Precision Fermentation Market Size

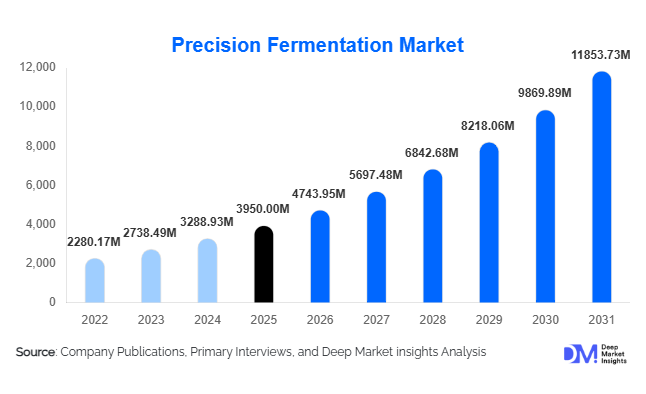

According to Deep Market Insights, the global precision fermentation market size was valued at USD 3,950 million in 2025 and is projected to grow from USD 4,743.95 million in 2026 to reach USD 11,853.73 million by 2031, expanding at a CAGR of 20.1% during the forecast period (2026–2031). The precision fermentation market growth is primarily driven by increasing demand for sustainable proteins, rapid advancements in synthetic biology, and expanding applications across food, pharmaceuticals, and specialty chemicals. Precision fermentation enables the production of specific functional molecules, such as dairy proteins, enzymes, collagen, and bioactive compounds, through engineered microorganisms, offering scalable and environmentally efficient alternatives to conventional manufacturing methods.

Key Market Insights

- Proteins represent the largest product segment, accounting for approximately 42% of global revenue in 2025, driven by dairy alternatives and egg protein analogues.

- Food & beverage applications dominate, contributing nearly 46% of total demand, particularly in plant-based dairy and functional beverages.

- North America leads the global market with around 38% share in 2025, supported by strong biotech infrastructure and venture capital funding.

- Asia-Pacific is the fastest-growing region, expanding at over 23% CAGR due to government-backed biomanufacturing initiatives in China, India, and Singapore.

- Large-scale industrial fermentation (>100,000L) is expanding rapidly as companies transition from pilot to commercial-scale operations.

- The top five companies collectively account for nearly 48% of the global market share, indicating moderate market concentration with increasing strategic partnerships.

What are the latest trends in the precision fermentation market?

Commercial-Scale Biomanufacturing Expansion

The market is transitioning from pilot-scale to industrial-scale production. Companies are investing heavily in fermentation facilities exceeding 100,000 liters to achieve economies of scale and price parity with conventional ingredients. Modular biomanufacturing plants are emerging in the U.S., Germany, China, and Singapore, supported by public-private funding. This trend is reducing per-unit production costs and accelerating B2B supply agreements with multinational food and pharmaceutical companies.

AI-Driven Strain Optimization and Synthetic Biology Integration

Artificial intelligence and machine learning tools are being deployed to optimize microbial strains and metabolic pathways. These technologies shorten development cycles, improve yield efficiency, and reduce raw material consumption. AI-enabled bioprocess monitoring and digital twin fermentation models are improving consistency and scalability, enhancing investor confidence in commercial deployment. Integration of CRISPR-based gene editing and automated fermentation platforms is further strengthening the technological foundation of the industry.

What are the key drivers in the precision fermentation market?

Rising Demand for Sustainable and Animal-Free Proteins

Global consumers are increasingly seeking sustainable, ethical, and climate-friendly food products. Precision fermentation-derived dairy proteins, egg substitutes, and specialty fats offer significantly lower greenhouse gas emissions compared to livestock agriculture. This environmental advantage is encouraging multinational food brands to incorporate fermentation-based ingredients into mainstream product lines.

Growth in Biopharmaceutical Manufacturing

The expansion of biosimilars, insulin analogues, monoclonal antibodies, and therapeutic proteins is driving demand for microbial fermentation platforms. Precision fermentation enables high-purity protein expression with scalable manufacturing capabilities, making it essential for pharmaceutical supply chains.

