Probiotics Dietary Supplements Market Size

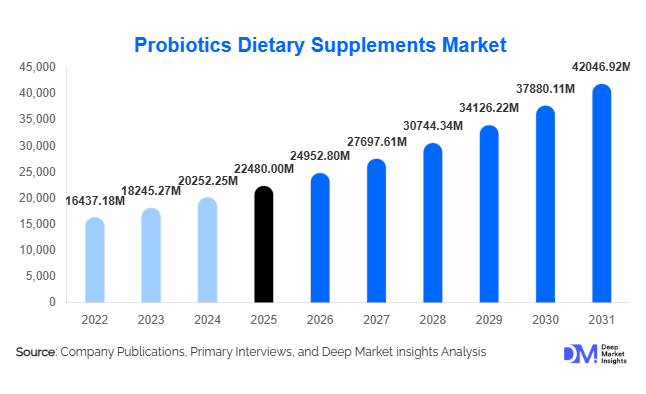

According to Deep Market Insights, the global probiotics dietary supplements market size was valued at USD 22,480 million in 2025 and is projected to grow from USD 24,952.80 million in 2026 to reach USD 41,046.92 million by 2031, expanding at a CAGR of 11.0% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer awareness regarding gut microbiome health, rising adoption of preventive healthcare practices, and expanding scientific validation linking probiotics with immunity, digestion, and mental wellness. Growing demand for natural health solutions, combined with innovation in delivery formats such as gummies and shelf-stable capsules, is accelerating global adoption across multiple consumer age groups.

Key Market Insights

- Preventive healthcare adoption is reshaping supplement consumption globally, positioning probiotics as daily wellness essentials rather than therapeutic products.

- Capsule-based probiotic supplements dominate global demand due to higher stability, convenience, and accurate dosage delivery.

- North America leads global consumption, supported by strong clinical awareness and mature dietary supplement markets.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class populations and rising e-commerce penetration.

- Multi-strain probiotic formulations are gaining popularity as research highlights microbiome diversity benefits.

- Digital retail channels and subscription-based sales models are transforming distribution strategies and improving customer retention.

What are the latest trends in the probiotics dietary supplements market?

Personalized Microbiome Nutrition Emerging as a Core Trend

Personalized nutrition is becoming one of the most transformative trends within the probiotics dietary supplements industry. Advances in microbiome sequencing and diagnostic technologies enable companies to develop customized probiotic formulations tailored to individual gut profiles and lifestyle factors. Subscription-based models combining microbiome testing with ongoing supplement delivery are gaining traction among health-conscious consumers seeking measurable outcomes. Companies are increasingly integrating AI analytics to recommend strain-specific formulations, enhancing consumer engagement and enabling premium pricing strategies. This shift toward personalization is expected to redefine product differentiation and long-term customer loyalty across developed markets.

Expansion of Functional and Multi-Benefit Formulations

Probiotic supplements are evolving beyond digestive health into multifunctional wellness products targeting immunity, mental health, metabolism, and women’s health. The rise of the gut-brain axis concept has encouraged the development of psychobiotic formulations aimed at stress reduction and mood enhancement. Manufacturers are combining probiotics with vitamins, prebiotics, adaptogens, and botanical ingredients to create comprehensive health solutions. Gummy and chewable formats are expanding accessibility among younger consumers and elderly populations, while shelf-stable technologies reduce refrigeration dependency, enabling broader global distribution.

What are the key drivers in the probiotics dietary supplements market?

Growing Awareness of Gut Health and Immunity

Increasing understanding of the relationship between gut microbiota and immune function is significantly driving probiotic adoption. Rising cases of digestive disorders, antibiotic-associated microbiome imbalance, and lifestyle-related health conditions have encouraged consumers to incorporate probiotics into daily wellness routines. Healthcare professionals are increasingly recommending probiotic supplementation, strengthening consumer confidence and accelerating repeat purchases globally.

Shift Toward Preventive Healthcare and Natural Solutions

Consumers are actively transitioning from treatment-based healthcare toward prevention-focused lifestyles. Probiotics align strongly with this trend as natural, non-pharmaceutical solutions supporting long-term health maintenance. Aging populations in developed economies and increasing health consciousness among younger demographics are expanding the addressable consumer base. Government healthcare systems promoting preventive health awareness further reinforce demand growth.

