Prosecco Market Size

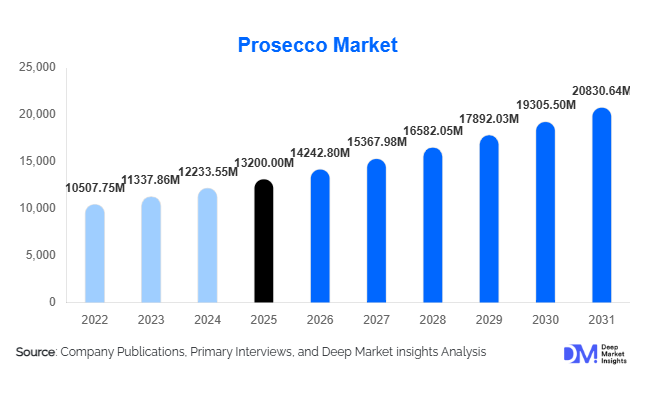

According to Deep Market Insights, the global prosecco market size was valued at USD 13,200 million in 2025 and is projected to grow from USD 14,242.80 million in 2026 to reach USD 20,830.64 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The prosecco market growth is primarily driven by the increasing global demand for affordable sparkling wines, rising preference among millennials and Gen Z consumers, and expanding distribution through modern retail and e-commerce platforms.

Key Market Insights

- Prosecco consumption is shifting toward casual and frequent drinking occasions, moving beyond traditional celebratory usage into everyday consumption patterns.

- Mid-range prosecco dominates global sales, offering a balance between affordability and perceived premium quality.

- Europe remains the largest market, driven by strong domestic consumption and export-oriented production in Italy.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and increasing wine awareness.

- Off-trade channels lead distribution, particularly supermarkets and e-commerce platforms enabling wider accessibility.

- Product innovation, including canned prosecco and low-alcohol variants, is reshaping consumption among younger consumers.

What are the latest trends in the prosecco market?

Premiumization and DOCG Expansion

The prosecco market is witnessing a steady shift toward premiumization, with increasing demand for DOCG-certified variants such as Conegliano Valdobbiadene Superiore. Consumers are becoming more quality-conscious, seeking authenticity, regional identity, and superior taste profiles. Producers are leveraging appellation-based branding and storytelling to differentiate their offerings and command higher price points. This trend is particularly strong in developed markets such as the U.S., U.K., and Germany, where consumers are willing to pay a premium for superior quality and provenance.

Growth of Alternative Packaging Formats

Innovative packaging formats such as cans and kegs are gaining traction, particularly among younger consumers and in outdoor or casual consumption settings. Canned prosecco offers convenience, portability, and portion control, making it popular for events, travel, and single-serve consumption. Keg-based prosecco is also expanding in bars and restaurants, enabling on-tap serving and reducing packaging waste. These formats are broadening the product’s accessibility and creating new consumption occasions beyond traditional bottle-based usage.

What are the key drivers in the prosecco market?

Rising Global Demand for Sparkling Wines

The increasing popularity of sparkling wines globally is a major driver for prosecco demand. Compared to champagne and other premium sparkling wines, prosecco offers a more affordable yet high-quality alternative, making it accessible to a broader consumer base. The rise of cocktail culture, particularly drinks like spritzers, has further boosted its appeal across multiple demographics.

Expansion of Retail and E-commerce Channels

The growth of organized retail and digital commerce has significantly improved accessibility to prosecco products. Supermarkets, specialty liquor stores, and online platforms are expanding their product offerings, allowing consumers to explore a wider variety of brands and price segments. E-commerce platforms, in particular, are driving growth by offering convenience, competitive pricing, and direct-to-consumer sales models.

What are the restraints for the global market?

Geographical Production Constraints

Prosecco production is strictly regulated and limited to specific regions in Italy under DOC and DOCG classifications. This restricts supply scalability and makes the market vulnerable to climatic conditions and agricultural risks. Limited production flexibility can constrain growth during periods of high demand.

Competition from Alternative Sparkling Wines

The market faces strong competition from other sparkling wine categories such as cava, champagne, and domestic sparkling wines. Price-sensitive consumers in emerging markets may opt for lower-cost alternatives, while premium consumers may shift toward champagne, creating competitive pressure across price segments.

