Protective Culture Market Size

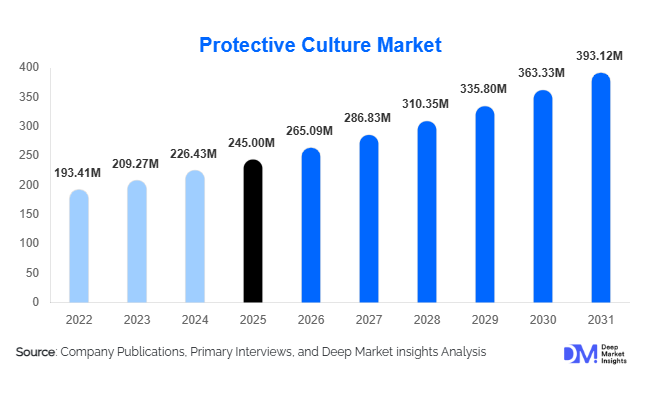

According to Deep Market Insights, the global protective culture market size was valued at USD 245 million in 2025 and is projected to grow from USD 265.09 million in 2026 to reach USD 393.12 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The protective culture market growth is primarily driven by rising demand for clean-label food preservation solutions, increasing regulatory scrutiny on chemical preservatives, and expanding global consumption of fermented dairy and meat products.

Protective cultures, live microorganisms added to inhibit spoilage and pathogenic bacteria, are becoming a core component of natural food preservation strategies. Their adoption is accelerating across cheese, yogurt, processed meats, and emerging plant-based alternatives, as manufacturers seek to enhance shelf life while meeting consumer expectations for minimally processed foods. Industrial-scale dairy processors remain the largest consumers, while the rapid expansion of plant-based fermented products is creating new application avenues. Strong R&D investment in microbial strain development and freeze-drying technologies is further strengthening commercial scalability, positioning protective cultures as a critical enabler of modern food safety and sustainability initiatives.

Key Market Insights

- Dairy applications dominate the market, accounting for nearly 65% of total demand in 2025, particularly in cheese manufacturing.

- Bacterial protective cultures led by microbial type, contributing approximately 72% of global revenue, driven by lactic acid bacteria adoption.

- Europe holds the largest regional share (35%), supported by strong cheese exports and stringent food safety regulations.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR due to dairy industrialization in China and India.

- Industrial food processors account for about 75% of end-use demand, reflecting structured adoption in large-scale production facilities.

- Technological advancements in strain genomics and fermentation optimization are enhancing efficacy and extending shelf life by up to 50% in select applications.

What are the latest trends in the protective culture market?

Clean-Label Reformulation Across Dairy and Meat

Food manufacturers are increasingly reformulating products to remove synthetic preservatives such as sorbates and nitrates. Protective cultures are being integrated as natural antimicrobial systems, enabling “no artificial preservatives” claims while maintaining product safety. In cheese and ready-to-eat meat products, anti-listeria and anti-fungal strains are replacing traditional chemical inhibitors. This trend is particularly strong in Europe and North America, where regulatory scrutiny and consumer awareness are high. Clean-label positioning is now a competitive differentiator, pushing suppliers to offer customized culture blends tailored to specific product matrices.

Expansion into Plant-Based and Alternative Proteins

The rapid growth of plant-based dairy alternatives is creating demand for fermentation-based preservation solutions. Oat, almond, soy, and pea-based yogurt analogues require microbial stabilization similar to conventional dairy. Protective culture suppliers are developing strain-specific formulations to support texture, safety, and shelf life in non-dairy substrates. As plant-based food markets expand at double-digit growth rates globally, protective cultures are emerging as essential functional ingredients in this evolving ecosystem.

What are the key drivers in the protective culture market?

Stringent Food Safety Regulations

Global food safety authorities have tightened microbial standards, particularly for pathogens such as Listeria monocytogenes in dairy and meat products. Protective cultures provide a proactive barrier against contamination, complementing HACCP protocols. Industrial processors increasingly adopt these cultures to minimize recall risks and comply with export standards.

Growth in Fermented Food Consumption

Rising global consumption of yogurt, specialty cheese, and fermented beverages is directly boosting demand. The global dairy processing industry exceeds USD 900 billion in value, and even marginal integration of protective cultures across this base translates into steady revenue growth. Export-oriented cheese producers particularly rely on bio-protection to maintain quality during long-haul shipments.

What are the restraints for the global market?

High R&D and Validation Costs

Developing strain-specific protective cultures requires advanced microbiological research, pilot validation, and regulatory documentation. These costs limit entry for smaller players and increase commercialization timelines.

Cold Chain and Storage Constraints

Protective cultures, especially frozen and freeze-dried forms, require temperature-controlled logistics. In emerging markets with fragmented supply chains, distribution complexity may slow adoption.

What are the key opportunities in the protective culture industry?

Emerging Market Dairy Modernization

Countries such as China and India are investing heavily in dairy infrastructure modernization. Integration of protective cultures in new processing facilities offers suppliers long-term contract opportunities. Growing urban consumption and export ambitions further strengthen this opportunity.

Customized Anti-Fungal Solutions for Bakery

Mold-related spoilage losses in bakery products are significant. Anti-fungal protective cultures are gaining traction as clean-label mold inhibitors, particularly in packaged breads and pastries distributed through modern retail channels.

