Processed Cheese Market Size

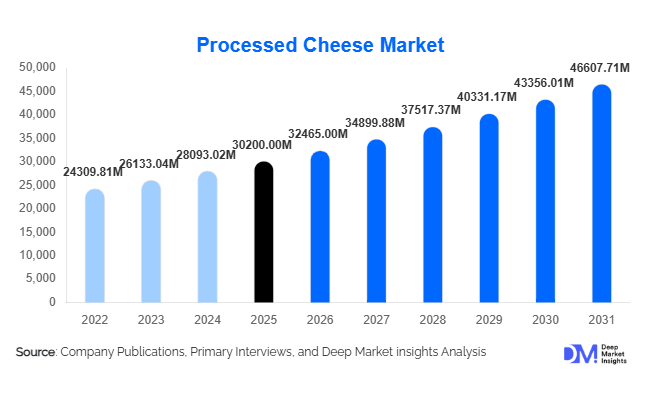

According to Deep Market Insights, the global processed cheese market size was valued at USD 30,200 million in 2025 and is projected to grow from USD 32,465.00 million in 2026 to reach USD 46,607.71 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The processed cheese market growth is primarily driven by the rising demand for convenience foods, increasing consumption of fast food and ready-to-eat meals, and the expanding applications of processed cheese across foodservice and packaged food industries.

Key Market Insights

- Processed cheese demand is rising due to convenience and versatility, making it a staple ingredient in fast food, snacks, and ready meals globally.

- Foodservice industry expansion, particularly QSR chains, is significantly boosting demand for cheese slices, sauces, and spreads.

- North America dominates the global market, supported by high per capita cheese consumption and strong fast-food culture.

- Asia-Pacific is the fastest-growing region, driven by urbanization, westernized diets, and rising disposable incomes.

- Product innovation, including low-fat, organic, and plant-based cheese variants, is reshaping consumer preferences.

- Flexible packaging formats are gaining traction, enhancing product accessibility and shelf life.

What are the latest trends in the processed cheese market?

Rise of Plant-Based and Functional Cheese Alternatives

The processed cheese market is witnessing a growing shift toward plant-based alternatives, driven by rising veganism, lactose intolerance awareness, and sustainability concerns. Manufacturers are introducing cheese alternatives derived from almond, soy, coconut, and cashew bases. In addition, functional processed cheese enriched with vitamins, probiotics, and high-protein formulations is gaining popularity among health-conscious consumers. These innovations are helping reposition processed cheese from a purely indulgent product to a more balanced dietary option.

Convenience-Driven Packaging Innovations

Packaging innovation is playing a critical role in driving processed cheese consumption. Single-serve slices, on-the-go sachets, resealable pouches, and portion-controlled packs are becoming mainstream. These formats cater to busy urban consumers and enhance product portability. Advanced packaging technologies are also improving shelf life and maintaining product freshness, especially in emerging markets where cold chain infrastructure is still developing.

What are the key drivers in the processed cheese market?

Growth of Fast Food and Quick Service Restaurants

The rapid expansion of global quick service restaurant (QSR) chains has significantly boosted processed cheese demand. Cheese is a core ingredient in burgers, pizzas, sandwiches, and wraps, making it indispensable in commercial food preparation. The increasing number of QSR outlets, especially in emerging markets, is directly contributing to higher consumption volumes.

Increasing Demand for Ready-to-Eat and Convenience Foods

Urbanization and changing lifestyles have led to a surge in demand for ready-to-eat and easy-to-cook food products. Processed cheese fits seamlessly into this trend due to its long shelf life, ease of use, and consistent taste. Its application across snacks, frozen foods, and packaged meals continues to expand, further driving market growth.

What are the restraints for the global market?

Health Concerns Related to Processed Foods

Growing awareness about the health implications of processed foods is a key restraint for the market. Processed cheese often contains high levels of sodium, preservatives, and emulsifiers, which may deter health-conscious consumers. This has led to increased scrutiny and demand for cleaner-label products.

Volatility in Raw Material Prices

Fluctuations in milk prices and dairy supply chains pose a significant challenge for manufacturers. Rising input costs can impact profit margins and force price adjustments, potentially affecting demand in price-sensitive markets.

What are the key opportunities in the processed cheese industry?

Expansion in Emerging Markets

Emerging economies such as India, China, Brazil, and Southeast Asian countries offer significant growth potential due to rising urban populations, increasing disposable incomes, and evolving dietary habits. Companies can tap into these markets by offering affordable products tailored to local tastes and preferences.

