Probiotic Ingredients Market Size

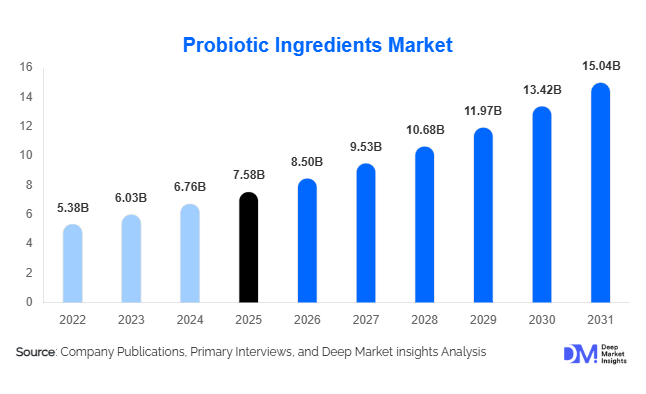

According to Deep Market Insights, the global probiotic ingredients market size was valued at USD 7.58 billion in 2025 and is projected to grow from USD 8.50 billion in 2026 to reach USD 15.04 billion by 2031, expanding at a CAGR of 12.1% during the forecast period (2026–2031). The probiotic ingredients market growth is primarily driven by increasing consumer awareness regarding digestive health, immunity enhancement, microbiome-based wellness, and preventive healthcare solutions. Growing demand for functional foods, dietary supplements, and clinically validated probiotic strains is further accelerating market expansion globally.

Key Market Insights

- Digestive health remains the largest application segment, accounting for a major share of probiotic ingredient demand globally due to rising gastrointestinal disorders and preventive wellness trends.

- Dietary supplements are witnessing rapid growth, particularly probiotic capsules, gummies, powders, and sachets targeted toward immunity and gut health.

- Asia-Pacific dominates the global probiotic ingredients market, led by China, Japan, South Korea, and India due to strong fermented food traditions and expanding nutraceutical industries.

- Plant-based and non-dairy probiotic applications are expanding rapidly, driven by veganism, lactose intolerance awareness, and clean-label consumer preferences.

- Microencapsulation and shelf-stable formulation technologies are improving probiotic survivability and enabling broader product applications.

- Personalized nutrition and microbiome-focused healthcare are emerging as major long-term growth drivers across developed markets.

probiotic ingredients market latest trends

Precision Probiotics and Personalized Nutrition

The probiotic ingredients market is increasingly shifting toward precision nutrition and microbiome-targeted wellness solutions. Consumers are seeking strain-specific probiotic formulations tailored to digestive health, immunity, women’s health, metabolic wellness, and cognitive support. Advances in microbiome sequencing, AI-driven nutritional analysis, and clinical microbiology are enabling companies to develop customized probiotic solutions based on individual gut microbiota profiles. This trend is particularly strong in North America, Japan, and Western Europe, where consumers are willing to pay premium prices for scientifically validated products. Personalized probiotic subscription services and direct-to-consumer wellness platforms are also gaining traction, creating new revenue opportunities for manufacturers and ingredient suppliers.

Expansion of Plant-Based and Functional Beverage Applications

Non-dairy probiotic applications are becoming one of the fastest-growing trends within the market. Rising vegan populations, lactose intolerance concerns, and clean-label preferences are encouraging food manufacturers to introduce plant-based probiotic yogurts, fermented oat drinks, kombucha, probiotic juices, and functional wellness beverages. Ingredient suppliers are investing heavily in heat-stable and shelf-stable probiotic strains suitable for ambient beverage applications. Functional beverages infused with probiotics are increasingly marketed as immunity boosters, digestive wellness enhancers, and energy-support solutions. Additionally, synbiotic formulations combining probiotics and prebiotics are emerging across beverage and snack categories, further strengthening product innovation within the global probiotic ingredients industry.

probiotic ingredients market drivers

Growing Consumer Focus on Digestive and Immune Health

Rising awareness regarding gut microbiome health and immunity enhancement is one of the strongest growth drivers for the probiotic ingredients market. Consumers are increasingly adopting preventive healthcare practices and seeking daily wellness products that support digestive balance and immune function. Increasing prevalence of gastrointestinal disorders such as irritable bowel syndrome (IBS), bloating, constipation, and inflammatory bowel diseases has significantly boosted demand for probiotic supplements and fortified foods. The post-pandemic emphasis on immunity and wellness has further accelerated global probiotic consumption across dietary supplements, beverages, dairy products, and pharmaceuticals.

