Protein Ball Market Size

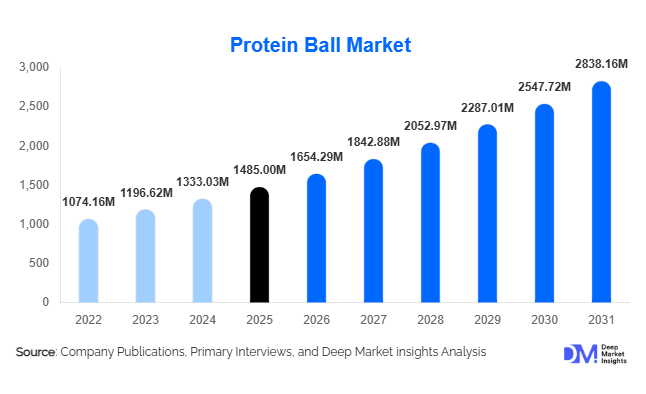

According to Deep Market Insights, the global protein ball market size was valued at USD 1,485 million in 2025 and is projected to grow from USD 1,654.29 million in 2026 to reach USD 2,838.16 million by 2031, expanding at a CAGR of 11.4% during the forecast period (2026–2031). The protein ball market growth is primarily driven by rising global demand for convenient high-protein snacks, increasing adoption of functional foods among health-conscious consumers, and the rapid expansion of plant-based nutrition products across developed and emerging economies.

Protein balls have evolved from niche sports nutrition products into mainstream functional snacks consumed by a wide demographic including athletes, working professionals, and wellness-focused consumers. Growing awareness regarding balanced nutrition, weight management, and clean-label ingredients has accelerated product adoption globally. Manufacturers are introducing innovative formulations incorporating superfoods, plant proteins, adaptogens, and low-sugar ingredients to align with evolving dietary preferences.

The expansion of e-commerce grocery platforms and direct-to-consumer (D2C) nutrition brands has further improved accessibility and product discovery. Additionally, rising veganism trends, increasing gym memberships, and demand for on-the-go nutrition solutions are reshaping snacking behavior worldwide. As consumers increasingly replace traditional confectionery snacks with functional alternatives, protein balls are emerging as a fast-growing category within the broader healthy snacks industry.

Key Market Insights

- Plant-based protein balls are witnessing accelerated adoption due to vegan and lactose-free dietary trends globally.

- Online retail channels are transforming market penetration through subscription snack models and influencer-driven marketing.

- North America leads global consumption owing to strong fitness culture and functional snack awareness.

- Asia-Pacific represents the fastest-growing region, supported by urbanization and rising middle-class health spending.

- Clean-label and low-sugar formulations are becoming primary purchase drivers among millennials and Gen Z consumers.

- Product innovation through superfoods and adaptogens is differentiating premium brands in competitive markets.

What are the latest trends in the protein ball market?

Shift Toward Clean-Label Functional Snacking

Consumers increasingly prefer minimally processed foods with recognizable ingredients, pushing manufacturers to reformulate protein balls using natural sweeteners such as dates, honey, and agave syrup. Artificial preservatives and refined sugars are being eliminated in favor of organic and non-GMO certifications. Functional positioning-such as immunity support, gut health benefits, and energy enhancement-is becoming central to product marketing. Brands are also highlighting allergen-free claims including gluten-free, dairy-free, and soy-free formulations to expand consumer reach.

Plant-Based and Alternative Protein Innovation

The rise of plant-based nutrition has significantly influenced product innovation. Pea protein, brown rice protein, hemp protein, and nut-based formulations are replacing whey in many new launches. Hybrid protein blends combining plant and dairy sources are emerging to enhance amino acid profiles while maintaining texture and taste. This innovation trend is enabling brands to cater simultaneously to athletes, vegans, and flexitarian consumers seeking sustainable nutrition solutions.

What are the key drivers in the protein ball market?

Growing Health and Fitness Awareness

Rising participation in fitness activities, gym memberships, and sports nutrition programs is driving demand for convenient protein-rich snacks. Consumers increasingly seek products that support muscle recovery, sustained energy, and weight management. Protein balls provide portion-controlled nutrition, making them attractive alternatives to protein bars and sugary snacks.