Microbial Type Insights

Bacterial protective cultures continue to dominate the global protective culture market, accounting for approximately 72% of total revenue in 2025. This leadership is primarily driven by the widespread use of lactic acid bacteria (LAB) in cheese, yogurt, and fermented dairy production. LAB strains are highly effective in inhibiting spoilage organisms and pathogenic bacteria such as Listeria monocytogenes, making them indispensable for industrial-scale dairy and processed meat manufacturers. Their compatibility with existing fermentation systems, proven regulatory safety status (GRAS in North America and QPS in Europe), and strong scientific validation further reinforce their market dominance. Additionally, bacterial cultures offer predictable performance across diverse temperature and pH ranges, supporting large-scale export operations.

Yeast- and mold-based protective cultures represent smaller but steadily growing segments, particularly in specialty cheese, fermented meats, and artisanal food applications. Growth in these segments is being supported by premiumization trends and the rising popularity of traditional and region-specific fermented foods.

Functionality Insights

By functionality, anti-fungal protective cultures account for nearly 38% of total market demand, making them the leading functional segment. Their dominance is largely attributed to high mold-related spoilage rates in cheese and bakery products. Industrial cheese manufacturers, in particular, rely on anti-fungal cultures to extend shelf life by 30–50% without resorting to chemical preservatives such as sorbates. The shift toward clean-label bakery products has further accelerated adoption, as retailers demand preservative-free packaged bread and pastries with longer shelf stability.

Anti-bacterial cultures, especially those targeting Listeria control, are witnessing steady growth in processed meat and ready-to-eat segments. Stricter global food safety regulations and increasing recall costs are encouraging meat processors to integrate bio-protective systems as preventive controls rather than corrective measures.

Form Insights

Freeze-dried protective cultures lead the market with approximately 60% share, primarily due to their superior stability, extended shelf life, and ease of international transportation. This format reduces cold-chain dependency compared to frozen cultures and offers dosing precision for automated fermentation systems. The scalability of freeze-drying technology aligns well with industrial dairy operations, which represent the largest end-use base. Frozen cultures remain important in high-performance fermentation environments where rapid microbial activation is required. Liquid cultures, although niche, are gaining relevance among artisanal and small-scale producers seeking flexible batch customization.

Application Insights

Dairy products account for approximately 65% of total protective culture demand, making dairy the dominant application segment. Cheese production is the single largest contributor within this category, driven by global consumption growth and expanding export trade. Protective cultures are increasingly used to safeguard long maturation periods and international shipments. The leading driver for dairy dominance is the combination of stringent microbial safety standards and high economic losses associated with spoilage in aged cheeses. Meat and poultry applications are expanding due to mandatory pathogen control requirements in ready-to-eat products. Meanwhile, beverages and plant-based alternatives are emerging as high-growth segments, particularly in fermented oat and soy-based yogurt substitutes.

End-Use Insights

Industrial food processors account for nearly 75% of global protective culture consumption. The dominance of this segment is driven by structured quality management systems, regulatory compliance requirements, and large production volumes that justify consistent integration of bio-protective solutions. Multinational dairy and meat processors are embedding protective cultures directly into standardized production protocols to reduce recall risks and optimize shelf-life performance. Artisanal producers and specialty fermentation companies represent smaller but premium segments, often focusing on differentiated, region-specific products with higher per-unit margins.

| By Microbial Type | By Functionality | By Form | By Application | By End-Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for roughly 32% of global revenue, led by the United States and Canada. Regional growth is primarily driven by stringent food safety enforcement, particularly zero-tolerance policies for Listeria in ready-to-eat foods. The presence of large-scale industrial dairy and processed meat manufacturers further accelerates adoption. Additionally, strong consumer preference for clean-label foods and high awareness of natural preservation technologies support sustained demand. Ongoing investments in dairy automation and export-oriented cheese production continue to reinforce regional market expansion.

Europe

Europe leads the global protective culture market with approximately 35% share in 2025. Major demand centers include France, Germany, Italy, Denmark, and the Netherlands—countries with strong cheese production and export capabilities. The region’s growth is driven by strict EU food safety regulations, a highly developed cold-chain infrastructure, and a mature clean-label consumer base. Europe’s leadership in specialty and aged cheese production further necessitates protective cultures to prevent mold contamination during long maturation cycles. Additionally, sustainability-focused reformulation initiatives are accelerating the replacement of chemical preservatives.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR. China is the fastest-growing national market, supported by rapid dairy industrialization, consolidation of milk processing facilities, and increasing demand for packaged yogurt and cheese. India shows strong long-term potential through cooperative dairy modernization programs and rising urban consumption of processed dairy. Growing middle-class income levels, expanding cold-chain logistics, and increasing export ambitions are key regional growth drivers.

Latin America

Brazil and Argentina lead demand in Latin America, driven by expanding dairy and beef export industries. Growth is supported by the need for extended shelf-life solutions to maintain product quality during international shipments. Regulatory harmonization with North American and European food safety standards is further encouraging protective culture adoption.

Middle East & Africa

Demand in the Middle East & Africa is rising steadily, particularly in GCC countries and South Africa. Regional growth is supported by dairy import substitution strategies, government-led food security initiatives, and investments in modern processing infrastructure. As domestic dairy production scales up, protective cultures are increasingly integrated to enhance product stability in hot climatic conditions and reduce spoilage losses.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Protective Culture Market

- Chr. Hansen

- IFF

- DSM-Firmenich

- Sacco System

- Bioprox

- Lallemand

- CSK Food Enrichment

- Angel Yeast

- Meat Cracks Technologie

- Dalton Biotechnologies