What are the restraints for the global market?

High Capital Expenditure Requirements

Industrial-scale fermentation infrastructure requires substantial upfront investment in bioreactors, purification systems, and downstream processing equipment. This limits entry for smaller startups and increases dependency on venture funding or strategic partnerships.

Regulatory and Labeling Uncertainty

Regulatory frameworks for novel fermented ingredients vary significantly across regions. Approval delays, labeling disputes, and evolving safety standards can slow the commercialization and international trade of precision fermentation products.

What are the key opportunities in the precision fermentation industry?

Government-Backed Biomanufacturing Hubs

Countries such as Singapore, Germany, the United States, and China are investing in fermentation infrastructure to enhance food security and biotechnology leadership. Public grants, tax incentives, and innovation clusters provide favorable conditions for startups and multinational ingredient producers.

Expansion into Cosmetics and Specialty Ingredients

Precision-fermented collagen, elastin, and bioactive peptides are gaining traction in premium cosmetic formulations. The global cosmetics ingredient industry is expanding steadily, creating new high-margin applications for fermentation-derived biomolecules.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3950 Million |

| Market Size in 2026 | USD 4743.95 Million |

| Market Size in 2031 | USD 11853.73 Million |

| CAGR | 20.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Proteins lead the precision fermentation market, accounting for approximately 42% of total revenue in 2025, primarily driven by the rapid commercialization of animal-free dairy proteins such as whey and casein. These proteins are increasingly used in alternative cheeses, yogurts, ice creams, and ready-to-drink protein beverages, where functional parity with conventional dairy is critical. The leading position of proteins is supported by three major drivers: rising consumer demand for sustainable and animal-free nutrition, expanding retail penetration of plant-based products, and strategic partnerships between biotechnology firms and multinational food manufacturers. In addition, improved strain engineering and higher protein expression yields have significantly reduced production costs, accelerating adoption.

Enzymes represent the second-largest segment, benefiting from well-established industrial demand across food processing, brewing, detergents, and textile manufacturing. Precision fermentation enhances enzyme specificity and production efficiency, making it attractive for high-performance industrial applications. Lipids and specialty fats, including omega-3 oils, human milk fat analogues, and cocoa butter equivalents, are emerging as high-growth segments due to demand in infant nutrition, confectionery, and functional foods. Functional ingredients such as vitamins, bioactive peptides, flavors, and specialty sweeteners are also expanding steadily, supported by clean-label trends and the growing nutraceutical market.

Application Insights

Food & beverage applications dominate the market with nearly 46% share in 2025, driven by rising demand for plant-based dairy, egg substitutes, and functional nutrition products. The leading position of this segment is attributed to consumer preference shifts toward climate-friendly diets, corporate ESG commitments, and strong retail distribution of alternative protein brands. The ability of precision fermentation to replicate taste, texture, and nutritional profiles of animal-derived ingredients has accelerated mainstream adoption.

Pharmaceutical applications represent a high-margin segment, supported by expanding biosimilar pipelines and increasing demand for recombinant proteins such as insulin and growth factors. Precision fermentation enables high-purity, scalable biologics production, making it essential to biopharma supply chains. Animal nutrition and pet food are emerging as fast-growing applications, where fermentation-derived proteins offer improved digestibility and reduced environmental footprint compared to conventional feed proteins. Cosmetics and personal care are also expanding, particularly for collagen, elastin, and specialty bioactives used in premium skincare formulations.

Fermentation Scale Insights

Large-scale industrial fermentation (>100,000 liters) holds approximately 41% of total revenue in 2025, reflecting the industry’s transition from pilot to commercial production. The primary growth driver for this segment is the pursuit of cost competitiveness and economies of scale. As demand from multinational food and pharmaceutical companies increases, manufacturers are investing in high-capacity bioreactors and downstream purification systems to secure long-term supply contracts. Public-private partnerships and government-supported fermentation hubs are further accelerating industrial-scale capacity expansion.

