Protein Bars Market Size

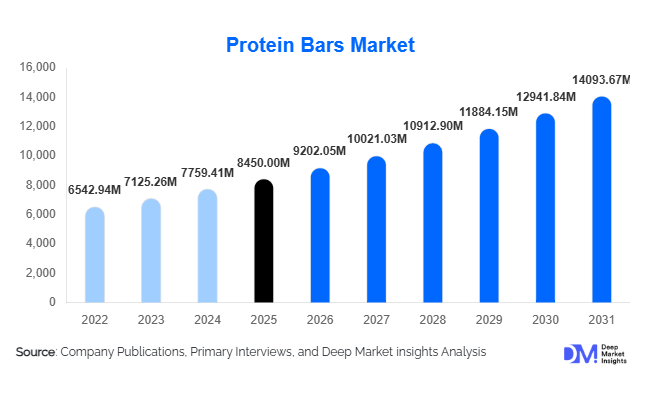

According to Deep Market Insights,the global protein bars market size was valued at USD 8,450 million in 2025 and is projected to grow from USD 9,202.05 million in 2026 to reach USD 14,093.67 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The protein bars market growth is primarily driven by rising global fitness participation, increasing consumer preference for high-protein diets, and strong demand for convenient, on-the-go functional snacks. Expanding plant-based product portfolios, clean-label innovations, and e-commerce penetration are further accelerating market expansion across developed and emerging economies.

Key Market Insights

- High-protein bars (≥20g protein) dominate globally, accounting for over 40% of total demand due to strong sports nutrition adoption.

- Whey protein remains the leading protein source, supported by superior amino acid profile and established consumer trust.

- North America dominates the global market, led by the U.S., driven by mature fitness culture and high per capita protein consumption.

- Asia-Pacific is the fastest-growing region, fueled by rising middle-class income and expanding gym memberships in China and India.

- Online retail is expanding rapidly, supported by subscription models and direct-to-consumer (DTC) strategies.

- Clean-label, low-sugar, and plant-based formulations are reshaping product development pipelines globally.

What are the latest trends in the protein bars market?

Plant-Based and Clean-Label Innovation

Plant-based protein bars are witnessing strong growth as consumers increasingly demand vegan, lactose-free, and allergen-free alternatives. Pea protein, soy protein, and blended plant proteins are gaining traction, particularly among flexitarian and environmentally conscious consumers. Manufacturers are reformulating products to reduce added sugars, eliminate artificial preservatives, and incorporate organic ingredients. Labels highlighting non-GMO, gluten-free, keto-friendly, and low-carb claims are significantly influencing purchasing decisions. This clean-label shift is strengthening premium product positioning while expanding appeal beyond traditional athletes to mainstream consumers.

Functional & Hybrid Nutrition Bars

Protein bars are evolving into multifunctional nutrition solutions. New launches increasingly incorporate collagen, probiotics, omega-3 fatty acids, adaptogens, and vitamin fortification. These hybrid bars are positioned for immunity support, gut health, skin health, and cognitive performance. Clinical-grade formulations targeting diabetic-friendly or keto-specific diets are expanding institutional demand in hospitals and wellness clinics. The blending of sports nutrition with functional wellness is widening the consumer base and enhancing average selling prices.

What are the key drivers in the protein bars market?

Rising Fitness Participation and Sports Nutrition Demand

Global gym memberships and participation in sports activities continue to expand, driving consistent demand for convenient protein supplementation. Protein bars serve as post-workout recovery snacks and meal replacements, particularly among athletes and bodybuilders. Growth in marathon participation, bodybuilding competitions, and recreational fitness has created sustained repeat purchase behavior.

On-the-Go Lifestyle and Snacking Culture

Urbanization and busy work schedules are accelerating demand for portable, ready-to-eat snacks. Protein bars offer portion control, long shelf life, and functional benefits, making them preferred alternatives to traditional confectionery products. Increasing demand from working professionals and students is supporting mid-range segment growth.

What are the restraints for the global market?

High Retail Pricing in Emerging Economies

Protein bars are significantly more expensive than conventional snacks, limiting adoption in price-sensitive markets. Import dependency and high raw material costs further inflate retail pricing in developing countries.