Expansion of On-the-Go Consumption Culture

Urban lifestyles and busy work schedules have increased demand for portable snack formats. Protein balls require no preparation and are easy to consume during travel, work breaks, or workouts. Their compact packaging and long shelf life make them ideal for modern retail environments including convenience stores and online grocery platforms.

What are the restraints for the global market?

High Product Pricing Compared to Conventional Snacks

Premium ingredients such as nuts, plant proteins, and organic sweeteners increase production costs, resulting in higher retail prices. This limits adoption among price-sensitive consumers in developing markets and restricts mass-market penetration.

Raw Material Price Volatility

Fluctuating prices of almonds, cashews, cocoa, and plant protein isolates impact manufacturing margins. Supply disruptions caused by climate variability and agricultural constraints create pricing instability, posing challenges for manufacturers attempting to maintain competitive pricing.

What are the key opportunities in the protein ball industry?

Expansion into Emerging Markets

Rapid urbanization in India, Southeast Asia, and Latin America presents strong growth potential. Rising disposable income and increasing exposure to Western dietary habits are encouraging adoption of functional snack products. Localization of flavors such as mango, matcha, and regional nuts provides opportunities for brands to penetrate new consumer segments.

Integration of Functional Ingredients and Personalized Nutrition

Protein balls enriched with probiotics, collagen, adaptogens, and vitamins are gaining popularity among wellness-focused consumers. Personalized nutrition trends supported by digital health platforms are expected to enable customized snack formulations targeting specific health outcomes such as energy, immunity, or stress management.

Corporate and Institutional Distribution Channels

Workplace wellness programs, airlines, schools, and fitness centers are emerging as new distribution avenues. Bulk procurement by institutional buyers offers scalable demand opportunities for manufacturers while increasing brand visibility.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1485 Million |

| Market Size in 2026 | USD 1654.29 Million |

| Market Size in 2031 | USD 2838.16 Million |

| CAGR | 11.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plant-based protein balls are the clear frontrunner in the global protein ball market, capturing approximately 42% of the projected market share in 2025. This dominance is fueled by a combination of factors, including the rising adoption of vegan diets, increasing awareness of lactose intolerance, and a broader shift toward sustainable and plant-forward nutrition. Consumers are increasingly seeking snacks that provide not only convenience but also functional health benefits, leading to the growing popularity of protein balls enriched with superfoods, probiotics, and micronutrients. Within the product spectrum, organic protein balls have carved a niche as a premium offering, supported by clean-label demand and a willingness among consumers to pay for transparency and ethically sourced ingredients. The keto and low-carb variants are gaining significant traction as weight management and metabolic health continue to drive purchasing behavior, particularly among urban professionals and fitness enthusiasts. Functional protein balls targeting specific health outcomes, such as immune support, energy enhancement, and mental focus, are experiencing rapid growth as wellness-oriented consumers increasingly integrate these products into their daily routines. Innovations in flavor, texture, and fortification are also playing a key role, with brands introducing exotic flavors and nutrient-dense ingredients to differentiate their offerings in a competitive marketplace. The convergence of taste, convenience, and health benefits positions protein balls as a versatile snack segment with a strong potential for continued expansion across global markets.

Protein Source Insights

The market for protein balls is predominantly driven by plant protein sources, which hold nearly 48% share of the overall market in 2025. Plant proteins such as pea, soy, and rice are favored for their sustainability credentials, lower environmental footprint, and suitability for vegan and vegetarian diets. This aligns with the growing consumer emphasis on eco-friendly consumption and dietary diversification, which has prompted manufacturers to innovate new blends that balance amino acid profiles and taste. Whey protein-based products continue to maintain significant popularity, particularly among athletes and performance-driven consumers in North America and Europe, due to their superior bioavailability and proven efficacy in muscle repair and recovery. Mixed-protein formulations, combining plant and dairy proteins, have emerged as a compelling solution that offers a balanced nutritional profile, improved texture, and enhanced flavor, appealing to a wider audience seeking both performance benefits and palatability. Additionally, niche protein sources such as insect-based, collagen-infused, and pea-rice blends are beginning to penetrate premium segments, reflecting consumers’ willingness to explore novel, high-protein alternatives. The ongoing trend toward functional fortification, including added vitamins, minerals, adaptogens, and fiber, further underscores the importance of protein source selection in meeting diverse consumer health goals.