Commercial-scale facilities below 100,000 liters support mid-sized ingredient production and regional supply chains, while laboratory and pilot-scale operations remain critical for R&D, strain optimization, and early-stage commercialization. The continued decline in bioreactor and automation costs is expected to further expand large-scale capacity over the forecast period.

End-Use Industry Insights

Alternative protein manufacturers represent around 44% of total market demand in 2025, making them the leading end-use segment. Growth is fueled by aggressive product launches in dairy alternatives, egg replacements, and hybrid plant-animal protein blends. Retail expansion and increasing consumer acceptance of fermentation-derived ingredients are reinforcing this dominance.

Biopharmaceutical companies constitute a significant share due to high-value therapeutic protein production. Traditional food processors are increasingly incorporating precision fermentation ingredients into existing product lines to enhance nutritional profiles and sustainability positioning. Cosmetic ingredient manufacturers are also expanding adoption of fermentation-derived collagen and bioactives, driven by premium skincare demand and clean-label trends.

Explore more data points, trends and opportunities Download Free Sample Report

Precision Fermentation Market Segmentations

By Product Type

- Proteins

- Enzymes

- Lipids & Specialty Fats

- Functional Ingredients

- Biopharmaceutical Proteins

By Application

- Food & Beverages

- Pharmaceuticals & Biologics

- Animal Nutrition & Pet Food

- Cosmetics & Personal Care

- Industrial & Chemical Processing

By Fermentation Scale

- Laboratory & Pilot Scale

- Commercial Scale (<100,000 Liters)

- Large-Scale Industrial (>100,000 Liters)

By End-Use Industry

- Alternative Protein Manufacturers

- Biopharmaceutical Companies

- Traditional Food Processors

- Cosmetic Ingredient Manufacturers

- Specialty Chemical Producers

Regional Insights

North America

North America leads the global market with approximately 38% share in 2025, with the United States representing the largest individual country market. Regional growth is driven by strong venture capital investment, advanced synthetic biology research ecosystems, and early regulatory clarity for novel ingredients. The presence of established biotechnology firms, contract manufacturing organizations, and food innovation hubs accelerates commercialization. In addition, rising consumer demand for plant-based foods and sustainable nutrition continues to drive large-scale capacity expansion across the U.S. and Canada.

Europe

Europe accounts for nearly 29% of the global market, led by Germany, the United Kingdom, France, and the Netherlands. Growth in the region is strongly supported by sustainability-focused policies, carbon reduction commitments, and increasing investments in alternative protein research. The European Union’s emphasis on food security and environmental impact reduction is accelerating the adoption of fermentation-based ingredients. Robust academic-industry collaborations and innovation clusters further strengthen the region’s competitive position.

Asia-Pacific

Asia-Pacific holds approximately 24% market share and is the fastest-growing region, expanding at over 23% CAGR. China and India are investing heavily in fermentation parks and domestic biomanufacturing capabilities to reduce import dependency and enhance food security. Singapore has emerged as a regulatory innovation hub, providing clear approval pathways and funding incentives for novel food technologies. Rising middle-class protein consumption, expanding pharmaceutical manufacturing capacity, and government-backed industrial biotechnology initiatives are key drivers of regional growth.

Latin America

Latin America contributes around 4% of global demand, with Brazil and Argentina leading regional adoption. Growth drivers include the expansion of animal feed and export-oriented agribusiness sectors seeking sustainable protein alternatives. Increasing investment in biotechnology research and collaboration with North American and European firms is expected to gradually strengthen regional capacity.

Middle East & Africa

The Middle East & Africa account for approximately 5% of the global market. Israel leads in food-tech innovation and startup activity, particularly in alternative dairy proteins. The United Arab Emirates and Saudi Arabia are investing in food security and domestic biotechnology infrastructure to reduce reliance on imports. In Africa, growing interest in sustainable protein solutions and in the development of industrial biotechnology is expected to support long-term market expansion.