Precision Nutrition Market Size

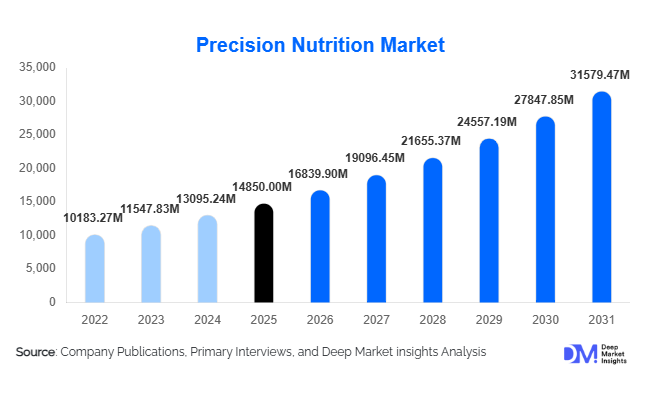

According to Deep Market Insights, the global precision nutrition market size was valued at USD 14,850 million in 2025 and is projected to grow from USD 16,839.90 million in 2026 to reach USD 31,579.47 million by 2031, expanding at a CAGR of 13.4% during the forecast period (2026–2031). The precision nutrition market growth is primarily driven by the rising prevalence of lifestyle-related diseases, growing adoption of genetic and microbiome testing, and increasing integration of AI-powered analytics into personalized dietary planning. As healthcare systems worldwide shift toward preventive and data-driven models, precision nutrition is emerging as a core pillar within digital health, functional nutrition, and personalized medicine ecosystems.

Key Market Insights

- Genetic testing-based nutrition solutions account for nearly 28% of global revenue, reflecting strong consumer acceptance of DNA-based dietary recommendations.

- Direct-to-consumer (DTC) subscription models dominate distribution, representing approximately 42% of total market revenue in 2025.

- North America leads the global market with 38% share, supported by advanced healthcare infrastructure and high digital health adoption.

- Asia-Pacific is the fastest-growing region, expanding at nearly 16% CAGR due to rising middle-class health awareness and genomics investments.

- Healthcare & clinical nutrition applications account for 30% of total demand, driven by chronic disease management programs.

- AI and machine learning integration is transforming personalization accuracy and enabling scalable subscription-based nutrition models.

What are the latest trends in the precision nutrition market?

Microbiome-Based Personalization Gaining Momentum

Microbiome sequencing and gut-health analytics are emerging as a major trend in precision nutrition. Consumers are increasingly seeking digestive health optimization, immunity enhancement, and metabolic support through microbiome-informed dietary interventions. Companies are expanding stool-based testing kits and integrating real-time gut flora analysis into subscription supplement programs. This trend is supported by growing clinical evidence linking microbiome diversity with obesity, diabetes, and inflammatory disorders. As sequencing costs decline and metagenomics technology becomes more accessible, microbiome-based nutrition solutions are transitioning from niche applications to mainstream wellness offerings.

AI-Integrated Adaptive Nutrition Platforms

Artificial intelligence-driven platforms capable of integrating genomics, wearable data, biomarker testing, and lifestyle inputs are reshaping consumer engagement. Rather than static diet reports, platforms now provide dynamic, adaptive meal planning based on continuous glucose monitoring, sleep patterns, and activity tracking. Cloud-based analytics dashboards are increasingly used by clinicians and corporate wellness providers to monitor patient outcomes. This shift toward predictive, real-time nutrition modeling is enhancing personalization accuracy and improving long-term adherence, particularly among tech-savvy consumers and performance-focused users.

What are the key drivers in the precision nutrition market?

Rising Burden of Chronic Diseases

The global increase in obesity, diabetes, and cardiovascular disorders is accelerating demand for individualized dietary interventions. Precision nutrition enables targeted glycemic control, lipid management, and inflammation reduction, positioning it as a preventive healthcare solution. Governments and insurers are increasingly supporting preventive health programs, further driving market penetration.

