity with puffed rice-based foods and strong retail penetration.

- Private label brands are expanding rapidly, particularly in supermarkets and discount retail chains.

- Fortified and flavored variants are attracting younger consumers and urban households.

- E-commerce grocery platforms are accelerating retail accessibility in developing markets.

- Export demand for traditional grains from India and Southeast Asia continues to grow across global diaspora markets.

What are the latest trends in the puffed wheat and puffed rice retail market?

Shift Toward Healthy and Functional Grain Snacks

Consumers are increasingly replacing fried snacks with lighter grain-based alternatives, positioning puffed wheat and puffed rice as convenient healthy snack substitutes. Manufacturers are introducing fortified variants enriched with iron, vitamins, and plant-based protein to appeal to wellness-focused buyers. Clean-label positioning, minimal processing claims, and whole-grain sourcing are becoming important differentiators. Demand is particularly strong among urban consumers seeking low-fat breakfast and snack options that align with calorie-conscious diets.

Product Premiumization and Flavor Innovation

Retail brands are diversifying offerings through flavored puffed grains such as masala, caramel, honey-coated, chocolate-infused, and savory seasoning formats. Premium packaging formats, resealable pouches, and portion-controlled snack packs are improving shelf visibility and impulse purchases. Innovation is also expanding into breakfast cereals and snack mixes combining puffed rice with nuts, seeds, and dried fruits, increasing product value realization.

What are the key drivers in the puffed wheat and puffed rice market?

Rising Demand for Affordable Staple Snacks

Puffed grains remain among the most cost-effective packaged food options globally. In price-sensitive markets across Asia, Africa, and Latin America, consumers prefer puffed rice products due to affordability and versatility in meals and snacks. Inflationary food environments have reinforced demand for economical cereal substitutes, making puffed grains resilient during economic fluctuations.

Expansion of Organized Retail and Modern Trade

Rapid growth of supermarkets, hypermarkets, and discount chains has improved shelf placement and brand visibility. Organized retail enables bulk packaging, private labeling, and promotional pricing strategies that stimulate volume sales. Emerging markets witnessing retail infrastructure investments are experiencing accelerated adoption rates.

Growth of Ready-to-Eat Breakfast Consumption

Changing lifestyles and increasing dual-income households are boosting consumption of quick breakfast options. Puffed wheat cereals and sweetened puffed rice products are gaining traction as convenient alternatives to traditional cooking-heavy meals, particularly among working professionals and students.

What are the restraints for the global market?

Price Volatility of Raw Grains

Fluctuations in wheat and rice prices caused by climate variability, export restrictions, and supply chain disruptions impact manufacturing margins. Producers operating with thin profit spreads face challenges maintaining stable pricing while ensuring product affordability.

Perception as Low-Value Commodity Product

In developed markets, puffed grains are sometimes viewed as basic or low-nutrition products compared with protein-rich cereals. Limited branding differentiation and commoditization restrict premium pricing opportunities unless manufacturers invest in fortification and innovation.

What are the key opportunities in the puffed wheat and puffed rice industry?

Functional and Fortified Food Expansion

Adding micronutrients, plant proteins, and dietary fiber provides manufacturers opportunities to reposition puffed grains as functional foods. Governments promoting nutrition security programs are encouraging fortified cereal consumption, opening institutional retail opportunities globally.

Export Growth Through Ethnic Food Demand

Global migration and diaspora communities are increasing demand for traditional puffed rice snacks across North America, Europe, and the Middle East. Export-oriented brands from India, Thailand, and Vietnam are expanding international retail footprints through ethnic grocery chains and online marketplaces.

Private Label and Discount Retail Penetration

Retailers are increasingly launching store-brand puffed grain products due to low manufacturing complexity and stable demand. Private labels offer higher margins for retailers while delivering affordable pricing to consumers, making this segment attractive for new entrants and contract manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5420 Million |

| Market Size in 2026 | USD 5918.64 Million |

| Market Size in 2031 | USD 9190.41 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Puffed rice continues to dominate the global puffed grains market, accounting for approximately 62% of global market share in 2025. Its widespread consumption in Asia-Pacific, coupled with a growing trend of convenient snack applications worldwide, supports its leading position. The surge in flavored puffed rice products is being driven by product innovation tailored to younger consumers who prefer on-the-go, healthy, and flavorful options. Puffed wheat holds roughly 28% of the market share, primarily fueled by breakfast cereal applications in North America and Europe, where demand for quick and nutritious morning meals is strong. Multigrain puffed blends, representing nearly 10% share, are emerging as a preferred choice among health-conscious consumers seeking diversified nutrition, higher fiber content, and premium snack alternatives. The growth of functional ingredients, such as protein enrichment and natural flavors, further supports the expansion of multigrain and specialty puffed products globally.

Application Insights

Ready-to-eat snacks remain the leading application, contributing nearly 46% of total demand due to changing lifestyles and convenience-driven consumption patterns. The growing preference for portable, ready-to-consume foods is encouraging manufacturers to introduce innovative flavors, portion-controlled packs, and healthier snack options. Breakfast cereals account for around 32% share, supported by rising adoption of quick morning meals, nutritional fortification, and the popularity of high-fiber and whole-grain variants. Traditional food preparations, including regional snack mixes and street-food-inspired packaged products, represent about 22% of the market. These products continue to expand through organized retail channels and modern packaging, enabling preservation of taste, texture, and authenticity while catering to urban consumers seeking cultural flavors.