What are the restraints for the global market?

Regulatory Variability Across Countries

Regulatory standards governing probiotic health claims vary widely between regions, creating compliance complexity for global manufacturers. Differences in labeling requirements, strain validation standards, and approval procedures increase operational costs and slow product launches. Companies must invest heavily in clinical evidence to satisfy regional authorities, particularly within Europe.

Product Stability and Shelf-Life Challenges

Maintaining viability of live microorganisms throughout manufacturing, transportation, and storage remains a key technical challenge. Temperature sensitivity and moisture exposure can reduce product efficacy, increasing logistics costs and limiting penetration in regions with underdeveloped cold-chain infrastructure.

What are the key opportunities in the probiotics dietary supplements industry?

Expansion Across Emerging Economies

Emerging markets such as India, Brazil, Indonesia, and the Middle East present significant untapped growth potential. Rising disposable incomes, growing urbanization, and expanding online retail access are enabling probiotic brands to reach new consumers. Government initiatives promoting preventive healthcare are further accelerating supplement adoption, creating strong opportunities for localized manufacturing and region-specific formulations.

Integration with Mental Wellness and Lifestyle Nutrition

The convergence of probiotics with mental wellness and lifestyle nutrition represents a major growth opportunity. Products targeting stress management, sleep improvement, and cognitive wellness are gaining attention due to increasing awareness of the gut-brain connection. Companies developing clinically validated psychobiotic supplements are expected to capture premium consumer segments and expand applications beyond traditional digestive health categories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 22480 Million |

| Market Size in 2026 | USD 24952.80 Million |

| Market Size in 2031 | USD 42046.92 Million |

| CAGR | 11% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global probiotic supplements market demonstrates strong product diversification; however, capsule-based probiotic supplements continue to dominate overall revenue generation, accounting for approximately 34% of total market share in 2025. The leadership of capsules is primarily driven by their superior ability to protect probiotic strains from moisture, oxygen exposure, and gastric acid degradation, which significantly enhances bacterial survival rates and delivery efficiency to the intestinal tract. Technological advancements such as delayed-release coatings, enteric encapsulation, and microencapsulation technologies have further strengthened the effectiveness and credibility of capsule formulations, making them the preferred format among healthcare professionals and clinically focused consumers. Increasing consumer demand for scientifically validated products and higher colony-forming unit (CFU) counts has reinforced capsule adoption across both developed and emerging markets.Gummies and chewable probiotics are emerging as the fastest-growing product category, supported by rising consumer preference for convenient, palatable, and easy-to-consume supplementation formats. These products are particularly popular among younger consumers and first-time supplement users who prioritize taste and lifestyle compatibility. Continuous innovation in sugar-free and plant-based gummy formulations is expanding market penetration among health-conscious buyers. Powder sachets maintain strong relevance in pediatric, therapeutic, and clinical nutrition applications, as they allow flexible dosing, easy mixing with beverages, and customized administration. Additionally, liquid probiotic formats continue to attract niche demand in functional nutrition and hospital-based applications. Overall, innovation in strain stabilization technologies and packaging solutions continues to enhance product efficacy, supporting sustained growth across all product types while reinforcing capsule segment leadership.

Application Insights

Digestive health remains the leading application segment, representing nearly 46% of global demand in 2025, primarily driven by increasing prevalence of gastrointestinal disorders, lifestyle-related digestive discomfort, and growing consumer awareness regarding gut microbiome balance. The strong scientific association between probiotics and improved digestion, reduced bloating, and enhanced nutrient absorption continues to position digestive health as the foundational driver of probiotic supplementation worldwide. Healthcare practitioners frequently recommend probiotics for digestive support, further strengthening this segment’s dominance.Immunity-focused probiotic applications have experienced accelerated expansion following heightened global awareness of preventive healthcare and immune resilience. Consumers increasingly view gut health as directly linked to immune system performance, driving demand for multi-strain formulations targeting immune modulation. Women’s health applications are gaining significant momentum, particularly formulations designed to support vaginal microbiome balance, urinary tract health, and hormonal wellness. Mental wellness represents an emerging high-growth application area, supported by expanding research into the gut–brain axis and the role of probiotics in stress management, mood stabilization, and cognitive well-being. Pediatric applications are also expanding steadily as parents increasingly prioritize microbiome development, allergy prevention, and immune strengthening during early childhood nutrition stages, contributing to long-term market expansion.