Volatility in Protein Raw Material Prices

Fluctuations in dairy prices impact whey protein costs, while plant protein sourcing depends on agricultural yields. This volatility pressures manufacturer margins and creates pricing instability in competitive markets.

What are the key opportunities in the protein bars industry?

Emerging Market Expansion

Asia-Pacific and Latin America offer strong growth potential due to expanding middle-class populations and increasing fitness awareness. Localized flavor innovation and affordable product variants can unlock mass-market demand. India and China are projected to grow at over 10% CAGR through 2031.

Clinical and Institutional Nutrition Integration

Protein bars are gaining traction in elderly care, diabetic-friendly diets, and hospital recovery programs. Partnerships with healthcare providers and corporate wellness programs create stable B2B revenue streams. This institutional demand offers premium pricing opportunities and long-term contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8450 Million |

| Market Size in 2026 | USD 9202.05 Million |

| Market Size in 2031 | USD 14093.67 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The high-protein bars segment continues to lead the global protein bars market, accounting for approximately 42% of total market share in 2025. This dominance is primarily driven by the sustained expansion of sports nutrition consumption, increasing gym memberships, rising participation in endurance sports, and growing consumer awareness regarding muscle recovery and strength enhancement. High-protein formulations are strongly positioned among athletes, bodybuilders, and performance-focused consumers who prioritize macronutrient density and functional benefits. The leading segment driver remains the expanding global fitness ecosystem, including health clubs, boutique fitness studios, and digital training platforms, which actively promote protein supplementation as part of structured workout regimens.

Meal replacement bars represent one of the fastest-growing product categories, supported by accelerating weight management trends, busy urban lifestyles, and demand for convenient on-the-go nutrition. Consumers increasingly seek balanced macronutrient profiles that combine protein, fiber, and essential vitamins to support satiety and controlled calorie intake. Moderate-protein snack bars are gaining traction among mainstream consumers transitioning from traditional confectionery snacks toward healthier alternatives, driven by clean-label positioning and reduced sugar formulations. Meanwhile, energy and performance bars maintain a strong presence within athletic and endurance categories, supported by carbohydrate-protein blends tailored for pre- and intra-workout consumption.

Protein Source Insights

Whey protein bars dominate the protein source segment with nearly 38% market share in 2025, supported by well-established scientific validation, rapid amino acid absorption, and long-standing credibility within sports performance communities. The leading driver for this segment is the proven efficacy of whey protein in muscle synthesis and recovery, which reinforces consumer trust and repeat purchasing behavior. Established brand recognition and strong retail penetration further sustain segment leadership.

Plant-based protein bars are the fastest-growing segment, expanding at double-digit growth rates due to the rising global adoption of vegan and flexitarian diets, lactose intolerance prevalence, and sustainability considerations. Increasing innovation in pea, soy, brown rice, and blended plant proteins has improved taste profiles and amino acid completeness, reducing earlier formulation limitations. Collagen protein bars are emerging within beauty-from-within and joint health applications, gaining traction among aging populations and wellness-focused consumers seeking multifunctional nutritional benefits.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 40% of global sales, maintaining their position as the leading distribution channel due to high product visibility, strong foot traffic, and impulse purchasing behavior. The primary driver for this segment is large-scale retail accessibility combined with in-store promotional strategies and private-label expansion, which enhance price competitiveness and consumer trial. Strategic shelf placement within health food aisles and checkout counters further strengthens sales performance.

Online retail represents the fastest-growing channel, expanding at a CAGR exceeding 12%, supported by subscription-based purchasing models, direct-to-consumer brand strategies, influencer-driven marketing, and personalized nutrition targeting. Digital platforms enable broader SKU variety and detailed nutritional transparency, which appeals to informed consumers. Specialty nutrition stores maintain a strong position within premium and sports-focused segments, offering expert recommendations and niche product assortments that reinforce consumer loyalty among performance-driven buyers.

End-Use Insights

Sports nutrition remains the dominant end-use segment, accounting for approximately 48% of the global market share. The leading segment driver is the continued globalization of fitness culture, including strength training, endurance sports, and recreational athletics, which directly stimulates demand for protein-enriched functional snacks. Increasing consumer emphasis on post-workout recovery and muscle maintenance supports sustained category growth.

