Protein Hydrolysate Market Size

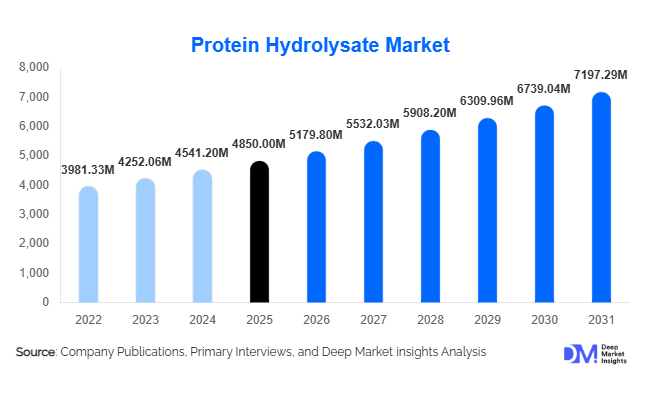

According to Deep Market Insights, the global protein hydrolysate market size was valued at USD 4,850 million in 2025 and is projected to grow from USD 5,179.80 million in 2026 to reach USD 7,197.29 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The protein hydrolysate market growth is primarily driven by increasing demand for high-bioavailability proteins in sports nutrition, clinical nutrition, and infant formula applications, along with the expansion of plant-based and allergen-reduced food formulations globally.

Key Market Insights

- Animal-based protein hydrolysates dominate, accounting for nearly 58% of the 2025 market value, led by whey and collagen hydrolysates.

- Powder form leads the market with approximately 72% share due to superior shelf life, transport efficiency, and blending compatibility.

- Enzymatic hydrolysis is the preferred production method, contributing nearly 65% of total market revenue.

- Sports and clinical nutrition represent the largest application segment, accounting for around 34% of total demand.

- North America holds the largest regional share (32%), while Asia-Pacific is the fastest-growing region with over 8% CAGR.

- Top five players control approximately 42% of the global market, reflecting moderate consolidation.

What are the latest trends in the protein hydrolysate market?

Shift Toward Plant-Based and Allergen-Reduced Proteins

Consumer demand for plant-based nutrition is reshaping product innovation. Soy, pea, and rice protein hydrolysates are increasingly incorporated into vegan sports supplements, dairy alternatives, and hypoallergenic infant formulas. Manufacturers are investing in advanced enzymatic hydrolysis technologies to improve taste profiles and reduce bitterness, historically a key barrier in plant hydrolysates. Sustainability considerations are further accelerating plant-based adoption, particularly in Europe and North America, where consumers favor low-carbon and non-GMO ingredients.

Growth of Medical and Personalized Nutrition

Protein hydrolysates are gaining traction in medical nutrition due to their rapid absorption and reduced allergenicity. Hospitals and clinical nutrition providers are incorporating hydrolyzed proteins in enteral feeding and post-operative recovery diets. Additionally, the rise of personalized nutrition platforms is increasing demand for peptide-specific formulations targeting muscle recovery, gut health, and metabolic disorders. This precision-based approach is expanding premium product segments with higher margins.

What are the key drivers in the protein hydrolysate market?

Rising Demand in Sports and Active Lifestyle Nutrition

Global participation in fitness and athletic activities has significantly boosted demand for rapidly absorbed proteins. Whey protein hydrolysate is particularly preferred for muscle recovery and post-workout supplementation. The expansion of fitness centers, endurance sports events, and digital fitness platforms continues to reinforce demand across developed and emerging markets.

Expansion of Infant Formula Industry

Hydrolyzed proteins are widely used in hypoallergenic and specialized infant formulas. Growing urbanization, higher female workforce participation, and rising middle-class income levels in Asia-Pacific are supporting strong demand growth in this segment. Regulatory requirements for allergen management also favor hydrolyzed protein inclusion.

What are the restraints for the global market?

