Protein Snack Market Size

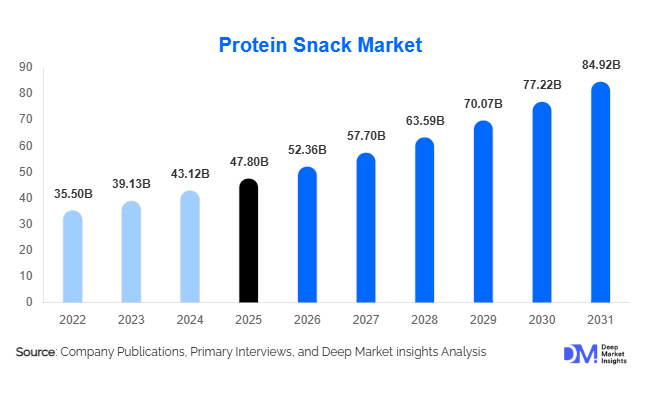

According to Deep Market Insights, the global protein snack market size was valued at USD 47.8 billion in 2025 and is projected to grow from USD 52.36 billion in 2026 to reach USD 84.92 billion by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). Growth in the protein snack market is primarily driven by rising health consciousness, increasing demand for convenient functional foods, and strong adoption of high-protein diets among fitness enthusiasts and mainstream consumers. Consumers are increasingly replacing traditional snacks with protein-enriched alternatives that offer satiety, energy support, and nutritional benefits, accelerating product innovation across bars, chips, dairy-based snacks, and ready-to-drink formats.

Key Market Insights

- Protein snacks are transitioning from niche sports nutrition products to mainstream everyday foods, supported by demand for healthier snacking habits.

- Plant-based protein snacks are expanding rapidly, driven by vegan, flexitarian, and sustainability-focused consumers.

- North America dominates global consumption due to strong fitness culture and functional food penetration.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable incomes, and westernized dietary patterns.

- Clean-label and low-sugar formulations are reshaping product development strategies among manufacturers.

- E-commerce and direct-to-consumer sales channels are accelerating market accessibility and product experimentation.

What are the latest trends in the protein snack market?

Functional Nutrition and Everyday Protein Consumption

Protein snacks are increasingly positioned as functional nutrition products rather than indulgent foods. Consumers seek benefits such as muscle recovery, weight management, sustained energy, and metabolic health. Manufacturers are responding by fortifying snacks with additional nutrients including fiber, probiotics, collagen, and adaptogens. This multifunctional positioning allows brands to target broader consumer groups beyond athletes, including working professionals, aging populations, and students. Portion-controlled packaging and on-the-go formats further support everyday consumption occasions such as breakfast replacement, office snacking, and post-workout recovery.

Rise of Plant-Based and Alternative Protein Sources

Innovation in protein sources represents a defining trend in the market. Pea protein, soy protein, chickpea protein, and emerging sources such as fava bean and algae proteins are gaining commercial traction. Sustainability concerns and lactose intolerance are encouraging consumers to explore dairy-free alternatives. Companies are investing heavily in taste improvement technologies and texture optimization to overcome historical challenges associated with plant proteins. Hybrid formulations combining plant and dairy proteins are also emerging, balancing nutrition, flavor, and affordability while appealing to flexitarian consumers globally.

What are the key drivers in the protein snack market?

Growing Health and Fitness Awareness

Rising participation in fitness activities and increased awareness of protein intake requirements are major growth drivers. Consumers increasingly associate protein consumption with muscle maintenance, weight control, and overall wellness. Gym memberships, home workouts, and digital fitness platforms have significantly increased demand for convenient protein-rich foods. Protein snacks offer a practical alternative to protein powders, enabling easy integration into daily diets without preparation.

Expansion of Convenience Food Culture

Urban lifestyles and longer working hours are accelerating demand for ready-to-eat nutrition solutions. Protein snacks combine convenience with perceived health benefits, making them ideal replacements for traditional high-carb snacks. Retailers are dedicating larger shelf space to functional snacks, while convenience stores and vending channels are expanding availability. Innovation in resealable packaging and single-serving portions further strengthens consumption frequency.

Product Innovation and Flavor Diversification

Continuous innovation in flavors, formats, and textures has broadened consumer appeal. Manufacturers are introducing dessert-inspired flavors, regional taste profiles, and savory protein snacks such as chips and crackers. Advances in food processing technologies have improved texture and reduced chalkiness often associated with protein products, enhancing consumer acceptance and repeat purchases.

What are the restraints for the global market?

High Production Costs and Ingredient Pricing

Protein ingredients such as whey isolate and specialty plant proteins remain relatively expensive compared to conventional snack inputs. Volatility in dairy and agricultural commodity prices impacts manufacturing margins and retail pricing, limiting affordability in price-sensitive markets.