Distribution Channel Insights

Online retail and e-commerce platforms represent the fastest-growing distribution channel, accounting for approximately 29% of global sales in 2025. The growth of digital commerce is driven by increasing consumer preference for convenience, broader product selection, and access to educational content supporting informed purchasing decisions. Direct-to-consumer business models enable brands to offer subscription-based services, personalized probiotic recommendations, and competitive pricing strategies, strengthening customer retention and recurring revenue streams. The rapid expansion of health-focused digital marketplaces and mobile commerce platforms continues to accelerate online adoption globally.Pharmacies and drug stores remain highly influential distribution channels, particularly for clinically recommended probiotic products and physician-guided purchases. Consumers often perceive pharmacy-distributed supplements as more trustworthy due to professional validation and regulated product availability. Health and wellness specialty stores attract premium consumers seeking advanced formulations, organic certifications, and targeted health solutions. Meanwhile, supermarkets and hypermarkets maintain strong relevance through mass-market accessibility, impulse purchasing behavior, and private-label product expansion. Digital marketing strategies, influencer-led health education, and social media engagement increasingly shape purchasing behavior, integrating omnichannel retail experiences across global markets.

Consumer Type Insights

General preventive healthcare consumers constitute the largest user segment, accounting for nearly 48% of total market demand as probiotics transition from condition-specific supplements to daily wellness essentials. The growing global emphasis on preventive health management, lifestyle disease prevention, and long-term immunity support has significantly expanded routine probiotic consumption. Consumers increasingly incorporate probiotics into holistic wellness routines alongside vitamins, functional foods, and personalized nutrition strategies, reinforcing consistent market demand.Clinical recommendation users represent a high-value consumer group influenced by physician, dietitian, and pharmacist guidance, particularly in managing digestive disorders, antibiotic recovery, and immune deficiencies. Sports and fitness consumers are rapidly adopting probiotics due to their perceived benefits in nutrient absorption, protein metabolism, inflammation reduction, and post-exercise recovery. Women’s wellness consumers are driving strong demand for gender-specific formulations addressing hormonal balance and microbiome health. Additionally, geriatric populations are increasingly incorporating probiotics into daily healthcare regimens to improve digestive comfort, reduce inflammation, and strengthen immune resilience, supporting sustained long-term market expansion.

Age Group Insights

Adults aged 13–59 years dominate global probiotic consumption, accounting for approximately 52% of market share in 2025. This leadership is primarily driven by rising lifestyle stress, irregular dietary habits, urbanization, and increasing awareness of preventive healthcare practices. Working-age consumers actively seek solutions that support digestion, immunity, and mental wellness, positioning probiotics as a convenient daily health supplement.Pediatric consumption is expanding steadily as parents become increasingly aware of the importance of early microbiome development and immunity enhancement. Pediatricians frequently recommend probiotics for digestive balance and antibiotic-associated gut health recovery, supporting sustained adoption. The geriatric population represents a rapidly growing opportunity due to global aging demographics and increasing incidence of digestive sensitivity and weakened immune function. Product format preferences vary by age group, with younger consumers gravitating toward gummies and chewables due to taste appeal, while older consumers prefer clinically validated capsule formulations offering higher potency and targeted therapeutic benefits.

