Probiotic and Prebiotic Pet Foods Market Size

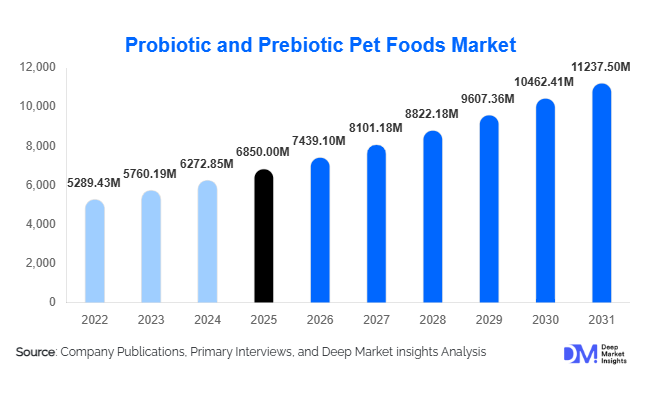

According to Deep Market Insights, the global probiotic and prebiotic pet foods market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,439.10 million in 2026 to reach USD 11,237.50 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing pet humanization trends, growing awareness of digestive and immune health in companion animals, and rising demand for premium functional pet nutrition products.

Pet owners worldwide are increasingly seeking scientifically formulated diets enriched with probiotics, prebiotics, and synbiotic blends to support gut health, immunity, and nutrient absorption. Manufacturers are responding with advanced strain-specific formulations, encapsulated probiotic technologies for stability in dry kibble, and fiber-enriched wet foods and treats. North America currently dominates the global market, while Asia-Pacific is emerging as the fastest-growing region due to rapid urbanization and rising disposable incomes. Expanding e-commerce penetration and veterinary-backed therapeutic diet adoption are further accelerating growth.

Key Market Insights

- Probiotic-based formulations account for over 52% of total revenue, driven by strong clinical validation and consumer familiarity with gut health benefits.

- Dogs represent nearly 64% of total demand, reflecting higher global dog ownership and greater per-pet spending compared to cats.

- Premium and super-premium price tiers contribute over 57% of global revenue, supported by rising willingness to pay for functional and therapeutic nutrition.

- North America holds approximately 38% market share, led by the U.S., while Asia-Pacific is growing at over 11% CAGR.

- Online retail channels are expanding rapidly, driven by subscription-based pet nutrition models and D2C brand strategies.

- Encapsulation and strain stabilization technologies are reshaping product innovation and extending shelf life in dry food applications.

What are the latest trends in the probiotic and prebiotic pet foods market?

Personalized and Breed-Specific Microbiome Nutrition

Advancements in microbiome science are enabling the development of breed-specific and life-stage-specific probiotic blends. Manufacturers are leveraging data analytics and veterinary research to create targeted formulations addressing digestive sensitivities, immunity gaps, and age-related gut health decline. Subscription-based personalized pet food services are emerging, allowing pet owners to receive customized probiotic-enriched meals based on health profiles and breed requirements. This precision nutrition approach mirrors human nutraceutical trends and supports premium pricing strategies.

Expansion of Synbiotic and Functional Treats

Synbiotic products—combining probiotics and prebiotics—are gaining traction as comprehensive gut health solutions. Functional treats and chews enriched with digestive-support strains are becoming popular among pet owners seeking convenient supplementation formats. Freeze-dried and raw formulations incorporating stabilized probiotic cultures are also expanding in specialty retail channels. As a result, manufacturers are investing in encapsulation technologies to ensure bacterial viability throughout processing and storage.

What are the key drivers in the probiotic and prebiotic pet foods market?

Pet Humanization and Premiumization

Pet owners increasingly consider pets as family members, driving demand for high-quality, functional nutrition. Premium and super-premium pet food categories are growing significantly faster than economy tiers. Consumers are willing to pay higher prices for products offering digestive health, immune support, and clinically supported benefits. This shift has expanded shelf space for probiotic-enriched kibble and veterinary therapeutic diets.

Growing Veterinary Endorsement of Gut Health

Veterinary clinics and hospitals are actively recommending probiotic supplementation to manage gastrointestinal disorders, antibiotic recovery, and stress-related digestive issues. Therapeutic diets formulated with specific probiotic strains are experiencing double-digit growth in several developed markets. Scientific validation and clinical trials are strengthening consumer confidence and supporting regulatory compliance for functional claims.