What are the key opportunities in the prosecco industry?

Emerging Market Expansion

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes and increasing exposure to global wine culture. Strategic pricing, localized marketing, and smaller packaging formats can help producers tap into these high-potential markets and expand their consumer base.

Low-Alcohol and Sustainable Product Innovation

There is growing demand for healthier and environmentally sustainable beverages. Producers can capitalize on this trend by introducing low-alcohol, organic, and eco-friendly prosecco variants. Sustainable viticulture practices and recyclable packaging are becoming key differentiators, particularly among environmentally conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13200.00 Million |

| Market Size in 2026 | USD 14242.80 Million |

| Market Size in 2031 | USD 20830.64 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global prosecco market continues to be overwhelmingly dominated by Prosecco DOC, which accounts for approximately 78% of the total market share in 2025. This dominance is primarily attributed to its significantly higher production volumes, broader geographic cultivation base, and well-established global distribution networks that enable widespread availability across both mature and emerging markets. The scalability of DOC production, supported by modern viticulture practices and efficient supply chain systems, allows producers to meet growing international demand while maintaining competitive pricing, which further strengthens its position in the mid-range and mass-premium segments.On the other hand, Prosecco DOCG, while representing a comparatively smaller share of the global market, is steadily gaining traction within premium and super-premium segments. The growth of DOCG variants is driven by increasing consumer awareness regarding quality differentiation, origin authenticity, and strict production standards. These wines are produced in limited geographic zones under stringent regulatory frameworks, ensuring superior quality, refined taste profiles, and enhanced brand value. As consumers in developed markets become more discerning and willing to pay a premium for authenticity and craftsmanship, DOCG products are witnessing consistent demand growth.Furthermore, the rising global trend toward premiumization in the alcoholic beverage sector is reinforcing the expansion of DOCG offerings. Consumers are increasingly seeking products with a strong regional identity and heritage narrative, which DOCG wines effectively deliver. This shift is particularly evident in markets such as Western Europe and North America, where wine consumers are progressively moving toward higher-value purchases, thereby creating a favorable environment for DOCG segment growth in the long term.

Application Insights

Individual consumption has emerged as the leading application segment in the global prosecco market, contributing approximately 54% of the total market share. This dominance reflects a fundamental shift in consumer behavior, where prosecco is no longer reserved solely for celebratory occasions but is increasingly integrated into everyday lifestyles. The growing trend of casual drinking, particularly among younger consumers, has significantly expanded the frequency of consumption, thereby driving consistent demand across retail channels.In contrast, event-based consumption, which includes weddings, parties, corporate events, and festive celebrations, continues to play a significant role in the market. However, its growth trajectory is comparatively slower than individual consumption due to the increasing normalization of prosecco as an everyday beverage. Despite this, the segment remains important for premium and bulk purchases, particularly in the on-trade channel, where prosecco is widely used in cocktails and celebratory settings.Additionally, the strong association of prosecco with popular cocktails such as spritzers has enhanced its appeal in both individual and social consumption scenarios. This dual applicability across casual and formal contexts provides a stable demand base and ensures sustained growth across application segments. The increasing influence of social media and lifestyle marketing is also contributing to the normalization of prosecco consumption in everyday settings, further strengthening the leading position of the individual consumption segment.

Distribution Channel Insights

The off-trade segment dominates the global prosecco market, accounting for approximately 65% of total market share. This leadership is driven by the extensive presence of supermarkets, hypermarkets, specialty liquor stores, and increasingly, online retail platforms that provide consumers with convenient access to a wide range of products. The affordability, accessibility, and promotional pricing strategies commonly associated with off-trade channels significantly contribute to their dominance.One of the primary drivers of off-trade growth is the increasing consumer preference for at-home consumption, which aligns with broader lifestyle trends emphasizing convenience and cost efficiency. Consumers are increasingly opting to purchase prosecco through retail outlets where they can compare prices, explore different brands, and benefit from discounts and bundled offers. This has led to higher sales volumes and strengthened the position of off-trade channels in both developed and emerging markets.Meanwhile, the on-trade segment, which includes bars, restaurants, hotels, and clubs, is experiencing a strong recovery following disruptions in recent years. The resurgence of social dining, tourism, and nightlife activities is driving demand within this channel. Prosecco’s versatility as both a standalone beverage and a key ingredient in cocktails makes it a popular choice in on-trade settings. Although the on-trade segment holds a smaller share compared to off-trade, it remains critical for brand visibility, premium positioning, and consumer engagement.