Distribution Channel Insights

Supermarkets and hypermarkets lead retail distribution with approximately 41% share, benefiting from bulk purchasing behavior, strong shelf visibility, and integrated marketing promotions. Convenience stores, contributing nearly 24%, are driven by impulse snack purchases and the increasing preference for small, on-the-go packaging formats. Online retail channels account for about 18% and are the fastest-growing segment as grocery e-commerce adoption rises, supported by improved delivery infrastructure and subscription-based snack offerings. Traditional grocery stores maintain relevance in emerging markets, contributing roughly 17%, due to their accessibility in rural and semi-urban areas and their role in promoting local snack varieties.

Packaging Type Insights

Flexible pouches dominate the packaging segment with nearly 55% market share, owing to their cost efficiency, convenience, lightweight design, and ability to extend product shelf life. Plastic jars and rigid containers account for around 25%, particularly for premium breakfast cereal and gift packaging, offering higher protection and aesthetic appeal. Bulk packaging formats represent approximately 20% and are widely used in discount retail and wholesale distribution channels, enabling economies of scale for both retailers and consumers. Sustainability trends are encouraging manufacturers to adopt recyclable and biodegradable materials, further enhancing growth potential for eco-friendly packaging.

End-Use Analysis

Household consumption represents the largest end-use segment, accounting for nearly 68% of global demand, driven by daily snack and breakfast usage across all age groups. The increasing penetration of organized retail, easy-to-prepare products, and health-focused puffed grain options further supports household demand. Foodservice applications, including snack manufacturers, quick-service restaurants, and street-food-inspired packaged products, contribute about 20% and are expanding alongside the growing popularity of ready-to-eat and on-the-go meals. Institutional demand, representing roughly 12%, is supported by schools, government nutrition programs, and food security initiatives targeting affordable, high-nutrition grains. Export-driven demand is also on the rise, particularly for ready-mix snack bases from Asia to diaspora markets, where consumers seek authentic regional flavors. The overall expansion of packaged snack manufacturing industries, projected to grow above 8% annually worldwide, continues to fuel puffed grain consumption across all end-use sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Puffed Wheat and Puffed Rice in Retail Market Segmentations

By Product Type

- Plain Puffed Rice

- Plain Puffed Wheat

- Flavored & Seasoned Puffed Grains

- Fortified & Organic Puffed Variants

By Packaging Type

- Loose/Bulk Packaging

- Retail Flexible Pouches

- Rigid Containers & Boxes

- Single-Serve & On-the-Go Packs

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Traditional Grocery & Kirana Stores

- Online Retail & E-commerce Platforms

- Specialty Health & Organic Stores

By Application

- Breakfast Cereals

- Snack Foods

- Traditional & Ethnic Food Preparations

- Ready-to-Eat Mixes & Instant Foods

Regional Insights

Asia-Pacific

Asia-Pacific leads the global puffed grains market with approximately 48% share in 2025. India, China, Thailand, and Vietnam are major production hubs and consumption centers. In India, traditional snack consumption, urbanization, increasing disposable incomes, and rapid expansion of organized retail drive demand, contributing nearly 18% of global consumption. China’s market growth is propelled by rising breakfast cereal adoption, increasing health awareness, and a growing packaged snack sector targeting urban consumers. Southeast Asian countries benefit from abundant rice production, export-oriented manufacturing, and strong cultural preference for rice-based snacks. The rising popularity of flavored, fortified, and ready-to-eat snacks is fueling regional innovation, while government initiatives promoting food processing and exports further support market expansion.

North America

North America holds nearly 17% market share, led by the United States and Canada. Breakfast cereal consumption remains a key driver, with increasing consumer preference for fortified, organic, and plant-based puffed grain products. Private-label expansion across discount retailers and supermarkets is boosting volume growth, while the rising health and wellness trend drives innovation in low-sugar, high-fiber, and protein-enriched offerings. Convenience-oriented lifestyles, snacking culture, and the expansion of online grocery channels are further accelerating demand for puffed rice and wheat products in the region.

Europe

Europe accounts for around 15% of the global market share, with Germany, the UK, and France leading consumption. Health-conscious consumers in Europe increasingly prefer clean-label cereals, organic puffed wheat products, and plant-based snack options. Snacking occasions, convenience, and rising awareness of dietary fiber and whole grains are driving steady growth. Market expansion is supported by retail modernization, product innovations in premium and functional snacks, and increasing adoption of fortified and allergen-free cereals. Growing trends in sustainable and eco-friendly packaging further enhance the market potential.

Middle East & Africa

The Middle East and Africa region represents approximately 11% of global demand. Gulf countries rely heavily on imports, with demand fueled by urbanization, rising disposable incomes, and preference for convenient snack options. In African markets, consumption is expanding due to affordable staple food demand, retail modernization, and government initiatives supporting food security. The increasing penetration of organized retail chains and supermarkets, coupled with rising awareness of nutrition and protein-rich diets, is driving growth in puffed rice, wheat, and multigrain products across both regions.

Latin America

Latin America contributes roughly 9% market share, led by Brazil and Mexico. Increasing urbanization, adoption of packaged snack foods, and modernization of retail infrastructure are supporting gradual market expansion. Brazil is among the fastest-growing markets, with annual growth exceeding 10%, driven by younger demographics, rising snack culture, and increasing disposable income. Mexico’s growth is supported by both traditional snack consumption and emerging demand for health-oriented, fortified puffed grains. Market development is further enhanced by investment in processing facilities, export potential, and expanding organized retail networks.

Key Players in the Puffed Wheat and Puffed Rice Retail Market

- Kellogg Company

- Nestlé S.A.

- PepsiCo Inc.

- General Mills Inc.

- Post Holdings Inc.

- Marico Limited

- Hain Celestial Group

- Nature’s Path Foods

- Bagrry’s India Ltd.

- B&G Foods Inc.

- Bob’s Red Mill Natural Foods

- Weetabix Limited

- Britannia Industries Limited

- Patanjali Foods Limited

- Ebro Foods S.A.