What are the restraints for the global market?

Regulatory Complexity and Health Claim Limitations

Regulations surrounding probiotic labeling and health claims vary significantly across regions, creating compliance challenges for global manufacturers. Restrictions on therapeutic positioning can limit marketing effectiveness and slow product approvals in certain markets.

High Ingredient and Stabilization Costs

Probiotic strains require specialized fermentation, encapsulation, and cold-chain management processes, increasing production costs. Prebiotic fibers, such as inulin and FOS, also face price volatility due to agricultural input fluctuations. These cost pressures can impact margins, particularly in price-sensitive emerging markets.

What are the key opportunities in the probiotic and prebiotic pet foods industry?

Emerging Market Penetration in Asia-Pacific and Latin America

Rapid urbanization and rising disposable incomes in China, India, and Brazil are driving pet adoption and premium food demand. Mid-premium probiotic formulations tailored for price-sensitive consumers present significant expansion opportunities. Local manufacturing partnerships and region-specific marketing strategies can accelerate penetration.

Veterinary Therapeutic Diet Integration

The integration of probiotics into prescription and therapeutic diets for gastrointestinal management represents a high-margin opportunity. Collaboration with veterinary networks and clinical research institutions can strengthen brand positioning and expand institutional sales channels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7439.10 Million |

| Market Size in 2031 | USD 11237.50 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

Probiotic pet foods dominate the global market, accounting for approximately 52% of total revenue in 2025, making them the leading ingredient segment. The primary driver behind this dominance is strong scientific validation and high consumer awareness regarding the role of live beneficial bacteria in supporting digestive balance, nutrient absorption, and immune resilience. Veterinary endorsements and increased research on gut microbiota have significantly strengthened consumer confidence in probiotic-enriched formulations. Multi-strain blends incorporating Lactobacillus, Bifidobacterium, and Bacillus species are widely used in premium dry kibble due to their proven survivability and efficacy. Advanced microencapsulation technologies further enhance bacterial stability during high-temperature extrusion processes, supporting large-scale commercial adoption.

Prebiotic formulations hold the second-largest share, driven by demand for plant-based fiber ingredients such as inulin, FOS, and MOS that stimulate beneficial gut bacteria growth. Synbiotic products are the fastest-growing sub-segment, benefiting from their combined functional advantage and increasing positioning within premium and therapeutic product lines.

Pet Type Insights

Dogs represent nearly 64% of global market demand in 2025, making them the leading pet type segment. The key growth driver is higher per-pet spending and greater global dog ownership, particularly in North America and Europe. Dog owners are more likely to invest in functional nutrition, including digestive-support diets and probiotic-enriched treats. Adult dog formulations account for the largest share within this segment, supported by routine preventive healthcare trends. However, senior dog digestive health products are expanding rapidly due to aging pet demographics and increased veterinary recommendations for gut health management.

Cats contribute approximately 30% of total revenue, with wet food applications showing strong probiotic integration. The rising trend of indoor cat ownership and sensitivity-related digestive issues is driving steady adoption in this segment.

Product Form Insights

Dry kibble leads the market with nearly 48% revenue share in 2025, primarily driven by its affordability, convenience, and compatibility with encapsulated probiotic strains. The scalability of dry food manufacturing and extended shelf life make it the preferred format for mass-market distribution. Technological advancements in strain stabilization during extrusion have further reinforced dry kibble’s dominance.

Wet food holds around 28% share, particularly strong in feline nutrition due to palatability and hydration benefits. Functional treats and chews are the fastest-growing format, supported by consumer preference for convenient supplementation. Freeze-dried and raw formulations are expanding in premium and specialty retail segments, driven by natural and minimally processed positioning.

Distribution Channel Insights

Pet specialty stores account for approximately 34% of total revenue, making them the leading distribution channel. The primary driver is the availability of expert guidance and premium product portfolios, which are crucial for functional and therapeutic nutrition purchases. Consumers often rely on in-store recommendations when selecting probiotic-enhanced diets. Online retail is the fastest-growing channel, supported by subscription-based delivery models, auto-replenishment systems, and direct-to-consumer brand strategies. Veterinary clinics contribute significantly to therapeutic and prescription diet sales, particularly for gastrointestinal management and post-antibiotic recovery nutrition.