Rapid Expansion of Functional Foods and Nutraceuticals

The rapid growth of the functional food and nutraceutical industries is creating strong downstream demand for probiotic ingredients. Consumers increasingly prefer food products offering additional health benefits beyond basic nutrition. Functional yogurts, probiotic beverages, fortified snacks, gummies, and wellness powders are becoming mainstream products globally. Food manufacturers are continuously introducing innovative probiotic formulations to cater to rising demand for convenient health solutions. The expansion of e-commerce and direct-to-consumer wellness platforms is also improving accessibility to probiotic products, particularly in emerging economies.

global market restraints

Regulatory Complexity and Health Claim Restrictions

One of the major restraints affecting the probiotic ingredients market is the lack of harmonized global regulatory frameworks regarding probiotic labeling, strain approvals, and health claims. Regulatory agencies across Europe, North America, and Asia maintain varying standards concerning clinical evidence and permitted marketing claims. Particularly in the European Union, stringent regulations surrounding probiotic health claims continue to create commercialization challenges for manufacturers. Regulatory compliance costs and lengthy approval processes may slow innovation and product launches within the industry.

Challenges Related to Stability and Shelf Life

Maintaining probiotic viability throughout manufacturing, transportation, and storage remains a major technical challenge. Probiotic microorganisms are highly sensitive to heat, moisture, oxygen exposure, and processing conditions, requiring specialized encapsulation technologies, cold-chain logistics, and advanced packaging systems. These requirements increase operational and production costs significantly. In developing regions with limited cold-chain infrastructure, maintaining product efficacy and shelf stability can be particularly difficult, restricting wider market penetration.

probiotic ingredients industry key opportunities

Expansion into Emerging Markets

Emerging economies such as India, Brazil, Indonesia, Vietnam, Mexico, and Saudi Arabia present substantial growth opportunities for probiotic ingredient manufacturers. Rapid urbanization, increasing healthcare awareness, rising disposable incomes, and expanding middle-class populations are driving higher demand for functional foods and dietary supplements. Governments in several emerging countries are also promoting preventive healthcare and nutritional fortification programs, indirectly supporting probiotic adoption. International players are increasingly entering these markets through strategic partnerships, localized manufacturing, and region-specific formulations tailored to local consumer preferences.

Growth in Animal Nutrition and Pet Health Applications

Animal nutrition is emerging as a strong opportunity area for probiotic ingredient suppliers. Rising concerns regarding antibiotic resistance and stricter food safety regulations are encouraging livestock and poultry producers to adopt probiotic feed additives as alternatives to antibiotic growth promoters. Probiotics are increasingly used to improve digestion, immunity, and feed efficiency in poultry, aquaculture, swine, and cattle industries. Additionally, premium pet nutrition products containing probiotics are witnessing rapid growth in North America, Europe, and Japan, creating new high-margin opportunities for ingredient manufacturers.

Ingredient Type Insights

Lactobacillus-based probiotic ingredients continue to dominate the global market, accounting for nearly 34% of total market share in 2025. The segment’s leadership is primarily driven by extensive clinical validation supporting digestive health, immune function, and gut microbiome balance, along with widespread incorporation across dietary supplements, functional foods, dairy products, and pharmaceutical formulations. Strong consumer familiarity with Lactobacillus strains, combined with increasing demand for preventive healthcare and wellness-focused nutrition, continues to strengthen segment growth globally. Manufacturers are increasingly utilizing Lactobacillus cultures in capsules, gummies, yogurts, fermented beverages, and synbiotic formulations due to their proven efficacy and formulation versatility. Bifidobacterium strains also represent a major segment within the market, supported by growing applications in infant nutrition, gastrointestinal health products, and immune-support supplements. Rising awareness regarding pediatric gut health and microbiome development is significantly increasing adoption of Bifidobacterium-based products across Asia-Pacific and Europe. Spore-forming probiotics, particularly Bacillus strains, are witnessing rapid market expansion because of their superior shelf stability, heat resistance, and compatibility with ambient storage and processing conditions, making them increasingly attractive for functional food and beverage manufacturers. Meanwhile, yeast-based probiotics such as Saccharomyces boulardii continue to experience strong demand growth within pharmaceutical and therapeutic applications due to increasing clinical evidence supporting their effectiveness in antibiotic-associated diarrhea management and gastrointestinal disorder treatment.

Form Insights

Dry probiotic ingredients represent the leading form segment, contributing approximately 61% of global market demand in 2025. The dominance of the dry form segment is driven by its superior shelf stability, extended product lifespan, lower transportation and storage costs, and broad compatibility with capsules, tablets, sachets, powdered beverages, and functional food applications. Freeze-dried powders and granules remain the preferred formats among manufacturers due to their ability to maintain microbial viability throughout large-scale production and distribution processes. Growing global demand for convenient dietary supplements and shelf-stable wellness products continues to support strong adoption of dry probiotic ingredients across both developed and emerging markets. Encapsulated probiotic ingredients are also witnessing significant growth as manufacturers increasingly adopt advanced microencapsulation technologies to improve probiotic survivability during food processing, storage, and gastrointestinal digestion. These technologies are becoming particularly important for premium nutraceutical and pharmaceutical applications where strain stability and targeted delivery are critical performance factors. Liquid probiotic formulations remain an important segment, especially within fermented dairy beverages, probiotic wellness shots, kombucha products, and ready-to-drink functional beverages. Demand for liquid probiotics remains particularly strong across Asia-Pacific and Europe, where fermented food traditions and daily probiotic beverage consumption continue to support market expansion.