Distribution Channel Insights

Distribution strategies are central to the growth of the protein ball market, with online retail emerging as the leading channel, contributing around 36% of global sales in 2025. E-commerce platforms, direct-to-consumer brand websites, and subscription snack boxes have transformed accessibility, enabling consumers to discover and purchase a diverse range of protein ball offerings with ease. The convenience of home delivery, coupled with tailored subscription models, fosters brand loyalty and encourages repeat purchases, particularly among busy urban consumers. Supermarkets and hypermarkets remain vital for mass-market visibility, providing a tactile experience and enabling impulse purchases, while fitness centers, gyms, and specialty nutrition stores contribute high-margin sales by targeting health-conscious consumers seeking premium, performance-oriented snacks. The rise of omnichannel retail strategies, combining offline and online touchpoints, allows brands to reach multiple consumer segments simultaneously, strengthening market penetration. Furthermore, strategic partnerships with meal delivery services, wellness programs, and corporate offices are creating new distribution avenues that drive trial and adoption. Retailers and brands increasingly leverage personalized marketing, data-driven recommendations, and social media integration to enhance consumer engagement and drive sales growth across regions.

End-Use Insights

The sports and fitness segment represents the largest end-use category, accounting for nearly 39% of global demand. Athletes, gym-goers, and performance-oriented consumers prefer protein balls for their portability, protein density, and functional benefits such as muscle recovery and sustained energy. However, mainstream lifestyle consumers are emerging as the fastest-growing segment, reflecting a broad cultural shift in which protein balls are increasingly viewed as an everyday snack rather than solely a fitness supplement. Corporate wellness programs, school nutrition initiatives, and health-focused workplace offerings are expanding the end-use base, introducing protein balls to populations beyond traditional sports enthusiasts. The global fitness industry, valued at over USD 100 billion, continues to expand, creating a sustained demand pipeline for convenient and functional snacks. Additionally, export-driven demand is rising, with North American and European brands exporting premium protein ball products to Asia-Pacific markets, where functional food adoption and e-commerce infrastructure are growing rapidly. Marketing campaigns highlighting wellness, taste, and lifestyle compatibility are accelerating awareness and adoption, further broadening the end-use reach and creating opportunities for cross-segment expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Protein Ball Market Segmentations

By Product Type

- Plant-Based Protein Balls

- Whey Protein Balls

- Collagen Protein Balls

- Keto & Low-Carb Protein Balls

- Functional & Superfood Protein Balls

By Distribution Channel

- Online Retail & D2C Platforms

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health & Organic Stores

- Fitness Centers & Direct Sales

By End Use

- Sports Nutrition

- Weight Management & Diet Programs

- Healthy Lifestyle Snacking

- Clinical & Functional Nutrition

By Ingredient Source

- Plant Protein

- Animal Protein

- Mixed Protein Formulations

By Packaging Type

- Single-Serve Packs

- Multi-Pack Retail Boxes

- Bulk Packs

- Eco-Friendly & Sustainable Packaging

Regional Insights

North America

North America is the largest regional market for protein balls, contributing approximately 34% of global revenue in 2025. The United States is the primary driver, supported by a sophisticated sports nutrition ecosystem, high health awareness, and a willingness among consumers to experiment with innovative snack formats. North American consumers increasingly prioritize convenience, functional benefits, and sustainability, which is boosting plant-based and organic protein ball sales. Canada is witnessing robust growth, fueled by rising adoption of plant-based diets, organic food consumption, and a strong presence of specialty nutrition retailers. Regional growth drivers include increasing gym memberships, the proliferation of boutique fitness studios, and widespread e-commerce adoption, enabling niche brands to reach consumers in urban and suburban areas. Health-focused marketing campaigns, partnerships with fitness influencers, and promotional programs in wellness-oriented retail channels have further strengthened market penetration. North America’s mature distribution infrastructure and consumer readiness to pay premium prices for innovative and health-promoting products ensure that the region remains a global leader while continuing to stimulate category innovation.