Explore more data points, trends and opportunities Download Free Sample Report

Probiotics Dietary Supplements Market Segmentations

By Product Type

- Capsules

- Tablets

- Powders & Sachets

- Gummies & Chewables

- Liquid Probiotics

By Application

- Digestive Health

- Immunity Support

- Women’s Health

- Mental Wellness

- Pediatric Health

- General Preventive Wellness

By Distribution Channel

- Online Retail & Direct-to-Consumer

- Pharmacies & Drug Stores

- Health & Wellness Specialty Stores

- Supermarkets & Hypermarkets

- Practitioner & Clinical Sales

By Consumer Type

- General Preventive Healthcare Consumers

- Clinically Recommended Users

- Sports & Fitness Consumers

- Women’s Wellness Consumers

- Geriatric Consumers

Regional Insights

North America

North America accounted for nearly 36% of global probiotic supplement market share in 2025, led primarily by the United States. Regional growth is strongly supported by high healthcare awareness, widespread adoption of dietary supplements as part of daily wellness routines, and strong practitioner recommendations. The presence of advanced nutraceutical manufacturing capabilities, well-established regulatory frameworks, and extensive retail infrastructure further strengthens market maturity. Increasing consumer interest in personalized nutrition, microbiome testing services, and subscription-based supplement delivery models is accelerating innovation. Canada contributes steady growth through pharmacy-led distribution networks, high consumer trust in regulated products, and increasing demand for premium and clinically validated probiotic formulations. Rising prevalence of digestive disorders and lifestyle-related health concerns continues to sustain regional demand expansion.

Europe

Europe holds approximately 27% of the global probiotic supplements market, driven by strong demand across Germany, France, Italy, and the United Kingdom. Regional growth is supported by stringent regulatory standards that enhance consumer confidence and promote high-quality product development. European consumers demonstrate strong preference for evidence-based supplementation, clean-label ingredients, and environmentally sustainable production practices, encouraging manufacturers to invest in advanced strain research and eco-friendly packaging solutions. Growing awareness of gut health, increasing aging populations, and integration of probiotics into preventive healthcare strategies are further accelerating adoption. Expansion of pharmacy chains and specialty health retailers continues to support stable market penetration across Western and Northern Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, experiencing double-digit growth rates driven by expanding middle-class populations, rising disposable incomes, and strong cultural acceptance of fermented foods and functional nutrition. China accounts for nearly 15% of global demand, supported by increasing health awareness, rapid urbanization, and strong e-commerce ecosystem development. India is emerging as the fastest-growing national market due to expanding digital retail penetration, rising preventive healthcare awareness, growing physician recommendations, and increasing consumer education regarding gut health benefits. Japan and South Korea remain technologically advanced markets emphasizing high-quality probiotic strains, scientific innovation, and functional food integration. Regional growth is further supported by increasing demand for immunity-focused products and expanding pediatric nutrition awareness.

Latin America

Latin America is witnessing steady probiotic supplement adoption, led by Brazil and Mexico. Regional growth is driven by increasing digestive health awareness, improving healthcare access, and expanding pharmacy and retail distribution networks. Rising middle-income populations and urbanization trends are enabling greater affordability and accessibility of dietary supplements. Growing penetration of international supplement brands, coupled with localized product offerings tailored to regional dietary habits, is strengthening market expansion. Consumer education campaigns highlighting gut health benefits and increasing preventive healthcare adoption are expected to further accelerate regional growth over the forecast period.

Middle East & Africa

The Middle East & Africa probiotic supplements market is expanding steadily, supported by rising health consciousness and evolving wellness lifestyles. The United Arab Emirates and Saudi Arabia lead regional adoption due to high disposable incomes, strong retail infrastructure, and increasing demand for premium health products. Government-led healthcare awareness initiatives and growing investments in preventive health programs are improving consumer understanding of probiotic benefits. Rapid urbanization, expansion of modern retail channels, and increasing availability of international supplement brands are enhancing market penetration across metropolitan areas. In Africa, gradual improvements in healthcare access, growing middle-class populations, and expanding pharmacy networks are expected to create long-term growth opportunities for probiotic supplement manufacturers.

Key Players in the Probiotics Dietary Supplements Market

- Danone S.A.

- Nestlé Health Science

- Procter & Gamble Co.

- BioGaia AB

- Chr. Hansen Holding A/S

- Yakult Honsha Co., Ltd.

- Kerry Group plc

- ADM (Archer Daniels Midland Company)

- DSM-Firmenich

- Amway Corporation

- Garden of Life LLC

- Nature’s Bounty Co.

- NOW Health Group Inc.

- Jarrow Formulas Inc.

- Himalaya Wellness Company