High Production and Processing Costs

Enzymatic hydrolysis requires specialized enzymes, membrane filtration systems, and quality control measures, increasing capital intensity. Smaller producers face challenges in achieving economies of scale, particularly in price-sensitive animal feed markets.

Sensory and Formulation Challenges

Hydrolysis can produce bitter peptides, limiting broader food and beverage applications. Additional masking agents and flavor optimization technologies increase formulation complexity and costs.

What are the key opportunities in the protein hydrolysate industry?

Expansion in Clinical and Elderly Nutrition

Aging populations in North America, Europe, and parts of Asia are increasing demand for easily digestible protein formats. Hydrolysates are well-suited for elderly nutrition products due to enhanced absorption and digestive comfort. Governments expanding healthcare spending further strengthen long-term demand visibility.

Animal Feed and Aquaculture Intensification

Rising global protein consumption is accelerating aquaculture and livestock production. Hydrolyzed proteins improve feed conversion ratios and gut health in animals, particularly in poultry and fish farming. Emerging economies such as China, India, Brazil, and Vietnam are expanding feed production capacities, creating scalable volume opportunities.

Source Insights

Animal-based protein hydrolysates continue to dominate the global market, accounting for approximately 58% of total revenue in 2025. This leadership is primarily driven by strong demand for whey, casein, and collagen hydrolysates in sports nutrition, clinical nutrition, and specialized dietary applications. Whey protein hydrolysate remains the most commercially significant sub-segment due to its rapid absorption rate, superior amino acid profile, and widespread use in post-workout recovery products. The presence of well-established dairy processing infrastructure in North America and Europe further strengthens this segment’s supply reliability and scalability. Collagen hydrolysates are also experiencing steady growth, supported by rising demand in joint health supplements and beauty-from-within formulations.

Plant-based hydrolysates, including soy, pea, rice, and wheat derivatives, represent the fastest-growing source category. Growth is fueled by increasing vegan adoption, lactose intolerance concerns, sustainability awareness, and regulatory emphasis on allergen-free formulations. Manufacturers are investing in enzymatic refinement technologies to improve taste and solubility, enhancing competitiveness against traditional dairy-based hydrolysates. Microbial and algal hydrolysates remain niche but are gaining strategic importance in biotechnology, fermentation media, and alternative protein development, particularly as precision fermentation technologies evolve.

Form Insights

Powdered protein hydrolysates account for nearly 72% of the global market, making them the leading form segment. The dominance of powder format is driven by extended shelf life, ease of transportation, lower storage costs, and compatibility with dry blending processes in food, beverage, and feed manufacturing. Spray-drying and advanced filtration systems have enabled efficient large-scale production, ensuring consistent peptide distribution and product stability. Powder formats are especially preferred in sports nutrition powders, infant formula blends, and feed premixes.

Liquid hydrolysates serve specialized applications requiring rapid integration into manufacturing lines, particularly in industrial fermentation, ready-to-drink beverages, and certain feed applications. Although smaller in market share, liquid formats are valued for reduced processing steps and improved dispersion in wet formulations.

Application Insights

Sports and clinical nutrition collectively represent the largest application segment, contributing approximately 34% of global market revenue. The leading position of this segment is supported by increasing consumer focus on muscle recovery, protein digestibility, and functional health benefits. Hydrolyzed whey proteins are widely used in post-exercise supplementation due to their faster gastric emptying rate and enhanced amino acid absorption. In clinical settings, hydrolysates are incorporated into enteral feeding solutions and recovery diets, especially for elderly and post-surgical patients.

Infant nutrition remains a high-value application, driven by hypoallergenic and partially hydrolyzed formulations designed for infants with cow milk protein sensitivities. Strict regulatory standards in developed markets ensure steady demand for premium-quality hydrolysates. Animal feed and pet nutrition constitute a volume-driven segment, particularly in aquaculture and poultry production, where hydrolysates improve feed efficiency and gut health. Functional food and beverage applications are expanding as brands integrate hydrolysates into fortified snacks, dairy beverages, and high-protein meal replacements.