Clinical and functional nutrition applications are expanding steadily, supported by medical nutrition therapy, geriatric dietary supplementation, and protein fortification for individuals with specific health conditions. General snacking applications are driving mass-market penetration, particularly in urban environments where consumers prioritize convenient yet nutritious snack options. Additionally, corporate wellness initiatives and institutional procurement programs are emerging as structured demand contributors, integrating protein bars into employee health benefits and organized dietary programs.

Explore more data points, trends and opportunities Download Free Sample Report

Protein Bars Market Segmentations

By Product Type

- High-Protein Bars (≥20g Protein)

- Moderate-Protein Bars (10–19g Protein)

- Low-Protein Snack Bars (<10g Protein)

- Meal Replacement Protein Bars

- Energy & Performance Protein Bars

By Protein Source

- Whey Protein Bars

- Casein Protein Bars

- Soy Protein Bars

- Pea Protein Bars

- Blended Plant Protein Bars

- Collagen Protein Bars

- Other Alternative Protein Bars (Egg, Insect-Based, etc.)

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health & Nutrition Stores

- Pharmacies & Drug Stores

- Online Retail (Brand Websites & Marketplaces)

- Fitness Centers & Gyms

By End-Use Application

- Sports Nutrition

- Clinical & Functional Nutrition

- General Snacking

- Corporate & Institutional Consumption

By Price Segment

- Economy

- Mid-Range

- Premium

Regional Insights

North America

North America holds approximately 38% of the global market share in 2025, with the United States contributing nearly 82% of regional demand. Regional dominance is driven by a highly developed sports nutrition ecosystem, advanced retail infrastructure, strong presence of leading protein bar manufacturers, and elevated consumer spending capacity. High awareness regarding protein intake, widespread gym culture, and strong adoption of functional foods further accelerate market maturity. Canada demonstrates steady growth supported by clean-label trends, plant-based adoption, and regulatory transparency that encourages premium product innovation.

Europe

Europe accounts for around 27% of global demand, led by the United Kingdom, Germany, and France. Regional growth is driven by stringent labeling regulations that promote product quality, increasing consumer demand for organic and non-GMO ingredients, and expanding plant-based dietary adoption across Western Europe. Health-conscious consumer behavior, coupled with rising interest in sustainable and ethically sourced protein ingredients, supports product innovation. Fitness participation rates and the expansion of private-label protein snack offerings in major retail chains further contribute to regional market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR of approximately 10.5%. China and India are witnessing rapid fitness adoption, increasing disposable incomes, and expanding middle-class populations that are driving demand for convenient protein-based snacks. Japan and Australia remain relatively mature markets with strong health awareness and established sports nutrition consumption patterns. Rapid e-commerce penetration, mobile-first purchasing behavior, and cross-border brand availability significantly accelerate market accessibility. Urbanization and the growing influence of Western dietary habits further stimulate protein bar adoption across metropolitan areas.

Latin America

Latin America contributes roughly 7% of global demand, led by Brazil and Mexico. Regional growth is supported by expanding urban fitness culture, increasing health awareness among younger demographics, and gradual improvement in modern retail infrastructure. Rising imports from North America and growing presence of international brands enhance product availability. Economic stabilization in key countries and the expansion of organized retail channels continue to create incremental growth opportunities.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global market share, driven primarily by the United Arab Emirates and Saudi Arabia. Growth is supported by high purchasing power in Gulf Cooperation Council countries, increasing fitness club memberships, and strong demand for premium imported nutrition brands. Urbanization, rising expatriate populations, and government initiatives promoting healthier lifestyles contribute to expanding protein snack consumption. While the market remains nascent in several African economies, improving retail penetration and growing health awareness present long-term growth potential.

Key Players in the Protein Bars Market

- Quest Nutrition

- Clif Bar & Company

- RXBAR

- Optimum Nutrition

- Kellogg’s

- General Mills

- Mars Incorporated

- Abbott Laboratories

- Glanbia Nutritionals

- Myprotein

- Barebells

- Grenade

- PowerBar

- MusclePharm

- Simply Good Foods