Price Tier Insights

Premium and super-premium segments collectively represent approximately 57% of global revenue in 2025, making them the dominant price category. The growth driver here is strong consumer willingness to pay for clinically supported functional benefits and high-quality ingredients. Premium positioning allows manufacturers to maintain profit margins ranging between 18–25%, supported by differentiated formulations and brand trust.

Mid-premium tiers are expanding rapidly in emerging markets, offering affordable probiotic integration for price-sensitive consumers. Economy segments show limited probiotic penetration due to ingredient cost constraints.

Explore more data points, trends and opportunities Download Free Sample Report

Probiotic and Prebiotic Pet Foods Market Segmentations

By Ingredient Type

- Probiotic Pet Foods

- Prebiotic Pet Foods

- Synbiotic Pet Foods

By Pet Type

- Dogs

- Cats

- Other Pets

By Product Form

- Dry Food (Kibble)

- Wet/Canned Food

- Freeze-Dried & Raw

- Functional Treats & Chews

- Supplements (Powder, Capsules, Liquid)

By Distribution Channel

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Veterinary Clinics & Hospitals

- Online Retail (E-commerce & D2C)

- Farm & Feed Stores

By Price Tier

- Economy

- Mid-Premium

- Premium

- Super-Premium / Therapeutic

Regional Insights

North America

North America holds approximately 38% of global revenue in 2025, with the United States accounting for nearly 85% of regional demand. The primary growth drivers include high pet ownership rates, elevated pet healthcare expenditure, and strong premiumization trends. The U.S. market benefits from advanced veterinary infrastructure, high consumer awareness of microbiome health, and widespread availability of premium retail chains. Canada contributes steadily, supported by the rising adoption of therapeutic veterinary diets and strong e-commerce penetration. Continuous product innovation and private-label premium launches further reinforce regional leadership.

Europe

Europe represents around 29% of the global market share, driven by strong demand in Germany, the UK, and France. The key regional growth driver is consumer preference for natural, non-GMO, and clinically validated ingredients. Germany leads the region due to strict quality standards and high acceptance of functional nutrition. The UK market is fueled by premium pet food retail chains and growing D2C adoption. Increasing regulatory clarity around functional claims is also encouraging innovation and product launches across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 22% of global revenue and is the fastest-growing region, expanding at over 11% CAGR. Rapid urbanization, rising disposable incomes, and increasing pet adoption in China are major growth drivers. China leads regional expansion due to premiumization trends and growth in cross-border e-commerce. Japan and Australia represent mature markets with strong demand for high-quality and specialty formulations. India is emerging as a high-growth mid-premium market, supported by expanding retail infrastructure and growing awareness of pet digestive health.

Latin America

Latin America contributes around 7% of global revenue, with Brazil representing nearly 45% of regional demand. Growth is primarily driven by increasing pet humanization, expanding middle-class income, and improving retail distribution networks. Mexico follows as a key contributor, benefiting from rising supermarket penetration and specialty pet store expansion. Gradual premium adoption and growing veterinary awareness are supporting probiotic product demand.

Middle East & Africa

The Middle East & Africa region accounts for approximately 4% of global revenue. The UAE leads regional demand due to high disposable income levels and a strong preference for premium imported brands. South Africa remains the largest African contributor, supported by an established pet food manufacturing infrastructure. Growth drivers include urbanization, rising expatriate populations, and expanding organized pet retail networks. Although penetration remains relatively low compared to developed markets, increasing awareness of pet wellness is expected to drive steady expansion in the coming years.

Key Players in the Probiotic and Prebiotic Pet Foods Market

- Mars Petcare

- Nestlé Purina PetCare

- Hill's Pet Nutrition

- Colgate-Palmolive

- Blue Buffalo

- Wellness Pet Company

- Diamond Pet Foods

- General Mills

- Heristo AG

- Virbac

- ADM

- Alltech

- Farmina Pet Foods

- Champion Petfoods

- Affinity Petcare