Technological Advancements and Product Innovation

Advances in food processing technologies are enabling manufacturers to develop improved textures, flavors, and nutritional profiles. Innovations such as low-fat cheese, fortified products, and clean-label formulations are creating new growth avenues and expanding the consumer base.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 30200.00 Million |

| Market Size in 2026 | USD 32465.00 Million |

| Market Size in 2031 | USD 46607.71 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Processed cheese slices continue to dominate the global processed cheese market, accounting for approximately 28% of the global market share in 2025. This dominance is primarily attributed to their unmatched convenience, standardized portioning, and widespread integration into fast-food and quick-service restaurant (QSR) menus. Their ability to melt uniformly and enhance the sensory appeal of burgers, sandwiches, and wraps has positioned them as an indispensable ingredient across both commercial and household applications.The growth of this segment is strongly driven by the accelerating global fast-food culture, particularly in urban centers where time-constrained consumers increasingly prefer ready-to-eat meals. Foodservice chains rely heavily on processed cheese slices due to their operational efficiency, reduced preparation time, and consistent quality. Additionally, the expansion of global QSR brands into emerging markets has significantly amplified demand. Another key driver is the rise of standardized food preparation systems, where portion control and cost predictability are essential, making sliced processed cheese a preferred choice.Beyond slices, cheese spreads and sauces are experiencing notable expansion, driven by evolving snacking behaviors and increasing experimentation in home cooking. These variants offer versatility across multiple cuisines, serving as dips, spreads, and cooking bases. The rising popularity of fusion foods and gourmet home dining experiences is further strengthening demand. Cheese blocks and shredded formats also maintain steady adoption, especially in institutional catering and bakery applications, where customization and bulk usage are critical. The overall product diversification trend reflects manufacturers’ efforts to cater to a broadening consumer palate and shifting dietary preferences toward convenience-oriented dairy products.

Application (End-Use) Insights

The foodservice industry remains the dominant end-use segment, contributing nearly 50% of total processed cheese demand. This leadership is anchored in the rapid expansion of global restaurant chains, cafes, and QSR outlets. The consistent inclusion of processed cheese in burgers, pizzas, sandwiches, and snack items makes it a core ingredient in foodservice menus worldwide. Operational advantages such as long shelf life, easy storage, and predictable melting behavior further enhance its attractiveness for commercial kitchens.The primary growth driver for this segment is the sustained globalization of eating-out culture. Increasing disposable incomes, urban lifestyles, and changing consumer habits are leading to higher frequency of dining outside the home. Additionally, menu innovation within fast-food chains, particularly the introduction of premium burgers and cheese-loaded offerings, is boosting per-unit cheese consumption. The growing penetration of international food chains into emerging economies is also significantly accelerating demand.Household consumption is steadily expanding, supported by rising demand for convenient meal solutions and ready-to-use ingredients. Busy lifestyles, dual-income households, and increasing awareness of Western cuisine are encouraging consumers to incorporate processed cheese into home cooking. The growing popularity of home-based snacking, particularly among younger demographics, is further contributing to this trend.The food processing industry also represents a key application area, utilizing processed cheese in packaged snacks, frozen meals, bakery products, and ready-to-eat foods. Manufacturers favor processed cheese for its emulsification stability and compatibility with large-scale production systems. The increasing demand for convenience foods, especially in urban retail environments, continues to drive adoption across this segment. Technological advancements in food processing and formulation are enabling improved texture, flavor retention, and extended shelf life, further supporting industrial usage.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape, holding approximately 45% market share in 2025. These retail formats provide consumers with wide product assortments, competitive pricing, and strong brand visibility. Their organized structure and ability to offer multiple product variants in one location make them a preferred shopping destination for processed cheese products.The key driver for this channel’s dominance is consumer trust and the perceived assurance of product authenticity and quality. Additionally, in-store promotions, discounts, and sampling activities significantly influence purchase decisions. The growing expansion of modern retail infrastructure in emerging economies further strengthens this channel’s position.Online retail is emerging as the fastest-growing distribution channel, fueled by rapid digital transformation, increased smartphone penetration, and the convenience of doorstep delivery. E-commerce platforms offer consumers access to a wider variety of brands, competitive pricing, and subscription-based purchasing options. The COVID-19 pandemic has permanently shifted consumer behavior toward online grocery shopping, accelerating long-term growth in this channel. Improved cold-chain logistics and efficient last-mile delivery systems are also enhancing product availability and freshness.Convenience stores continue to play a vital role, particularly in urban and semi-urban regions where quick, on-the-go purchases are common. Their strategic locations near residential areas, transportation hubs, and workplaces make them highly accessible. The demand for single-serve and smaller packaging formats aligns well with this channel’s consumer base, particularly among working professionals and students.