Price Segment Insights

The mid-range price segment leads the global prosecco market, accounting for nearly 46% of the total market share. This segment’s dominance is primarily driven by its ability to strike a balance between affordability and quality, making it accessible to a wide consumer base while still offering a premium drinking experience. The strong positioning of mid-range products aligns with the overall market trend toward value-for-money offerings, particularly in economically diverse regions.Mid-range prosecco products benefit from high production volumes, efficient supply chains, and strong brand recognition, which enable competitive pricing without compromising quality. This segment is particularly popular in both mature markets, where consumers seek everyday indulgence, and emerging markets, where affordability remains a key purchasing criterion. The consistent demand for mid-range products ensures stable revenue generation and supports the overall growth of the market.The premium and super-premium segments, however, are witnessing faster growth rates, driven by increasing disposable incomes, changing consumer preferences, and a growing inclination toward luxury and experiential consumption. Consumers are increasingly willing to pay higher prices for superior quality, distinctive taste profiles, and strong brand heritage. This trend is particularly prominent in developed markets, where premiumization is a key driver of market expansion.At the same time, the economy segment continues to perform well in price-sensitive markets, especially in regions such as Asia-Pacific and Latin America. These products cater to first-time wine consumers and those seeking affordable options for casual consumption. While the growth rate of the economy segment is relatively moderate, its role in expanding the consumer base and driving market penetration remains significant.

Packaging Insights

Glass bottles remain the dominant packaging format in the global prosecco market, accounting for approximately 88% of the total market share. This dominance is largely attributed to consumer perception, as glass packaging is strongly associated with quality, tradition, and authenticity in the wine industry. Glass bottles are preferred across both off-trade and on-trade channels, as they preserve the product’s integrity, carbonation, and flavor profile, while also enhancing its visual appeal.The widespread adoption of glass bottles is further supported by established production and distribution infrastructure, which ensures cost efficiency and scalability. Additionally, glass packaging aligns with premium branding strategies, making it the preferred choice for both DOC and DOCG products. The ability to incorporate elegant designs, labeling, and branding elements further reinforces its position as the leading packaging format.However, alternative packaging formats, particularly cans, are gaining rapid popularity, especially among younger consumers and in informal consumption settings. Canned prosecco offers convenience, portability, and portion control, making it ideal for outdoor activities, travel, and casual social gatherings. The growing demand for ready-to-drink beverages and the increasing emphasis on sustainability are also contributing to the adoption of alternative packaging solutions.Manufacturers are increasingly exploring innovative packaging options to cater to evolving consumer preferences and differentiate their offerings in a competitive market. While glass bottles will continue to dominate in the foreseeable future, the rising popularity of alternative formats represents a significant growth opportunity and reflects the dynamic nature of the market.