Taste and Texture Challenges

Despite technological improvements, achieving desirable taste and mouthfeel remains challenging, particularly for plant-based protein snacks. Consumer skepticism toward overly processed functional foods may also slow adoption among traditional snack consumers.

What are the key opportunities in the protein snack industry?

Emerging Market Expansion

Rapid urbanization and middle-class expansion in Asia-Pacific, Latin America, and the Middle East create significant opportunities for market penetration. Rising awareness of nutrition and increasing gym culture in countries such as India, China, and Brazil are opening new demand pools. Localization of flavors and affordable product formats can help brands capture first-time consumers in these regions.

Technology Integration and Personalized Nutrition

Digital health ecosystems and wearable fitness technologies enable personalized dietary recommendations, creating opportunities for tailored protein snack solutions. Brands integrating AI-driven nutrition insights and subscription-based snack models can enhance customer retention and lifetime value. Functional claims linked to immunity, energy management, and cognitive performance further expand product positioning.

Retail and E-Commerce Channel Expansion

Online grocery platforms and direct-to-consumer channels allow emerging brands to enter markets without heavy retail investments. Subscription snack boxes, influencer-driven marketing, and social commerce are helping companies rapidly scale brand awareness. Cross-border e-commerce is also facilitating exports of premium protein snacks into high-demand regions.

Product Type Insights

The global mochi market is primarily led by mochi ice cream, which accounts for approximately 58% of total global revenue in 2025. The dominance of this segment is strongly linked to its successful positioning as a premium, portion-controlled frozen dessert that blends traditional Asian confectionery with modern indulgence trends. Mochi ice cream benefits from strong retail visibility, attractive packaging formats, and compatibility with evolving consumer preferences for novelty desserts that offer both texture differentiation and flavor variety. The leading driver for this segment is the rapid globalization of frozen dessert innovation, supported by expanding freezer infrastructure in modern retail outlets and the growing popularity of Asian-inspired desserts among younger consumers. Manufacturers continue to prioritize this category due to its scalability, higher margins compared to traditional confectionery, and strong potential for flavor innovation and seasonal product launches.Traditional sweet mochi represents nearly 24% of the global market share, supported by deeply rooted cultural consumption patterns across East Asian markets, particularly Japan, China, and South Korea. This segment maintains steady demand due to ceremonial usage, gifting traditions, and daily snack consumption. While growth remains moderate compared to frozen formats, product diversification through healthier fillings, reduced sugar formulations, and premium artisanal positioning is sustaining relevance among modern consumers seeking authenticity. The preservation of heritage food culture combined with modernization in packaging and shelf-life technology continues to support stable expansion.Savory mochi variants remain a relatively niche but evolving category, primarily gaining traction within foodservice environments such as fusion restaurants and specialty cafés. The expansion of experimental culinary concepts and cross-cultural menu innovation is gradually introducing savory fillings including cheese, seafood, and plant-based ingredients. Although the segment currently contributes a smaller revenue share, it reflects the broader industry transition toward versatility and culinary experimentation. Innovation-led frozen and ready-to-eat formats are expected to further expand commercialization opportunities as manufacturers explore new consumption occasions beyond desserts.

Flavor Insights

Flavor innovation plays a central role in shaping consumer engagement within the mochi market, with matcha emerging as the leading flavor, accounting for nearly 18% of global demand. The primary driver behind matcha’s leadership is the global expansion of Japanese culinary culture alongside increasing consumer perception of matcha as a premium and wellness-associated ingredient. Its distinct taste profile, antioxidant positioning, and strong visual appeal contribute to sustained popularity across both traditional and modern retail environments.Mango and chocolate flavors closely follow in market share due to their universal acceptance across diverse geographic regions. Mango benefits from strong appeal in tropical and emerging markets where fruit-based desserts resonate with local taste preferences, while chocolate continues to serve as an accessible entry point for first-time consumers unfamiliar with mochi textures. These flavors help bridge cultural gaps, enabling brands to localize products without losing authenticity.Fusion flavors combining Western dessert profiles with Asian ingredients are witnessing double-digit growth rates globally. Innovations such as cookies-and-cream mochi, salted caramel variants, and fruit-cheesecake combinations are expanding consumer demographics and encouraging repeat purchases. The leading growth driver within the flavor segment is experiential consumption, where consumers seek novelty, social media appeal, and premium sensory experiences. Limited-edition launches and seasonal flavor rotations are increasingly used as strategic tools to maintain consumer excitement and brand differentiation.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 46% of total market share in 2025. The leading driver for this segment is the rapid expansion of frozen food infrastructure combined with impulse purchasing behavior influenced by in-store visibility and promotional bundling. Large retail chains provide consistent cold-chain reliability, enabling broader product availability and encouraging trial purchases among mainstream consumers. Enhanced freezer placements, private-label collaborations, and premium dessert aisles continue to strengthen retail penetration.Online retail represents the fastest-growing distribution channel, driven by advancements in temperature-controlled logistics and the rise of direct-to-consumer frozen delivery models. E-commerce platforms allow niche brands and artisanal producers to access wider audiences without traditional retail constraints. Subscription dessert boxes, specialty Asian food marketplaces, and quick-commerce platforms are accelerating adoption, particularly in urban regions where convenience-driven consumption patterns dominate. Digital marketing and influencer-led promotions further amplify online channel expansion by educating consumers about mochi products.

