Proanthocyanidin Market Size

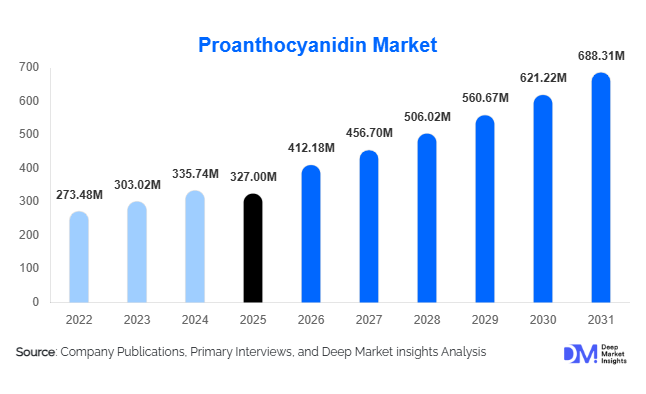

According to Deep Market Insights,the global proanthocyanidin market size was valued at USD 372 million in 2025 and is projected to grow from USD 412.18 million in 2026 to reach USD 688.31 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for plant-based antioxidants, rising adoption of preventive healthcare supplements, and expanding applications of proanthocyanidins across nutraceuticals, cosmetics, functional foods, and pharmaceutical formulations. Growing scientific validation supporting cardiovascular, anti-inflammatory, and anti-aging benefits is accelerating global adoption, while technological advancements in botanical extraction are improving product standardization and commercial scalability.

Key Market Insights

- Dietary supplements remain the largest application segment, accounting for nearly half of global consumption due to strong consumer preference for antioxidant-based wellness products.

- Grape seed extract dominates raw material sourcing, supported by abundant availability from wine industry by-products and high OPC concentration levels.

- North America leads global consumption, driven by mature nutraceutical markets and preventive healthcare spending.

- Asia-Pacific is the fastest-growing region, supported by expanding middle-class populations and rising herbal supplement adoption.

- High-purity proanthocyanidin extracts (>75% OPC) are gaining traction due to clinical-grade applications and premium supplement positioning.

- Technological innovation in green extraction methods, including supercritical CO₂ processing, is improving yield efficiency and sustainability compliance.

What are the latest trends in the proanthocyanidin market?

Shift Toward Functional Foods and Beverages

Proanthocyanidins are increasingly incorporated into functional foods and beverages as manufacturers respond to consumer demand for convenient wellness products. Antioxidant-enriched beverages, fortified snacks, and ready-to-drink formulations are emerging as key growth areas. Food companies are developing water-soluble extracts that maintain stability without altering flavor profiles, enabling broader commercialization beyond capsules and tablets. This transition reflects a broader industry movement toward everyday nutrition solutions rather than episodic supplementation.

Rise of Nutricosmetics and Beauty-from-Within Products

The convergence of nutrition and personal care is transforming market demand. Cosmetic brands are integrating proanthocyanidins into ingestible beauty supplements targeting skin elasticity, collagen protection, and anti-aging benefits. Consumers increasingly prefer natural alternatives to synthetic ingredients, encouraging cosmetic companies to invest in clinically supported botanical actives. The nutricosmetics trend is expanding distribution into beauty retail channels and strengthening cross-industry collaboration between nutraceutical and skincare manufacturers.

What are the key drivers in the proanthocyanidin market?

Growing Preventive Healthcare Awareness

Rising incidence of cardiovascular diseases, metabolic disorders, and aging-related health concerns is driving adoption of antioxidant supplements globally. Consumers are proactively investing in preventive healthcare solutions, positioning proanthocyanidins as essential wellness ingredients. Physician recommendations and expanding clinical research further support market credibility and long-term demand growth.

Expansion of Botanical and Clean-Label Ingredients

Clean-label trends are encouraging manufacturers to replace synthetic additives with plant-derived bioactives. Proanthocyanidins align with consumer expectations for transparency, sustainability, and natural sourcing. Food, supplement, and cosmetic brands increasingly highlight botanical origins as marketing differentiators, accelerating ingredient adoption across multiple industries.

What are the restraints for the global market?

Raw Material Supply Volatility

The availability and pricing of grape seeds and pine bark depend heavily on agricultural output and wine industry cycles. Seasonal fluctuations and climate variability can influence extraction costs, creating pricing instability for manufacturers and buyers.

Regulatory and Health Claim Limitations

Regulatory frameworks differ significantly across regions, particularly regarding botanical health claims. Compliance requirements increase product development timelines and operational costs, posing challenges for smaller manufacturers attempting global expansion.

What are the key opportunities in the proanthocyanidin industry?

Clinical-Grade Nutraceutical Development

Growing clinical validation of polyphenols presents opportunities for pharmaceutical-grade formulations targeting cardiovascular and vascular health. Companies investing in standardized extracts and clinical trials can access premium healthcare channels and physician-recommended supplement markets, significantly improving margins.