Europe

Europe holds nearly 27% of the global protein ball market, with the U.K., Germany, and France leading demand. Consumer preferences in this region are strongly shaped by clean-label regulations, high vegan adoption rates, and widespread retail penetration of health-focused brands. Scandinavian countries, including Sweden, Norway, and Denmark, are showing particularly strong growth due to sustainability-driven consumption, awareness of environmental impact, and preference for plant-based nutrition. Growth is further fueled by government policies supporting healthy lifestyles, the rising popularity of functional foods, and urban consumer trends that favor premium, nutrient-dense snacks. The expansion of specialty retail, health food stores, and online wellness marketplaces has enhanced accessibility, enabling brands to cater to diverse dietary preferences. Innovation in flavors, ingredient transparency, and packaging sustainability resonates strongly with European consumers, driving repeat purchases and loyalty. Cross-border e-commerce and international trade agreements also facilitate market expansion, allowing emerging brands to scale rapidly and compete with established players in major Western European markets.

Asia-Pacific

Asia-Pacific is the fastest-growing region for protein balls, expanding at over 13% CAGR. Major contributors include China, India, Japan, and Australia, driven by a combination of demographic, lifestyle, and technological factors. India’s urban youth population, increasing gym culture, and growing health awareness are accelerating adoption of protein balls as convenient snacks for active lifestyles. China’s robust e-commerce ecosystem and mobile-first retail platforms enable rapid distribution and mass adoption, particularly in Tier 1 and Tier 2 cities. Japan and Australia exhibit strong demand for premium and functional variants, reflecting rising disposable incomes and an appetite for health-promoting snacks. Regional growth drivers include rising awareness of dietary supplementation, government campaigns promoting fitness and nutrition, and the expansion of modern retail formats. Social media influence, celebrity endorsements, and influencer-led campaigns play a critical role in shaping consumer perceptions and accelerating market penetration. Additionally, Asia-Pacific consumers increasingly seek products aligned with functional health benefits, such as immunity, cognitive support, and energy, offering significant opportunities for innovation and segmentation.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, led by the United Arab Emirates and Saudi Arabia, which are benefiting from premium retail expansion, rising health consciousness, and increased disposable income. South Africa represents a dynamic growth market, driven by an expanding fitness culture, increasing gym memberships, and modern retail penetration that introduces global and regional protein ball brands to urban consumers. Drivers in this region include rising awareness of the benefits of functional snacks, growing interest in plant-based nutrition, and an increasing preference for convenient, ready-to-eat products. Retail modernization, online retail adoption, and marketing campaigns highlighting wellness and lifestyle appeal are fostering rapid growth. The combination of affluent urban populations and rising demand for Western-style health snacks presents an attractive opportunity for both international and local brands seeking market entry and expansion.

Latin America

Latin America is characterized by growing demand for functional snacks, with Brazil and Mexico leading consumption due to increasing health awareness, a rising middle class, and expanding access to modern retail channels. Regional brands are introducing affordable protein ball variants to improve accessibility and cater to price-sensitive consumers, while premium imported offerings appeal to urban, health-conscious demographics. Growth is supported by rising fitness culture, government nutrition initiatives, and awareness campaigns promoting healthier snack alternatives. Expansion of online marketplaces, supermarkets, and convenience stores ensures wider distribution, while promotional strategies highlighting energy, satiety, and wellness benefits further drive adoption. Latin America represents a high-potential growth market, particularly as consumers embrace global health trends and the concept of functional, protein-enriched snacking becomes more mainstream.

Key Players in the Protein Ball Market

- General Mills, Inc.

- Mondelez International, Inc.

- Hormel Foods Corporation

- Clif Bar & Company

- The Simply Good Foods Company

- RXBAR (Kellogg Company)

- Garden of Life LLC

- Orgain, Inc.

- Quest Nutrition LLC

- GoMacro LLC

- Nutree Life

- Bounce Foods Ltd.

- Creative Nature Ltd.

- Lärabar (General Mills)

- Perfect Snacks, Inc.