Application Insights

Dietary supplements account for nearly 37% of total probiotic ingredient consumption globally, making them the largest application segment within the market. The segment’s growth is primarily driven by rising consumer preference for convenient daily wellness products that support digestive health, immunity, and overall microbiome balance. Increasing awareness regarding preventive healthcare, coupled with growing adoption of self-care and personalized nutrition trends, continues to accelerate demand for probiotic capsules, gummies, powders, tablets, and sachets across North America, Europe, and Asia-Pacific. The expanding aging population and rising incidence of digestive disorders are further contributing to higher supplement consumption globally. Functional food and beverage applications also represent a major growth area, supported by increasing demand for probiotic yogurt, fermented dairy products, kombucha, functional juices, and plant-based wellness beverages. Food manufacturers are increasingly incorporating probiotics into everyday products to meet consumer demand for health-enhancing foods with clean-label positioning. Pharmaceutical applications are steadily expanding due to increasing clinical evidence supporting probiotics in gastrointestinal, metabolic, and immune-related treatments. Growing physician acceptance of probiotics as adjunct therapies is encouraging pharmaceutical companies to invest in clinically validated strains and therapeutic probiotic formulations. Additionally, personal care applications including probiotic skincare, oral care, and beauty-from-within products are emerging as rapidly growing niche segments, supported by rising consumer interest in microbiome-focused beauty and wellness solutions.

End-Use Industry Insights

Food and beverage manufacturers remain the largest end-use industry segment, accounting for nearly 41% of global probiotic ingredient demand in 2025. The segment’s dominance is driven by rising global consumption of functional dairy products, fermented beverages, fortified snacks, and wellness-oriented food products enriched with probiotic cultures. Increasing consumer preference for functional nutrition and digestive wellness foods continues to encourage manufacturers to expand probiotic product portfolios across mainstream retail channels. Nutraceutical companies are witnessing the fastest growth among end-use industries due to rapidly increasing demand for preventive healthcare supplements, immunity-support formulations, and microbiome wellness products. The growing popularity of personalized nutrition and daily supplementation trends is further supporting demand for high-potency and clinically validated probiotic ingredients. Pharmaceutical companies are also increasingly incorporating probiotics into gastrointestinal, immunity-focused, and antibiotic-support formulations as scientific research continues to validate probiotic therapeutic benefits. In addition, animal feed manufacturers are emerging as important consumers of probiotic ingredients as livestock producers increasingly seek sustainable alternatives to antibiotic growth promoters. Rising regulatory restrictions on antibiotic use in animal nutrition and growing focus on livestock gut health are expected to support long-term growth within the animal feed probiotic segment.

Distribution Channel Insights

Direct B2B ingredient supply continues to dominate the probiotic ingredients market as major food, pharmaceutical, and nutraceutical manufacturers prefer sourcing probiotic cultures directly from specialized ingredient suppliers to ensure quality consistency, strain traceability, and technical formulation support. The leading position of this distribution channel is supported by long-term supply agreements, increasing demand for customized strain development, and growing regulatory requirements related to probiotic efficacy and stability. Specialty ingredient distributors also play a critical role in expanding regional market penetration by offering localized technical expertise, formulation assistance, and regulatory guidance to manufacturers operating in diverse markets. Online ingredient procurement platforms are gaining traction among small and mid-sized manufacturers due to increasing digitalization of sourcing activities, improved pricing transparency, and simplified global procurement processes. These platforms are enabling easier access to specialty probiotic ingredients for emerging supplement and functional food brands. Contract manufacturing partnerships are also expanding rapidly as supplement and food companies increasingly outsource product development, formulation, and manufacturing activities to specialized third-party producers in order to reduce operational costs, accelerate commercialization timelines, and improve scalability.

| By Ingredient Type | By Form | By Application | By Functionality | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the global probiotic ingredients market, led primarily by the United States. Strong consumer awareness regarding digestive health, increasing adoption of dietary supplements, and growing interest in personalized nutrition continue to support regional market expansion. The United States represents the largest regional market due to high consumption of probiotic gummies, capsules, functional beverages, and microbiome-focused wellness products. Rising prevalence of digestive disorders, increasing healthcare expenditure, and growing demand for preventive wellness solutions are further accelerating probiotic ingredient adoption across the country. Canada is also witnessing rising demand for plant-based probiotic foods, fermented beverages, and clean-label nutritional products as consumers increasingly prioritize holistic health and immunity support. In addition, the region benefits from advanced clinical research infrastructure, strong probiotic innovation activity, significant investment in microbiome science, and the presence of major nutraceutical and functional food manufacturers. Expanding e-commerce penetration and increasing availability of premium wellness products through retail and online channels are further supporting regional growth.