Declining Costs of Genomic & Biomarker Testing

Advancements in DNA sequencing and metabolomics have reduced testing costs by nearly 30–40% over the past decade. Lower entry barriers are encouraging mass-market adoption, particularly in North America, Europe, and emerging Asia-Pacific economies.

What are the restraints for the global market?

High Cost of Advanced Testing Panels

Despite declining sequencing costs, comprehensive genomic, metabolomic, and microbiome panels remain expensive for middle-income populations. Premium subscription pricing can restrict widespread adoption in developing markets.

Regulatory & Data Privacy Challenges

Handling sensitive genetic and health data presents compliance challenges under global frameworks such as GDPR and HIPAA. Regulatory inconsistencies across regions can delay product approvals and limit cross-border service expansion.

What are the key opportunities in the precision nutrition industry?

Integration into National Preventive Healthcare Programs

Governments aiming to reduce long-term healthcare expenditures are increasingly investing in preventive health strategies. Precision nutrition solutions integrated into public health screening programs and chronic disease management frameworks present a scalable growth opportunity. Partnerships with insurers and public health agencies can accelerate adoption across aging populations.

Expansion into Corporate Wellness & Performance Nutrition

Employers are investing in employee wellness programs to reduce healthcare costs and improve productivity. Precision nutrition platforms offering biomarker-based dietary planning and metabolic tracking are gaining traction in corporate environments. Similarly, sports performance nutrition is expanding rapidly, with elite athletes and fitness-conscious consumers adopting personalized supplementation for endurance, recovery, and performance optimization.

Product Type Insights

Genetic testing-based nutrition solutions continue to lead the precision nutrition market, accounting for approximately 28% share of 2025 revenue. The dominance of this segment is primarily driven by increasing consumer trust in DNA-driven dietary recommendations and the growing clinical validation of nutrigenomics. Consumers are increasingly seeking long-term, data-backed personalization rather than generalized diet plans, which positions genetic testing as the foundational entry point into precision nutrition programs. The declining cost of genomic sequencing and the widespread availability of at-home DNA kits have further accelerated adoption across North America and Europe. Additionally, healthcare providers are increasingly incorporating genetic insights into chronic disease management plans, reinforcing demand.

Personalized dietary supplements account for nearly 25% market share, benefiting significantly from subscription-based recurring revenue models and attractive profit margins ranging between 20–35%. The ability to tailor micronutrient blends based on individual biomarkers enhances perceived efficacy, driving customer retention. Microbiome-based solutions represent the fastest-growing product category, fueled by rising global awareness of gut health, immunity, and metabolic function. Continuous research linking gut microbiota diversity to obesity, diabetes, and inflammatory disorders is further strengthening this segment. Meanwhile, wearable-integrated nutrition analytics is emerging as a high-growth niche, particularly among sports professionals and fitness-conscious consumers who demand real-time metabolic feedback.

Technology Platform Insights

AI and machine learning platforms account for around 24% of the total market, serving as the core enabler of scalable personalization. The leading driver for this segment is the growing integration of multi-source health data, including genomics, continuous glucose monitoring, sleep patterns, and activity tracking, into predictive dietary models. AI-powered adaptive meal planning is increasingly replacing static nutrition reports, offering dynamic recommendations that evolve with real-time data inputs.

Genomics and DNA sequencing technologies remain foundational, particularly in clinical and hospital-based applications where long-term disease risk profiling is critical. Cloud-based health data platforms are expanding rapidly, supporting interoperability across wearable devices, healthcare systems, and corporate wellness dashboards. Biomarker and metabolomics testing is gaining clinical traction, especially for managing diabetes, cardiovascular disorders, and hormonal imbalances. The expansion of precision diagnostics infrastructure globally is reinforcing demand for these platforms.