Expansion in Emerging Markets

Rapid urbanization and rising disposable income across Asia-Pacific and Latin America are creating new growth avenues. Countries such as China, India, Brazil, and Indonesia are witnessing strong growth in herbal supplement consumption. Localized product formats and affordable dosage options enable companies to penetrate high-growth consumer bases.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 327 Million |

| Market Size in 2026 | USD 412.18 Million |

| Market Size in 2031 | USD 688.31 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Grape seed extract remains the dominant source segment in the global proanthocyanidin market, accounting for approximately 44% of total revenue. Its leadership position is primarily driven by the high concentration of oligomeric proanthocyanidins (OPCs), strong antioxidant efficacy, and cost-efficient availability derived from wine industry by-products, enabling large-scale and sustainable raw material sourcing. Increasing utilization of circular economy practices within the food and beverage sector further strengthens supply stability and pricing advantages for grape-derived extracts. Pine bark extract maintains a strong premium niche supported by extensive clinical validation, particularly in cardiovascular health, circulation improvement, and anti-inflammatory formulations, allowing manufacturers to position these ingredients within high-value nutraceutical and pharmaceutical applications. Cranberry and berry-derived extracts are gaining traction due to growing consumer focus on urinary tract health, immune support, and women’s wellness supplements, while expanding scientific evidence continues to reinforce their functional benefits. Meanwhile, cocoa and apple-based proanthocyanidin sources are emerging within functional foods and beverages as manufacturers diversify botanical sourcing strategies to meet clean-label demands and develop differentiated antioxidant-rich formulations.

Product Form Insights

Powdered proanthocyanidin extracts lead the global market with an estimated 36% share, primarily driven by their superior formulation flexibility, extended shelf stability, and compatibility across a wide range of applications including dietary supplements, functional beverages, bakery fortification, and ingredient premixes. The leading position of powdered formats is further supported by ease of transportation, scalable manufacturing integration, and cost efficiency for bulk ingredient buyers. Capsules and tablets continue to maintain strong market presence within retail supplements due to consumer familiarity, dosage accuracy, and convenience in daily consumption routines. Liquid extracts are witnessing expanding adoption in functional beverages, wellness shots, and personalized nutrition solutions as liquid delivery formats align with fast-acting absorption trends and ready-to-drink product innovation. Softgel formulations are increasingly used in premium supplement categories where enhanced bioavailability, ingredient protection from oxidation, and precise dosing are critical for high-value clinical positioning.

Purity Level Insights

High-purity proanthocyanidin extracts containing more than 75% OPC represent approximately 41% of global demand and constitute the leading purity segment, driven by increasing preference for clinically standardized and scientifically validated ingredients. The growing emphasis on efficacy, regulatory compliance, and measurable health outcomes encourages manufacturers to invest in advanced purification technologies such as solvent-free extraction and chromatography-based refinement. High-purity extracts enable product differentiation within premium nutraceutical, pharmaceutical, and medical nutrition segments while supporting health claims backed by clinical research. Rising regulatory scrutiny across developed markets further accelerates demand for standardized purity levels, ensuring consistent bioactivity, improved formulation reliability, and enhanced consumer trust in botanical supplements.

Application Insights

Dietary supplements dominate application demand, contributing nearly 48% of global market revenue, primarily driven by increasing consumer adoption of preventive healthcare practices and growing awareness regarding antioxidant supplementation for cardiovascular, skin, and immune health. The leading position of this segment is supported by expanding aging populations, rising lifestyle-related health concerns, and strong global penetration of nutraceutical retail channels. Functional foods and beverages represent the fastest-growing application category as food manufacturers increasingly incorporate proanthocyanidins into everyday consumption products such as fortified drinks, nutrition bars, and wellness snacks to deliver convenient health benefits. Cosmetics and personal care applications continue expanding through nutricosmetics and dermaceutical innovations, where proanthocyanidins are valued for collagen protection, anti-aging effects, and skin oxidative stress reduction, aligning with beauty-from-within product positioning.

Distribution Channel Insights

B2B ingredient supply dominates distribution channels with approximately 52% market share, driven by large-scale procurement of standardized botanical extracts by nutraceutical, pharmaceutical, and cosmetic manufacturers seeking consistent quality and long-term supplier partnerships. Ingredient manufacturers increasingly engage in contract manufacturing and customized formulation development, strengthening B2B channel expansion. Online retail and direct-to-consumer distribution channels are growing rapidly as digital health awareness, subscription-based supplement models, and cross-border e-commerce platforms improve accessibility to specialty botanical supplements. The integration of digital marketing strategies, influencer-led wellness promotion, and personalized nutrition platforms continues to accelerate online sales growth globally.