End-Use Industry Insights

Food and beverage manufacturers account for nearly 40% of total global demand, making them the largest end-use industry. Hydrolysates are increasingly incorporated into protein bars, ready-to-drink beverages, dairy-based drinks, and fortified bakery products. The segment’s leadership is driven by growing consumer preference for high-protein functional foods and clean-label ingredients. Pharmaceutical and medical nutrition companies represent the fastest-growing end-use segment, expanding at over 7.5% CAGR, supported by rising healthcare expenditure, aging populations, and clinical dietary management requirements. Hydrolysates offer enhanced digestibility and reduced allergenicity, making them suitable for therapeutic nutrition products.

Animal feed manufacturers contribute consistent volume demand, particularly in export-driven aquaculture economies such as China, Vietnam, and Brazil. Increasing restrictions on antibiotic feed additives are encouraging the adoption of bioactive peptides as functional feed enhancers.

| By Source | By Form | By Application | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% of the global protein hydrolysate market in 2025, with the United States accounting for nearly three-quarters of regional consumption. Regional growth is driven by a highly developed sports nutrition industry, widespread gym and fitness culture, and strong demand for premium protein supplements. The region also benefits from advanced dairy processing infrastructure, enabling large-scale production of whey-based hydrolysates. High healthcare expenditure and established clinical nutrition protocols further support demand in medical and elderly nutrition applications. Additionally, innovation in personalized nutrition and functional beverages is reinforcing long-term market expansion.

Europe

Europe represents around 27% of global demand, led by Germany, France, the United Kingdom, and the Netherlands. Growth in the region is supported by stringent allergen labeling regulations, encouraging the use of hydrolyzed proteins in infant and specialized nutrition products. Europe’s strong dairy industry provides a stable supply base for whey and casein hydrolysates. Sustainability trends and increasing vegan adoption are also driving demand for plant-based hydrolysates. Moreover, the region’s aging demographic profile is accelerating uptake in medical and elderly nutrition segments.

Asia-Pacific

Asia-Pacific accounts for nearly 28% of global market share and is the fastest-growing region, expanding at over 8% CAGR. China dominates regional consumption, driven by robust infant formula demand and expanding aquaculture production. Government investments in domestic dairy processing and food ingredient manufacturing are strengthening supply chains. India is emerging as a high-growth market due to expanding nutraceutical consumption, increasing disposable incomes, and growing awareness of protein supplementation. Japan and South Korea contribute steady demand in clinical and elderly nutrition, supported by aging populations and advanced healthcare systems.

Latin America

Latin America contributes approximately 8% of global revenue, with Brazil representing the largest national market. Regional growth is supported by expanding poultry and aquaculture industries, increasing sports supplement penetration, and rising middle-class consumption of fortified foods. Argentina and Mexico are also experiencing growth in the nutraceutical and feed sectors. Export-oriented livestock production further drives demand for performance-enhancing feed ingredients.

Middle East & Africa

The Middle East & Africa region accounts for nearly 5% of the global market. Growth in the Middle East is supported by increasing healthcare investments in the UAE and Saudi Arabia, rising demand for clinical nutrition, and expanding premium food imports. In Africa, rising livestock production and gradual modernization of feed industries are contributing to incremental demand. Government initiatives to strengthen food security and reduce import dependency are encouraging local ingredient processing, which may support long-term market expansion in the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Protein Hydrolysate Market

- Arla Foods Ingredients

- Glanbia Nutritionals

- Kerry Group

- Fonterra Co-operative Group

- Hilmar Cheese Company

- Royal FrieslandCampina

- Carbery Group

- Rousselot

- Titan Biotech

- Axiom Foods

- Tate & Lyle

- AIDP Inc.

- Agropur Ingredients

- NZMP

- AMCO Proteins