Europe

Europe contributes nearly 24% of global probiotic ingredient demand, with Germany, France, the United Kingdom, Italy, and the Netherlands representing major regional markets. Germany remains a leading consumer of probiotic supplements and pharmaceutical formulations due to its advanced healthcare system, mature nutraceutical industry, and strong consumer focus on digestive wellness. France and Italy continue to maintain robust demand for probiotic dairy products, fermented foods, and functional nutrition applications driven by longstanding consumer familiarity with gut health products. The United Kingdom is witnessing increasing adoption of probiotic supplements and microbiome-focused wellness products as awareness regarding immunity and preventive healthcare continues to expand. Regional growth is further supported by rising aging populations, increasing demand for clean-label functional foods, and growing investment in microbiome research and clinical validation. However, relatively strict European Union regulations regarding probiotic health claims and product labeling continue to influence commercialization strategies and marketing approaches within the region. Despite regulatory complexity, manufacturers continue to invest heavily in scientifically validated probiotic strains to strengthen product differentiation and consumer trust.

Asia-Pacific

Asia-Pacific dominates the global probiotic ingredients market with approximately 39% share in 2025 and remains the fastest-growing regional market globally. China leads regional demand due to rapid expansion of functional foods, infant nutrition products, dietary supplements, and immunity-support formulations. Rising disposable incomes, increasing urbanization, and growing health consciousness among middle-class consumers continue to drive probiotic consumption across the country. Japan remains one of the world’s most mature probiotic markets because of longstanding consumer familiarity with fermented foods, scientifically validated wellness products, and daily probiotic consumption habits. South Korea continues to witness strong demand for probiotic beverages, beauty-from-within nutrition products, and functional skincare applications supported by the country’s highly developed wellness and beauty industries. India is emerging as one of the fastest-growing markets globally, with CAGR exceeding 14%, supported by rapid urbanization, rising healthcare awareness, increasing prevalence of digestive disorders, expanding nutraceutical manufacturing, and growing demand for preventive healthcare supplements. Additionally, expanding retail infrastructure, rapid e-commerce growth, and increasing investments by international probiotic manufacturers are accelerating regional market penetration across Asia-Pacific.

Latin America

Latin America is witnessing steady growth in probiotic ingredient consumption, particularly across Brazil and Mexico. Expanding middle-class populations, improving awareness regarding digestive wellness, and increasing demand for fortified dairy products and nutritional supplements are supporting regional market expansion. Brazil remains the dominant regional market due to its large dairy processing industry, growing supplement consumption, and rising demand for functional beverages and probiotic yogurts. Mexico is also experiencing increasing adoption of probiotic products as consumers become more focused on immunity support and preventive healthcare solutions. Regional growth is further supported by increasing urbanization, improving retail accessibility, and rising investment by international ingredient manufacturers entering the market through partnerships with local food and nutraceutical companies. The growing popularity of affordable wellness products and increasing penetration of modern retail channels are expected to continue driving probiotic ingredient demand across the region.

Middle East & Africa

The Middle East & Africa region currently represents a smaller share of the global probiotic ingredients market but offers strong long-term growth potential. Saudi Arabia and the United Arab Emirates are witnessing rising demand for premium wellness supplements, immunity-focused products, and functional beverages due to increasing health awareness, growing disposable incomes, and expanding preventive healthcare initiatives. The region is also benefiting from increasing adoption of Western dietary supplement trends and rapid expansion of modern retail and e-commerce channels. South Africa remains the leading African market due to improving retail penetration, expanding middle-class populations, and rising awareness regarding digestive health and nutritional wellness. Government initiatives aimed at improving nutritional standards, preventive healthcare infrastructure, and food fortification programs are expected to support long-term regional growth. Increasing investment by international nutraceutical and food companies, along with rising demand for functional nutrition products among younger consumers, is expected to further accelerate probiotic ingredient adoption across the Middle East & Africa over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Probiotic Ingredients Market

- Chr. Hansen

- Danone

- Yakult Honsha

- IFF

- Lallemand

- Probi

- BioGaia

- Kerry Group

- DSM-Firmenich

- Nestlé Health Science

- Morinaga Milk Industry

- Sabinsa

- ADM

- Novonesis

- Kaneka Corporation