End-Use Insights

Retail household consumption dominates the market, accounting for nearly 62% of total global demand, reflecting mochi’s transformation from a culturally specific confection into a mainstream packaged snack. The leading driver behind this segment is the shift toward at-home indulgence and premium snacking occasions, supported by increasing freezer ownership and rising demand for portion-controlled desserts. Consumers increasingly view mochi as a convenient alternative to traditional ice cream servings, aligning with lifestyle trends emphasizing moderation and novelty.Foodservice applications are expanding rapidly as cafés, dessert chains, and quick-service restaurants integrate mochi-based offerings into menus. Urban dining culture and experiential dessert consumption are key growth contributors, with operators leveraging mochi’s unique texture and customizable flavor formats to differentiate menus. Mochi toppings for beverages, plated desserts, and fusion culinary applications are becoming increasingly common, particularly in metropolitan markets where international cuisine adoption is accelerating.

| By Product Type | By Protein Source | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global mochi market, accounting for approximately 48% share in 2025, supported by strong cultural heritage, established manufacturing ecosystems, and high consumer familiarity. Japan remains the largest producer and consumer, benefiting from deep-rooted traditional consumption as well as continuous product innovation in premium frozen desserts. China is experiencing rapid expansion driven by premium retail modernization, rising disposable incomes, and the growing popularity of aesthetically appealing desserts among younger consumers. South Korea and Taiwan contribute significantly through vibrant café cultures and dessert-focused social trends that encourage frequent product experimentation. India is emerging as a high-growth market, fueled by increasing exposure to Asian cuisines through digital media, expansion of organized retail, and rising demand for premium frozen desserts among urban middle-class consumers. The region’s growth is further supported by strong supply chain capabilities and localized flavor development tailored to regional tastes.

North America

North America accounts for nearly 24% of global demand, led primarily by the United States where mochi ice cream has transitioned into a mainstream supermarket dessert category. Regional growth is driven by increasing multicultural food adoption, strong demand for gluten-free dessert options, and consumer openness toward globally inspired snacks. Health-conscious positioning, portion control benefits, and premium branding strategies continue to attract younger demographics. Canada follows a similar growth trajectory, supported by expanding Asian populations, specialty grocery retail expansion, and increased availability through both traditional supermarkets and online frozen delivery platforms.

Europe

Europe represents approximately 16% of global market share, with strong demand emerging across the United Kingdom, Germany, and France. Regional growth is primarily driven by premium dessert culture, rising experimentation with international cuisines, and strong consumer interest in plant-based and vegan alternatives. European consumers demonstrate high acceptance of innovative textures and artisanal dessert concepts, encouraging manufacturers to introduce organic, dairy-free, and sustainably sourced mochi products. Expanding Asian restaurant presence and specialty food retailers further accelerate product awareness and trial rates across major metropolitan areas.

Middle East & Africa

The Middle East & Africa region is witnessing steady expansion, led by the United Arab Emirates and Saudi Arabia where premium dessert consumption continues to rise alongside rapid urbanization. Growth drivers include high expatriate populations familiar with Asian cuisine, expanding luxury retail environments, and the proliferation of upscale dessert cafés and mall-based dining destinations. Increasing tourism and hospitality sector investments are also contributing to higher demand for innovative dessert offerings, positioning mochi as a premium experiential product within the region’s evolving foodservice landscape.

Latin America

Latin America remains an emerging but fast-developing market, with Brazil and Mexico leading regional adoption. Growth is primarily supported by increasing exposure to global dessert trends through social media, improving cold-chain logistics infrastructure, and expansion of modern retail formats. Younger consumers are demonstrating strong interest in novel international snacks, encouraging retailers to introduce imported and locally produced mochi varieties. Although market penetration remains at an early stage, accelerating urbanization, rising disposable incomes, and growing premium dessert experimentation are expected to drive sustained long-term growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Protein Snack Market

- Nestlé S.A.

- PepsiCo Inc.

- Mondelez International Inc.

- General Mills Inc.

- The Hershey Company

- Kellogg Company (Kellanova)

- Clif Bar & Company

- Quest Nutrition

- Hormel Foods Corporation

- Glanbia plc

- Premier Nutrition Company

- Simply Good Foods Co.

- Otsuka Holdings Co., Ltd.

- Kind LLC

- Mars Incorporated