End-Use Industry Insights

The nutraceutical industry accounts for nearly 46% of total demand, making it the leading end-use sector due to sustained global growth in dietary supplement consumption and increasing consumer preference for plant-derived functional ingredients. The expansion of preventive healthcare models and physician-recommended supplementation further strengthens market penetration within this segment. Cosmetics and personal care represent the fastest-growing end-use industry, supported by rising demand for anti-aging solutions, natural beauty formulations, and ingestible skincare products aligned with holistic wellness trends. Functional food manufacturers are progressively incorporating proanthocyanidins into antioxidant beverages, dairy alternatives, and fortified snacks to enhance nutritional value and product differentiation. Pharmaceutical applications are expanding gradually as clinical research continues to validate proanthocyanidins for vascular health, inflammation management, and adjunct therapeutic formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Proanthocyanidin Market Segmentations

By Source

- Grape Seed Extract

- Pine Bark Extract

- Cranberry Extract

- Blueberry & Berry Extracts

- Cocoa Extract

- Apple & Other Botanical Sources

By Product Form

- Powder Extracts

- Capsules & Tablets

- Liquid Extracts

- Softgels

- Functional Ingredient Premixes

By Purity Level

- Below 40% OPC

- 40%–75% OPC

- Above 75% OPC (High-Purity Extracts)

By Application

- Dietary Supplements

- Functional Foods & Beverages

- Cosmetics & Personal Care

- Pharmaceutical Applications

- Animal Nutrition

By Distribution Channel

- B2B Ingredient Supply

- Online Retail & E-commerce

- Pharmacies & Health Stores

- Specialty Nutraceutical Retailers

- Direct-to-Consumer (Brand Websites)

By End-Use Industry

- Nutraceutical Industry

- Food & Beverage Industry

- Cosmetics & Personal Care Industry

- Pharmaceutical Industry

- Animal Health Industry

Regional Insights

North America

North America holds approximately 34% of the global proanthocyanidin market share, led by the United States, where dietary supplement penetration, preventive healthcare awareness, and high consumer spending on wellness products remain well established. Regional growth is driven by increasing adoption of scientifically backed nutraceuticals, strong presence of leading supplement brands, and advanced retail and e-commerce infrastructure supporting widespread product availability. Physician endorsement of antioxidant supplementation and rising demand for clean-label botanical ingredients further stimulate market expansion. Canada contributes steady growth through rising consumer preference for natural health products, regulatory support for standardized botanical extracts, and growing demand for functional foods aligned with healthy aging trends.

Europe

Europe accounts for nearly 24% of global demand, supported by major markets including Germany, France, Italy, and Spain. Regional growth is strongly influenced by stringent quality and safety regulations that favor high-purity botanical extracts, enabling premium pricing strategies and encouraging innovation in standardized formulations. Increasing consumer awareness of sustainability and ethical sourcing drives demand for traceable supply chains and certified raw materials. The region also benefits from established herbal medicine traditions and expanding adoption of nutraceuticals within preventive healthcare frameworks, while clean-label product development and plant-based nutrition trends continue to reinforce long-term market growth.

Asia-Pacific

Asia-Pacific represents around 29% of the global market and is the fastest-growing region, supported by expanding middle-class populations, rising disposable incomes, and increasing awareness of preventive health management. China leads global manufacturing and export activity due to large-scale botanical extraction capabilities and cost-efficient production infrastructure. Japan’s rapidly aging population significantly drives demand for cardiovascular and anti-aging supplements, while innovation in functional foods accelerates ingredient adoption. India is emerging as a high-growth market fueled by expanding herbal medicine acceptance, integration of traditional wellness systems with modern nutraceuticals, and rapid growth of online supplement retail platforms that improve product accessibility across urban and semi-urban populations.

Latin America

Latin America holds approximately 6% market share, led by Brazil and Mexico, where improving healthcare awareness and expanding nutraceutical manufacturing capabilities are driving demand for antioxidant ingredients. Regional growth is supported by increasing consumer interest in natural health products, rising fitness and wellness culture, and growing availability of dietary supplements through pharmacy and specialty retail channels. Local food and beverage manufacturers are also incorporating botanical antioxidants into functional products to address increasing demand for immunity and wellness-focused nutrition.

Middle East & Africa

The Middle East & Africa region accounts for about 7% of global consumption, supported by rising health consciousness and expanding modern retail infrastructure. The United Arab Emirates serves as a major supplement import and distribution hub due to strong expatriate demand and premium wellness product availability. Growth in South Africa is driven by expanding pharmacy retail networks, increasing awareness of lifestyle-related diseases, and growing adoption of preventive nutrition solutions. Increasing investments in healthcare infrastructure, coupled with rising demand for natural and plant-based supplements, are expected to support gradual but steady regional market expansion.

Key Players in the Proanthocyanidin Market

- Naturex (Givaudan)

- Indena S.p.A.

- Nexira

- Euromed S.A.

- Diana Food (Symrise)

- Polyphenolics

- Botaniex Inc.

- Xi’an Lyphar Biotech Co., Ltd.

- Shaanxi Hongda Phytochemistry Co., Ltd.

- Hunan Nutramax Inc.

- Chengdu Wagott Bio-Tech Co., Ltd.

- Nutra Green Biotechnology Co., Ltd.

- Alvinesa Natural Ingredients

- Sabinsa Corporation

- Martin Bauer Group