Delivery Model Insights

Direct-to-consumer (DTC) subscription models dominate the market with approximately 42% market share. The primary growth driver for this segment is consumer preference for convenience, digital onboarding, and home-based testing kits. DTC platforms reduce dependency on clinical visits while enabling scalable global distribution through e-commerce channels. Personalized supplement refills, digital dashboards, and subscription-based meal planning services strengthen customer lifetime value.

Clinical and healthcare-provider-based models represent roughly 30% share, driven by integration into chronic disease management programs and preventive healthcare frameworks. Hospitals and specialized clinics increasingly recommend precision nutrition as part of metabolic disorder treatment plans. Corporate wellness programs and sports performance channels are the fastest-growing delivery segments, expanding at over 15% CAGR, supported by employer investments in workforce health optimization and the rising professionalization of athletic performance analytics.

End-Use Insights

Healthcare and clinical nutrition applications account for nearly 30% of total demand, valued at approximately USD 4,450 million in 2025. The leading driver for this segment is the global shift toward preventive healthcare and cost reduction in chronic disease treatment. Insurers and healthcare providers are increasingly recognizing personalized nutrition as a tool to reduce long-term hospitalization and medication costs.

Sports and performance nutrition is the fastest-growing end-use segment, expanding at nearly 15% CAGR. Increased professional sports participation, fitness culture expansion, and data-driven training methodologies are fueling demand for biomarker-guided supplementation. Weight management and preventive healthcare applications remain strong contributors, particularly among aging populations in developed economies where obesity and metabolic syndrome prevalence is high. Corporate wellness adoption is accelerating as multinational employers integrate metabolic health assessments and AI-based diet optimization programs into employee benefit structures.

| By Product Type | By Technology Platform | By Delivery Model | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 38% of the global market share, with the United States contributing over 85% of the regional revenue. The primary drivers of regional growth include advanced genomics infrastructure, strong venture capital investments in digital health startups, and high consumer awareness regarding preventive healthcare. The U.S. benefits from well-established nutraceutical manufacturing capabilities and strong adoption of wearable technologies. Canada is witnessing steady growth supported by public health digitization initiatives and increasing chronic disease prevalence.

Europe

Europe accounts for nearly 26% share, led by Germany, the UK, and France. Regional growth is driven by strict regulatory frameworks that enhance consumer trust, strong nutraceutical exports, and increasing public health emphasis on preventive strategies. Germany’s advanced functional food manufacturing base and the UK’s rapid digital health adoption are key contributors. Rising aging demographics across Western Europe are further increasing demand for personalized supplementation and metabolic monitoring solutions.

Asia-Pacific

Asia-Pacific represents around 22% of global revenue and is the fastest-growing region at nearly 16% CAGR. China and India are primary growth engines due to expanding middle-class populations, increasing health awareness, and government investments in biotechnology under national innovation programs. Japan and South Korea are also significant contributors, supported by aging populations and strong adoption of advanced health diagnostics. Rapid urbanization, rising disposable income, and increasing digital penetration are accelerating regional demand.

Latin America

Latin America contributes a roughly 7% share, led by Brazil and Mexico. Growth is primarily driven by rising wellness awareness, increasing dietary supplement consumption, and expanding e-commerce penetration. Urban populations are increasingly adopting preventive healthcare approaches, particularly for weight management and diabetes prevention. However, pricing sensitivity remains a moderating factor.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of global revenue. The UAE and Saudi Arabia are emerging high-value markets due to rising lifestyle disease prevalence, strong consumer spending power, and government-led healthcare modernization initiatives. In Africa, South Africa leads regional adoption, supported by expanding private healthcare networks. Regional growth is increasingly influenced by government initiatives aimed at reducing obesity and diabetes prevalence, creating long-term demand for precision nutrition solutions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Precision Nutrition Market

- Nestlé Health Science

- DSM-Firmenich

- Amway

- Herbalife Nutrition

- Viome Life Sciences

- 23andMe

- Nutrigenomix

- Care/of

- DayTwo

- InsideTracker

- Baze

- Persona Nutrition

- Thorne HealthTech

- GX Sciences

- Habit Food Personalized