Explore more data points, trends and opportunities Download Free Sample Report

Prosecco Market Segmentations

By Product Type

- Prosecco DOC

- Prosecco DOCG

By Sweetness Level

- Brut

- Extra Dry

- Dry

By Packaging Type

- Glass Bottles

- Cans

- Kegs

By Price Segment

- Economy

- Mid-Range

- Premium

- Super Premium

By Distribution Channel

- On-Trade

- Off-Trade

- Supermarkets & Hypermarkets

- Specialty Liquor Stores

- E-commerce / Online Retail

Regional Insights

Europe

Europe dominates the global prosecco market, accounting for approximately 48% of total market share in 2025. The region’s leadership is primarily driven by Italy, which serves as the production hub and global exporter of prosecco. The presence of well-established vineyards, favorable climatic conditions, and centuries-old winemaking traditions provides a strong foundation for sustained production and quality assurance.In addition to Italy, countries such as the United Kingdom and Germany represent major consumption markets within Europe. The strong wine culture, high consumer awareness, and established distribution networks across these countries contribute significantly to regional dominance. The widespread availability of prosecco in retail outlets, coupled with strong brand recognition, ensures consistent demand across various consumer segments.Key growth drivers in Europe include increasing premiumization, rising demand for authentic and region-specific products, and the growing popularity of sparkling wines in everyday consumption. The region also benefits from robust tourism, which enhances on-trade sales, particularly in hospitality and fine dining sectors. Furthermore, regulatory frameworks and quality certifications such as DOC and DOCG reinforce consumer trust and support long-term market growth.

North America

North America holds approximately 28% of the global prosecco market share, with the United States emerging as one of the largest importers. The region’s strong growth is driven by a well-developed alcoholic beverage industry, high disposable incomes, and evolving consumer preferences that favor sparkling wines.One of the primary drivers of growth in North America is the region’s vibrant cocktail culture, where prosecco is widely used as a base ingredient in popular beverages. The increasing popularity of brunch culture and social drinking occasions further supports demand. Additionally, millennials and younger consumers are playing a crucial role in market expansion, as they exhibit a strong preference for lighter, refreshing, and lower-alcohol beverages.The expansion of e-commerce and direct-to-consumer sales channels is also contributing to market growth, enabling greater product accessibility and consumer engagement. The trend toward premiumization, coupled with increasing interest in imported wines, is expected to further drive demand for high-quality prosecco variants in the region.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in the global prosecco market, with a CAGR exceeding 9%. The region’s rapid growth is driven by a combination of economic development, urbanization, and changing lifestyle patterns that are fostering increased adoption of wine consumption.Countries such as China, India, and Japan are witnessing significant growth in demand, supported by rising disposable incomes and increasing exposure to Western culture. The growing middle-class population, particularly in urban areas, is increasingly embracing wine as a symbol of sophistication and social status. This trend is further reinforced by the expansion of modern retail formats and the increasing availability of imported products.Additional growth drivers include the rising influence of digital marketing, the expansion of e-commerce platforms, and the growing popularity of social drinking occasions among younger consumers. While the market is still in its early stages compared to Europe and North America, the long-term growth potential of the Asia-Pacific region remains substantial, making it a key focus area for global producers.

Latin America

Latin America is experiencing steady growth in the prosecco market, driven by improving economic conditions and expanding middle-class populations. Countries such as Brazil and Mexico are at the forefront of regional growth, with increasing consumer interest in premium alcoholic beverages.The growing popularity of social gatherings, celebrations, and Western lifestyle influences is contributing to the rising demand for sparkling wines, including prosecco. Additionally, the expansion of retail infrastructure and the increasing presence of international brands are enhancing product accessibility across the region.Although the market size remains relatively smaller compared to other regions, the long-term growth prospects are promising. Increasing urbanization, rising disposable incomes, and evolving consumer preferences are expected to drive sustained demand in the coming years.

Middle East & Africa

The Middle East & Africa region represents a niche but steadily growing market for prosecco. Growth is primarily concentrated in urban centers such as the United Arab Emirates and South Africa, where demand is supported by tourism, expatriate populations, and a well-developed hospitality sector.Key growth drivers include the expansion of luxury hotels, fine dining establishments, and international events, which contribute to increased consumption in on-trade channels. The presence of a diverse and affluent consumer base, particularly in metropolitan areas, further supports demand for premium and imported beverages.While cultural and regulatory factors may limit consumption in certain areas, the overall market is expected to grow steadily, driven by ongoing economic development and increasing globalization. The region’s focus on tourism and hospitality will continue to play a crucial role in shaping the demand for prosecco in the years ahead.

Key Players in the Prosecco Market

- La Marca

- Mionetto

- Zonin1821

- Villa Sandi

- Ruggeri & C.

- Bisol1542

- Santa Margherita

- Bottega S.p.A.

- Maschio Benassi

- Freixenet

- Gancia

- Carpenè Malvolti

- Astoria Wines

- Ruffino

- La Gioiosa