Packaging Insights

Flexible packaging leads the global processed cheese market, accounting for approximately 40% of total packaging share. This dominance is driven by its cost-effectiveness, lightweight nature, and ability to preserve product freshness. Flexible packaging formats such as pouches, wraps, and resealable packs enhance convenience while reducing transportation costs and environmental impact.A major growth driver in this segment is the increasing consumer preference for portability and convenience. Modern lifestyles demand packaging that supports on-the-go consumption, especially in urban environments. Flexible packaging also offers superior shelf-life extension through improved barrier properties, which helps maintain product quality over time.Single-serve and portion-controlled packaging formats are gaining significant traction, particularly among younger consumers and working professionals. These formats align with health-conscious consumption trends by enabling controlled intake and reducing food waste. Additionally, manufacturers are increasingly adopting sustainable packaging materials, including recyclable and biodegradable films, in response to rising environmental awareness and regulatory pressures.Rigid packaging formats such as tubs and boxes continue to maintain relevance in bulk purchasing and foodservice applications, where durability and ease of stacking are important. However, innovation in hybrid packaging solutions that combine rigidity with flexibility is expected to shape future market dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

Processed Cheese Market Segmentations

By Product Type

- Processed Cheese Blocks

- Processed Cheese Slices

- Processed Cheese Spread

- Processed Cheese Sauce & Dips

- Processed Cheese Cubes & Portions

- Processed Cheese Powder

By Source

- Cow Milk-Based Processed Cheese

- Buffalo Milk-Based Processed Cheese

- Mixed Milk Processed Cheese

- Plant-Based Processed Cheese Alternatives

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Foodservice/Institutional Sales

Regional Insights

North America

North America holds approximately 30% of the global processed cheese market share, with the United States serving as the primary growth engine. The region’s strong demand is driven by deeply entrenched fast-food culture, high per capita cheese consumption, and a well-established dairy processing infrastructure. The widespread presence of global QSR chains further reinforces consistent demand for processed cheese products.The key growth driver in North America is the sustained dominance of convenience-based eating habits. Consumers increasingly prefer ready-to-eat meals and restaurant-style food at home, boosting retail and foodservice consumption. Additionally, product innovation in reduced-fat, organic, and clean-label cheese variants is expanding the consumer base. Canada also contributes significantly, supported by high dairy consumption patterns and strong retail penetration.

Europe

Europe accounts for nearly 28% of the global market, supported by a mature dairy industry and strong culinary integration of cheese-based products. Key markets such as Germany, France, and the United Kingdom drive regional demand through both traditional consumption and modern processed food applications.The primary growth driver in Europe is the increasing demand for premium and organic processed cheese products. Consumers in the region exhibit strong preferences for high-quality, sustainably sourced dairy products. Additionally, innovation in gourmet and artisanal-style processed cheese is gaining traction. The expansion of bakery and convenience food sectors also contributes to steady demand. Regulatory emphasis on food safety and quality standards further strengthens consumer confidence in processed dairy products.

Asia-Pacific

Asia-Pacific holds approximately 25% market share and is the fastest-growing regional market, registering a CAGR exceeding 9%. Major contributors include China, India, Japan, and Southeast Asian countries. Rapid urbanization, rising disposable incomes, and increasing exposure to Western dietary patterns are reshaping food consumption habits across the region.The key growth driver in Asia-Pacific is the expanding middle-class population and the rapid proliferation of modern retail and foodservice infrastructure. The increasing popularity of fast food, coupled with aggressive expansion by international QSR chains, is significantly boosting demand. Additionally, rising demand for convenience foods among working populations is accelerating household consumption. Local manufacturers are also introducing regionally adapted flavors, further enhancing market penetration.

Latin America

Latin America contributes approximately 7% of the global market, with Brazil and Mexico leading regional consumption. The market is characterized by a growing foodservice sector and increasing penetration of processed and packaged foods.The primary growth driver in this region is the expansion of urban populations and the rising adoption of Western-style diets. The increasing presence of international fast-food chains is significantly boosting demand for processed cheese. Additionally, economic development and improving retail infrastructure are making packaged dairy products more accessible to consumers. The growing popularity of convenience foods among younger populations is further supporting market growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 10% of the global market share, with key growth markets including the United Arab Emirates, Saudi Arabia, and South Africa. Demand is primarily driven by urbanization, tourism, and increasing exposure to global cuisines.The main growth driver in this region is the strong influence of expatriate populations and Western dietary habits. The rapid expansion of hospitality and foodservice sectors, particularly in Gulf countries, is significantly increasing processed cheese consumption. Additionally, rising investments in retail infrastructure and cold-chain logistics are improving product availability. Economic diversification efforts in several countries are also contributing to increased consumer spending on packaged food products.Overall, the global processed cheese market continues to evolve through a combination of lifestyle changes, urbanization, and food innovation trends. Across all segments and regions, convenience, versatility, and consistency remain the foundational drivers shaping long-term demand growth.

Key Players in the Processed Cheese Market

- Kraft Heinz Company

- Nestlé S.A.

- Lactalis Group

- Fonterra Co-operative Group

- Arla Foods

- FrieslandCampina

- Savencia Fromage & Dairy

- Bel Group

- Dairy Farmers of America

- Saputo Inc.

- Amul (GCMMF)

- Britannia Industries

- Schreiber Foods

- Sargento Foods

- Bongrain SA